(1) Overview of the Semiconductor Materials Industry

Semiconductor materials are a crucial support segment of the entire semiconductor industry, primarily providing essential wafer manufacturing materials and packaging materials for the production of semiconductor products, with the highest proportion and technical difficulty in the integrated circuit field.

The packaging materials mainly include: packaging substrates, lead frames, bonding wires, packaging materials, ceramic substrates, and chip adhesive materials. Among these, the cost of packaging substrates accounts for a significant proportion in chip packaging, approximately 40%-50% in WB packaging, and can be as high as 70%-80% in FC packaging. The market size of packaging substrates holds the highest share in the packaging materials market.

In the entire electronic information industry, semiconductor materials have immense added value and a unique industrial ecological support role. The self-sufficiency of semiconductor materials is crucial for the ecological safety of the entire electronic information industry, and semiconductor materials are key to driving advancements in semiconductor technology. The company primarily provides packaging materials to the integrated circuit field.

(2) Global Development Status of the Semiconductor Materials Industry

① The semiconductor materials industry is experiencing stable growth, with process development and wafer expansion stimulating further demand for materials.

According to the latest data from SEMI, the global semiconductor materials market sales are projected to reach $72 billion in 2024, an increase of 7.95% year-on-year. Among these, wafer manufacturing materials will account for $42.1 billion, and packaging materials will account for $29.9 billion, with year-on-year increases of 9.4% and 6.0%, respectively. The increase in the wafer manufacturing materials market is mainly influenced by the rising demand for silicon wafers, expansion of advanced processes, and the increase in the number of 3D NAND layers; while the growth in the packaging materials market is primarily driven by the increasing demand for organic substrates, a relative recovery in the lead frame and bonding wire markets, and the rising penetration of advanced packaging.

Data Source: SEMI, Wind, Sihan

With the recovery of global consumer electronics demand, driven by emerging application fields such as automotive electronics, wearable devices, the Internet of Things, and artificial intelligence, as well as the concentrated release of new wafer production capacity, the global semiconductor materials market is expected to maintain a growth trend. Additionally, upgrades in semiconductor technology will drive the iteration of semiconductor materials and the expansion of market size, with more precise advanced processes, higher integration levels, and more process steps leading to increased material value and usage.

② The global semiconductor materials industry is mainly dominated by overseas companies, with a high concentration in the industry.

The high technical barriers, purity requirements, numerous sub-sectors, complex processes, and long verification cycles of semiconductor materials have resulted in most of the semiconductor materials field being in an oligopolistic situation. The global semiconductor materials industry is primarily dominated by countries such as Japan, the United States, South Korea, and Germany, holding a monopolistic position in the mid-to-high-end product sector, while China’s overall self-sufficiency rate remains low.

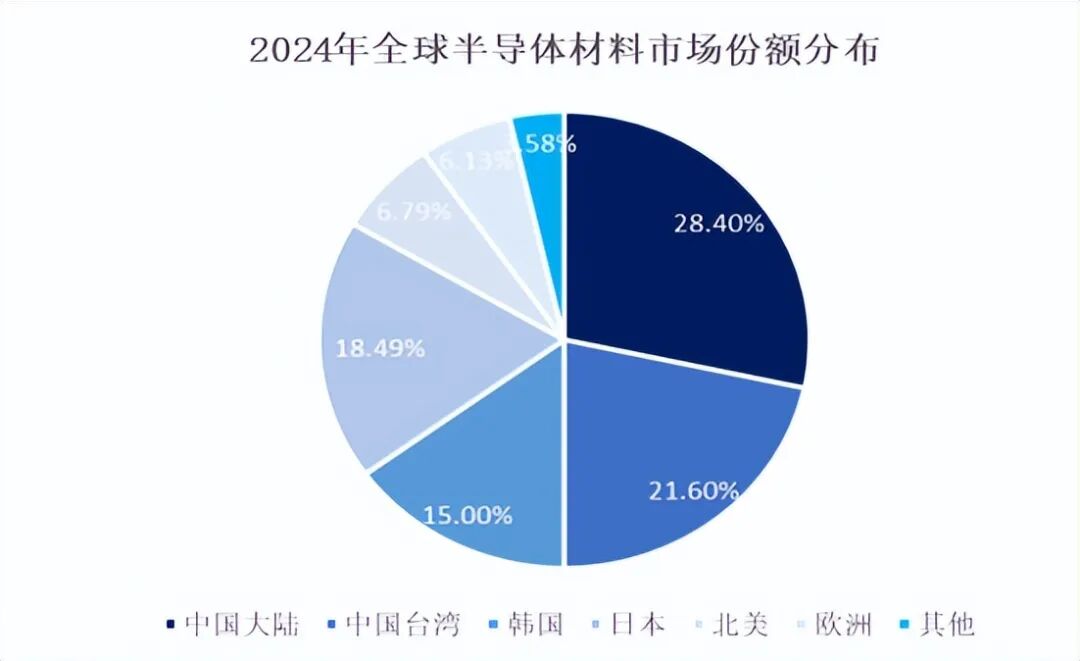

③ The global semiconductor materials consumption market is concentrated in the East Asian market.

From the demand side, the current semiconductor materials consumption market is mainly concentrated in the East Asia region, with Taiwan, mainland China, South Korea, and Japan collectively accounting for 83.49% of the global semiconductor materials consumption market share in 2024. Among these, mainland China ranks first, with semiconductor materials market revenue reaching $20.5 billion.

Data Source: SEMI

(3) Trends in the Development of China’s Semiconductor Materials Industry

① The market size of China’s semiconductor materials is steadily growing, with a growth rate higher than the global average.

In 2024, the revenue of China’s mainland semiconductor materials market is expected to reach $20.5 billion, with a compound annual growth rate of 11.18% from 2010 to 2024, significantly higher than the global semiconductor materials growth rate during the same period. The further increase in global semiconductor materials demand, the continued transfer of the global semiconductor industry to mainland China, and domestic manufacturers’ considerations for supply chain security will all drive further expansion of domestic semiconductor materials demand.

Data Source: SEMI, Sihan

② Development started relatively late, and the degree of localization urgently needs to be improved.

China’s semiconductor materials industry mainly started in the 1990s, developing relatively late, with technology and production experience lagging behind the semiconductor industries of Europe, the United States, Japan, South Korea, and Taiwan. Therefore, the overall localization of semiconductor materials in China remains at a low level, with self-sufficiency rates generally not high across various sub-sectors, making it difficult to break the technological blockade by overseas manufacturers, especially in the mid-to-high-end sector, in a short time.

In terms of packaging materials, although local manufacturers have made some breakthroughs in recent years, high-end products such as packaging substrates and high-end bonding wires still heavily rely on imports, indicating significant room for improvement in localization.

For more industry research and analysis, please refer to the official website of Sihan Industrial Research Institute, which also provides industry research reports, feasibility reports (project approval, bank loans, investment decisions, group meetings), industrial planning, park planning, business plans (equity financing, investment promotion, internal decision-making), special research, architectural design, and overseas investment reports and other related consulting service solutions.

About Us

About Us  Sihan Industrial Research InstituteChinasihan.comLeader in Chinese Industrial ResearchInnovation City of the FutureCustomized contact information for report orders: · Contact Number:4008087939 0755-28709360· Customer Service WeChat:g15361035605 · Customer Service QQ:454058156· Email:chinasihan@126.com

Sihan Industrial Research InstituteChinasihan.comLeader in Chinese Industrial ResearchInnovation City of the FutureCustomized contact information for report orders: · Contact Number:4008087939 0755-28709360· Customer Service WeChat:g15361035605 · Customer Service QQ:454058156· Email:chinasihan@126.com

· Official Website: Chinasihan.com