“Special Report on the AI Industry (12): Current Status and Development Trends of AI Agent Development Platforms, Models, and Applications” is published by Guosen Securities. The report mainly includes the following research content: Definition of Agents, Technology and Development, Layout of Agent Development Platforms, Analysis of Model Layers and Token Call Volumes, Progress of C-end and B-end Agents, Market Space and Development Expectations for Agents.

This report contains:78 pages. The complete PDF version of the report can be downloaded at the end of this article.

Summary of the Research Report:

AI Agent: The Core Engine Reshaping Enterprise Intelligence

-

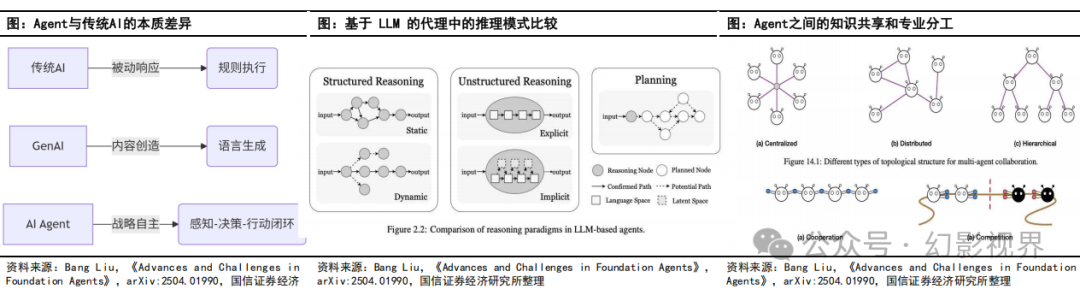

Definition: An intelligent entity with autonomy, planning ability, and execution capability, transcending the era of “command execution” into the era of “agency”. The core breakthrough lies in granting “agency” → proactive perception of the environment, autonomous planning and decision-making, and execution of complex tasks.

-

Key Features:: 1) Autonomous decision-making: proactively perceiving the environment, setting goals, and taking action; 2) Dynamic learning: achieving continuous optimization through memory and experience accumulation; 3) Cross-system collaboration: utilizing tools, APIs, and multi-Agent collaboration to complete complex tasks.

-

Core Modules:: 1) Perception Layer: multimodal input (text/voice/image); 2) Memory Layer: short-term memory (dialogue context) + long-term memory (knowledge base); 3) Decision Layer: action strategies based on goal planning and reinforcement learning; 4) Execution Layer: tool invocation (API), cross-system collaboration (RAG technology).

-

Key Differences:: 1) LLM ≠ Agent: LLM is a “knowledge consultant”, while Agent is a “strategic commander”; 2) Traditional automation: only rule execution vs Agent: end-to-end task closure.

AI Agent Market Map

① Infrastructure Agents: Focus on underlying support, covering development platforms, multi-agent collaboration, data management, etc., to build a foundation for AI applications.

② Horizontal Functional Agents: Serving B/C-end customers, from productivity tools to customer service, human resources, etc., adaptable across industries, optimizing processes and enhancing daily operations.

③ Vertical Application Agents: Deeply engaged in specific industries such as finance and healthcare, closely aligned with industry processes, regulations, and needs, deeply integrating professional knowledge to form industry-specific solutions.

AI Agent Development: Rapid Growth, High Proportion in Customer Service and Software Development

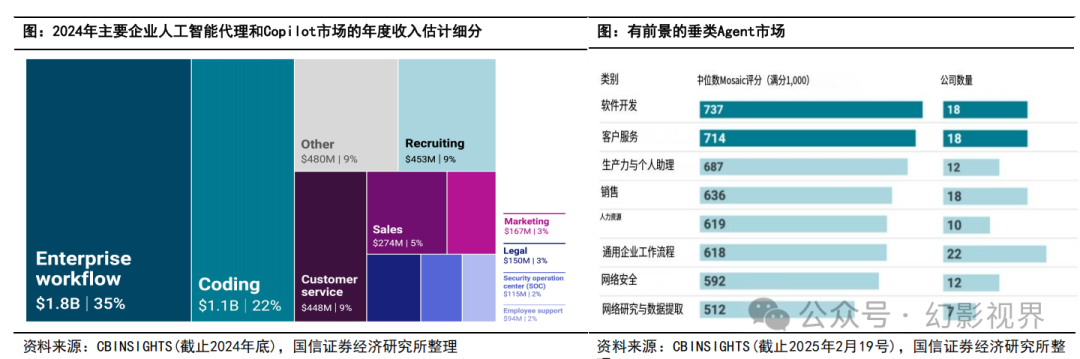

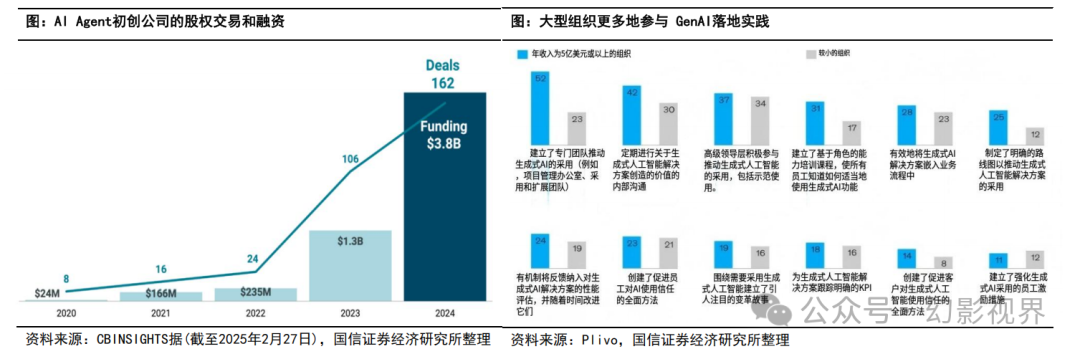

Leading Segmented Markets: According to CBINSIGHTS, revenue in the fields of enterprise workflow and coding is expected to exceed $1 billion in 2024, with the former covering general productivity, research, etc., and the latter experiencing an explosion of AI coding tools, creating unicorns within six months, at a speed four times the industry average.

Core Drivers and Players: In 2024, tech giants will dominate revenue, with Microsoft’s Copilot (approximately $800 million in 2024 revenue) and GitHub Copilot (approximately $600 million in 2024 revenue), together accounting for over 25% of the overall market share. Startups are growing rapidly, such as Cursor, whose annual recurring revenue (ARR) increased from $1 million to $200 million.

Vertical Markets: The survey mainly targets the enterprise side, with customer service and software development being high-potential tracks. By the end of 2024, the survey shows that two-thirds of 64 organizations plan to use AI agents to support customer service within 12 months. Vertical AI Agents cover general enterprise scenarios (human resources, marketing, security operations, etc.), which are more mature in commercial implementation compared to infrastructure and vertical tracks.

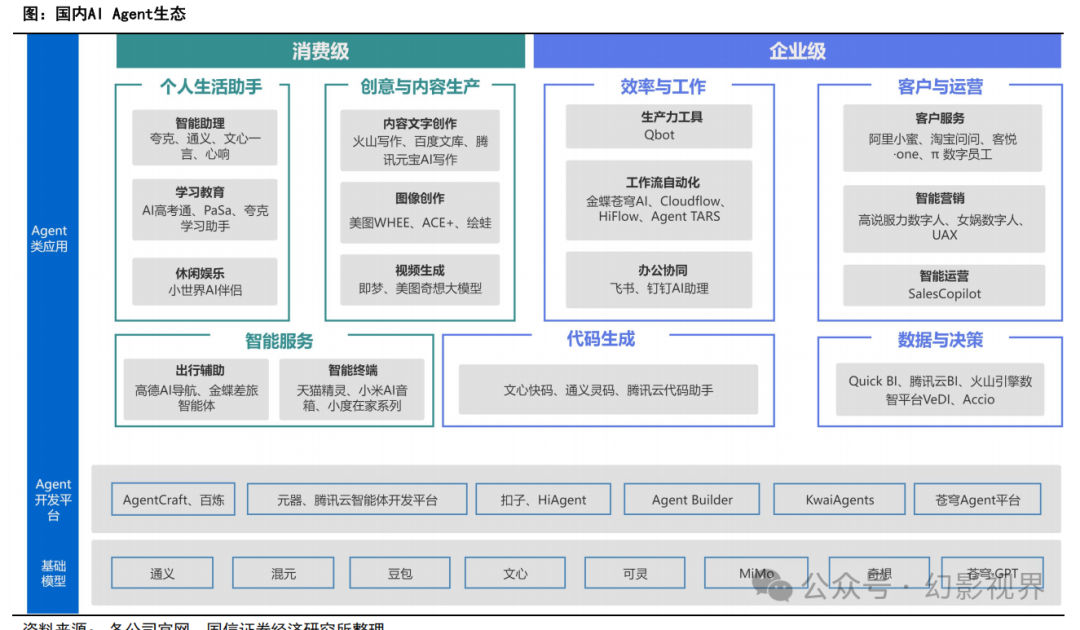

Domestic AI Agent Ecosystem: Alibaba, Tencent, ByteDance, Baidu, Kuaishou, Xiaomi, Meitu, Kingdee

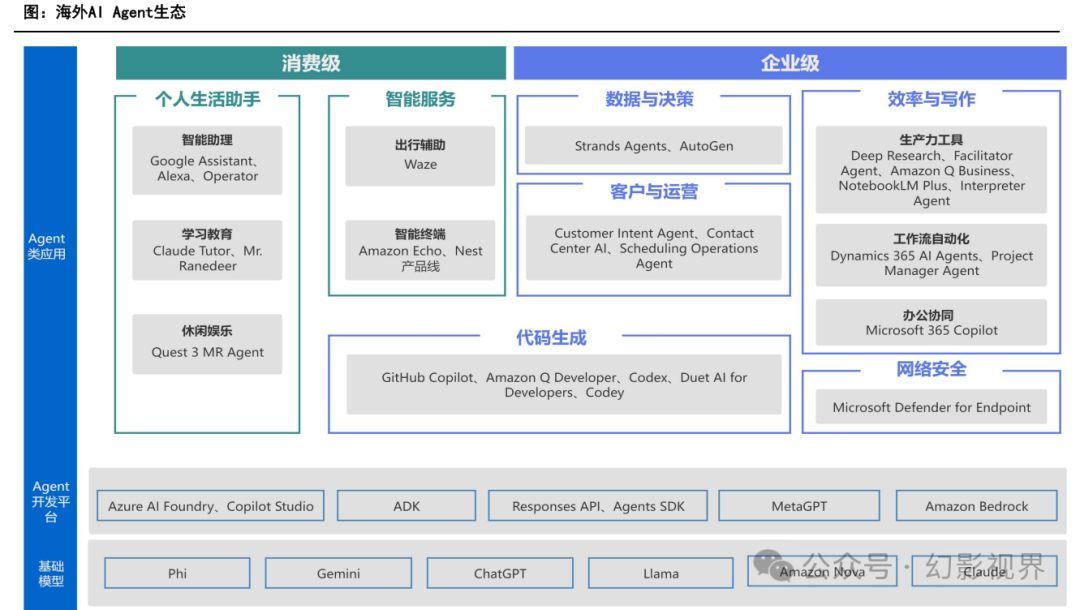

Overseas AI Agent Ecosystem: Microsoft, Google, OpenAI, META, Amazon, Anthropic Agents

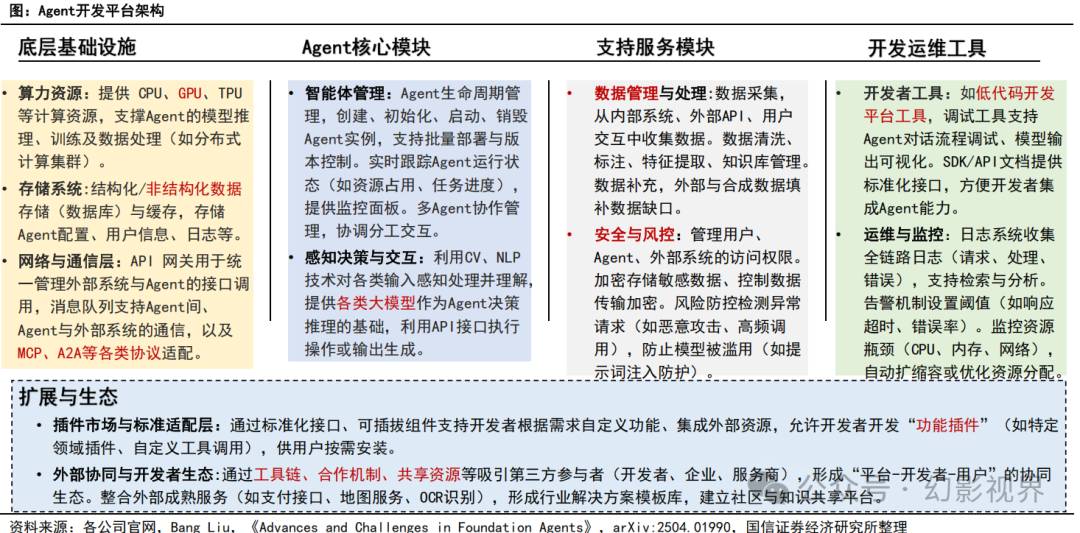

Typical Platform Architecture and Core Elements

Agents are the key bridge for GenAI to move from “proof of concept” to “enterprise-level application”, with the core being to release the scalable value of AI through process reconstruction and data integration.

Overseas Agent Platform Layout: Comparison of Microsoft, Google, and Amazon

Summary: Microsoft focuses on B-end infrastructure, being the most comprehensive platform in terms of model support, with a fully integrated toolchain and ecosystem, strong security and stability; Google relies on AI Studio to cater to multiple scenarios for B/C-end, with strong multimodal capabilities but an immature ecosystem and low market share; Amazon/Anthropic primarily serve small and medium enterprises through AWS services, focusing on computing power sales and convenient deployment, with the Claude model being highly practical, but the toolchain is fragmented.

Domestic Agent Platform Layout: Comparison of ByteDance, Alibaba, and Tencent

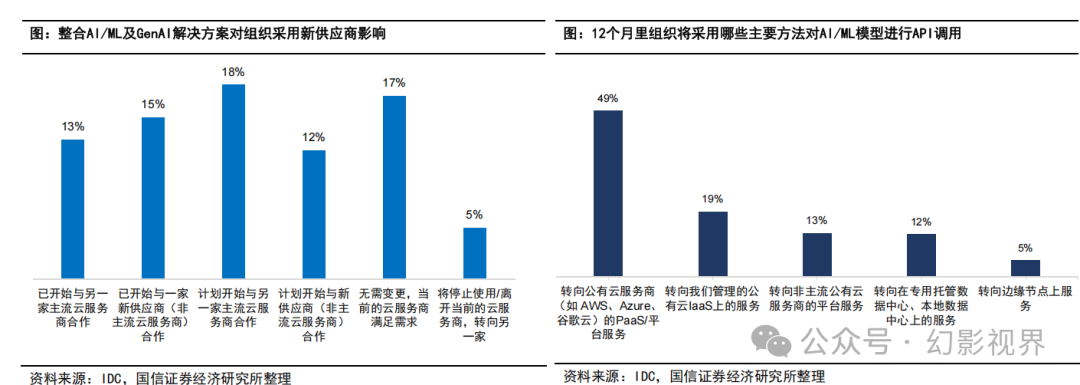

PaaS/Agent Platform Evolution: Customers Will Re-select Based on AI/Tool Deployment Capabilities

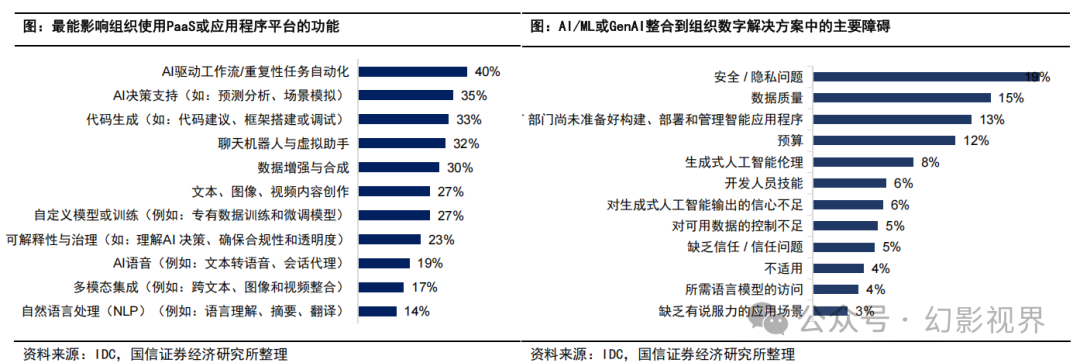

PaaS/Application platform suppliers face new market share division opportunities: According to IDC surveys, 70% of respondents will change or add cloud/AI platform suppliers. Only 17% of respondents believe their current cloud provider can meet their AI/ML/GenAI needs. 28% of respondents have already been forced to change providers, while another 42% plan to leave their current provider or join a cloud provider mix.

Key Barriers to AI Solution Implementation: Security and privacy issues are the biggest barriers affecting the implementation of AI projects in enterprises (19%), followed by data quality (15%) and insufficient IT department capabilities (13%). Additionally, budget, technical and ethical risks, insufficient output credibility, and inadequate data usage control are also significant challenges.

PaaS/Agent Platform Selection: Cloud as the Foundation, Scene Implementation Priority

-

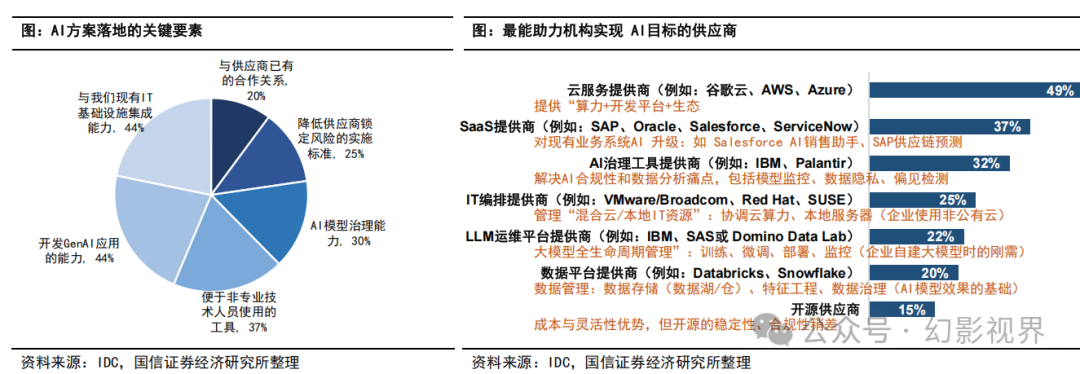

When enterprises implement AI solutions, they focus most on “technical integration capability (44%)” and “application development capability (44%)”. Enterprises want to quickly implement dedicated GenAI applications (such as customer service, marketing), with large model applications being the core link, while avoiding AI silos, existing systems (such as ERP, CRM) need to be integrated to truly embed AI into business processes.

-

Among the vendors that can help enterprises achieve AI goals, cloud service providers (49%) are overwhelmingly leading, reflecting that AI applications depend on AI platforms, and AI platforms = cloud computing power + development platform + ecosystem construction logic.

-

Additionally, to enable AI technology to quickly empower existing businesses, the importance of SaaS providers and AI governance tool providers/solution providers is also highlighted. SaaS providers can help enterprises upgrade existing business systems to AI, while AI governance tool providers can address compliance and data analysis pain points.

Important Suppliers of Agent Platforms: Strong Stock Prices Accompanying Agent Implementation Demand

Overseas Large Model Differentiated Development

-

OpenAI: Technologically leading, focusing on enhanced reasoning and specialized domain capabilities, gradually improving cost-effectiveness, but with weaker end-to-end multimodal generation capabilities compared to Google. Market expectations previously anticipated that GPT-5 would have strong native understanding of various modal inputs and could convert them into executable instructions/multimodal outputs, which has not been realized.

-

Google:: Leading in end-to-end native multimodal understanding (video, audio, text) input, with output limited to text. AIGC, especially in video generation, is industry-leading.

-

Anthropic:: Emphasizing practicality and leading in programming scenarios, high accuracy has brought a high market share, but general performance and multimodal capabilities are slightly weaker compared to leading models.

Domestic Large Models Have Not Shown Significant Gaps, Leading Models Are Mainly Self-Developed

DeepSeek: Leading in technical research, adopting hybrid attention mechanisms, dynamic routing, MoE, and other architectural innovations to reduce computational complexity and communication overhead, improving data utilization, excelling in code generation, mathematical calculations, and other specialized fields, open-sourced, supporting over 100 languages.

Alibaba: Strong self-development and comprehensive capabilities, with rich model parameters and types, Qwen3.0 performs outstandingly in multimodal and dialogue interaction, supporting long text processing.

Others: ByteDance’s Doubao large model performs relatively balanced across modalities, although most modalities are not leading, the overall score is high. Baidu’s Wenxin large model is deeply optimized for Chinese scenarios, with outstanding long text understanding capabilities. Tencent’s Hunyuan large language model is based on DeepSeek’s modifications, with less self-development investment.

Various SaaS Companies’ Traditional Business and AI Development Stages

Applications: B-end Copilot/Agent Product Forms Are Diverse and Continuously Penetrating, Opportunities and Challenges Coexist. Currently, Microsoft’s Copilot family has over 100 million monthly active users, becoming a representative product of B-end Agents/Copilots, but enterprise implementation still faces issues such as hallucinations, data security, and high costs (Agent invocation costs are 15 times that of LLM), B-end SaaS faces a reconstruction of industrial paradigms under the technological revolution (the cost of software production is gradually approaching zero). From an industry perspective, the hotel/restaurant/tourism sectors have the highest GenAI investment.

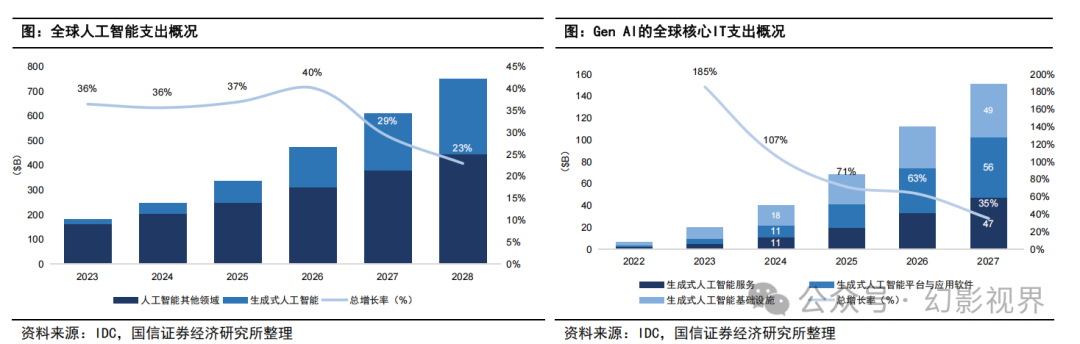

Market Size and Development Forecast for Agents: According to IDC data, global AI IT spending is expected to grow at a CAGR of 22.3% from 2023 to 2028, with GenAI reaching 73.5%. CBINSIGHTS predicts that AI Agent revenue is expected to reach $10.36 billion by 2032 (CAGR 44.9%). According to Gartner and IDC, in the short term (2023-2025), GenAI will be embedded in existing applications, in the medium term (2025-2027), Agents will become core components, and in the long term (2027+), autonomous agent networks will dominate business. After 2035, Agents will become cognitive symbiotic human assistants, and intelligent agents will become mainstream applications.

This article is for reference only and does not represent any investment advice from us.The materials organized and shared by Huanshi Vision are recommended for reading only, and the materials obtained by users are for personal learning purposes. For any usage, please refer to the original report. Huanshi Vision’s industry report resource library shares practical resources daily. Scan the QR code below to join and directly search for downloads, with a wealth of historical materials available for viewing and downloading at any time.

This article is for reference only and does not represent any investment advice from us.The materials organized and shared by Huanshi Vision are recommended for reading only, and the materials obtained by users are for personal learning purposes. For any usage, please refer to the original report. Huanshi Vision’s industry report resource library shares practical resources daily. Scan the QR code below to join and directly search for downloads, with a wealth of historical materials available for viewing and downloading at any time. Disclaimer: The above reports are obtained by this platform through public and legal channels, and the copyright of the report belongs to the original author/publishing institution.If there is any infringement, please contact us for timely deletion. The content is for recommended reading only and for learning purposes. If there are any doubts about the content, please contact the original author/publishing institution.

Disclaimer: The above reports are obtained by this platform through public and legal channels, and the copyright of the report belongs to the original author/publishing institution.If there is any infringement, please contact us for timely deletion. The content is for recommended reading only and for learning purposes. If there are any doubts about the content, please contact the original author/publishing institution. Click “Read the original text” to download the report.

Click “Read the original text” to download the report.