Current Status and Future Development Trends of the PCB Industry in 2025 (September Update)

Executive Summary

The PCB industry, known as the “mother of electronic products,” has overall entered a mature phase but is undergoing a structural upgrade driven by AI computing power, new energy vehicles, and 5G communication. The demand for high-end products such as IC substrates and HDI is surging, pushing the industry towards high technology content and high added value, exhibiting a significant characteristic of “overall maturity with localized high growth.” The upstream material segment of the industry chain is profit-stable, while the midstream manufacturing shows significant differentiation, with leading companies enjoying valuation premiums due to technological barriers. The long-term outlook is supported by domestic substitution and global layout, but potential risks such as valuation adjustments, demand falling short of expectations, and geopolitical factors must be monitored. Investment opportunities are focused on companies leading in high-end technology trends and capacity layout..

1 Overview of the PCB Industry

1.1 Definition of the PCB Industry

A Printed Circuit Board (PCB) is an indispensable key electronic interconnect component in electronic devices, often referred to as the “mother of electronic products.” PCBs are manufactured using electronic printing technology, primarily providing mechanical support and electrical connections for electronic components, enabling signal transmission between them. As a fundamental component of electronic devices, PCBs are present in nearly all electronic devices, from everyday smartphones and computers to advanced aerospace equipment, relying on PCBs to ensure their normal operation.

1.2 Role and Impact of the PCB Industry in Life

(1) The Role of the PCB Industry in Technological Development

The PCB industry serves as the fundamental support for the electronic information industry, profoundly driving technological advancement. In the wave of digital economic development, innovations in PCB technology are directly related to the performance and functionality of electronic products. With the vigorous development of artificial intelligence, high-performance computing, and new energy applications, the PCB industry is actively evolving towards high layer counts, high density, high performance, and high transmission efficiency. This trend significantly drives the growth in demand for related PCB equipment and materials and technological upgrades.

(2) The Impact of the PCB Industry on Population Structure and Employment

The PCB industry, combining labor-intensive and technology-intensive characteristics, has a complex and profound impact on population structure and the job market. On one hand, the PCB manufacturing industry provides numerous job opportunities for a large workforce; on the other hand, with industrial upgrades and increasing automation levels, the demand structure for labor is continuously changing.

(3) The Broad Impact of the PCB Industry on Social Development

The PCB industry, as the foundation of the electronic information industry, has a profound impact on various aspects of social life. From everyday smartphones and computers to communication networks and energy systems that society relies on, all depend on PCB technology for support.

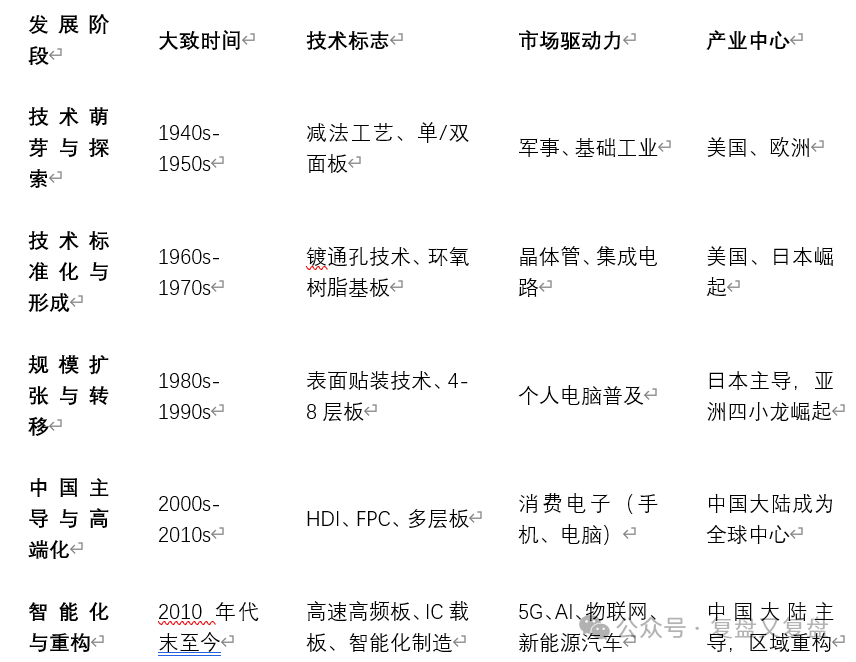

2 Review of the Development History of the PCB Industry

The history of the PCB industry is a microcosm of the global electronic industry’s technological evolution and pattern changes. Its development can be roughly divided into several key stages, each driven by technological breakthroughs, market demand, or changes in global industrial division. Currently, the PCB industry is entering a new development cycle driven by next-generation technologies represented by 5G communication, artificial intelligence, the Internet of Things, and new energy vehicles. The requirements for PCBs are no longer limited to simple connectivity but need to support high frequency and speed, high heat dissipation, and high reliability. High layer counts, high-density IC substrates, and arbitrary layer HDI have become the high ground of technological competition. On the other hand, changes in the global trade environment, rising labor costs in mainland China, stricter environmental requirements, and geopolitical factors are driving regional restructuring of the PCB industry chain, showing a trend of “dual transfer” towards certain regions in Southeast Asia and inland areas of China. Meanwhile, the concept of Industry 4.0 is deeply penetrating, with automation and intelligent production becoming key to enhancing competitiveness, and the industry is accelerating its transformation from labor-intensive to technology-intensive.

Table: Summary of Key Stages in the Development History of the PCB Industry

Reviewing the nearly eighty-year development history of the PCB industry, its path clearly demonstrates the interactive evolution of technological breakthroughs, market demand, and global industrial division. Currently, the industry stands on the threshold of a new technological revolution, and its future evolution will continue to profoundly impact the global electronic industry landscape.

3 Analysis of the Current Development Status of the PCB Industry Chain

3.1 Market Size of the PCB Industry Chain

Global Market Size

-

Overall Size: The global PCB output value is expected to reach 73.565 billion USD in 2024 (a year-on-year increase of 5.8%), and is projected to grow to 78.6 billion USD in 2025 (growth rate of 6.8%), and is expected to exceed 94.0 billion USD by 2029 (CAGR of 4.8%). China dominates the global market, with the output value of PCBs in mainland China reaching 41.213 billion USD in 2024, accounting for 56.02% of the global share.

-

Segmented Product Structure (Global Share in 2024):

-

Multilayer Boards:38.05% (largest market share);

-

Packaging Substrates:17.13%;

-

HDI (High-Density Interconnect Boards):17.02%;

-

FPC (Flexible Circuit Boards):17.00%.

-

Regional Distribution:

-

China has formed three major industrial clusters: the Pearl River Delta (led by Guangdong, focusing on high-end consumer electronics and HDI boards, accounting for 45% of the national output), the Yangtze River Delta (focusing on automotive electronics and communication IC substrates, accounting for 60% of national capacity), and the Central and Western regions (such as Jiangxi and Hubei, which are receiving capacity transfers and growing faster than the national average).

-

Southeast Asia has become a hotspot for capacity transfer (such as Vietnam and Thailand), expected to account for 12% of global output value by 2025 (with cost reductions of about 15%).

Market Size in China

-

In 2024, the market size of PCBs in China is expected to reach 415.6 billion CNY (approximately 60 billion USD), with a year-on-year growth of 8.3%, and is projected to increase to 554.51 billion CNY by 2029 (CAGR of 5.5%). China’s share of global PCB manufacturing has risen from 8.1% in 2000 to 56.1% in 2024, firmly establishing it as the largest production base globally.

-

Cost Structure of the Industry Chain:

-

Upstream materials (such as copper-clad laminates and copper foil) account for 30-50% of PCB production costs, with copper-clad laminates alone accounting for about 27%. Fluctuations in copper prices directly impact costs, with copper prices expected to rise by 12% year-on-year in 2025, squeezing corporate profits.

-

High-end materials (such as high-frequency and high-speed copper-clad laminates) still rely on imports for over 50%, but domestic substitution is accelerating (for example, domestic materials from Shengyi Technology are about 15% cheaper than foreign ones).

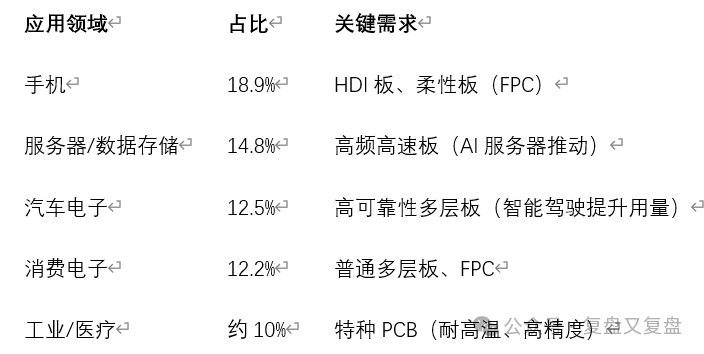

Downstream Application Market Distribution (2024 Share)

3.2 Core Drivers of Future Growth

-

AI Computing Power and Data Centers

-

Simultaneous Increase in Quantity and Price: The value of a single PCB for AI servers reaches 5000 CNY (three times that of traditional servers), driving the demand for high-frequency and high-speed PCBs. The global market size for AI server PCBs is expected to reach 12 billion USD in 2025, with a compound annual growth rate (CAGR) exceeding 30%.

-

Technological Upgrades: AI servers require high multilayer boards with more than 18 layers (40.2% growth in 2024) and HDI boards (18.8% growth), with domestic companies like Shennan Circuit and Huitian Technology capturing over 30% of the AI server market share.

New Energy Vehicles and Intelligent Driving

-

Explosive Demand: The electronic rate of vehicles exceeds 65%, with the share of automotive PCBs rising from 12% in 2020 to 20% in 2025 (market size exceeding 30 billion USD). Intelligent driving systems increase the PCB area per vehicle from 0.5㎡ to 3㎡, with the PCB value for L4 autonomous vehicles exceeding 2000 CNY.

-

High Voltage Platforms and ADAS: The 800V high-voltage system and ADAS domain controllers drive the demand for high multilayer boards, increasing the value per vehicle by 5 times compared to traditional vehicles..

5G Communication and Satellite Internet

-

Over 5 million global 5G base stations have been built, driving a 25% increase in demand for high-frequency PCBs; the construction of low-orbit satellite constellations (such as Starlink) is generating demand for PCBs that can withstand extreme environments, with a single satellite using 20㎡, opening up a new market worth about 5 billion CNY.

Recovery and Innovation in Consumer Electronics

-

AI smartphones (such as Apple’s AI smartphone) and VR devices (Vision Pro) are driving demand for SLP (substrate-like PCB) and FPC, with the penetration rate of HDI in the Android camp accelerating. The consumer electronics PCB market is expected to grow by 8-10% year-on-year in 2025.

Green Manufacturing and Domestic Substitution

-

Environmental regulations (such as the EU carbon border adjustment mechanism) are forcing industrial upgrades: the coverage of lead-free processes has increased from 80% to 95%, with photovoltaic PCB factories accounting for over 20%, and energy consumption per unit of output decreasing by 18%.

-

Domestic substitution is accelerating: the localization rate of wet electronic chemicals and other materials has increased (costs are 25-30% lower than imports), with the localization rate of high-end IC substrates rising from 15% in 2023 to 28% in 2025.

4 Analysis of the Competitive Landscape and Profitability of the PCB Industry Chain

The competitive landscape and profitability of the PCB industry chain show significant differences across the upstream raw materials, midstream manufacturing, and downstream applications segments. The upstream materials have high technological barriers, high concentration, and strong profitability; the midstream manufacturing shows significant differentiation, with high-end products being particularly profitable; the downstream applications drive technological upgrades, with emerging fields offering substantial profit margins.

4.1 Upstream Competitive Landscape and Profitability

Core Characteristics:Strong material monopolies, outstanding cost transmission capabilities, and gross profit margins of 30%-40%.

1. Competitive Landscape

-

Highly Concentrated: Key materials such as copper-clad laminates, copper foil, and fiberglass cloth are dominated by a few giants. The top five manufacturers in the global copper-clad laminate market account for over 50%, with leading Chinese companies like Shengyi Technology (the second-largest rigid copper-clad laminate manufacturer globally, with a market share of over 10%), and Kingboard Group leveraging scale and technological advantages to dominate the market.

-

High Technological Barriers: High-frequency and high-speed copper-clad laminates (such as those certified by Shengyi Technology through NVIDIA) and environmentally friendly substrates are high-end products that rely on imports, with significant room for domestic substitution.

-

Regional Clustering: Material companies are concentrated in the Yangtze River Delta and Pearl River Delta, closely collaborating with midstream manufacturing.

2. Profitability

-

Leading Gross Profit Margins: The gross profit margins for copper-clad laminates generally reach 30%-35%, with high-end products (such as high-frequency and high-speed materials) exceeding 40%. The main reasons include:

-

Cost-Plus Pricing: Rising copper prices (expected to increase by 12% year-on-year in 2025) can be quickly passed on to downstream customers.

-

Technological Premium: For example, after the copper-clad laminates for AI servers from Shengyi Technology are certified, the conversion of orders drives profit growth.

-

Profit Drivers::

-

Surge in High-End Demand: The demand for high-frequency and high-speed materials driven by AI servers and new energy vehicles has led to a net profit of 635 million CNY for Shengyi Technology in the first quarter of 2025 (a year-on-year increase of 43%).

-

Accelerated Domestic Substitution: Domestic materials are 25%-30% cheaper than imports, with the substitution rate rising from 15% in 2023 to 28% in 2025.

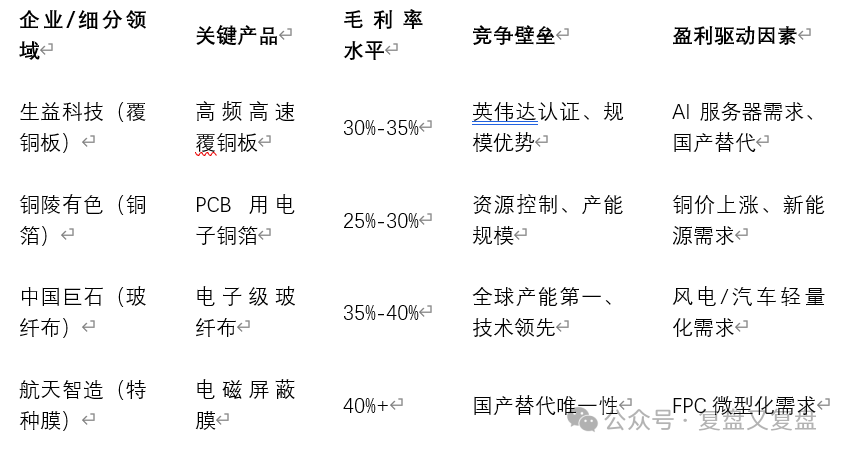

Table: Profitability and Competitive Indicators of Major Upstream Material Companies (First Half of 2025)

4.2 Midstream Competitive Landscape and Profitability

Core Characteristics:Structural differentiation, strong profitability in high-end technologies (HDI, IC substrates), and intense competition in low-end homogeneous products.

1. Competitive Landscape

-

Clear Tiering: (based on revenue scale):

-

First Tier (Revenue > 10 billion CNY): Pegatron (12% global market share), Dongshan Precision (third globally), Shennan Circuit (eighth globally), dominating high-end markets such as AI server PCBs and packaging substrates.

-

Second Tier (50-100 billion CNY): Huitian Technology, Shenghong Technology, Chongda Technology, focusing on niche markets (such as servers and automotive electronics).

-

Third Tier (< 50 billion CNY): Small and medium-sized manufacturers primarily produce low-end standard boards, facing intense price competition.

-

High Concentration in High-End Markets: The top two manufacturers of AI server PCBs (Shenghong Technology and Huitian Technology) account for over 70% of the global market share; the IC substrate market is monopolized by companies like Xinxing Electronics and Shennan Circuit.

-

Global Capacity Layout: Companies are accelerating factory construction in Southeast Asia (such as Shenghong Technology in Vietnam and Shennan Circuit in Thailand) to avoid tariffs and meet local demand.

2. Profitability

-

Significant Differentiation::

-

High-End Products Have Gross Profit Margins of 35%-40%: For example, Shenghong Technology’s AI computing card PCB (gross margin of 38%), Huitian Technology’s 800G switchboard (gross margin over 40%), primarily due to technological barriers (20+ layer HDI, IC substrate processes) and direct binding with leading customers like NVIDIA/AMD.

-

Low-End Products Have Gross Profit Margins of Only 15%-20%: The oversupply of standard multilayer boards for consumer electronics and intense homogeneous competition are squeezing profits.

-

Cost Pressures and Responses::

-

In the first half of 2025, rising copper prices upstream caused about 18 companies’ operating cost growth to outpace revenue growth.

-

Leading companies maintain profitability through product structure optimization (for example, Shenghong Technology’s server board proportion increased to 48.96%) and refined cost control (Huitian Technology’s copper etching liquid recovery rate is 98%).

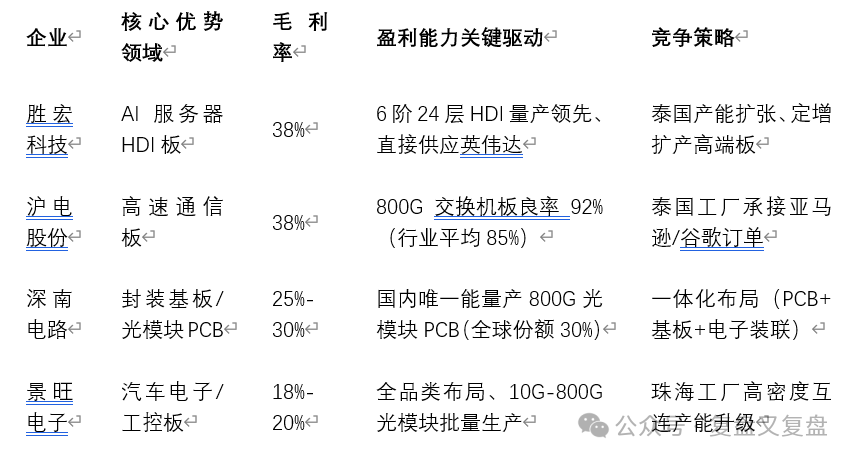

Table: Profitability and Competitive Strategies of Representative Midstream Companies (First Half of 2025)

4.3 Downstream Competitive Landscape and Profitability

Core Characteristics:Demand-driven technological upgrades, with emerging applications (AI servers, automotive electronics) having the strongest pricing power.

1. Competitive Landscape

-

Diversified Application Fields: Communication (23%), automotive electronics (12.5%), and consumer electronics (12.2%) are the top three sources of demand, but growth momentum is differentiated:

-

High-Growth Areas: AI servers (CAGR of 38.3% from 2023-2028), automotive electronics (L2+ intelligent driving penetration), and low-orbit satellites (20㎡ PCB usage per satellite).

-

Mature Areas: Smartphones (accounting for 18.8%), personal computers, stable demand but innovation focuses on high-end boards (such as HDI).

-

High Customer Barriers: Downstream leading manufacturers (such as NVIDIA and Tesla) have strict PCB certification requirements and collaborate with suppliers on design (such as NVIDIA’s partnership with Huitian Technology), strengthening the advantages of leading companies through long-term binding relationships.

2. Profitability

-

Significant Gross Margin Differences Across Downstream Industries::

-

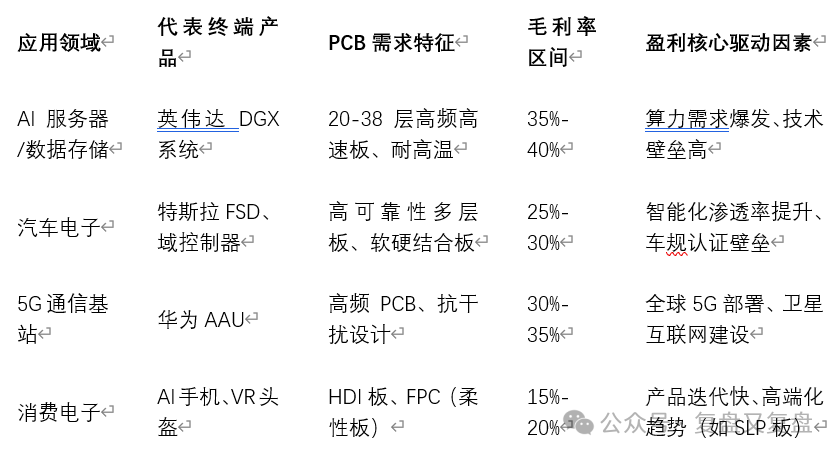

Communication Equipment (35%-40%): The value of a single PCB for AI servers reaches 5000 CNY (three times that of traditional servers), driving demand for high-frequency and high-speed boards.

-

Automotive Electronics (25%-30%): The PCB area for intelligent vehicles has increased from 0.5㎡ to 3㎡ (L4 vehicles valued over 2000 CNY), with domain controllers driving simultaneous increases in volume and price for high multilayer boards.

-

Consumer Electronics (15%-20%): Intense competition, but AI smartphones and VR devices are driving growth in high-margin niche markets such as SLP boards.

-

Profit-Driving Logic::

-

Technological Upgrade Premium: AI servers require 20-30 layer HDI boards, and automotive high-voltage platforms require high-temperature resistant materials, pushing up PCB prices.

-

Supply Chain Collaboration: Downstream manufacturers reduce costs through “one-stop procurement” (such as Jialichuang), while midstream companies are transitioning to service-oriented models to enhance added value.

Table: Profitability Demand Characteristics of Major Downstream Application Areas

5. Current Industry Lifecycle Status of the PCB Industry Chain

As a whole, the PCB industry has entered a mature phase. However, unlike classic lifecycle theories, this industry does not develop synchronously but exhibits significant structural differentiation characteristics. Different segments and products are at different lifecycle stages, with distinct driving factors and future trajectories.

5.1 Overall Industry: In a mature phase, but driven by structural innovation

Core Judgment: The global PCB industry has crossed the rapid growth introduction and growth phases, entering a mature phase characterized by “stable quantity and improved quality”..

-

Market Characteristics::

-

Slowing Growth: The global market size growth rate is stabilizing, with a compound annual growth rate (CAGR) maintained in the range of 4%-6%, far below the double-digit growth of the growth phase. This indicates that the market has shifted from “land grab” incremental competition to “fine cultivation” stock competition.

-

Increased Concentration: Industry mergers and integrations are intensifying, with leading companies continuously increasing market share through scale effects, technological advantages, and global layouts, resulting in a significant Matthew effect.

-

Increased Cost and Environmental Pressures: A typical characteristic of mature markets is that cost control becomes a core competitiveness, while environmental and social responsibility regulations are becoming increasingly stringent, forcing companies to transform and upgrade.

-

Growth Logic Shift: The growth of the industry no longer relies on the popularity of a single electronic product (such as feature phones or PCs) but shifts towards being driven by multidimensional and structural innovations. This means that while the overall market growth rate is stable, segments that align with new trends are experiencing a new round of rapid growth.

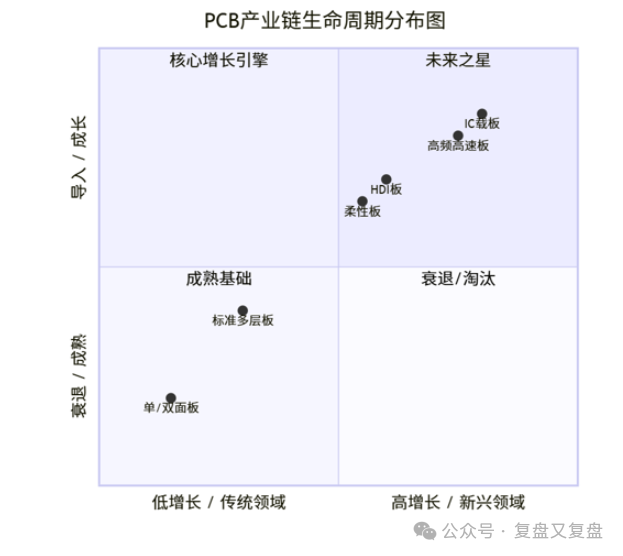

5.2 Differentiation in Lifecycle Stages Across Segments and Products:

The following diagram clearly depicts the lifecycle stages and growth potential of each major segment in the PCB industry chain:

In summary, the lifecycle status of the PCB industry chain can be summarized as:

-

Overall maturity with localized growth: The industry as a whole has entered a mature phase, but segments driven by cutting-edge technologies are experiencing a “second spring,” demonstrating strong growth potential.

-

Dual-track Growth Drivers: Growth momentum is shifting from “demographic dividends” and “scale expansion” to “technological innovation dividends” and “application upgrade dividends”.

-

Differentiated Corporate Strategies: Leading companies are enhancing valuation and profitability by positioning themselves in high-growth areas (such as IC substrates); medium-sized companies are focusing on deep cultivation in specific mature markets; while small companies lacking technological advantages are struggling to survive in declining areas, facing the risk of elimination.

6 Industry Prosperity and Valuation Analysis of the PCB Industry Chain

The industry prosperity and valuation levels of the PCB industry chain directly reflect market expectations and investment value in this field. Currently, the industry is in a high prosperity expansion cycle, but there is significant valuation differentiation across different segments and companies, presenting a structural characteristic of “high prosperity and high valuation for high-end products, intense competition and low valuation for low-end products”.

6.1 Industry Prosperity: AI Computing Power and Technological Innovation Drive High Prosperity Expansion

The prosperity of the PCB industry has been continuously improving since the second half of 2024, maintaining a high level in Q1-Q3 of 2025, primarily driven by the explosive demand from AI computing power, automotive electronics, and edge AI hardware.

6.1.1 Demand Side: High-End Applications Drive Simultaneous Increases in Quantity and Price

-

AI Servers and Computing Infrastructure::

-

Explosive Demand: The value of a single PCB for AI servers reaches 5000 CNY (3-5 times that of traditional servers), with NVIDIA’s GB200 cabinet PCB value reaching as high as 171,000 USD/cabinet. The global market size for AI server PCBs is expected to be approximately 53.88 billion CNY in 2024, projected to increase to 79.47 billion CNY by 2031 (CAGR of 6.4%).

-

Technological Upgrades: AI servers are driving PCBs towards high multilayer boards with more than 18 layers and high-end HDI (4 layers and above), with the increase in layers raising prices by 3-5 times. Prismark predicts that the AI/HPC server PCB market will have a CAGR of 32.5% from 2023 to 2028.

-

Automotive Electronics::

-

The popularization of intelligent driving (L2+ penetration rate exceeding 45%) is driving the value of PCBs per vehicle from traditional vehicles 500 CNY to 3000 CNY (L4 vehicles exceeding 2000 CNY), with strong demand for ADAS domain controllers and 800V high-voltage platforms.

-

Recovery in Consumer Electronics and Edge AI::

-

Hardware iterations such as Apple’s AI smartphone and Vision Pro are driving demand for SLP (substrate-like PCB) and FPC, with the penetration rate of HDI in the Android camp accelerating.

6.1.2 Supply Side: High Utilization Rates, Capacity Concentrating on High-End

-

Capacity Utilization Rates: In Q1-Q2 of 2025, the overall utilization rate of PCB manufacturers remains at 90%-95%, with high-end HDI and IC substrate capacities in short supply.

-

Expansion Direction: Capacity expansion is concentrated on high-end HDI (such as Shenghong Technology’s mass production of 6-layer 24-layer HDI), high-frequency and high-speed boards (for AI servers), and overseas bases (Southeast Asia with cost reductions of 15%). However, there are emerging risks of oversupply in low-end standard boards.

-

Supply Chain Bottlenecks: Upstream high-end materials (such as M8 grade copper-clad laminates) are in tight supply, with demand CAGR (26%) far exceeding capacity growth (7%), leading to ongoing price pressures.

6.1.3 Prosperity Indicators Verification:

-

Taiwan PCB Leading Indicators: The CP value (order/shipment ratio) of the Taiwan PCB industry has been above 0.5 for six consecutive months, indicating strong demand.

-

Company Orders and Performance: Many AI-PCB companies are fully booked (such as Huitian Technology and Shenghong Technology), with explosive performance in Q1 of 2025 (Shenghong Technology’s net profit growth rate of 272%-367%).

6.2 Valuation Analysis: Performance-driven differentiation, with high-end leaders enjoying premiums

The valuation of the PCB sector presents a “pyramid-like” structure, with technological barriers and growth potential determining valuation levels.

6.2.1 Overall Valuation Level of the Sector

-

Overall Valuation Space: Institutions such as CICC believe that the current valuation of the PCB sector still has upward potential, primarily due to performance growth (some companies’ net profit growth exceeding 30%) not yet fully priced in.

-

Valuation Differences Across Segments::

-

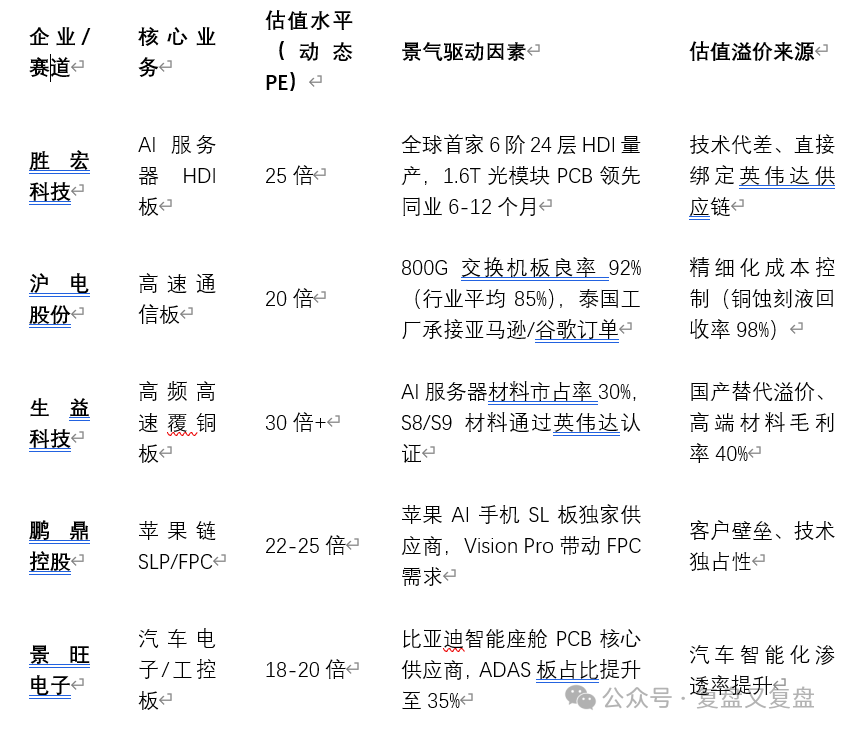

High-End PCBs (AI Servers/HDI/Substrates): Due to high technological barriers and tight supply-demand dynamics, leading companies enjoy valuation premiums, with dynamic PEs typically in the range of 25-40 times (for example, Shenghong Technology at 25 times, Huitian Technology at 20 times).

-

Mid-Low-End PCBs (Consumer Electronics Standard Boards): Intense homogeneous competition leads to PEs in the range of 15-20 times, with limited potential for valuation increases.

-

Upstream Materials (Copper-Clad Laminates/Copper Foil): Stable profitability (gross margins of 30%-40%), with leading companies like Shengyi Technology achieving PEs exceeding 30 times.

6.2.2 Valuation and Driving Factors of Key Companies

Table: Valuation and Prosperity Correlation of Representative Companies in the PCB Industry Chain (Based on 2025 Data)

6.2.3 Valuation Catalysts:

-

Short-Term Event-Driven: The release of new architectures (such as the Rubin architecture) at NVIDIA’s GTC conference has doubled the value of orthogonal backplane PCBs; the hot sales of Apple’s iPhone 17 have driven the valuation recovery of the industry chain.

-

Policy Support: Equipment update policies with subsidized loans (interest rates as low as 1.75%), and FC-BGA substrates included in national key projects, reducing corporate costs.

-

Cost Improvements: Fluctuations in copper prices and stabilization of copper-clad laminate prices have led to a year-on-year increase of 3-5 percentage points in PCB companies’ gross margins.

7 Financial Analysis of Leading Companies in the PCB Industry Chain

The financial analysis of leading companies in the PCB industry chain shows that the industry is benefiting from strong demand driven by AI computing power and automotive electronics, with leading companies achieving rapid growth through technological upgrades and capacity expansions.

The following table can help you quickly grasp the financial performance and core driving forces of the three leading companies.

Across the Entire Industry Chain: Resonating with the Waves of AI and Electrification in Automotive The core driving force behind the high growth of the three companies’ performances is directly or indirectly derived from the strong demand for AI computing infrastructure and automotive electronics. This also reflects that the current prosperity of the PCB industry is not universally thriving but is dominated by high-end demand, thus the growth dividends obtained by leading companies through technological advantages are more pronounced.

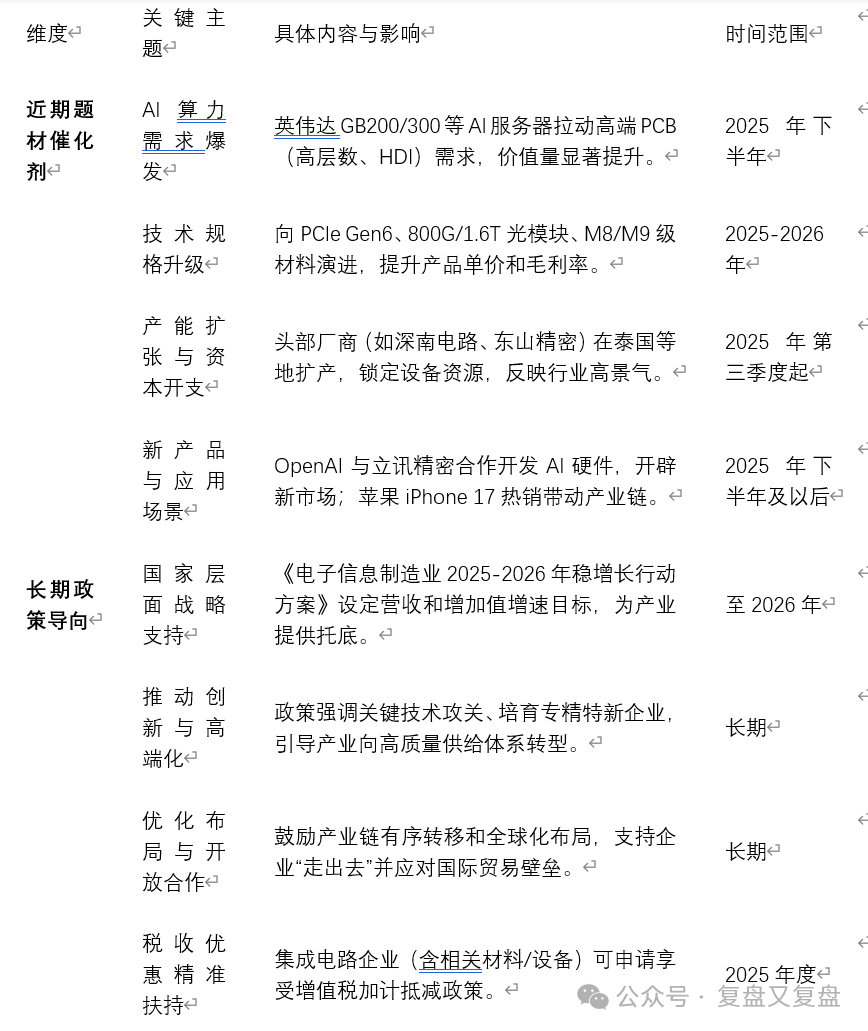

8 Recent Themes and Long-Term Policies

The PCB industry is currently in a development phase characterized by short-term catalysts and long-term support. The following table summarizes recent key thematic catalysts and long-term policy directions, helping you quickly grasp the core points.

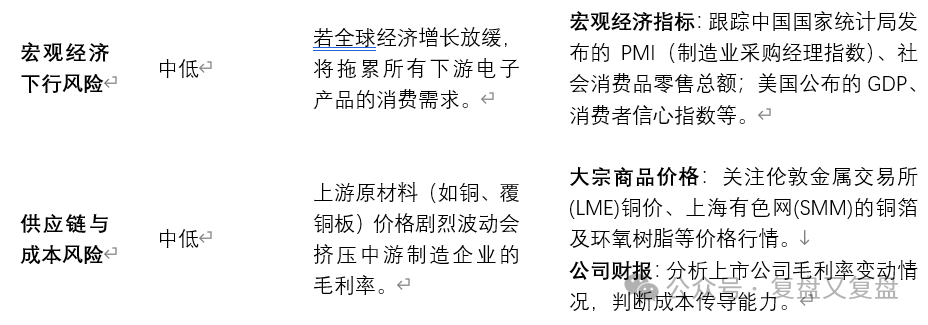

9 PCB Sector Potential Risk Matrix

The following table summarizes the main risk points currently faced by the PCB industry chain, their impact mechanisms, and key tracking indicators and data sources, facilitating dynamic monitoring.

🔍 Detailed Explanation of Key Risks

-

Beware of Valuation Bubbles and Sentiment Shifts: The most easily triggered risk currently is valuation adjustments. After significant increases, any minor disturbance could trigger profit-taking. You need to closely monitor changes in trading volume and the strength of leading stocks. For example, if stock prices reach new highs but trading volume continues to shrink, indicating a “top divergence” phenomenon, or if leading stocks first break important moving averages (such as the 30-day line), these are signals to be cautious.

-

Validate the Sustainability of High Growth Stories: The core supporting high valuations is the demand from AI servers, automotive electronics, and other fields. You need to closely verify whether these stories are being fulfilled as expected. Key tracking should focus on the financial meetings of leading industry companies (such as NVIDIA) and the capital expenditure plans of major downstream customers (such as major global cloud service providers). If signs of slowing demand growth or orders falling short of expectations are detected, it could catalyze a decline in the sector.

-

Monitor the Rhythm of Capacity Deployment: Be cautious of the risk of supply-demand imbalances that may arise from capacity expansions. It is recommended to regularly review industry reports (such as those published by Prismark and TPCA) and pay attention to global and regional capacity growth forecasts and utilization rate data. If capacity growth significantly exceeds demand growth, it is necessary to maintain caution regarding the industry’s profit outlook.

Disclaimer: This report was completed with AI assistance and contains AI-generated content (data may be inaccurate), representing personal opinions and not constituting investment advice! It has no commercial value!