The CMOS image sensor market for mobile devices remains the largest application market in the industry, accounting for over 60% of total industry revenue. According to Yole statistics, this market is expected to recover in 2024, driven by a rebound in smartphone shipments (IDC data shows a year-on-year increase of +6%) and a continuous upgrade towards high-performance solutions. However, Counterpoint data indicates that the average number of cameras per device has decreased from 3.8 in 2023 to 3.7 in 2024.

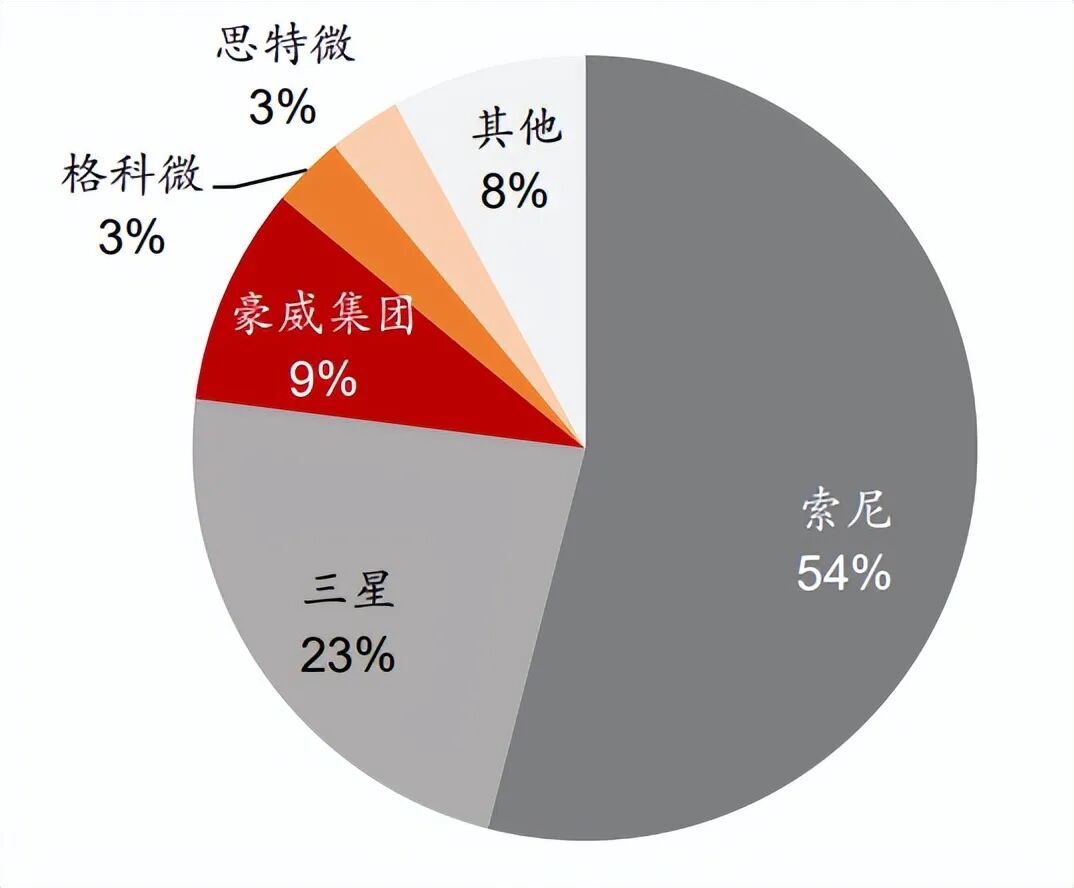

CMOS Image Sensor Market Share for Mobile Devices (2024)

Source: Counterpoint, Canalys Techinsights, Bloomberg, Public Data, CMB International Global Market Forecast

It is expected that the CMOS image sensor market for mobile devices will achieve single-digit percentage growth in the coming years, primarily driven by an increase in average selling prices. The overall cost of mobile CMOS image sensors is expected to remain between 2.5% and 3.0% of the total material cost of smartphones.

We maintain our expectation for the number of CMOS image sensors per device to remain stable, with overall image sensor shipment growth aligning with global smartphone sales trends. After experiencing two consecutive years of decline in 2022/23 (-11%, -3%), shipments are expected to grow by 6% year-on-year in 2024. In the first three quarters of 2025, the market is expected to stabilize further, with a year-on-year growth of 1.5%. IDC predicts that shipments will maintain a stable growth of about 1% in 2025 and 2026.

Despite moderate growth in smartphone shipments, IDC expects the average selling price of smartphones to increase by 5% this year, mainly due to a clear consumer preference shift towards high-end devices and OEM manufacturers shifting their strategies from market share competition to value growth. The penetration rate of generative AI smartphones is expected to reach 30% by 2025 and exceed 70% by 2029. Although shipment growth is limited, we expect demand for high-end models and technological iterations to drive a continuous increase in the average selling price of CMOS image sensors.

The mobile image sensor market is showing signs of consolidation: Sony maintains its leading position, followed closely by Samsung, while Chinese manufacturers are accelerating their catch-up and gradually entering the high-end market.

Sony (ranked first) continues to lead with over 50% market share, although Counterpoint expects its shipment growth for smartphone image sensors in 2024 to be slightly lower than its peers. In the medium to long term, Sony has positioned mobile image sensors as a core growth engine. While maintaining a large pixel size technology route, the company acknowledges that simply increasing pixel size will not meet future market demands for video performance, and is shifting towards a “high-density” development path, horizontally advancing process node technology upgrades and vertically evolving from a two-layer stacked architecture to a three-layer stacked architecture. This approach enhances sensor performance by increasing component integration density, achieving significant breakthroughs in sensitivity, noise reduction, and dynamic range, ultimately expanding the application scenarios of the sensors. We believe that Sony, with its technological leadership and continuous R&D investment, is likely to maintain its competitiveness in the mobile image sensor market.

Samsung (ranked second) has returned to Apple’s supply chain after ten years (according to Dealsite), marking a significant strategic breakthrough. The company’s initial order (possibly for 50 million pixel image sensors) has increased to 4,000 wafers per month. However, mass production has been delayed from March 2026 to late 2026 or early 2027, reflecting the company’s cautious approach to meet Apple’s stringent specifications.

Chinese supplier OmniVision (ranked third) and Gekewei (ranked fourth) are expected to see year-on-year shipment growth of 14% and 34% respectively in 2024 (Counterpoint). The simultaneous increase in volume and price has driven revenue growth for these two companies’ mobile image sensor businesses by 24% and 58% respectively. SmartSens (ranked fifth) has also gained market share, with the company’s mobile image sensor revenue growing significantly by 264% year-on-year.

Looking ahead, we expect the growth momentum to continue. In the first half of 2025, Gekewei and SmartSens are expected to see mobile image sensor sales grow year-on-year by 41.5% and 40.5% respectively, likely continuing their strong performance. Gekewei’s 50 million pixel product has achieved mass production in 2024 and has entered the mid-to-high-end mobile market. SmartSens recently launched a 0.61-micron 200 million pixel smartphone image sensor SCC80XS, filling the technological gap from 50 million pixels (the first product to be released in January 2025) to 200 million pixel products. This sensor is designed for flagship models and is expected to achieve mass production in 2026. OmniVision’s mobile image sensor revenue has decreased by 19.5% year-on-year, mainly due to product cycle transitions (e.g., from OV50H to OV50X). We expect the company’s mobile image sensor sales to temporarily decline in 2025, but to regain growth in 2026 as new products are released.

For more industry research and analysis, please refer to the official website of Sihan Industry Research Institute, which also providesindustry research reports, feasibility reports (project approval, bank loans, investment decisions, group meetings), industry planning, park planning, business plans (equity financing, investment promotion, internal decision-making), special research, architectural design, overseas investment reports and other related consulting service solutions.

About Us

About Us  Sihan Industry Research InstituteChinasihan.comLeader in Chinese Industry ResearchBuilding a Future City of InnovationContact for Customized Report Orders: · Phone:4008087939 0755-28709360 · Customer Service WeChat:g15361035605 · Customer Service QQ:454058156 · Email:chinasihan@126.com

Sihan Industry Research InstituteChinasihan.comLeader in Chinese Industry ResearchBuilding a Future City of InnovationContact for Customized Report Orders: · Phone:4008087939 0755-28709360 · Customer Service WeChat:g15361035605 · Customer Service QQ:454058156 · Email:chinasihan@126.com

· Official Website: Chinasihan.com