1. Overview of the Electronics Industry: Demand Continues to Recover, Operations Steady with Growth

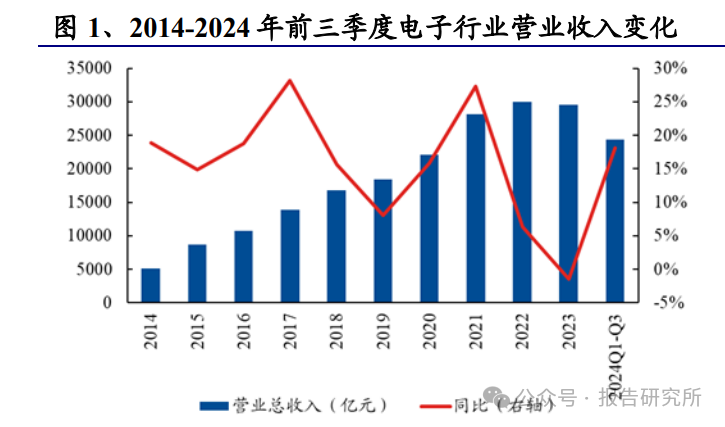

According to Shenwan Electronics, the total operating revenue and net profit attributable to shareholders of 469 companies in the electronics industry (excluding SMIC and Hua Hong) for the first three quarters of 2024 were 2.4329 trillion yuan and 103.5 billion yuan, representing year-on-year growth of 18.09% and 36.56%, respectively. In Q3 2024, the single-quarter operating revenue and net profit attributable to shareholders were 916.7 billion yuan and 40.6 billion yuan, with year-on-year growth of 19.04% and 20.24%.

In terms of profitability, the gross margin and net margin for the first three quarters of 2024 were 15.79% and 4.07%, respectively, with a year-on-year decrease of 0.26 and an increase of 0.12 percentage points. In Q3 2024, the gross margin and net margin were 15.75% and 4.15%, respectively, with year-on-year decreases of 1.25 and 0.51 percentage points, and quarter-on-quarter decreases of 0.22 and 0.25 percentage points. (Note: The above data is as of October 31, 2024.)

Overall, the operating conditions of the electronics industry in the first three quarters of 2024 showed significant improvement year-on-year, with Q3 revenue growth maintaining momentum. Due to fluctuations in exchange rates and demand recovery, profit growth has slowed. In the semiconductor sector, the trend of autonomous control in equipment is accelerating, with orders clearly increasing. Component companies are experiencing rapid growth, while materials continue to improve. Inventory levels for digital chips, memory chips, CIS, and packaging and testing are decreasing well, supported by a continued recovery in some downstream sectors, maintaining growth momentum. The analog and power sectors are also showing clear signs of bottoming out. In the consumer electronics sector, companies related to computing power in the Apple supply chain and PCBs are seeing continuous revenue growth, although profits are affected by exchange rates. Passive components, panels, and the Android supply chain remain relatively stable, awaiting the replacement cycle driven by edge-side AI.

From a valuation perspective, as of December 6, 2024, the Shenwan Electronics Index PE-TTM was 55.02 times, positioned at the 75th percentile over the past decade, indicating a historically high level.

By the end of Q3 2024, the total market capitalization of the electronics industry reached 7.15 trillion yuan, accounting for 8.51% of the total A-share market capitalization, ranking second, with a significant increase in total market capitalization, although the proportion has slightly decreased.

By the end of Q3 2024, the electronics sector accounted for 13.96% of the total market capitalization of public funds, with an overweight ratio of 5.45 percentage points, a decrease of 0.49 percentage points compared to Q2 2024, but still above the historical average.

2. Edge AI Initiates a Wave of Hardware Innovation, Sustained Growth in Computing Power Demand

Since the explosion of AI driven by ChatGPT, the development of AI has spread across various industries. According to the information equity report by Menlo VC, overall corporate AI spending has risen from 2.3 billion USD last year to 13.8 billion USD this year. The foundational models still account for the largest portion of spending, while the growth rate of model deployment and application layers is even faster, indicating that while data center construction is ongoing, AI is gradually being applied at the application level.

Previously, corporate AI applications merely enhanced existing human workflows, but they are now transitioning towards “fully automated processes.” Agents capable of handling complex, end-to-end processes and operating independently are emerging, moving from simple horizontal text and image generation to complex vertical application workflows.

As AI gradually lands in applications, large model vendors are beginning to focus on edge-side solutions. Compared to cloud solutions, edge-side large models can significantly reduce latency, enable local data processing, and provide personalized user experiences. Security, convenience, low latency, privacy, and diversity are the advantages of edge-side AI, which opens up better application spaces for large model vendors. Entering 2024, major large model vendors are starting to push for edge-side solutions, with OpenAI, Google, Microsoft, and Apple all releasing models or products suitable for edge-side applications, marking a new development stage for edge-side AI.

2.1. AI Phones and AI PCs Emerge, Driving Up Related Hardware Value

The official release of iOS 18.1 marks the launch of Apple Intelligence. On October 29, 2024, Apple pushed the official version updates of iOS 18.1, iPadOS 18.1, and macOS Sequoia 15.1 to users, with the highly anticipated Apple Intelligence feature officially going live. Specific features include enhancements to writing tools, intelligent upgrades to Siri, smart replies for emails and messages, new features in the photo application, and summaries of call records and transcriptions. In the developer beta of iOS 18.2, Apple further updated four major AI features: Image Creation, Visual Intelligence, Siri integrated with ChatGPT, and Writing Tools, representing Apple’s deepening involvement in AI applications for smartphones. Meanwhile, Cook stated in an interview that compared to the same period last year when iOS 17.1 was released, the speed of user downloads and installations for iOS 18.1 is twice as fast.

Qualcomm and MediaTek have successively released new processors, and major brands are actively laying out AI phones. On October 9, 2024, MediaTek released the Dimensity 9400, equipped with MediaTek’s new eighth-generation AI processor NPU 890, opening a new chapter for “edge-side video” and “edge-side training.” On October 22, Qualcomm released the Snapdragon 8 Gen 2, which has undergone significant architectural upgrades in several key areas, further materializing the concept of edge-side AI, especially in auditory and visual aspects. Domestic manufacturers also launched their flagship AI phones in October: Xiaomi 15, Honor Magic7, OPPO Find X8, vivo X200, etc. With AI phones emerging one after another, the penetration rate is expected to rise rapidly. IDC predicts that AI phone shipments will reach 170 million units in 2024, with a penetration rate of 15%. Counterpoint expects that by 2027, AI phone shipments will exceed 550 million units, with a penetration rate of about 43%, and the installed base is expected to reach 1.23 billion units, with rapid growth in shipments and a broad market space.

AI is accelerating its landing on the PC side, and the penetration rate of AI PCs is expected to rise rapidly. Global hardware leaders continue to launch AI processors, and AI large models are rapidly iterating, with AI PC shipments expected to grow rapidly. Canalys predicts that AI PC shipments will reach 44 million units in 2024, and are expected to reach 103 million units in 2025. The acceleration of AI on the laptop side is expected to drive a wave of replacement in the laptop industry, bringing new growth momentum.

Edge-side large models are continuously iterating, and parameters are expected to keep increasing. Currently, flagship models from several smartphone brands have already implemented large models on the edge side, such as the vivo X100 with its 7 billion parameter large model. The parameter scale of large models is still in the upgrading process, with Counterpoint predicting that the upper limit of local large model parameters will grow to 13 billion in 2024 and 17 billion in 2025. The growth in the parameter scale of large models will further expand the capabilities of generative AI phones and will also impose higher requirements on hardware, driving upgrades in various hardware aspects such as computing power scale, memory capacity, battery life, and heat dissipation.

2.1.1. Processors: Chip Manufacturers Iterating AI Processors, Continuously Enhancing Computing Power

AI phone processors are continuously iterating, driving performance upgrades for AI phones. In October 2024, MediaTek and Qualcomm successively released the Dimensity 9400 and Snapdragon 8 Elite chips, opening a new era for edge-side AI. The MediaTek Dimensity 9400 adopts TSMC’s second-generation 3nm process, integrating a more powerful and energy-efficient eighth-generation AI processor NPU 890, with edge-side multimodal AI computing performance reaching 50 Tokens/s. Compared to the Dimensity 9300, its large language model (LLM) prompt processing performance has achieved an 80% improvement, the execution performance of Stable Diffusion has doubled, and the text length for AI models has increased by 8 times, while power consumption has decreased by 35% year-on-year. The Snapdragon 8 Elite features the second-generation Qualcomm Oryon CPU, Qualcomm Adreno GPU, and an enhanced Qualcomm Hexagon neural processing unit (NPU). The performance of both the Oryon CPU and Adreno GPU is up to three times that of the previous generation, while the Hexagon NPU’s performance is up to 12 times that of the previous generation. As AI phone processors continue to iterate and upgrade, the performance of phones handling AI tasks will significantly improve.

Apple’s A-series processors continue to innovate in transistor count and computing power. The iPhone 16 series released this year supports Apple Intelligence across the board, and to support edge-side AI functions, Apple has further upgraded its chips. Both the A18 and A18 Pro adopt the world’s first second-generation 3nm process, with smaller transistor sizes, faster speeds, and higher energy efficiency; they use the latest Armv9 instruction set architecture, equipped with a 6-core CPU (2 performance cores + 4 efficiency cores), and a 16-core neural network engine optimized for running large generative AI models, with the AI computing power of the A18 Pro reaching 35 TOPS. Both chips have upgraded their memory subsystems, increasing the total memory bandwidth by 17%, a record high for iPhones, allowing the chips to utilize generative AI models “the fastest and most efficiently” through collaborative design with Apple Intelligence.

Global hardware leaders are actively launching AI PC processors, with performance continuously improving. Global chip leaders such as AMD, NVIDIA, Qualcomm, and Intel are actively introducing PC processors with AI capabilities, continuously enhancing computing power. AI-enabled processors are actively empowering PCs, driving the rapid development of AI PCs.

2.1.2. PCB: Enhanced Computing Power and Complex Structural Design Drive Up Soft and Hard Board Value

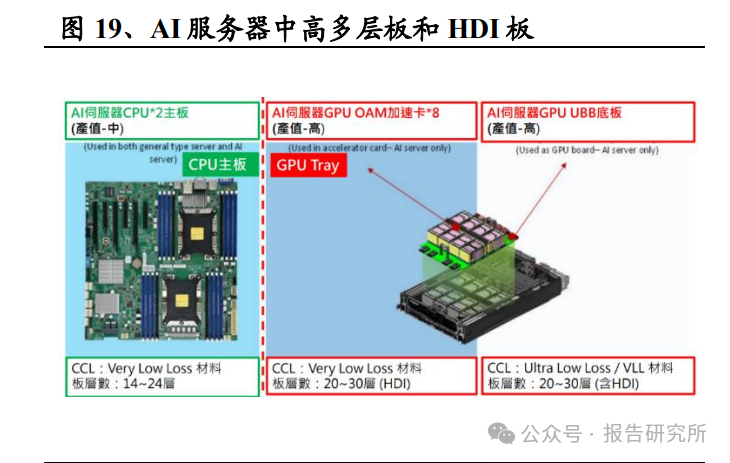

As edge-side AI processors upgrade in size and process, the value of motherboards is expected to increase. There are several possible ways: 1) Similar to the server side, due to the increase in chip size, the area of accelerator cards has significantly increased; the area of the GB200 accelerator card is several times that of the H100, and as data volume increases, the number of layers on the motherboard is also expected to increase. 2) Currently, mobile motherboards mainly use HDI technology, while computer motherboards are primarily multilayer through-hole boards. After upgrading to AI Phones/PCs, due to the improvement in chip processes, the line width and spacing of the motherboard need to be reduced. Ordinary PCBs can generally achieve a minimum line width and spacing of 70-80μm, while HDI can reduce the minimum line width and spacing to around 40μm through laser drilling of micro vias and stacked vias. SLP motherboards using mSAP technology can achieve a minimum line width and spacing of around 20μm. Based on currently launched AI Phone/PC products, we judge that the proportion of computer motherboards adopting HDI is expected to rise. For mobile motherboards, Android mainly adopts high-end HDI, which is expected to upgrade to SLP in the future. Apple has been using SLP motherboards since the iPhone X, with line widths and spacings around 30μm, which are expected to further decrease in the future.

3) From a materials perspective, high-speed, lightweight, good heat dissipation, energy-saving, and low-loss are the development directions. Traditional circuit boards use fiberglass as the core layer, filled with resin and then covered with copper foil, which has certain thickness limitations. Lianmao has developed a new generation of materials for SLP/HDI, RCC (Resin Coated Copper), which can eliminate the need for fiberglass, directly using resin for curing and then covering with copper foil, thus reducing the thickness of fiberglass, making PCBs lighter and thinner, overcoming the traditional solution’s minimum thickness limitation of 15-20 microns, while also improving signal quality and efficiency, reducing costs and weight. For computer motherboards, as computers increasingly approach small servers, high-speed materials M4 and M6 are also expected to be used in motherboard manufacturing. Additionally, FPC serves as the medium for signal transmission between various modules and motherboards in smartphones, and in the future, running large models on the edge will require receiving large amounts of audio, video, and image data, which will also impose higher requirements on FPC transmission performance, driving up its value.

2.1.3. Batteries: AI Increases Power Consumption, Driving Up Battery Capacity for Smartphones and PCs

Silicon materials have a high volume expansion rate, and steel shell batteries can effectively alleviate expansion compared to aluminum-plastic film. The volume expansion rate of silicon materials is 320%, while that of carbon materials is 12%. As smartphone battery anode materials shift towards silicon-carbon materials, the volume expansion rate will correspondingly increase. Currently, smartphones mostly use soft-pack batteries, whose shells are primarily made of aluminum-plastic film, which has ductility and low rigidity, causing swelling when stressed internally, leading to battery expansion. In contrast, steel shells have excellent processability, toughness, and forming capabilities, which can suppress battery expansion. In the future, the use of steel materials for battery shells is expected to become mainstream.

The iPhone 16 Pro is the first to use a steel shell battery, leading the trend for AI smartphone batteries. In this year’s iPhone 16 series, the iPhone 16 Pro has adopted a steel shell battery, which has a higher surface hardness than aluminum-plastic soft-pack batteries, providing better protection for the battery cell and certain heat dissipation effects. In terms of battery capacity density, the iPhone 16 Pro’s battery capacity is 3582mAh, which is an increase of 308mAh compared to the previous generation, achieving an energy density of 764Wh/L, an improvement over the previous generation. We judge that as the computing power consumption of AI smartphones increases, battery capacity density will continue to upgrade.

The theoretical capacity advantage of silicon-carbon anodes is significant, and they are expected to be an important upgrade direction for enhancing battery density. According to Counterpoint Research, the average battery capacity of global smartphones has increased from 3000mAh in 2018 to 4500mAh in 2022. Currently, mainstream consumer battery anode materials are primarily graphite. Compared to graphite, silicon-based anode materials can achieve a theoretical capacity of 4000mAh/g, far exceeding the theoretical capacity of mainstream graphite anodes at 370mAh/g. Silicon-carbon composite materials are expected to be one of the future directions for enhancing battery energy density. Several smartphones have already adopted silicon-carbon anode batteries, leading to an increase in AI smartphone battery capacity. Currently, many smartphone brands have adopted silicon-carbon anode batteries, such as Honor, Huawei, OPPO, and vivo, effectively improving battery capacity and energy density. Based on currently released AI smartphones, brands like Honor, Samsung, Xiaomi, OPPO, and vivo have all upgraded their battery capacities, with varying degrees of improvement. In the future, as AI continues to land on smartphones, the parameter scale of edge-side large models continues to upgrade, and AI applications are continuously launched, battery capacity is expected to continue to upgrade, benefiting battery manufacturers.

Laptop battery capacities are gradually increasing, and AI empowerment is expected to accelerate this process. Taking Lenovo’s Xiaoxin Pro series as an example, in 2019, Lenovo released the Xiaoxin Pro with a battery capacity of 56Wh. In 2021, the Xiaoxin Pro 14’s battery capacity increased by 5Wh to 61Wh, and in 2023, the Xiaoxin Pro 14’s battery capacity was further increased to 75Wh. The latest release, the Xiaoxin Pro 16 AI version in 2024, has also seen an increase in battery capacity to 84Wh. Overall, laptop battery capacities are showing an upward trend, and with the landing of AI on the PC side, power consumption may increase, further driving battery capacity upgrades. Based on currently released AI PCs, several models have already upgraded their battery capacities, such as the Lenovo Xiaoxin Pro 16, Lenovo ThinkPad T14p, Lenovo YOGA Pro 16s, Microsoft Surface Pro, ASUS Zenbook 14, and MSI Prestige 16 AI EVO. In the future, as AI continues to land on the PC side and AI On phase PCs are continuously released, battery capacity is expected to continue to upgrade, benefiting battery manufacturers.

2.1.4. Memory: The Landing of Large AI Models on the Edge Drives Up Storage Capacity

The landing of large models on the PC side requires sufficient memory space. AI PCs need to have enough storage space to store model parameters and data for offline operation of personal large models. According to TrendForce, Microsoft has set 16 GB as the minimum system requirement for AI PCs. According to hardware data, when running a 7 billion parameter LLaMA model on a CPU, under INT4 quantization, the landing of large models on terminals is expected to bring about a 3.9-7.5GB increase in PC memory demand, while under INT8 quantization, it is expected to bring about an 8.5-10GB increase in PC memory demand.

Some existing AI PC memory has already been upgraded, and future models with larger parameter models are expected to further increase memory. Based on currently launched AI PC models, many models have significantly increased their starting memory, such as Lenovo YOGA Air 14s and ThinkPad X1 Carbon, where the starting memory has increased from 16GB to 32GB. In the future, as larger parameter models land on the PC side, storage capacity is expected to further increase, benefiting storage-related companies.

2.1.5. Heat Dissipation: The Scale Upgrade of Edge-Side Large Models Drives Up Both Quantity and Price of Heat Dissipation Materials

VC vapor chambers combined with graphite and graphene are gradually becoming the mainstream heat dissipation solution for smartphones. The development history of smartphone heat dissipation can be roughly divided into three stages: initially dominated by graphite heat dissipation films, gradually evolving to heat pipe cooling, and in October 2018, Huawei launched the Mate20X, which used VC vapor chambers and graphene materials for heat dissipation. Since then, the heat dissipation solution primarily based on vapor chambers, supplemented by graphite and graphene heat dissipation technologies, has gradually become mainstream. VC vapor chambers have significant advantages in heat dissipation efficiency and are accelerating towards thinner, simpler structures and lower costs, with continuous technological iteration.

The heat dissipation performance of the iPhone 16 Pro series has significantly improved. As the parameter scale of edge-side large models continues to increase, the related data volume and computational demand are experiencing explosive growth, leading to heat generation and making heat management increasingly important. Generally, the larger the area of the VC vapor chamber, the better it can reduce hot spots. Taking the iPhone 16 Pro series as an example, the large-sized heat dissipation film has moved to the aluminum alloy inner frame, completely covering the rear camera, mainboard core heating area, and battery position, working in conjunction with the aluminum alloy inner frame below for uniform heat distribution. In the rear cover layout, compared to the previous generation, which only covered the wireless charging coil, the new heat dissipation film extends from the coil outward, covering about 60% of the rear cover area to enhance heat dissipation efficiency. In the future, as AI large models accelerate their landing on smartphones and parameter scales increase, it is expected to impose more requirements on heat dissipation, such as larger vapor chamber areas or increased use of graphite materials, driving up both the quantity and price of heat dissipation materials.

2.2. Glasses Expected to Become Important Carriers for Future Edge-Side AI Agents

Glasses and headphones are expected to become important carriers for future edge-side AI. As edge-side AI technology matures, more and more major companies are focusing on smart and wearable devices. In 2023, Apple released the Vision Pro, Meta launched AR glasses, ByteDance released AI headphones, and various smartphone manufacturers launched AI phones. We believe that glasses and headphones are likely to become important carriers for edge-side AI for several reasons: 1) Glasses can enhance human-computer interaction, serving as external interfaces for “visual” and “auditory” interactions, providing stronger interactivity; 2) Glasses and headphones are portable and lightweight, not burdening users; 3) Price advantages, as glasses and headphones are relatively inexpensive compared to other application terminals, they are likely to open up market space more quickly. The “Ray-Ban Meta” smart glasses have sparked a wave of AI glasses. In September 2023, Meta and Ray-Ban launched the second-generation co-branded smart glasses, Ray-Ban Meta (priced the same as the first generation), which are AI glasses that can awaken AI functions through dialogue, featuring capabilities such as photography, conversation, and music playback. Additionally, in 2024, they will undergo AI updates, with the large model enabling voice interaction, object recognition, and text translation. The Ray-Ban Meta smart glasses exceeded 300,000 units in shipments in Q4 2023, nearly matching the total sales of their first-generation product. According to data from The Verge cited by the photonic phenomenon, as of May 2024, global sales of Ray-Ban Meta smart glasses have surpassed 1 million units, with expected shipments for the entire year of 2024 likely to exceed 1.5 million units.

Meta has released its first AR smart glasses, indicating significant potential in the AI+glasses market. At the 2024 MetaConnect conference, Meta unveiled its first AR glasses prototype, codenamed Orion. Weighing only 98g, the glasses feature a magnesium frame and are equipped with seven cameras. Orion supports AI voice, gesture tracking, eye tracking, and allows users to control it using neural signals through an EMG wristband. Users can wear the glasses to open multiple MetaHorizonApp windows for multitasking or use MetaAI to recognize real-world objects.

The AI+glasses market is gradually rising. With the rapid development of virtual reality and augmented reality technologies, the AI+glasses market is gradually emerging. According to IDC data cited by Sina VR, global AR glasses shipments reached 480,000 units in 2023, while smart glasses shipments reached 1.01 million units. In the first quarter of 2024, global AR glasses shipments reached 100,000 units, a year-on-year increase of 56%; smart glasses shipments reached 260,000 units, a year-on-year increase of 217%. The future development market space for AI+glasses is vast. The AI glasses industry chain is currently in a relatively early stage. If they do not have display functions, the value of SoC chips and complete devices is relatively high, with SoC chip manufacturers including Qualcomm, Hengxuan Technology, and Juchip Technology, while complete device brands include Ray-Ban, Meta, Snap, Huawei, Meizu, Rokid, XREAL, and others. For complete devices with display functions, i.e., AR glasses, the optical and display components represent a new value-added segment. Optical components include LCos, Micro OLED, and Micro LED solutions, with major industry players including JBD, Visionox, Sony, Weir, Huacan Optoelectronics (overseas group coverage), GoerTek, and Fuguang Optoelectronics; display components include BB and waveguides, with major industry players including DigiLens, Crystal Optoelectronics, GoerTek, Lantech Optics, MoJie, Lumus, and WaveOptics.

2.3. 800G Ethernet Switches Volume Production, CPO Expected to Become a New Packaging Trend

Global leaders such as Microsoft, META, Google, Apple, and Amazon are increasing capital expenditures in data centers, with a continuous upward trend since Q3 2023 for five consecutive quarters. In Q3 2024, total capital expenditures reached a new quarterly historical high, and major CSP manufacturers remain optimistic about future Capex guidance.

Global AI chip leader NVIDIA continues to exceed expectations, demonstrating the sustainability of high demand for computing power. NVIDIA’s FY25Q3 revenue was $35.1 billion, with a quarter-on-quarter increase of 17% and a year-on-year increase of 94%. Data center revenue reached a record $30.8 billion, with a quarter-on-quarter increase of 17% and a year-on-year increase of 112%. The company expects FY25Q4 revenue to reach $37.5 billion (with a 2% fluctuation), continuing to grow, proving confidence in AI demand.

In data center construction, switches and GPUs are core hardware for AI computing power. Referring to Meta’s 24K Infiniband cluster solution, which uses 24,576 H100 chips, if we estimate the total cost of ownership over a four-year lifecycle, it requires an investment of about $1.4 billion, with H100 and Infiniband switches being the main cost sources, requiring about $599 million and $193 million, respectively, accounting for about 66% and 21% of the total construction cost after excluding related operating costs (WACC, hosting costs, and electricity costs).

Driven by AI, the market scale for switches continues to grow. According to IDC data cited by SDNLAB, the global Ethernet switch market reached $44.2 billion in 2023, a year-on-year increase of 20.1%, with data center market revenue growing by 13.6% year-on-year, especially for 200/400 GbE switches, which saw a 68.9% increase in revenue throughout 2023. Since 2024, the scale of high-speed switches has maintained high growth, with total revenue for the 200/400 GbE switch market increasing by 104.3% year-on-year and 35.7% quarter-on-quarter, indicating strong demand from data centers for high-speed Ethernet switches.

As data center construction deepens, the pace of switch iteration and upgrades is accelerating. According to a report by Arista cited by Dell’Oro, the trend of switch high-speed continues to evolve, with 800G switches expected to see rapid volume production around 2025 and become mainstream by 2026. The addition of AI will further accelerate the volume production of 800G switches. Meanwhile, 1.6T switches will continue the penetration trend of 800G and will gradually be introduced in the coming years. According to LightCounting statistics, sales of InfiniBand switch ASICs grew by 2.3 times in 2023, with an expected compound annual growth rate of 25% from 2024 to 2029. In terms of Ethernet, due to reduced investments in computing nodes within cloud data centers, sales of Ethernet switch ASICs remained flat in 2023, but this market is expected to recover growth in 2024 and then grow steadily, with an expected compound annual growth rate of 14% for Ethernet switch ASIC sales from 2024 to 2029.

As the demand for transmission rates increases, PCB losses will also increase, necessitating the use of lower-loss CCL materials to match equipment requirements and increase the number of layers. For example, the H3C 400G switch has introduced multiple Ultra Low Loss layer materials to meet loss requirements, and as it upgrades to 800G or even 1.6T, the material requirements will only become higher. Additionally, similar to the upgrades of general-purpose servers, according to Lianmao’s statistics, every time a general-purpose server iterates a generation, the number of PCB layers increases by 4-6 layers, which will also lead to a significant increase in PCB value. According to industry chain research, the number of PCB layers for 800G switches is expected to exceed 30 layers, using M8 grade CCL materials, and further upgrades to 1.6T will likely see an increase in PCB layers and materials. Driven by AI demand, the demand and value of PCBs related to Ethernet switches are expected to see significant increases, and we believe the 800G switch industry chain is likely to drive continuous growth in the PCB industry.

Moreover, due to the increasing complexity of data centers and computing tasks, CPO (Co-packaged optics) technology, which tightly integrates optical and electronic components within a single package, significantly shortens signal transmission paths, reduces system power consumption, and enhances bandwidth density, is seen as a key technology for future data centers and high-performance computing networks. Traditional pluggable optical modules are connected to switch chips via copper wires, which are limited by signal attenuation, interference, and power consumption, making it difficult to provide sufficient bandwidth density at higher data rates, leading to latency and power consumption issues. CPO integrates optical modules directly onto the switch ASIC substrate, reducing electrical connections and effectively addressing signal integrity issues.

According to IDTechEx, the Co-packaged optics (CPO) market is expected to exceed $1.2 billion by 2035, with a compound annual growth rate (CAGR) of 28.9% from 2025 to 2035. As the usage of CPO increases, the demand for substrates is also expected to grow.