1. Company Development History

Founded in December 2004, initially focused on the research, production, and sales of optoelectronic film devices and window lenses.

In 2014, the company initiated a business transformation, focusing on key materials in the integrated circuit field.

In May 2015, it was listed on the National SME Share Transfer System, and in May 2021, it completed the delisting.

In 2017, imported photoresist materials and precursor materials were validated by mainstream domestic 12-inch wafer fabs and achieved regular supply.

In 2020, self-produced photoresist materials and precursor materials began mass production, and the subsidiary Fujian Hongguang commenced production; the same year, it undertook a national major science and technology project sub-topic.

In 2022, sales revenue from self-produced products exceeded 100 million yuan, and it gradually obtained national-level qualifications such as “Specialized, Refined, Unique, and Innovative” and “Little Giant”.

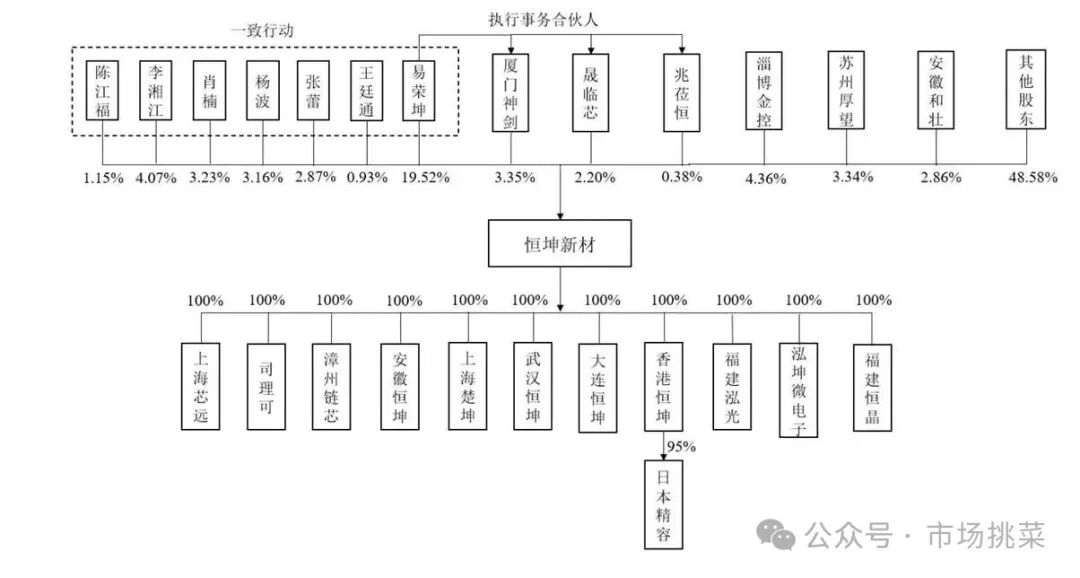

2. Shareholding Structure and Background of Actual Controller

1. Shareholding Structure

Total share capital before issuance is 381.92166 million yuan, with actual controller Yi Rongkun controlling a total of 40.87% of voting rights (directly held 19.52% + indirectly controlled 5.94% + concerted action control 15.41%).

2. Background of Actual Controller

Yi Rongkun, born in June 1971, holds a bachelor’s degree. He has a background in industry.Since 1999, he has served as the executive director and general manager of Hengkun Industrial and Trade, general manager and supervisor of Hengkun Limited, and since January 2014, he has been the chairman of Hengkun New Materials, also serving as general manager since February 2017.

3. Executive and Personnel Structure

Chairman and General Manager: Yi Rongkun (fully responsible for company operations and management).

Directors and Deputy General Managers: Wang Tingtong, Xiao Nan (responsible for company operations and business development respectively).

There are a total of 4 core technical personnel, namely Xiao Nan (Director, Deputy General Manager), Song Liqian (Operations Director), Wang Jing (R&D Director, PhD in Organic Chemistry from the Changchun Institute of Applied Chemistry, Chinese Academy of Sciences), and Mao Hongchao (R&D Director, PhD in Organic Chemistry from the Changchun Institute of Applied Chemistry, Chinese Academy of Sciences). All core technical personnel have many years of experience in the integrated circuit or chemical materials field.

Honestly, the proportion of R&D personnel in this employee structure is not high, while there are many in management and operations.

4. Main Products

Mainly engaged in the research, production, and sales of photoresist materials and precursor materials. It is one of the few companies in the country capable of R&D and mass production of key materials for 12-inch integrated circuits, with self-produced photoresist sales ranking among the top in the domestic industry.

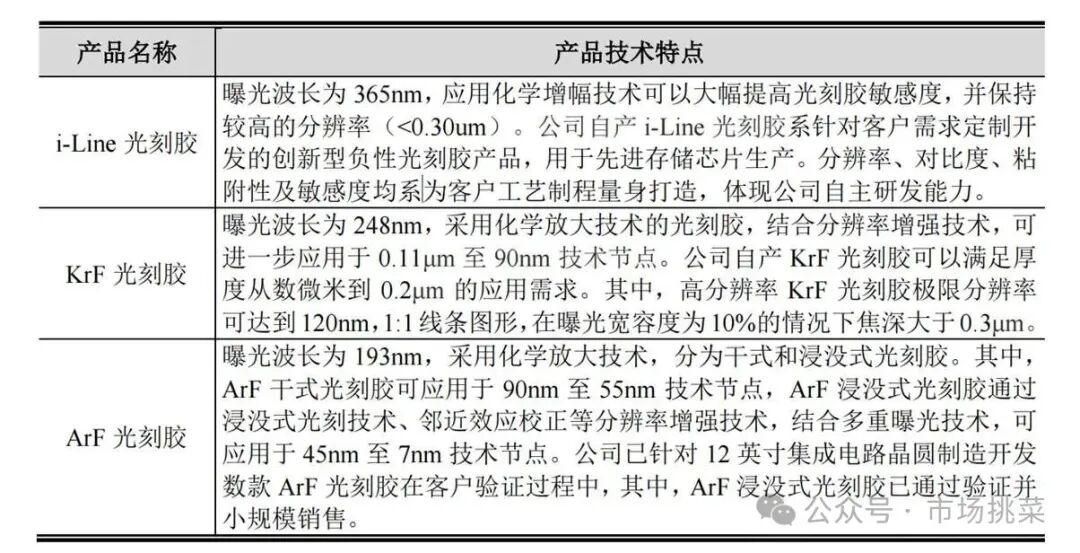

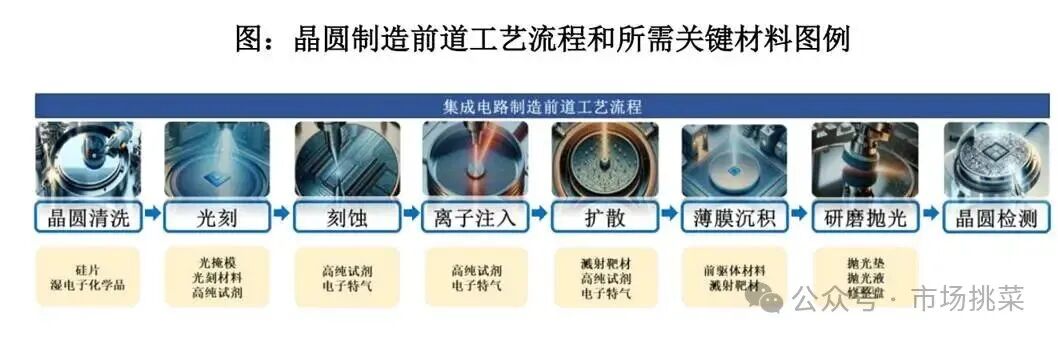

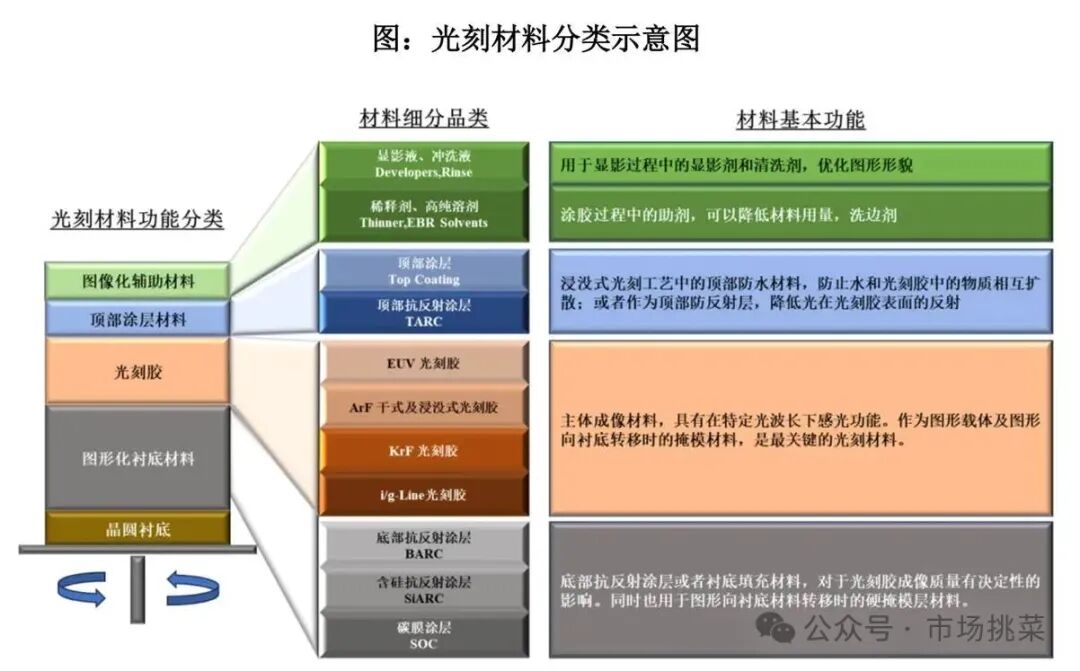

During the reporting period, the company’s self-produced products mainly include SOC, BARC, KrF photoresist, i-Line photoresist, and other photoresist materials, as well as TEOS and other precursor materials. The ArF immersion photoresist has been validated and is sold on a small scale, mainly used in advanced NAND, DRAM memory chips and in the photolithography, thin film deposition, and other process steps for the production of logic chips at the 90nm technology node and below.

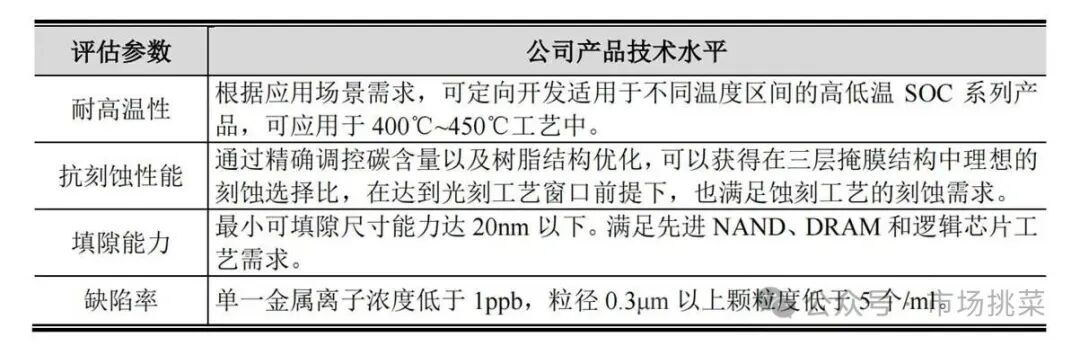

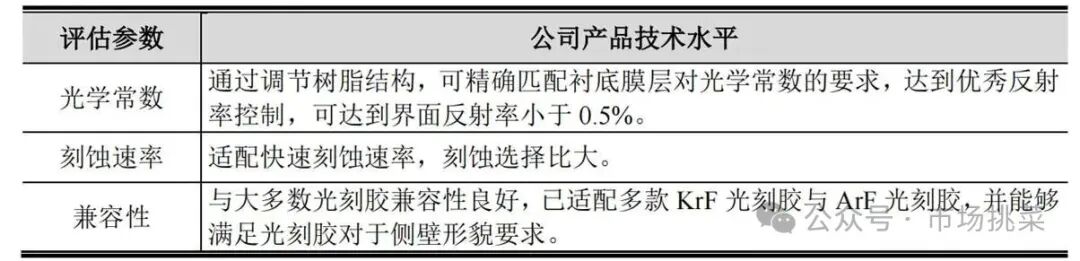

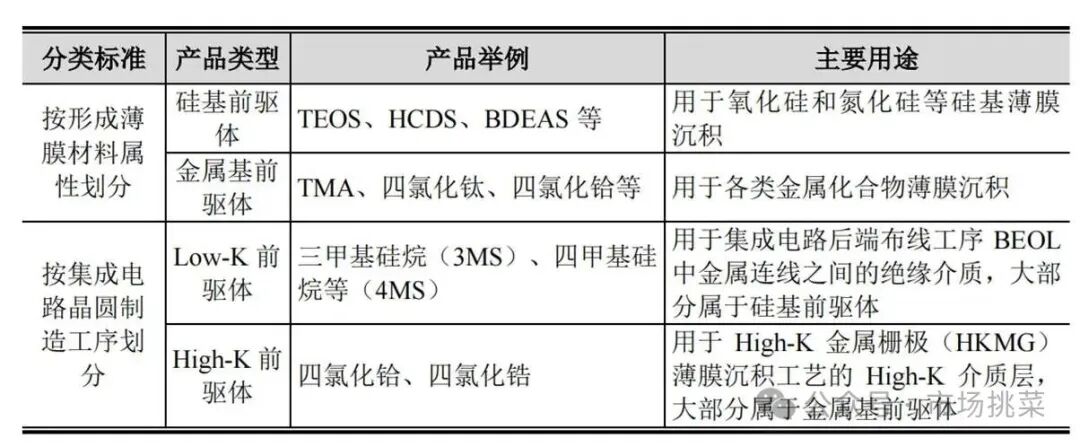

1. Photoresist Materials

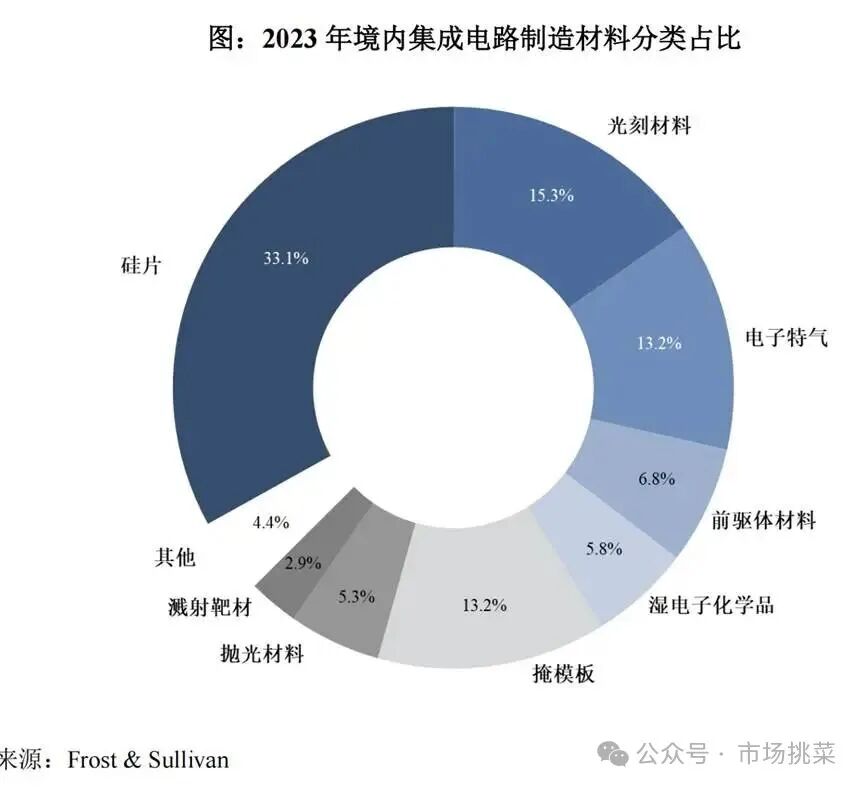

SOC (carbon film coating), BARC (bottom anti-reflective coating), i-Line/KrF photoresist (mass-produced), ArF immersion photoresist (small-scale sales), with sales revenue in 2024 reaching 29,998.67 million yuan, with both SOC and BARC sales revenue accounting for over 90% of the sales revenue of self-produced photoresist materials.

In the context of the domestic integrated circuit industry lacking EUV photolithography technology, the flexible application of SOC, BARC, and other photoresist materials combined with multiple exposure technology and immersion photolithography technology is a key solution for achieving breakthroughs in advanced technology nodes and process manufacturing.

SOC

BARC

The company has cumulatively mass-produced and supplied over 36,000 gallons of self-produced SOC and BARC, with the total number of mass-produced products exceeding 35 types, successfully replacing similar products from foreign manufacturers, breaking the monopoly of foreign manufacturers. Before the company’s mass production supply, domestic wafer fabs mainly sourced SOC and BARC from foreign manufacturers such as Shin-Etsu Chemical, Japan Synthetic Rubber, Nissan Chemical, and Brewer Science. The company is one of the few that has achieved mass production supply of SOC and BARC in the 12-inch integrated circuit field in China. According to Frost & Sullivan market research, in 2023, the company’s SOC and BARC sales scale ranked first among domestic manufacturers in the market.

Photoresist

The company has cumulatively mass-produced and supplied over 3,600 gallons of self-produced KrF photoresist and i-Line photoresist. In addition to the products already supplied in bulk, the company has more than 10 types of i-Line photoresist, KrF photoresist, and ArF photoresist entering the validation process, with some products already validated and sold on a small scale.

2. Precursor Materials

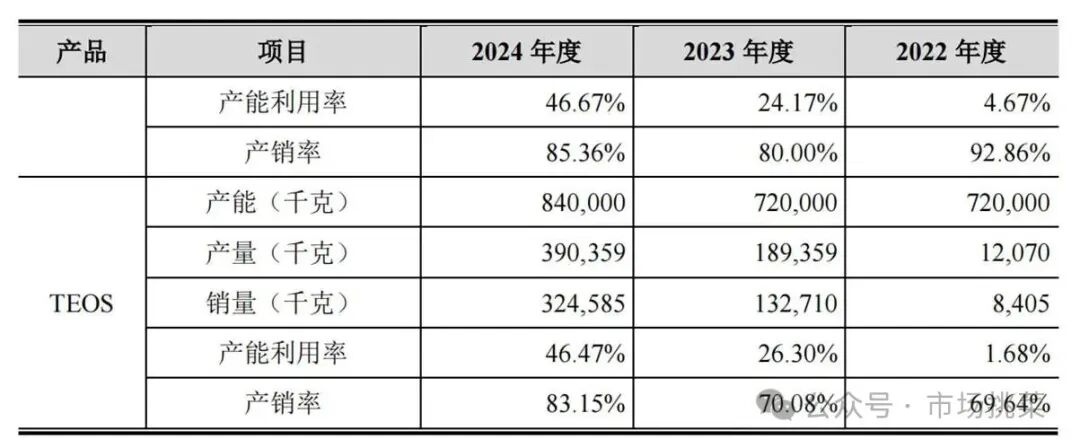

The company produces silicon-based precursor materials mainly based on TEOS. The company’s subsidiary Dalian Hengkun has introduced TEOS production management technology through cooperation with Soulbrain to achieve self-production, with product purity reaching 9N electronic grade requirements, and will gradually replace the TEOS introduced from Soulbrain at client sites in the future.

3. Introduced Products

Photoresist materials, precursor materials, electronic special gases, with sales revenue in 2024 reaching 19,556.25 million yuan, with gross profit margin declining year by year.

5. Core Competitiveness

Technical advantages: holding 89 patents (including 36 invention patents), undertaking national major science and technology projects such as the 02 project, with SOC and BARC products filling domestic gaps.

Localization advantages: product performance benchmarks against foreign manufacturers, achieving import substitution, with SOC and BARC sales ranking first among domestic manufacturers in the market in 2023.

Customer resource advantages: establishing stable cooperation with mainstream domestic wafer fabs, with some customers accumulating sales exceeding 100 million yuan, receiving awards such as “Value Creation Award” and “R&D Cooperation Award”.

Team advantages: R&D personnel account for 15.56%, with the core team possessing both wafer fab process experience and material R&D capabilities.

6. Industry Development and Market Position

1. Overall Market Size

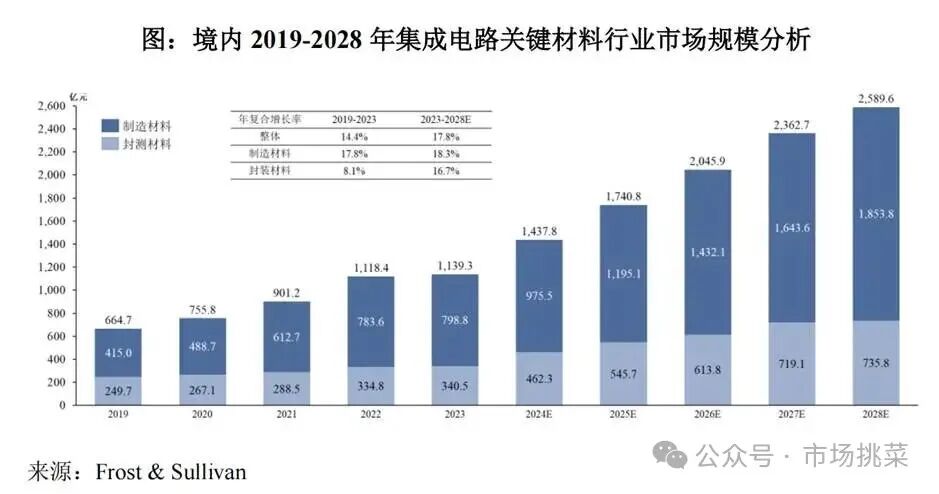

Key materials for integrated circuits are a strategic emerging industry, with the domestic market size reaching 1139.3 billion yuan in 2023, and is expected to reach 2589.6 billion yuan by 2028.

Domestic localization rates for photoresist materials and precursor materials are low (with the localization rate for ArF photoresist being less than 1%), indicating an urgent need for import substitution.

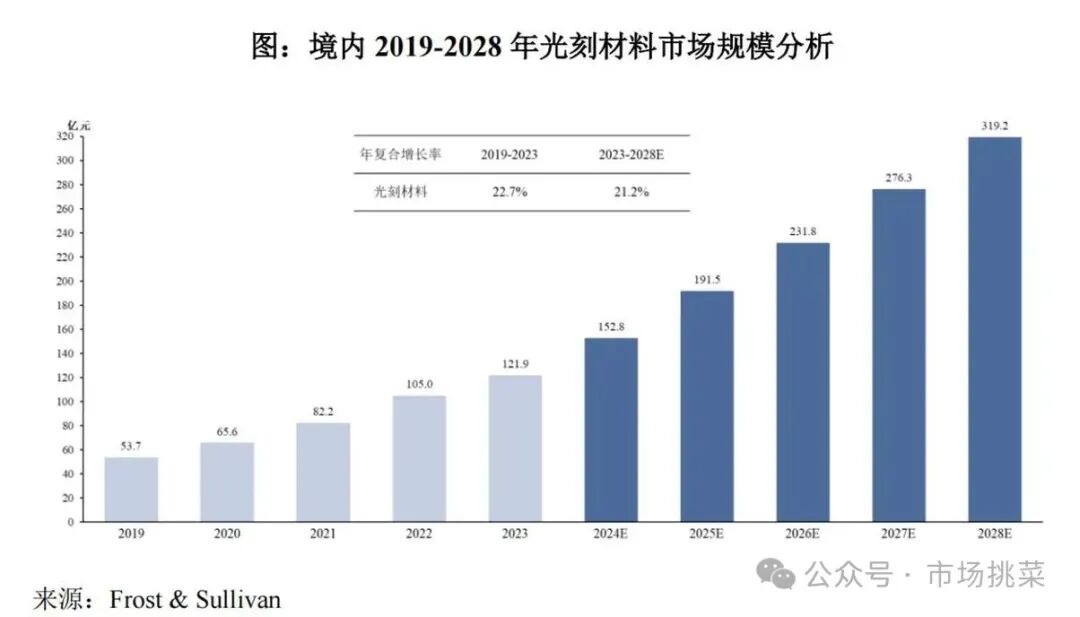

According to Frost & Sullivan market research, the overall market size for photoresist materials in China has grown from 5.37 billion yuan in 2019 to 12.19 billion yuan in 2023, with a compound annual growth rate of 22.7%, and is expected to grow to 31.92 billion yuan by 2028, with a compound annual growth rate of 21.2%.

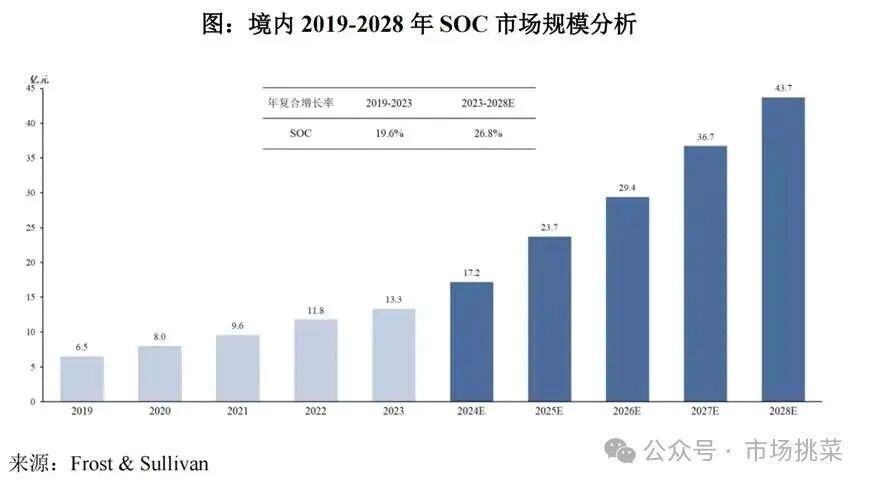

2. SOC Market

According to Frost & Sullivan market research, the domestic SOC market size has shown a continuous upward trend, growing from 650 million yuan in 2019 to 1.33 billion yuan in 2023, with a compound annual growth rate of 19.6%, and is expected to reach 4.37 billion yuan in 2028, with a compound annual growth rate of 26.8%. Therefore, it is expected that from 2023 to 2028, the domestic SOC annual compound growth rate will exceed the overall annual compound growth rate of photoresist materials, and the proportion of SOC in photoresist materials will continue to increase.

The company’s SOC sales scale reached 232.3634 million yuan, with an expected domestic market share exceeding 10%.

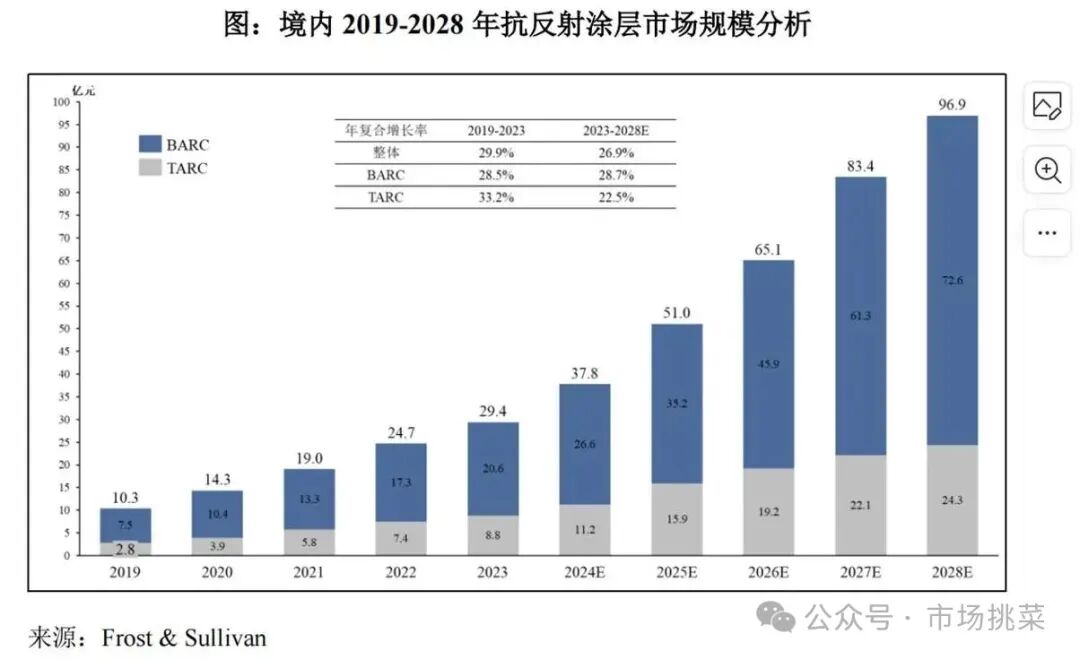

3. BARC Market

BARC accounts for over 70% of the anti-reflective coating market size. According to application scenarios and the types of photoresist used, BARC can be further divided into i-Line BARC, KrF BARC, ArF BARC, and iArF BARC types. It is expected that the market size for KrF photoresist and ArF immersion photoresist will further increase, corresponding to the market size for KrF BARC and iArF BARC growing simultaneously.

Globally, the main companies producing SOC and anti-reflective coatings include Japan Synthetic Rubber, Shin-Etsu Chemical, DuPont, Brewer Science, Merck, and PIBOND.

4. Photoresist

According to Frost & Sullivan market research, the localization rate of KrF photoresist is around 1-2%, while the localization rate of ArF photoresist is less than 1%, and the localization rate of i-Line photoresist is around 10%.

In addition to Hengkun New Materials, which has achieved mass production supply of i-Line photoresist and KrF photoresist, companies such as Nanda Optoelectronics, Beijing Kehua, Shanghai Xinyang, and Ruihong Suzhou also have semiconductor photoresist products in the validation or mass production supply process.In the fiscal year 2024, the company’s i-Line photoresist sales scale reached 7.1519 million yuan, while the sales scale of KrF photoresist reached 13.5231 million yuan.

5. Precursor Materials

Metal-based precursor materials are expected to see rapid growth in advanced process applications.

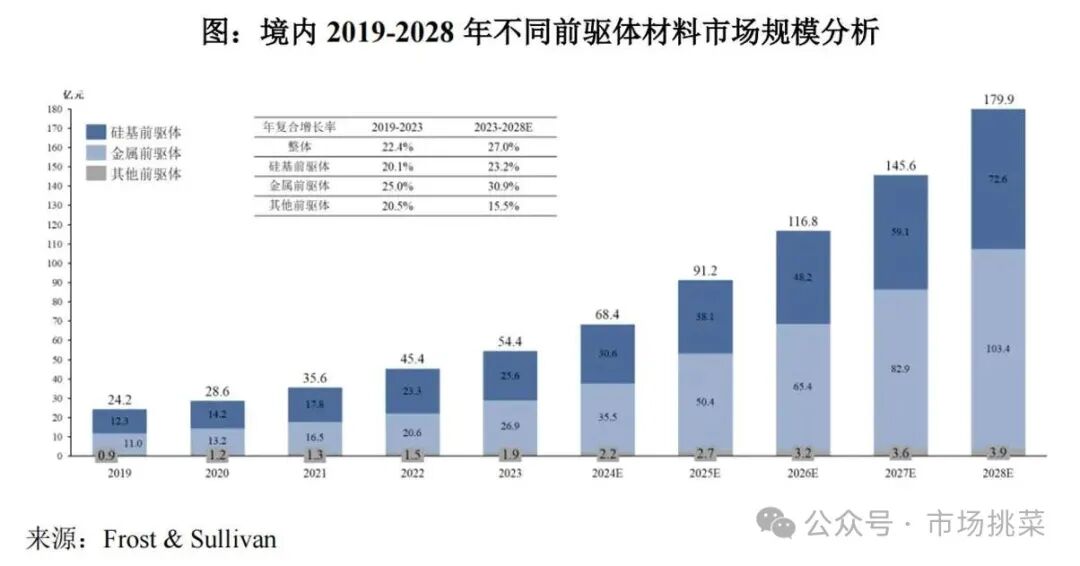

According to Frost & Sullivan market research, the domestic precursor materials market has grown from 2.42 billion yuan in 2019 to 5.44 billion yuan in 2023, with a compound annual growth rate of 22.4%, and is expected to reach 17.99 billion yuan by 2028, with a compound annual growth rate of 27.0%. Among them, silicon-based precursor materials are expected to grow from 2.56 billion yuan in 2023 to 7.26 billion yuan in 2028, with a compound annual growth rate of 23.2%, while metal-based precursor materials are expected to grow from approximately 2.69 billion yuan in 2023 to approximately 10.34 billion yuan in 2028, with a compound annual growth rate of 30.9%

7. Fundraising Projects and Expectations

This fundraising project plans to establish approximately 500 tons of KrF/ArF photoresist and other photoresist materials, and 760 tons of TEOS and other precursor materials production capacity.

To be honest, compared to other companies, the content in this prospectus is quite sloppy.

8. Major Risks

Operational: Termination of cooperation with SKMP affects short-term performance.

Customer dependency: The revenue from the top five customers accounts for 97.20% of the main business revenue, with sales to the largest customer accounting for 64.07%, indicating a significant dependency on them.

Import dependency: The main raw materials, production, and testing equipment or core components required for the company’s self-produced products still need to be imported.