At the latest 2025 US-Saudi Investment Forum, Musk stated that he believes artificial intelligence and robotics will eliminate poverty and make everyone wealthier.

He later added on X that people will receive extraordinary health insurance and various things that are more interesting than current games.

He also mentioned a prerequisite: We need to ensure that artificial intelligence places a high value on truth and beauty, so that this can become a reality in the future.

Additionally, he believes that poverty is an engineering problem. Of course, he also mentioned in a chat on X that the poverty he refers to is absolute poverty, not the relative poverty that people feel psychologically. Implicitly, this means that the wealth gap will still exist, and may even persist.

Undoubtedly, Musk’s extremely optimistic sentiment has given the field of embodied intelligence more momentum and attention, as we can see various major groups accelerating in venture capital, startups, and the stock market.

Unprecedented Heat for Embodied Intelligence

This year, “embodied intelligence” has become the second hottest concept after large models. According to Wind data, as of October 31 this year, the secondary market’s embodied intelligence index has risen over 60%, and the robotics index has also exceeded 35%.

To explain briefly, embodied intelligence refers to an intelligent system that perceives and acts based on a physical body, meaning artificial intelligence applied to a body with a non-fixed form, currently including various forms such as quadruped robots (robot dogs), wheeled robots, and humanoid robots. Among them, humanoid robot technology is the most challenging and complex, and it is widely believed in the industry that humanoid applications have the broadest space, making it the hottest direction.

Especially this year, which is also referred to as the year of mass production for humanoid robots, has achieved critical breakthroughs in policy support and industry chain maturity, beginning to transition from laboratories to real commercial applications.

However, who will become the industry leader and go public first remains full of suspense and competition.

Humanoid robot development requires continuous investment, and an IPO can provide long-term stable funding to support technological development. More importantly, being a publicly listed company provides a certain level of reliable trust endorsement, meaning it has passed the “initial stage of making promises” and can occupy a natural advantage when vying for large orders and collaborating with leading enterprises. This also means that an IPO is no longer merely a financing act, but a strategic positioning concerning future survival and development rights.

“Each Showing Their Talents” in Going Public

To go public, the currently leading companies, Yushu and Zhiyuan, have made a series of unusual moves.

First is Yushu, as the market leader in humanoid robots, Yushu is still not satisfied with the current market price, believing it has not hit the bottom yet.

On July 25, less than a week into the counseling period, Yushu launched its bipedal humanoid new product, Unitree R1. Starting at 39,900 yuan, weighing 25 kg, with 26 joints, and integrating voice + image multimodal large models, R1 has once again pulled the price anchor of humanoid robots down a notch.

Yushu’s wheeled dual-arm robot G1-D

On November 13, Yushu launched a new full-stack data collection training solution, introducing the wheeled dual-arm robot G1-D for the first time. It has 19 degrees of freedom, a vertical working space of 0–2m, dual cameras + high-definition cameras on the wrist, and an optional 1.5m/s mobile chassis, supporting full-process data collection, labeling, asset management, and distributed training, integrating into the “data-model-deployment” closed loop.

Some media voices believe that Yushu only has advantages in price and hardware capabilities, lacking long-term competitiveness. But is that really the case?

Yushu Technology’s business path adopts a gradual expansion and breakthrough strategy. With the large-scale sales and profitability achieved by quadruped robots, Yushu has accumulated experience in motors, reducers, and global channels, gradually expanding from the relatively low technical difficulty of quadruped balance to biped humanoid robots.

In terms of finance, Yushu disclosed that it has achieved profitability for five consecutive years since 2020, reaching a revenue milestone of 1.84 billion yuan in 2023, with a net profit of 210 million yuan, and in recent years, the net profit has exceeded 300 million yuan. This level is enough to surpass some listed companies, indicating that Yushu’s commercialization path has been initially validated and is not merely a startup relying on financing for survival.

Previously, there were rumors in the market that Zhiyuan was going to go public in Hong Kong, and many netizens were already preparing to subscribe to Zhiyuan’s IPO. However, unexpectedly, Zhiyuan took the lead in July by achieving listing through the acquisition of Shangwei New Materials, becoming “the first A-share humanoid robot stock”, creating a stock price surge of 15 times, from 7.78 yuan/share to a peak of 132.1 yuan/share. It is not an exaggeration to say that at least half of the heat in the stock market for robots this year comes from Shangwei New Materials.

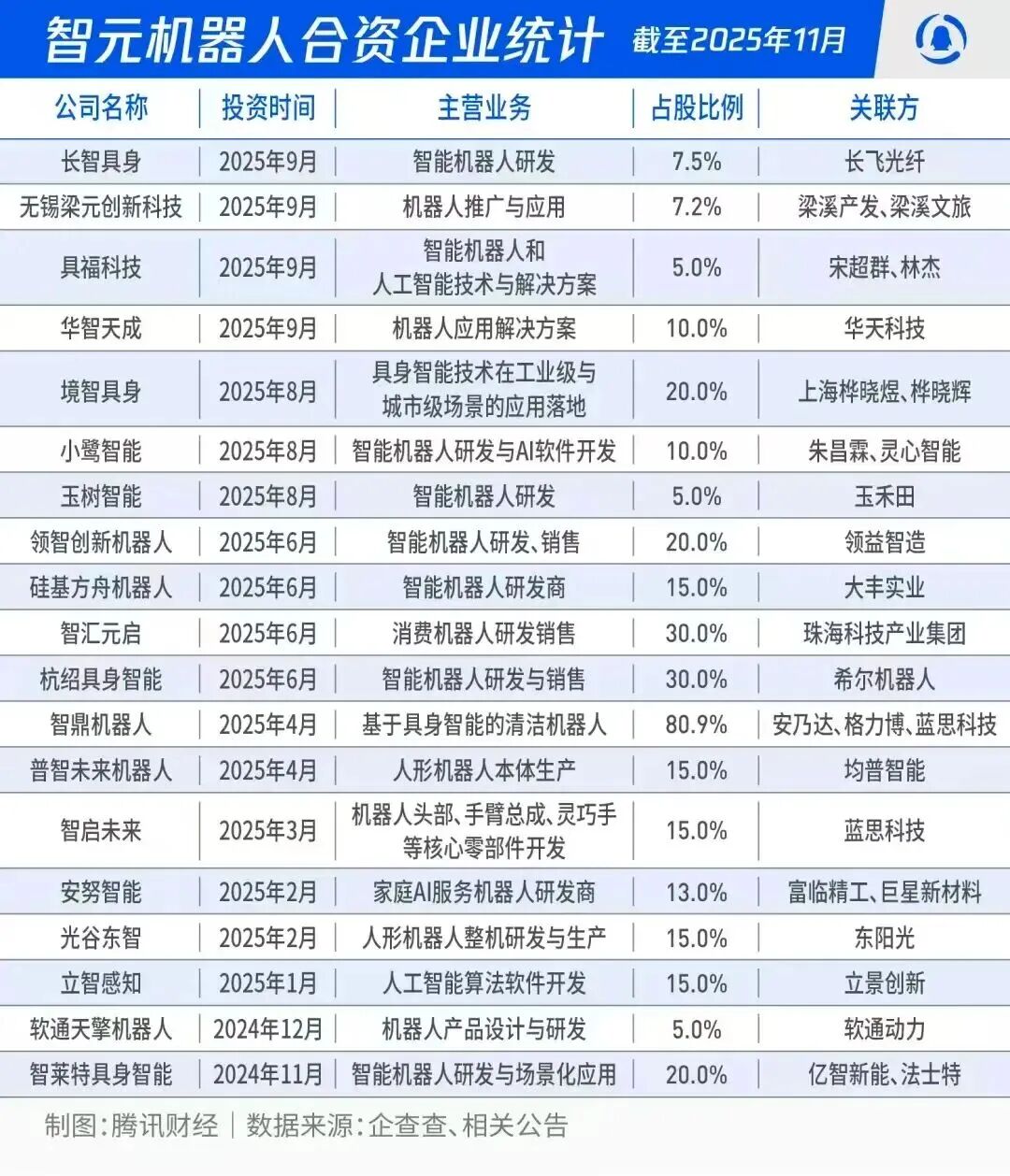

According to Qichacha data, Zhiyuan has intensively invested in nearly 30 startups within a year, covering core components (such as Fuxing Motors, Qianjue Robotics), AI brains (such as Lingchu Intelligence, Xingyuan Intelligent Robotics), and scene implementation (such as Feikuo Technology).

According to Tencent Finance, to support this investment landscape, Zhiyuan has also jointly established a multi-billion yuan embodied intelligence industry fund with Hillhouse Capital and launched the “Zhiyuan A Plan”, aiming to incubate over 50 early-stage projects.

If relying solely on Zhiyuan’s financing capabilities is clearly insufficient to support this large-scale operation, its latest two rounds of financing have led to a valuation exceeding 15 billion yuan, but last year’s revenue was only 100 million yuan. High valuation with high losses, what Zhiyuan currently needs are two capabilities: one is financing capability, to find continuous funding channels; the other is mass production capability, as only mass production can bring revenue. Therefore, being the first to go public and seize market concepts becomes particularly important.

Interestingly, Zhiyuan seems to have been avoiding the issue of “backdoor listing”, but a series of operations make one think otherwise. For example, recently, Zhiyuan co-founder Peng Zhihui led the independent business development at “Zhiyuan Shangwei”, and Zhiyuan repeatedly stated that there is no business relevance, and both parties are operating independently. Meanwhile, the securities department of Shangwei New Materials stated in an interview that it was not aware of any developments in the robotics business.

After this tug-of-war, most netizens must be confused, and on November 11, Shangwei New Materials announced that the recently launched embodied intelligence robot business is in the development stage, and the company and related parties are independently conducting embodied intelligence robot business.

It seems to clarify, yet it does not clarify. The author believes that it cannot be simply assumed that Shangwei New Materials equals Zhiyuan’s main body; since it is to operate independently, it indicates more like an independent brand operation. Currently, Zhiyuan can be said to be in a position to advance or retreat, as the market environment is hot enough to achieve “A+H” listing, and if the environment is poor, it can operate Shangwei New Materials well.

Of course, choosing to go public in Hong Kong is also a good path, as the Hong Kong Stock Exchange’s 18C rules provide two channels for robotics companies to go public: one is a valuation of at least 4 billion HKD with a revenue of at least 250 million HKD, and the other is a valuation of at least 8 billion HKD with very little revenue. Under this logic, raising valuation and revenue figures becomes the main condition for robotics companies to go public in Hong Kong.

Thus, we can see various forms of “first” endorsements for embodied intelligence companies going public in Hong Kong, such as Woan Robotics initiating an IPO to become the “first AI embodied home robot stock”, building an ecosystem centered on intelligent home robot products. Extreme Intelligence successfully landed in Hong Kong, raising 2.7 billion HKD, becoming the “first global AMR warehouse robot stock”. Hotel service robot Yunji Technology also successfully went public, becoming the “first robot service intelligence agent stock”.

Some may question the practical significance of competing for the title of “first stock”; ultimately, it still depends on the product market.

However, the author believes that under the current premise of generally lacking large-scale mass production capabilities, early layout and capital locking to build one’s own industrial ecosystem is winning the first opportunity. If one does not seize the position now and waits until the industry truly begins mass production, startups will not even get a drop, as has been fully verified in the new energy vehicle industry.

References:

Yushu, Zhiyuan, and Leju jointly push for IPO Source: 21st Century Business Herald

Embodied Intelligence, Stumbling Start Source: Finance Magazine

If you are a robotics or AI practitioner or interested in it,

we can add you to a high-quality group chat; please provide your personal information to join.

Click「Recommend❤」

– END –

Submission and Content Cooperation|[email protected]Advertising and Business Cooperation|[email protected]

Submission and Content Cooperation|[email protected]Advertising and Business Cooperation|[email protected]