Wu Ni | Author

You Yi | Editor

In October, Hansoh Pharmaceutical licensed the overseas rights of its self-developed ADC drug targeting CDH17 to Roche. This gastrointestinal tumor target was also a hot topic at this year’s AACR conference, where over ten related ADC drugs were showcased, with nine from Chinese pharmaceutical companies.

Industry insiders joke, “Toxicology experiments generally require 10 experimental monkeys, which means over 100 monkeys in China have died in trials for the same target.”

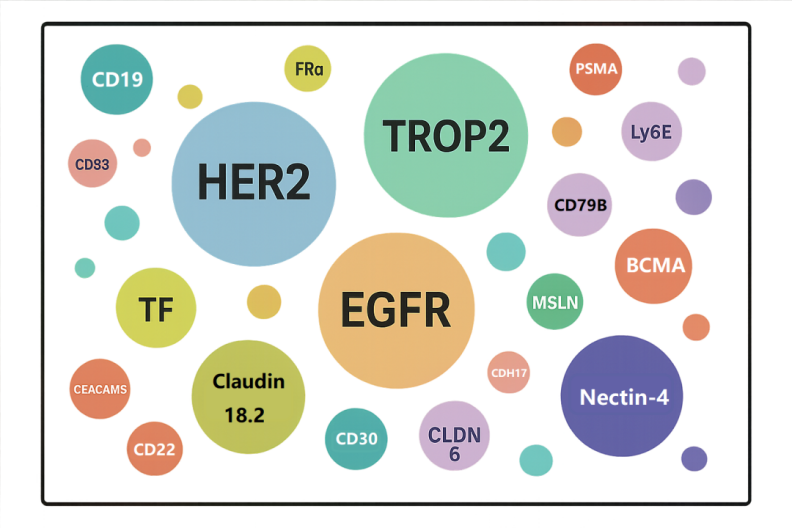

Among the popular ADC targets, CDH17 does not even rank in the top five.

Global ADC Popular Targets Source: Sanyou Biopharmaceuticals

In 2024, as GLP-1 and bispecific/trispecific antibodies steal the spotlight in business development (BD), ADC companies remain silent, focusing on hard work. This leads to another BD explosion in 2025: Incyte and Avenzo Therapeutics reached a $1.2 billion ADC deal, licensing overseas rights for an EGFR/HER3 bispecific ADC; Hansoh Pharmaceutical sold the overseas rights for its CDH17-targeted ADC, with a total transaction amount reaching $1.53 billion; Innovent Biologics reached a deal with Takeda for a bispecific and two ADCs worth $11.4 billion.

This round of BD is dazzling, with various new targets and routes of ADCs being “wholesale sold.”

However, most successful ADC projects from China still follow the technical frameworks of Daiichi Sankyo or Seagen.

Some biotech companies are jokingly referred to as “Second Daiichi Sankyo” because they not only have a pipeline layout highly similar to Daiichi Sankyo but have even directly recruited clinical researchers from Daiichi Sankyo, accelerating their pipeline advancement.

Of course, Chinese pharmaceutical companies are gradually breaking out of the imitation cycle, beginning to show the courage to deviate from the “big company route.” For example, Junshi Biosciences’ PD-L1 ADC diverges from Pfizer’s ADC targeting the same point, and Hengrui Medicine has proposed a complete theory addressing the industry pain point of “treatment resistance to HER2 ADC” and is starting to build a platform…

However, these innovations regarding the next generation of ADCs have yet to reach the final verification stage. Yet, each direction has proponents who firmly believe they are on the true cutting edge.

–01–

ADC Battle Royale

Currently, all so-called “next-generation ADC” explorations are fundamentally centered around three components of ADCs—target, payload, and linker.

The “target faction” believes that finding better targets is the key to breakthroughs; changing a target may open up new possibilities. The other two factions focus more on incremental advancements in underlying technologies, such as breakthroughs in drug loading capacity or optimizations in administration methods.

A researcher engaged in antibody studies is more likely to believe that target selection remains the most important. “But my colleagues in chemistry often do not see it this way; they generally feel that the target is not that critical, and instead, the payload is what determines success, with many believing that linker technology is the core.”

For example, Ilyang emphasizes the uniqueness of its linker, while Shijian also positions linker technology as a core differentiator. Other companies focus more on the payload, emphasizing that their toxin structure differs from DS-8201 (Enhertu).

In drug development, the emergence of new concepts often comes with extremely high expectations. Just as people once believed bispecific antibodies would surpass monoclonal antibodies, and placed hopes on “1+1>2,” concepts like “dual toxin ADCs,” “bispecific ADCs,” and “dual payload ADCs” are now imbued with similar expectations.

However, as expectations rise, the subsequent research paths and indication selections often face more realistic challenges.

Compared to monoclonal ADCs, bispecific ADCs indeed have a harder time grasping indications. The core issue lies in “too many choices”; when a drug targets two targets simultaneously, the potential range of indications expands significantly, making the clear research path more ambiguous. During the dose-escalation phase of Phase I clinical trials, the key questions researchers need to answer become more complex: which cancer type should be prioritized for exploration? How should the expression level thresholds for the two targets be set?

Pharmaceutical companies start from different points but end up on the same battlefield. In such a chaotic environment, companies need to quickly validate the clinical value of their technologies to avoid being overwhelmed.

Not only are domestic biotechs in the early clinical stages speeding up, but multinational corporations (MNCs) are also accelerating the market entry of ADCs.

A noteworthy trend is that in the past two years, some multinational pharmaceutical companies have begun to adopt more aggressive strategies in the clinical development of ADC drugs, advancing directly from Phase I to Phase III clinical trials.

As long as data from 40 to 50 patients is accumulated in a certain indication during Phase I clinical trials, companies will conduct a comprehensive evaluation of this data. If the data shows that the ADC demonstrates certain advantages in efficacy (such as ORR, PFS) compared to historical chemotherapy regimens, and the toxicity is controllable, they are willing to “skip” traditional Phase II trials and directly initiate Phase III clinical trials.

For example, in the field of lung cancer, these ADCs are often compared with docetaxel. Notably, docetaxel is typically used in later-line treatments, where patients often receive targeted therapy and platinum-based chemotherapy before using docetaxel in second-line or later settings. ADC drugs also usually start exploring in later-line treatments; if the ADC under investigation shows efficacy in such pre-treated patients that exceeds historical data for docetaxel, companies tend to directly conduct head-to-head Phase III clinical trials to accelerate progress.

Pfizer’s ADC project targeting ITGB6 has adopted this “skipping” development strategy.

This strategy has become particularly evident in the past two years, reflecting companies’ attempts to push drugs to market faster and reserve more resources and space for subsequent combination strategies.

–02–

BD Cannot Stop

Drug development for tumors generally follows three paths: the first path focuses on immunotherapy, developing the next generation of PD-1, whether PD-1/VEGF or PD-1/IL2, aiming to break through the bottlenecks of existing immunotherapy. Additionally, new activation methods like TCE and tumor vaccines are also options.

The third path is ADCs, which are “taking over” indications traditionally treated with chemotherapy. Today, ADCs are becoming the new standard in many end-stage cancer treatments; except for indications unsuitable for chemotherapy, such as liver cancer and kidney cancer, most common cancers have entered the range of ADCs.

This trend is closely related to MNCs’ strategies to cope with the “patent cliff.” MNCs must continuously launch new drugs in their original advantageous tumor types to maintain market position. For example, in the field of gynecological tumors, developing ADCs targeting folate receptor alpha, B7-H4, etc., has almost become a necessary choice. For MNCs, this is no longer a question of “whether to do it,” but rather “how to do it,” whether to develop in-house or license in?

Foreign companies often exhibit a kind of “stubbornness” in their technical routes. Once they select a certain technical platform or direction, they tend to form path dependence and are reluctant to easily start over. Because they have already invested a significant amount of sunk costs in one direction, they are more inclined to continue seeing its advantages rather than overturn it.

However, this “stubbornness” will continue to patch new solutions. Taking Pfizer as an example, although they acquired Seagen, they are not entirely limited to the latter’s original platform. Pfizer retains the core targets of Seagen, which are their exclusive assets with high barriers, making it difficult for other players to follow. At the same time, they actively introduce new pipelines from places like China to maintain diversity.

The cost differences between Chinese and American pharmaceutical companies keep BD a highly attractive business.

In the U.S., a full-time researcher earns about $300,000 a year, while in China, a similar position may only require 300,000 RMB. Despite a sevenfold cost difference, Chinese teams have scientific capabilities comparable to those in Europe and the U.S., with faster speeds, and now demonstrate the ability for differentiated innovation.

Junshi Biosciences recently announced key data for its PD-L1 ADC in non-small cell lung cancer research, which has almost reached two extremes compared to Pfizer’s similar product. Pfizer follows the conventional Seagen design, using MMAE toxin, but faces significant toxicity and moderate affinity, leading to limited efficacy in low-expressing patients. Junshi Biosciences attempts to tell a better story by using a higher-affinity antibody with better internalization and selecting a topoisomerase I inhibitor with strong bystander effects, aiming to tackle the 60% of PD-L1 low-expressing patient population. Theoretically, Pfizer’s solution may only cover the 40% of PD-L1 high-expressing patients, while Junshi Biosciences aims to be effective for the entire population.

In the most popular HER2 ADC field, most companies still tend to benchmark against DS-8201 when initiating projects or make slight adjustments based on it. Considering the extensive clinical application of DS-8201, its exploration in later lines becomes invaluable. Companies like Hengrui Medicine, with their latest designs in the ATTC platform, are expected to become learning and surpassing targets for many pharmaceutical companies.

These innovations have yet to receive final clinical validation. When big pharma is on a shopping spree, they also understand the inherent high failure rate of drug development; buying ten Chinese projects, as long as one succeeds, the math works out. For this reason, even if some projects fail, they will continue to seek opportunities in the Chinese market.

–03–

Limitations and Possibilities

In the ADC landscape depicted by Daiichi Sankyo, there has always been a vision of “5Dxd ADCs,” which includes the approved HER2 ADC DS-8201, TROP2 ADC Datopotamab, HER3 ADC Patritumab, the relatively early-stage B7-H3 ADC DS-7300, and CDH6 ADC DS-6000.

Ideally, they should surpass one generation after another; in reality, it seems that each stage struggles to surpass the previous one.

The capabilities of ADCs have objective limitations. Currently, they are more often viewed as a precision version of chemotherapy; whether using bispecific or monospecific carriers, the actual amount of drug that can be precisely delivered to the tumor site may only be 1%-5%.

Of course, if the tumor target expression is low and drug delivery efficiency is not high, we also hope for mechanisms like the “bystander effect” to compensate. This may be a form of self-comfort, but it also reflects the practical considerations in ADC design. In fact, no ADC can achieve a 100% overall response rate (ORR); some can reach 70%-80%, while others only achieve 20%-30%. This means that for a significant portion of patients, current drugs remain ineffective.

Despite the limitations of ADCs, this field will remain hot. Compared to oral formulations, ADCs achieve superior pharmacokinetic properties; a single injection can have sustained effects for weeks and gradually penetrate target tissues. Theoretically, all scenarios applicable to oral small molecules may potentially be replaced by ADCs in the future.

Now, the industry is beginning to explore combination therapies. For example, combining ADCs with PD-1 inhibitors, TCEs, etc., has become the direction for many research projects. The logic behind this strategy is not entirely based on confidence in synergistic mechanisms; more often, it is to enhance efficacy data and increase the likelihood of approval, even if combinations inevitably lead to additive toxicity.

To some extent, this is an inevitable situation driven by existing drug pipelines; since there are drugs on hand, they must be pushed into clinical trials, even if only to validate their combination potential.

In this light, ADCs are likely to remain popular for a long time.

……

Feel free to connect with the author:

Wu Ni: nora4409