【Beiyu Jincheng】

(Financial Concepts, Green Finance, Embedded Finance)

Financial Concept: Green Finance

Green Finance: Financial Innovation and Ecological Co-construction under the Dual Carbon Goals

Authors: Han Shuyan, Yan Yunqiao

In the wave of green transformation led by the dual carbon goals, green finance has grown into a core link connecting capital markets and green development. It is not only a financial innovation that promotes the development of environmental protection, energy conservation, and clean energy, but also an important support for achieving sustainable economic and social development. The following analysis will cover definitions, characteristics, values, and development paths of this hot financial topic.

1

1. Essential Deconstruction: Anchoring Green Development with New Financial FormsFinancial New Forms

Green finance refers to financial services provided to support environmental improvement, respond to climate change, and promote efficient resource utilization. Its core is to guide capital flow towards green projects and industries through investment and financing, risk management, and other financial means. It encompasses a wide range of products, including green bonds, green loans, green funds, and green insurance. In recent years, the scale of green finance in China has continued to expand. By the end of 2024, the outstanding amount of green bonds is expected to exceed 8 trillion yuan, and the balance of green loans will exceed 28 trillion yuan, making it one of the largest green finance markets in the world, providing stable funding support for projects such as photovoltaic power stations, new energy vehicles, and sewage treatment.

2

2. Characteristics and Causes: Dual Driving Forces of Policy Dividends and Market Demand

Green finance has three distinct characteristics: strong policy orientation, prominent social benefits, and stable long-term returns. Its rapid development stems from the superposition of multiple demands. From a national perspective, the green transformation under the dual carbon goals requires huge capital investment, which cannot be covered solely by fiscal funds and needs to rely on the financial market to fill the gap. From the enterprise perspective, green industry projects generally have long investment cycles and high upfront costs, making traditional financing models difficult to match, thus creating a demand for specialized green financial products. From the investor’s perspective, with the enhancement of environmental awareness, the concept of responsible investment that pursues financial returns alongside environmental benefits has gained popularity, driving funds towards green assets. At the same time, government work reports have emphasized the development of green finance for many years, and the structural monetary policy tools’ inclination towards policy dividends has further accelerated market expansion.

3

3. Value Examination: Dual Responsibilities of Economic Transformation and Risk Prevention

The value of green finance presents a dual effect. As a “booster” for economic transformation, it addresses the pain points of financing difficulties and high costs for green projects, promotes energy structure optimization and industrial upgrading, while also giving rise to a diversified product system, expanding the business boundaries of financial institutions, forming new profit growth points, and achieving a unity of economic and ecological benefits. However, challenges also exist in development, such as the risk of “greenwashing” in some projects, non-unified green standards, and insufficient information disclosure, which may trigger a market trust crisis that needs to be prevented through institutional construction.

4

4. Future Path: Coordinated Development of Standardization and Diversification

The high-quality development of green finance requires the establishment of an ecological system characterized by “policy guidance, market dominance, unified standards, and controllable risks.” The core focuses on four aspects: first, improving the standard system to unify the definition and assessment standards of green projects, eliminate “greenwashing” behaviors, and strengthen the supervision of information disclosure during the duration; second, enriching product supply by encouraging the development of innovative tools such as green REITs and carbon-neutral funds to meet the financing needs of different entities; third, strengthening policy coordination to optimize support policies such as green finance tax incentives and interest subsidies, promoting medium- and long-term funds to enter the market for green investment; fourth, improving risk control mechanisms by using financial technology to establish environmental risk assessment models for green projects, enhancing risk identification and management capabilities.

Green finance is an inevitable choice for the financial system to respond to the demands of the times. It reflects the inadequacy of traditional finance in adapting to the needs of green development and highlights the core value of financial innovation in serving national strategies. Only by continuously deepening market-oriented and rule-of-law reforms, and addressing key links such as standard unification, product innovation, and risk prevention, can green finance truly become the engine of ecological protection, safeguarding ecological security while injecting lasting momentum into high-quality development.

Hot Terms in Financial Technology

Embedded Finance: The Invisible Engine Reshaping Business Ecosystems

Author: Xu Jiahao

The digital economy is surging, and an “invisible” financial revolution is taking place.

It does not occupy the desktop like a star app, but quietly penetrates into e-commerce, ride-hailing, travel, takeout, social media… all the non-financial scenarios you are accustomed to. In the past, finance was a “destination”—to transfer money, you had to open a bank; to buy insurance, you had to search for an insurance company. Now, finance has become an “instant function”—the installment button appears the moment you place an order; during the ride, you can add travel insurance with one click; if the order is overdue, compensation is instantly credited to your account.

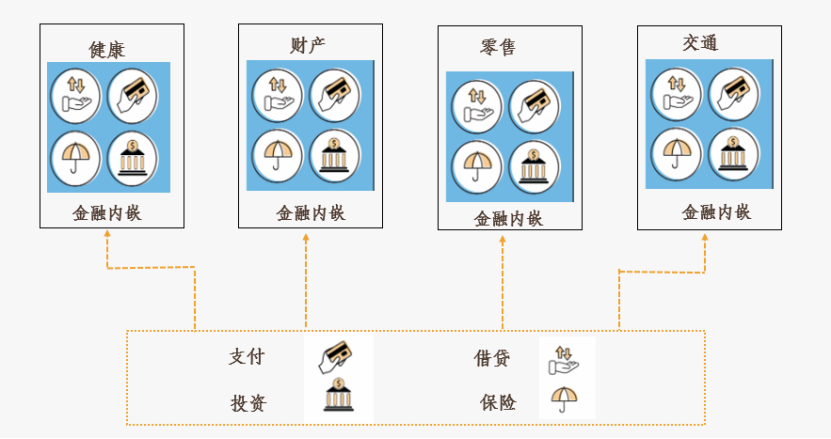

Embedded finance breaks down granular services such as payment, lending, insurance, and wealth management into APIs, seamlessly integrating them into others’ business processes like Lego. It is no longer product-centered but scenario-centered: wherever the user is, finance breathes there, even making users forget the existence of finance.

This is not a simple technical integration but a “core replacement” of business paradigms—from “selling financial products” to “managing scenario ecosystems,” where traffic, data, and funds converge, and profit statements are rewritten.

1

1. The Three Pillars of Embedded Finance and Value Restructuring

The rise of embedded finance relies on the convergence of three forces: technology, market, and consumer behavior.

1. Technological Empowerment

Open banking APIs are the cornerstone of embedded finance. They allow non-financial platforms to securely connect to the backend systems of banks and financial institutions through standardized interfaces, thus accessing core functions such as payment, account information, and credit assessment. Cloud computing and microservices architecture make the integration of these financial capabilities as flexible and efficient as “building blocks.”

2. Market Expectations

Consumers, especially millennials and Generation Z, have long been accustomed to the digital experience of “one-click solutions.” They have very low tolerance for lengthy processes and switching between multiple apps. The seamless experience provided by embedded finance caters to this extreme pursuit of convenience and immediacy.

3. Business Value

For non-financial platforms, embedded finance is a powerful tool for enhancing user loyalty and opening up new revenue sources. By reducing friction in transaction processes, it significantly increases conversion rates; by providing value-added financial services, it enhances user stickiness and upgrades the single traffic monetization model to a high-value financial technology model.

2

2. Core Areas and Case Analysis

1. Embedded Payments: The Cornerstone of E-commerce and the Sharing Economy

Embedded payments are the most mature and widespread application of embedded finance. They transform the payment process from “redirecting” to “embedding,” becoming part of the user experience.

(1) Case Study: Shopify & Shopify Payments

Shopify, as a leading global SaaS e-commerce platform, owes much of its success to its embedded payment solution—Shopify Payments. In the early days, Shopify merchants had to connect to third-party payment gateways like PayPal and Stripe, a cumbersome process that incurred additional transaction fees.

Shopify Payments is directly embedded into the merchant’s backend management system. Merchants can activate it with one click when setting up their stores, without the need for technical integration, and all transaction data seamlessly connects with the store’s orders, inventory, and customer data. This not only simplifies operations and reduces costs for merchants but, more importantly, allows Shopify to analyze merchants’ operational conditions more accurately by mastering payment data, laying a solid foundation for subsequent services like embedded credit (Shopify Capital).

(2) Analysis: Through embedded payments, Shopify has built a moat for its business ecosystem. Payments are no longer just a tool but a core part of its value proposition, firmly locking merchants into its ecosystem and paving the way for the expansion of its financial services.

2. Embedded Lending: Making Funds “Instantly Available” in Scenarios

Embedded lending integrates loan functions into specific consumption or business scenarios, providing “timely assistance” solutions when users face funding shortages.

(1) Case Study: Meituan and Meituan Business Loan

Meituan, as a leading life service platform in China, connects millions of restaurants, hotels, and entertainment businesses. The platform deeply understands the financing difficulties faced by these small and medium-sized merchants when expanding stores, purchasing equipment, and preparing for peak seasons.

Meituan Business Loan was born out of this need. It is directly embedded into the Meituan merchant app. When the platform analyzes data and determines that a merchant’s operational status is good and has potential funding needs, it may display a credit limit in the merchant’s backend. Merchants only need to perform a few simple operations, and funds can be quickly credited without collateral. The core of its risk control lies in the exclusive data accumulated by the Meituan platform: merchant transaction flow, user reviews, order growth rates, repurchase rates, etc. This real-time, multidimensional data reflects the merchant’s repayment ability more accurately than traditional bank credit reports.

(2) Analysis: Meituan Business Loan perfectly exemplifies “scenario equals risk control.” It deeply binds financial services with merchants’ operational pain points, achieving a full-process scenarioization of “pre-loan, during loan, and post-loan.” For merchants, financing has become unprecedentedly convenient; for Meituan, this not only creates profits but also promotes the prosperity of the entire platform ecosystem through financial support.

3. Embedded Insurance: Achieving “On-Demand” and “Invisible” Protection

Embedded insurance integrates relevant insurance products as options into specific stages of the purchasing process, achieving precise matching of risk protection and consumer behavior.

(1) Case Study: Tesla and Embedded Car Insurance

Tesla is not just a car company; it is also a technology and financial services company. It provides embedded insurance services for its car owners. When car owners purchase vehicles through the Tesla app or website, they can directly select and purchase Tesla’s self-operated insurance products.

A more advanced form is its behavior-based insurance. Through embedded telematics technology, Tesla can collect real-time driving data from car owners (such as mileage, number of hard brakes, usage of autopilot, etc.) and dynamically adjust premiums based on this data. Safe drivers can receive lower premiums, achieving personalized and fair pricing.

(2) Analysis: Tesla’s embedded insurance transforms insurance from a “one-time purchase” into a continuous service deeply tied to vehicle usage. It disrupts the traditional insurance pricing model, achieving “personalized pricing” while enhancing interaction and stickiness between car owners and the brand, forming a perfect closed loop of “manufacturing cars – selling cars – insurance – data collection – optimizing services.”

3

3. Conclusion

The essence of embedded finance is the evolution of business from “traffic thinking” to “user value thinking.” It no longer views users as the endpoint of monetization but creates new business value by deeply integrating into every aspect of their lives and production while solving specific problems.

For all enterprises, understanding and embracing embedded finance is no longer about chasing a trend but about building core competitiveness for the future. This silent transformation is redefining the boundaries of finance and business, shaping a new economic landscape that is more intelligent, convenient, and personalized.

Industry Chain Analysis

Lithium Battery Industry Chain

Author: Xu Ziwei

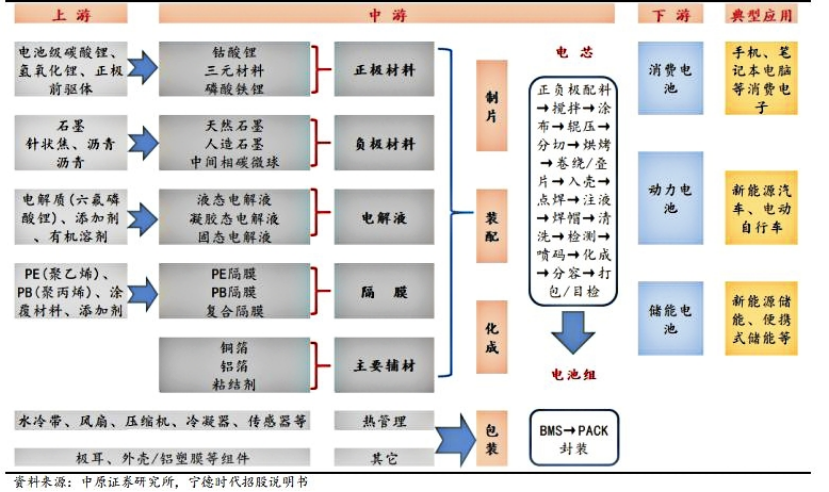

Figure: Lithium Battery Industry Chain Diagram 1

The lithium battery industry chain follows a three-layer structure of “materials – cells – applications,” forming a collaborative system of “technology – manufacturing – services,” with value distribution exhibiting a “smile curve” characteristic.

Upstream—Materials and Core Components

Key resources: Lithium, cobalt, nickel, and other minerals form the cost base, with lithium resources accounting for over 40% of the cost of positive electrode materials. Global lithium resources show a supply pattern of “Western Australia lithium mines, South American salt lakes,” with Chinese companies ensuring supply chain security through overseas mergers and acquisitions.

Core materials: Positive electrode materials (determining energy density, with the highest value proportion), negative electrodes, electrolytes, and separators (with high technical barriers) are the four key materials. High-end separators and high-nickel ternary positive electrodes are led by top companies in China, Japan, and South Korea, with the domestic production rate continuously increasing.

Midstream—Cell Manufacturing and Integration

Cell manufacturing: This segment requires heavy assets, with significant economies of scale, accounting for about 35%-40% of the value. Global production capacity is concentrated in China, with giants like CATL and BYD leading the way, but facing pressures from overcapacity and price wars.

System integration: Integrating cells into battery packs (PACK) involves core technologies of BMS (Battery Management System), which directly affect safety and performance, and is key to enhancing added value. According to data from GGII, in 2023, the installed capacity of power batteries in China accounted for over 60%.

Downstream—Applications and Service Ecosystem

End applications: Power batteries (new energy vehicles) are the largest demand engine, accounting for over 70%; the energy storage market is rapidly rising alongside photovoltaic and wind power, becoming the second growth curve; the consumer electronics market remains stable.

Recycling: An emerging high-value segment driven by policy, achieving value from recycling valuable metals such as lithium and cobalt from retired batteries, is key to the green closed loop of the industry chain.

Core logic: The value of the industry chain is tilted towards upstream resources and core materials, as well as downstream brand services and recycling. Currently, China has achieved global leadership in manufacturing scale and market share, but upstream resource supply security, key material iteration, and global green trade barriers are key challenges for sustained competitiveness in the future.

[1] Image source: Zhongyuan Securities Research Institute, CATL prospectus

[2] Data source: Reports from the Lithium Industry Branch of the China Nonferrous Metals Industry Association, Bloomberg New Energy Finance (BNEF), China Automotive Power Battery Industry Innovation Alliance (CBEA), and annual reports from GGII

Editor | Financial Society

Initial Review | Lu Xuanyu, Zhang Shuo Nan

Final Review | Liao Dingyao

Final Approval | Chen Sijia