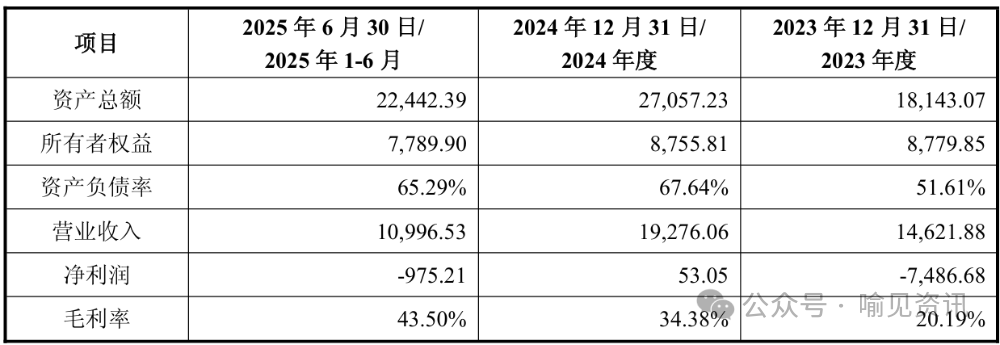

On November 16, 2025, Heshun Petroleum (603353.SH) announced its plan to acquire at least 34% equity in Kuixin Technology through a cash transaction not exceeding 540 million yuan, utilizing a “purchase of old shares + capital increase” method, and to control 51% of the voting rights of the target company through a voting right entrustment, thereby achieving consolidated control.01Transaction Plan: Four Key HighlightsThis cross-industry acquisition of Kuixin Technology by Heshun Petroleum adopts a composite structure of “cash acquisition + voting right entrustment + reverse equity binding”, showcasing multiple highlights that effectively balance core issues such as control acquisition, financial pressure, risk isolation, and benefit synergy.1. Transaction Structure: Low Proportion Equity + Voting Right EntrustmentHeshun Petroleum will acquire at least 34% equity in Kuixin Technology through the “purchase of old shares + capital increase” method, while obtaining 17% of the voting rights through voting right entrustment, totaling 51% control of the voting rights, thus achieving consolidation of the target company.The core advantage of this design lies in reducing financial pressure and achieving light asset control. The total valuation of Kuixin Technology’s 100% equity is not more than 1.588 billion yuan (after capital increase), and the transaction amount does not exceed 540 million yuan, which is only about 32% of Heshun Petroleum’s net assets at the end of 2024, avoiding the impact of large cash expenditures on cash flow.2. Step-by-Step Acquisition: First Control + Then Increase HoldingsThis transaction is not a “one-off deal” but is designed with a step-by-step acquisition framework.If Kuixin Technology achieves the cumulative performance for 2025-2026, or fails to achieve it but meets the cumulative performance for 2025-2027, Heshun Petroleum will further acquire 33% of its equity through “issuing shares + cash payment”.If it achieves the cumulative performance for 2025-2028, or meets other agreed performance commitments, Heshun Petroleum will acquire all remaining equity.This design’s value lies in risk stratification. By initially controlling with a small amount of cash, it allows observation of the target’s performance realization capability before deciding whether to increase holdings, thus avoiding the risk of excessive one-time investment and providing Kuixin Technology with a growth time window.3. Supporting Transactions: Actual Controller’s Shareholding + Phased UnlockingTo avoid the issue of “insufficient motivation of the target team post-acquisition”, this transaction has designed a two-way equity binding mechanism.The actual controller of Kuixin Technology, Chen Wanyi, will acquire 6% of Heshun Petroleum’s shares (a total of 10.314 million shares) at a price of 237 million yuan (22.93 yuan per share), becoming the major shareholder of the listed company.This portion of shares will adopt a “performance-linked phased unlocking” rule. The first phase unlocking (20%) requires achieving the cumulative performance commitment for 2025-2026; the second phase unlocking (40%) requires achieving the cumulative performance commitment for 2025-2027; the third phase unlocking (100%) requires achieving the cumulative performance commitment for 2025-2028 (or fulfilling all performance compensation obligations).This design deeply binds Chen Wanyi’s interests with the growth of Kuixin Technology, transforming him from a “seller” to a “stakeholder of the listed company”, while also compelling him to fulfill performance through unlocking conditions.4. Performance Commitment: Dual Indicators of Revenue + ProfitIn light of Kuixin Technology’s current unprofitable status, this transaction sets a strict performance commitment mechanism covering two core goals: revenue growth and profit normalization.From 2025 to 2028, Kuixin Technology’s revenue must not be less than 300 million yuan, 450 million yuan, 600 million yuan, and 750 million yuan respectively, with core IP and high-speed interconnect product revenues not less than 105 million yuan, 158 million yuan, 210 million yuan, and 263 million yuan respectively (to ensure the growth of core business).At the same time, the net profit attributable to the parent company must be positive for each year from 2025 to 2028. If the targets are not met, Chen Wanyi and other compensation obligors must compensate in cash.02Basic Information of Kuixin TechnologyKuixin Technology was established in August 2021 and is headquartered in Minhang District, Shanghai. The actual controller, Chen Wanyi, controls 81.4216% of the target company’s equity. The company is one of the few semiconductor enterprises in China with a complete high-speed interface IP product matrix, focusing on solving computing power expansion and high-speed interconnection issues. Its core business includes the R&D of high-speed interface IP (such as UCIe, HBM, LPDDR, PCIe, etc.), Chiplet solutions, and chip design services, with technology covering process nodes from 5nm to 55nm, and a cooperative network extending to well-known foundries such as TSMC and Samsung.

The company is one of the few semiconductor enterprises in China with a complete high-speed interface IP product matrix, focusing on solving computing power expansion and high-speed interconnection issues. Its core business includes the R&D of high-speed interface IP (such as UCIe, HBM, LPDDR, PCIe, etc.), Chiplet solutions, and chip design services, with technology covering process nodes from 5nm to 55nm, and a cooperative network extending to well-known foundries such as TSMC and Samsung. The company has not yet achieved profitability, with a net profit of -74.8668 million yuan in 2023, a net profit of 530,500 yuan in 2024, and a loss of -9.7521 million yuan in the first half of 2025.03Basic Information of Heshun PetroleumHeshun Petroleum (603353.SH) was established in July 2005 and is headquartered in Changsha. The company focuses on the finished oil circulation field, constructing a complete industrial chain ecosystem of “gas station retail chain + finished oil storage + logistics distribution + wholesale”, with business coverage in Hunan and surrounding provinces.As a traditional energy enterprise, Heshun Petroleum has faced challenges from new energy in recent years, leading to a continuous decline in performance. In the first three quarters of 2025, the company’s total operating revenue was 2.126 billion yuan, a slight decrease of 0.13% year-on-year; the net profit attributable to shareholders of the listed company was 21.8062 million yuan, a year-on-year decrease of 49.44%.

The company has not yet achieved profitability, with a net profit of -74.8668 million yuan in 2023, a net profit of 530,500 yuan in 2024, and a loss of -9.7521 million yuan in the first half of 2025.03Basic Information of Heshun PetroleumHeshun Petroleum (603353.SH) was established in July 2005 and is headquartered in Changsha. The company focuses on the finished oil circulation field, constructing a complete industrial chain ecosystem of “gas station retail chain + finished oil storage + logistics distribution + wholesale”, with business coverage in Hunan and surrounding provinces.As a traditional energy enterprise, Heshun Petroleum has faced challenges from new energy in recent years, leading to a continuous decline in performance. In the first three quarters of 2025, the company’s total operating revenue was 2.126 billion yuan, a slight decrease of 0.13% year-on-year; the net profit attributable to shareholders of the listed company was 21.8062 million yuan, a year-on-year decrease of 49.44%. Previous Selections:Observation of the Capital Market’s “Agreement Transfer + Acquisition” ModelAnalysis of Cross-Industry Acquisition Cases After Six Merger RulesAnalysis of Acquisition Cases of Unprofitable Enterprises After Six Merger Rules

Previous Selections:Observation of the Capital Market’s “Agreement Transfer + Acquisition” ModelAnalysis of Cross-Industry Acquisition Cases After Six Merger RulesAnalysis of Acquisition Cases of Unprofitable Enterprises After Six Merger Rules