While tracking mergers and acquisitions and investment information in the sensor industry, we found that there has been a surge in capital operations in the magnetic sensor chip field recently. Based on publicly available information, we have organized the development history of this industry over the past 30 years, which has been serialized into four parts on our public account. To facilitate coherent reading, this article integrates these four parts and includes some modifications and supplements. The full text is approximately 18,000 words.

——-——-——-————————–

Over the past 30 years, numerous technologies have emerged and made breakthroughs, companies have grown from small to large and become stronger, and entrepreneurs have matured and made leaps.

In these 30 years, there have been cooperative win-win partnerships, as well as legal disputes and rivalries; there have been bustling celebrations of high-rise buildings and banquets that evoke envy, as well as the embarrassment of collapsed buildings that elicit sighs.

On August 26, 2025, Anhui Xici Technology officially submitted its listing application to the Hong Kong Stock Exchange. Based on the revenue of 2024, the company ranks sixth among global magnetic sensor IDM companies, and in the TMR sensor field, it ranks second globally. On the same day, Biyimi announced the acquisition of 100% of Xingan Semiconductor; in the same month, Xirui Technology gained control of the listed company Anche Detection through a reverse acquisition; in March of the same year, Shengbang Electronics acquired 67% of Ganrui Intelligent; last October, Naxinwei fully acquired Maigeen at a valuation of 1 billion yuan. A series of intensive capital actions clearly outline the accelerated integration of China’s magnetic sensor industry—this industry is gradually bidding farewell to the previous scattered development reminiscent of “small workshops” and entering a new stage of deep restructuring based on capital and strategy.

This article reviews the profound changes experienced by China’s magnetic sensor chip industry over the past thirty years, from the 1990s to the present.

In this journey from nothing to something, from small to large, the industry has achieved a critical leap from complete reliance on imports to partial domestic substitution: the domestic magnetic sensor chip market size has grown from less than 10% of the global market to over 30%, and the localization rate of chips has increased from zero to over 25%. The development over the past thirty years is not only a history of scientists and entrepreneurs bravely pioneering but also an important chapter in the epic rise of China’s high-tech industry.

01 Magnetic Sensor Chip Technology Routes and Development

A magnetic sensor is a device that converts changes in the magnetic properties of sensitive elements caused by external factors such as magnetic fields, electric currents, stress, temperature, and light into electrical signals, widely used in modern industry and electronic products to measure physical parameters such as current, position, and direction by sensing magnetic field strength.

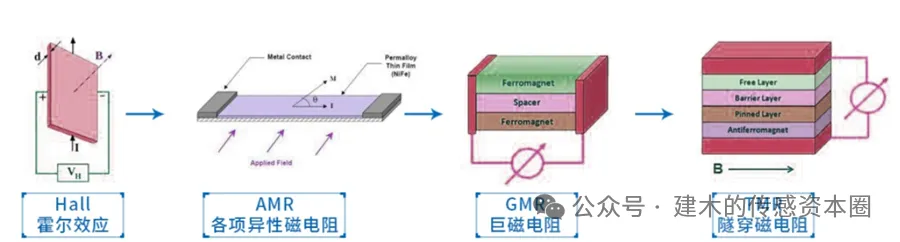

According to different technical principles, magnetic sensors are mainly divided into two categories: Hall effect sensors and magnetoresistive effect sensors, with the latter further including anisotropic magnetoresistance (AMR), giant magnetoresistance (GMR), and tunnel magnetoresistance (TMR) sensors. Although these sensors operate on different principles, they all play an important role in achieving magnetoelectric conversion, boasting excellent lifespan, reliability, and cost-effectiveness, thus standing out in numerous application fields.

1. The Development of Magnetic Sensor Technology: Four Technical Routes

In the 1970s and 1980s, magnetic sensor technology reached a peak of development in developed Western countries, entering a period of maturity and refinement in the 1990s. During this period, Hall effect sensors were the focus of research. In 1967, technicians at Honeywell first integrated silicon Hall plates and signal processing circuits into a single chip, creating a switch circuit and pioneering the era of integrated magnetic sensors. Japan’s Asahi Kasei (AKM) achieved an annual production capacity of 500 million InSb Hall elements by the end of the 1990s, relying on low-cost InSb thin film technology.

The magnetoresistive effect was discovered and verified as early as 1857, but its commercialization was relatively delayed due to the limitations of thin film technology. It wasn’t until 1991 that IBM broke through the mass production threshold of magnetic thin film technology, allowing anisotropic magnetoresistance (AMR) effect sensors to become the earliest commercialized magnetoresistive sensors, which are currently the most widely used magnetoresistive sensors.

In 1988, Professor Fert’s research team at the University of Paris discovered the giant magnetoresistance (GMR) effect in Fe/Cr metal multilayers, leading to a new focus on research related to electron spin. In 1994, NVE Corporation in the United States was the first to achieve the industrialization of the GMR effect and began selling GMR sensors. In 1997, IBM successfully applied the GMR effect in computer hard disk drives, developing GMR magnetic heads.

In 1975, physicist Michel Jullière from the University of Rennes observed spin-related tunneling effects in Co/Ge/Fe magnetic tunnel junctions, known as the TMR effect. In 2014, TDK launched the world’s first TMR sensor, also used in hard disk magnetic heads.

2. Commercialization of Magnetic Sensors and Early Market Leaders

Since the 1970s, with the commercialization of Hall, AMR, GMR, and TMR technologies in Western countries, foreign large enterprises have monopolized almost all core chip markets for magnetic sensors.

By the mid-1990s, dozens of large foreign companies had listed Hall sensors as important products. Companies such as AKM (InSb Hall elements), Honeywell, Allegro (formerly Sprague), TI, and Siemens (Infineon was once its semiconductor division) were able to mass-produce various types of Hall chips. Philips (which established NXP after splitting its semiconductor division), Honeywell, IBM, TDK, Sony, Matsushita, and Toshiba had also begun large-scale production in fields such as metal film magnetoresistive sensors and amorphous metal magnetic sensors, most of which had entered the Chinese market long before 2000.

Magnetic sensors have gained industrial applications in many fields, with the total number of magnetic sensors required each year reaching billions. According to statistics from the Japan Electronics Industry Promotion Association in 1992, the number of magnetic sensors used in Japan alone reached 1.108 billion, of which 64% were Hall devices, mainly used in brushless DC motors, and 32% were magnetic heads.

02 Industry Emergence: Research Institutions Leading Phase (1990-1999)

In the 1990s, domestic research and development of magnetic sensor chips was mainly led by research institutions, primarily to meet the needs of specific national projects (such as military and aerospace), with a low degree of commercialization and an incomplete industrial chain and market competition structure.

During the national “Eighth Five-Year Plan” from 1991 to 1995, five major categories of sensors—force, magnetic, thermal, humidity, and gas—were identified as key national research areas, leading to the formation of three sensor research centers: Shenyang Instrument Technology Institute, Shanghai Metallurgical Institute (now Micro Systems Institute), and Harbin Institute 49, which successively developed InSb magnetic sensitive films and Hall elements, as well as various magnetic sensors based on Hall elements.

During this period, the Space Physics Institute of the Chinese Academy of Sciences produced magnetic sensors and fluxgate magnetometers, while the Aerospace Ministry’s 15th Institute, Hebei Xuanhua 701 Factory, Beijing Semiconductor Device 10 Factory, Southwest Applied Magnetics Research Institute, Hefei Semiconductor Factory, Beijing 701 Institute, Yingkou Huaguang Sensor Components Factory, and Xiangfan Instrument Factory all developed one or more types of Hall elements (Ge, InSb, GaAs) with research capabilities. Among them, the Hefei Semiconductor Factory developed a relatively complete range of products, including Ge, Si, GaAs, and InSb Hall devices, mostly discrete devices. The domestic research capability for silicon-based Hall integrated circuits was generally weak, and most of these units’ products remained at the “sample/small batch” stage, with low commercialization and almost no competitiveness in the international market.

According to statistics at the time, by 1995, there were 41 domestic enterprises producing magnetic sensors (most of which were modules rather than chips), with a total of 150 specifications and models, and a total output of only 27.8 million units, which was only 5% of the annual production of InSb Hall devices by Japan’s AKM.

In 1994, Nanjing Zhongxu Microelectronics Co., Ltd. was established from the Nanjing Semiconductor Device General Factory, continuing to undertake the task of developing military Hall sensors for the defense industry while also developing the civilian market. The company transitioned the preparation process of InSb magnetic sensitive film chips from compound evaporation to elemental evaporation of In and Sb, achieving a yield rate of 60%. By the end of the 1990s, the Hall integrated circuits produced by Nanjing Zhongxu Microelectronics had dropped in price from 5 yuan per unit before large-scale production to the price of ordinary transistors, with an annual output of about 30 million units, making it the largest Hall device manufacturer in China.

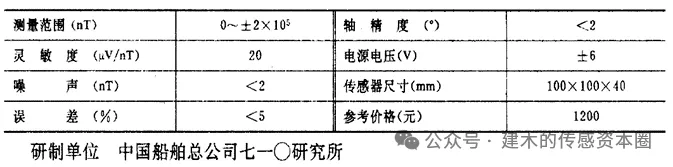

In 1998, the 710 Institute of China Shipbuilding Industry, based on the first weak magnetic experimental base established in Asia in 1970, established the Magnetic Measurement and Testing Station of China Shipbuilding Industry, which gradually expanded to various types of magnetic sensor components and products, including fluxgates and GMR.

By 1999, apart from Nanjing Zhongxu Microelectronics, which could mass-produce Hall integrated circuits, Yingkou Huaguang Sensor Components Factory, which could mass-produce thin-film magnetoresistive devices, and Southwest Applied Magnetics Research Institute, which could mass-produce Weigand devices, other types also had research and small-batch production capabilities.

The entire 1990s saw the domestic magnetic sensor industry fail to form a scale. With subsequent institutional reforms, these research institutes and state-owned factories either split or transformed into companies, and some units gradually exited the historical stage.

Those who planted trees for future generations to enjoy. Although the main bodies disappeared, with the onset of the new century’s reforms and the wave of globalization and commercialization, they branched out, accumulating technology and cultivating talent for the country’s magnetic sensor industry.

The wheels of history have entered a new century, and a “reform” drama concerning the fate of research institutes is about to unfold. Meanwhile, the spring breeze of the market economy has given birth to the first truly commercial companies.

03 Breaking the Ice Exploration Period: Reforming Institutions and Early Commercialization (2000-2009)

1. Reformed Institutions

To address the phenomenon of the separation of science and technology from the economy, China began exploring the transformation of research institutions from the late 1970s. Through practical exploration and the establishment and continuous improvement of related systems, a large-scale transformation of research institutions began in 1999, marked by the transformation of 242 research institutions.

In 1999, relying on the first batch of key technology innovation projects in Nanjing—the “Hall Current Sensor” project—Nanjing Zhongxu Electronic Technology Co., Ltd. was established with joint investment from state-owned enterprise Nanjing Electronic Holdings (Group) Co., Ltd., Nanjing Zhongxu Microelectronics Co., Ltd., and key technical personnel, focusing on military current sensors, with the brand name Chimin Zhongxu.

Two years later, in 2001, Nanjing Zhongxu Microelectronics Co., Ltd., Hong Kong Dongjie Industrial Company, and Shantou Dongfeng Printing Factory Co., Ltd. jointly invested to establish Nanjing Xinjie Zhongxu Microelectronics Co., Ltd., inheriting the silicon Hall integrated circuit and antimony-based thin film magnetic component business from the parent company Zhongxu Microelectronics.

In 2017, the state-owned shareholders of Xinjie Zhongxu exited, and the company was wholly owned by Nanjing Chengyuan Auction Co., Ltd. In June 2021, the Nanjing Semiconductor Device General Factory, which gave birth to Zhongxu Microelectronics in the 1990s, was deregistered. In the same year, after Nanjing State-owned Assets acquired part of Zhongxu Electronic Technology’s equity, it gained a total of 53% control, and the latter completed its share reform in May 2025. Zhongxu Electronic has become a designated research and production unit for military Hall components and Hall sensors by relevant state ministries.

In September 2023, Nanjing Zhongxu Microelectronics Co., Ltd., the largest Hall component manufacturer in China at the end of the last century, was deregistered, completing its historical mission. Meanwhile, former key personnel have branched out in Nanjing, establishing several Hall component and current sensor companies, such as Nanjing Aichi.

In 2004, Beijing 701 Factory implemented state-owned enterprise reform, and the sensor division team registered Beijing Sensha Electronics Co., Ltd. As early as 1989, 701 Factory began using advanced closed-loop Hall sensing technology to develop and produce Hall current and voltage sensors/transmitters, and has produced thousands of varieties, with products excelling in harsh environments such as military and aerospace.

In 2008, relying on its wholly-owned parent company, the 710 Institute of China Shipbuilding, as the core research institution for weak magnetic detection technology, Yichang Dongfang Micro Magnetic Technology Co., Ltd. was established. Dongfang Micro Magnetic is one of the earliest companies in China dedicated to the research and industrialization of SA series multilayer GMR and spin valve GMR magnetic sensor chips.

It established the first domestic 6-inch MEMS magnetic sensor chip production line, which was fully operational by the end of 2015, becoming the first production line in China capable of meeting industrial production standards, with a conservative capacity of 1,000 chips/month, and an annual production of at least 200 million chips. However, by the end of February 2017, the company’s debt-to-asset ratio reached 144.02%, leading to bankruptcy and deregistration in December 2020.

After the transformation of research institutes or state-owned factories into companies, most still did not break away from the habits of their previous paths, maintaining their original customer base and research pace without achieving full marketization. Although their technical strength and product quality were good, there was a disconnect between the company’s operations and the rapidly changing domestic market environment, and true commercialization relied on those who had experienced the market.

2. Early Commercialization

From 1978 to 1992, foreign-funded enterprises began to enter China in small numbers, primarily with exploratory investments, mainly concentrated in manufacturing, with small scales and limited fields. From 1992 to 2000, a large number of foreign-funded enterprises flooded into China. According to statistics, by the end of 2000, more than 400 of the world’s top 500 companies had settled in China, with investments covering machinery, electronics, chemicals, communications, pharmaceuticals, food, and other fields.

Entering the 21st century, with the initial emergence of market economic vitality, large foreign enterprises entering China on a large scale, and the growth of demand for consumer electronics, China’s magnetic sensor industry entered a phase of commercial exploration. This was also the most glorious period for foreign-funded enterprises in China, attracting the best graduates of the time. However, these well-known European and American companies perhaps did not expect that they became the training ground for Chinese entrepreneurs, and many of their strong competitors in the Chinese market were once their own.

During this period, developed regions began to support high-tech industries and entrepreneurial subsidies, and technology-oriented returnees gradually returned to start businesses; a small number of technical or sales backbones from foreign enterprises began to abandon stable, high-paying jobs to try entrepreneurship; some companies that accumulated customer resources and market awareness while representing foreign brands also began their own chip development paths.

In 1999, Dr. Zhao Yang, a Chinese American working in ADI’s MEMS department, persuaded ADI to provide technical authorization and funding support, establishing Meixin Semiconductor in the United States and Wuxi, China, successively, positioning it as the world’s first company to integrate MEMS with mixed-signal processing circuits in a single chip for inertial sensors. The thermal accelerometer became a hit, making it the first company in China to mass-produce MEMS sensors. After going public on NASDAQ in 2007, the company increased its investment in AMR magnetic sensor chip research and released its first product in 2010, establishing its own packaging and testing line.

In 2013, Meixin Semiconductor was privatized by IDG Capital, and in 2017, it was acquired by Huazhan Optoelectronics, and in 2020, it was spun off from Huazhan Optoelectronics to operate independently, still controlled by founder Zhao Yang and the management team, with investments from IDG Capital and others.

Currently, Meixin has mass-produced unique thermal accelerometers, capacitive accelerometers, AMR geomagnetic sensors, low-power Hall switches, and six-axis IMUs, widely used in automotive, industrial, medical, wearable, smart home, and consumer electronics fields, with cumulative shipments exceeding 4 billion units.

In December 2000, Ku Wan Jun, who developed a series of GMR sensors at the Institute of Computer Engineering and Applied Research in Lisbon, Portugal, gathered classmates who studied magnetic electronics with him and domestic experts to establish Huaxia Magnetic Electronics Technology Development Co., Ltd. in Shenzhen, becoming one of the earliest companies engaged in the research and production of magnetic sensors in China. Ku Wan Jun graduated from the Physics Department of Lanzhou University, which has had a significant impact on the domestic magnetic sensor industry. The founding teams or technical backbones of Xici Technology and Duowei Technology all include graduates from the Physics Department of Lanzhou University.

The company initially focused on the development of GMR chips and sensors, and its product matrix has now expanded to include rotary transformers, magnetic encoders (robot motor encoders), eddy current sensors, linear displacement sensors, and angle sensors, widely used in key fields such as new energy vehicles, electric engineering vehicles, and low-speed electric vehicles.

In 2002, Shaoxing Guangda Chip Microelectronics Co., Ltd. (SDC) was established. The 33-year-old founder, Tian Jianbiao, had years of experience in the research and development and sales of electronic components. The company initially focused on high-end DC fan magnetic sensor chips, and the SDC277 Hall sensor circuit it developed once occupied 70% of the domestic market share. In 2022, it received A-round investment from Haibang Investment and Silicon Port Capital, and currently, the company has three product lines: sensor chips, power management chips, and motor control chips, with annual shipments exceeding one billion units, and cumulative shipments exceeding ten billion units, with annual revenue in the hundreds of millions, widely used in consumer electronics, motion control, power tools, smart homes, IT and communication devices, industrial equipment, and robotics.

In 2005, Luo Liqian, after years of working in integrated circuit sales, partnered with friends and established Canrui Semiconductor (Shanghai) Co., Ltd. with an investment of 500,000 USD from Hong Kong Siwei Semiconductor Group. The company used magnetic sensor chips as a business entry point and collaborated with Shanghai University on technology. In 2008, the first product achieved mass supply. Riding the wave of the 2009 rural appliance subsidy policy, Canrui’s magnetic sensor chips rapidly entered Chinese home appliance companies, and the company’s products quickly gained market share.

In 2022, Canrui Technology went public on the Sci-Tech Innovation Board, and now has four product lines: magnetic sensors, power management chips, motor drivers, and optical sensor chips, as well as full-process integrated circuit packaging and testing service capabilities, with related products widely used in smart homes, smartphones, computers, wearable devices, industrial control, and automotive electronics.

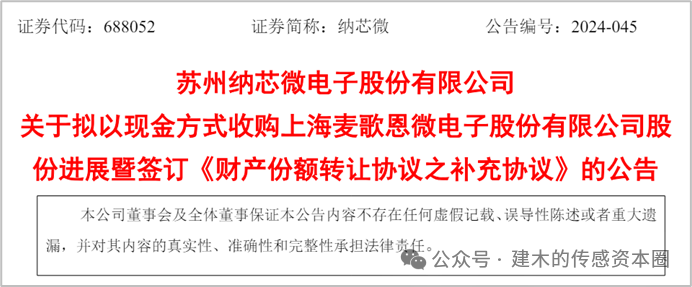

In 2009, Shanghai Maigeen Microelectronics Co., Ltd. was established. The founder, Fang Jun, a graduate of Shanghai Jiao Tong University, previously served as a sales manager at Honeywell China. The core team of the company comes from leading sensor and semiconductor companies such as Honeywell, MaxLinear, and Marvel. Maigeen has developed and sold a series of magnetic switch position detection chips, magnetic current/linear position detection chips, magnetic encoder chips, magnetic sensors, and related module products, capable of detecting multiple physical quantities such as position, speed, angle, current, and wheel speed, becoming a core “invisible champion” in the industry chain, with products widely used in industrial, automotive, and consumer fields. In 2023, it achieved sales revenue of 300 million yuan, with a net profit of 18.83 million yuan.

In the sixth year since its establishment, in 2015, Maigeen was invested by Shanghai Lianhe Investment and the Micro Systems Institute’s associated fund, thus becoming a company incubated by the Micro Systems Institute. In 2017, it was listed on the New Third Board. In 2018, the same Shanghai Lianhe and Micro Systems Institute’s associated fund invested in Maigeen, increasing its stake to 57.38%, achieving control and consolidation. In 2024, Maigeen was sold 100% to Naxinwei, becoming a wholly-owned subsidiary of Naxinwei and its affiliates, marking the end of Maigeen’s capital market journey.

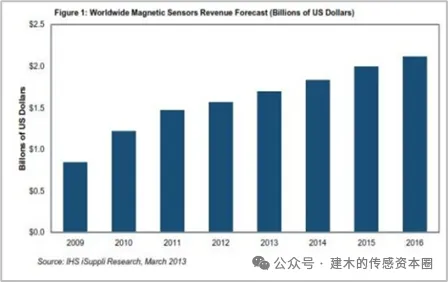

During this period, the domestic market size accounted for only about 10% of the global market, but its growth rate was high. According to IHS iSuppli’s report, in 2010, the global magnetic sensor market size was 1.18 billion USD, with China’s market capacity around 100-200 million USD per year. As more design companies shifted to China, the annual growth rate of the Chinese market could reach 20%-30%.

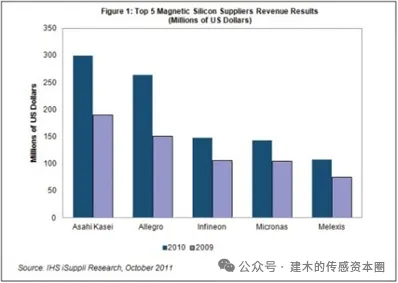

According to statistics, in 2010, the total revenue of the top five silicon magnetic sensor suppliers globally reached 962 million USD, accounting for 82% of the total. These five major suppliers are AKM, Allegro, Infineon, Micronas (acquired by TDK in 2015), and Melexis. Although some of the aforementioned startups in China have achieved some success, they still account for a negligible share in the global and Chinese markets.

04 The Golden Decade: Returnee Entrepreneurship and Industry Upgrade (2010-2019)

In the second decade of the 21st century, China’s economy grew rapidly, and the wave of innovation and entrepreneurship triggered a surge of entrepreneurial activity, releasing a large number of blank tracks. Local governments also offered funding, venues, and settlement packages for returnees, while various factors such as tightening immigration and employment in Europe and America, the explosion of PE/VC funds, and the gradual maturity of the supply chain contributed to the rise of high-tech industry returnees and technical backbones from foreign enterprises joining this wave of entrepreneurship, marking the golden decade of domestic entrepreneurship, and also the fastest and most vibrant decade of China’s economic development. In this wave, the explosion of smartphones, the rise of the Internet of Things, and new energy vehicles propelled the rapid development of China’s magnetic sensor industry.

In September 2009, Wang Jianguo, who holds a PhD in Physics Technology Engineering from the University of Lisbon in Portugal, along with his classmate Bai Jianmin from Lanzhou University and several other PhDs, founded Wuxi Le’er Technology Co., Ltd., focusing on high-sensitivity tunnel magnetoresistance (TMR) core technology, specializing in magnetic identification sensors, magnetic image scanning sensors, and other products used in financial equipment and biomedical testing. Wuxi Le’er was integrated into Xici Technology in 2014, becoming its wholly-owned subsidiary, and in 2021, it became a subsidiary of Bengbu Xici (now Anhui Xici Technology Co., Ltd.).

In 2013, Ningbo Xici Technology Co., Ltd. was established. The prospectus submitted by Xici Technology to the Hong Kong Stock Exchange shows that Dr. Wang Jianguo, after graduating with a PhD in Portugal, worked in the United States, where he met Dr. Mao Sineng, an expert in the field of magnetics. Mao Sineng is a top expert in international magnetics and magnetoelectronics, having served as the director of sensor research and development at Seagate, leading the development of multiple generations of GMR magnetic head products, and later served as vice president at Western Digital, responsible for the development of magnetic head devices, earning the title of “Father of TMR Magnetic Heads.” Ningbo Xici was established to initiate Mao Sineng’s entrepreneurial project related to high-end magnetic sensor research and development. Wang Jianguo gathered potential investors and established a new investment vehicle, inviting Bai Jianmin to provide support, forming a core team to explore business opportunities.

In 2021, Xici acquired the German wafer manufacturing center Sensitec, which was once IBM’s wafer manufacturing base in Germany that first commercialized AMR magnetoresistive technology for magnetic heads. In the same year, the headquarters of Ningbo Xici moved to Bengbu, and after a series of capital operations and restructuring, Ningbo Xici became the sole shareholder of Wuxi Le’er, which is also a wholly-owned subsidiary of Anhui Xici, becoming the main company for Wang Jianguo’s team to operate the magnetic sensor business. The company has sensor wafer design and manufacturing centers in Germany, a sensor wafer design and R&D center in Portugal, and three subsidiaries in China, making it one of the few IDM companies in the magnetic sensor chip industry.

As of now, Anhui Xici’s main products include AMR, GMR, and TMR wafers, magnetic angle encoders, magnetic displacement sensor chips & modules, magnetic detection systems, etc., with downstream application fields mainly including green energy (mainly photovoltaics), new energy vehicles, industrial automation, and robotics. In 2024, the revenue reached 703 million yuan. By 2025, Anhui Xici ranked sixth among global magnetic sensor IDM companies and first among Chinese companies. The company began accepting IPO guidance for A-shares in April 2024 but was affected by the broader environment and shifted to the Hong Kong Stock Exchange, submitting its listing application to the Hong Kong Stock Exchange on August 26, 2025, initiating a new round of capital operations.

In January 2010, Xu Mingfeng founded Shanghai Yan Hua Electronic Technology Co., Ltd. (the predecessor of Shanghai Xinyan Microelectronics Co., Ltd.), focusing on integrated circuit research and sales in the sensor field. Prior to this, Xu Mingfeng founded Jinxin Electronics, which engaged in agency sales of electronic components, including the British Otter brand. In 2015, Xu Mingfeng and Guan Hui became the real-name shareholders of Xinyan Micro. Guan Hui founded Hangzhou Xinxin Electronics Co., Ltd. in 2004, and after joining Xinyan Micro, the company was deregistered in 2017. The founder of Saizhuo Electronics mentioned later, Song Honggang, served as a supervisor at Hangzhou Xinxin.

The company completed its share reform in January 2022 and was listed on the Shanghai Equity Exchange in August of the same year, achieving revenue of 64.69 million yuan and a net profit of 6.32 million yuan. Currently, the company’s main products include general magnetic sensing, motor drive, gear transmission, and other series of Hall chips, covering hundreds of magnetic sensor chip products, gradually forming a development pattern focused on automotive electronics, while continuously deepening its development in new energy, industrial automation, and consumer electronics.

In 2010, Dr. Xue Songsheng led ten returnee PhDs to establish Jiangsu Duowei Technology Co., Ltd. in Zhangjiagang. Dr. Xue had served as the R&D director of the technology record magnetic head department at Seagate and the Asian technology director at Honeywell. At the beginning of the venture, he received funding support from his classmate at the Institute of Optics and Mechanics of the Chinese Academy of Sciences, Shi Zhengrong, the founder of Shanda. Since its establishment, the company has been committed to providing TMR-based magnetic sensors and application solutions, building a thin-film sensor industry platform centered on “magnetics,” and establishing China’s first TMR magnetic sensor mass production line, achieving 100% domestic process localization.

As of 2024, Duowei has over 400 patents and has shipped over 100 million chips, with products applicable in smart cities, industrial control, consumer electronics, smart homes, the Internet of Things, new energy, automotive electronics, and medical fields. The company has attracted significant capital attention since its inception, with a total of over ten rounds of financing and more than 50 shareholders, with the latest round of financing completed at the end of 2022.

In 2011, Song Honggang and Yang Ying founded Saizhuo Electronics Technology (Shanghai) Co., Ltd. Song Honggang, a graduate of Tongji University, had previously worked as a design engineer and project manager at Silan Micro and Skyworks, while Yang Ying had served as a layout engineer at Skyworks and China Resources Shanghua. Saizhuo Electronics is one of the earliest IC design companies in China focused on automotive electronics, initially developing automotive-grade ABS wheel speed sensor chips. In 2014, its sales exceeded 10 million yuan, and five years after its establishment, its shipment volume exceeded ten million units. The company has its own automotive-grade chip packaging and testing factory, and its products now cover magnetic sensor chips, power management chips, motor driver chips, and other high-performance mixed-signal chips, widely used in automotive electronics, consumer electronics, and industrial control.

In 2024, the number of products has exceeded 350, with total shipments exceeding 543 million units, and operating revenue of 320 million yuan.

The prospectus shows that Saizhuo holds about 3% of the market share for automotive magnetic sensor chips, and its position sensor chips have over 30% market share in domestic light electric vehicle motor control systems, leading among local similar products. The company plans to apply for an IPO on the Sci-Tech Innovation Board in 2022, but withdrew its materials in July 2023, temporarily halting its IPO journey.

In December 2022, Saizhuo Electronics aimed for an IPO on the Sci-Tech Innovation Board, planning to raise 1.1 billion yuan for automotive-grade chip research and industrialization projects, but withdrew its listing application in July 2023. The withdrawal was influenced by tightening regulations on IPOs at the time, as well as potential challenges the company faced, including declining gross margins, increasing accounts receivable, and supplier concentration risks, all of which drew inquiries from the exchange and market attention.

Saizhuo Electronics’ major investment of 500 million yuan in automotive-grade packaging and testing projects was put into production in Jiashan in April 2025. The company’s main products are still concentrated in magnetic sensor chips, remaining the leader in domestic automotive-grade magnetic sensor chips, aiming to provide complete automotive-grade analog chip product solutions, including sensor chips, power management chips, motor driver chips, and other high-performance mixed-signal chips.

On August 26, 2025, the magnetic sensor industry IDM company Xici Technology transitioned to the Hong Kong Stock Exchange, officially submitting its main board listing application, with fundraising plans for the construction of a new R&D and production base in Wuxi, upgrading the German wafer production line, and potential strategic acquisitions to strengthen its vertical integration capabilities and expand into emerging application scenarios.

Currently, Xici Technology has become the number one magnetic sensor company in China by revenue. Its products are primarily current sensors (accounting for over 80% of revenue), widely used in green energy (mainly photovoltaics), new energy vehicles, and industrial automation fields. Although revenue temporarily declined in 2023 due to fluctuations in the photovoltaic industry, it rebounded to 703 million yuan in 2024, achieving profitability; in the first four months of 2025, revenue grew by 34% year-on-year, with net profit exceeding 10 million yuan and gross margin rising to 19.5%. The company will continue to increase R&D investment, leveraging the advantages of xMR sensor technology to enter high-end markets and actively layout in emerging fields such as robotics and third-generation semiconductors.

Now, let’s take a look at the global market and competitive landscape during this period.

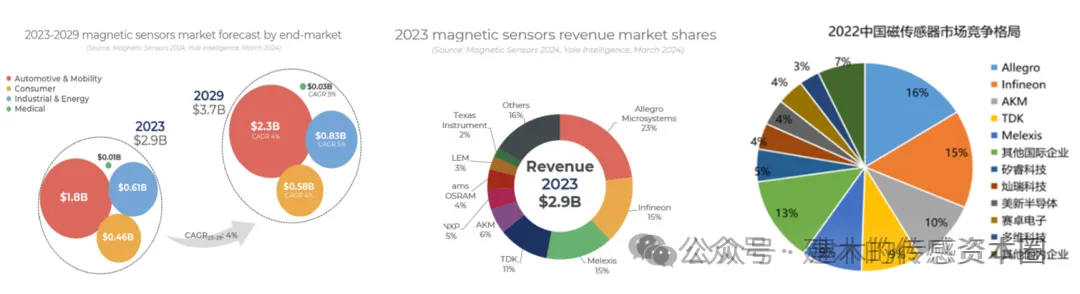

According to Yole data, the global magnetic sensor chip market was approximately 20.3 billion yuan in 2023, expected to grow to 22.4 billion yuan by 2025, with a CAGR of 4%. Among them, the Chinese magnetic sensor chip market was about 8.25 billion yuan in 2023, expected to grow to 11.23 billion yuan by 2025, with a CAGR of 16.67%, accounting for 40%-50% of the global market.

In terms of competitive landscape, Allegro leads with a 23% market share, benefiting from its strong influence in automotive and industrial applications, along with a broad technology portfolio (including not only Hall but also GMR and TMR). Infineon and Melexis follow closely, holding about 15% market share, with their product portfolios mainly targeting automotive and mobile applications. The top five global suppliers account for about 70% of the market, indicating a high level of market concentration.

To estimate, in 2022, the localization rate of China’s magnetic sensor chips was about 25% (according to statistics from Yicun Capital), and the domestic magnetic sensor chip market accounted for about 40% of the global market, so the combined share of domestic companies in the global market is about 25% x 40% = 10%.

Over the past 30 years, the market share of Chinese manufacturers has increased from 0 to 10%, making significant progress and capturing a lot of market share from multinational giants in China, but it still mainly occupies the domestic mid-to-low-end market and non-critical application scenarios.

Combining the global competitive landscape, a 10% share is comparable to the 11% share of the fourth-ranked TDK, but in reality, there is no Chinese company among the top ten globally (>=2% share), indicating that the concentration of domestic magnetic sensor chip companies is too low, with a small and scattered pattern. Even the largest companies have not exceeded 100 million USD in annual revenue, and domestic companies still have significant gaps in design capabilities and process levels, especially in independent process capabilities.

2. Mergers and Acquisitions! An Industry Necessity (2023-2025)

Starting in August 2023, regulatory authorities clarified the “phase-wise tightening of IPO rhythms,” prioritizing the stability of the secondary market over financing functions, while simultaneously raising the evaluation standards for the “scientific and technological attributes” of the Sci-Tech Innovation Board, leading to a large number of companies withdrawing their IPO applications. After the full opening of the pandemic, the market did not recover as quickly as expected; instead, it faced a new situation of declining consumer electronics and loosening wafer production capacity, with the domestic market shifting from incremental dividends to stock competition, intensifying competition within various industries, which has been transmitted to upstream semiconductor companies, resulting in widespread profit declines in 2023, with many companies triggering the “performance face-changing” red line for IPOs.

Entrepreneurs’ expectations for A-share IPOs have plummeted, and uncertainties surrounding listings have sharply increased. Compounding the situation, a large number of funds from the era of innovation and entrepreneurship are entering the liquidation phase, facing significant exit obstacles, leading to a situation where GPs are forced to “cash out” at any cost, becoming the main theme of the past two years.

As a result, founders, in order to lift the sword of repurchase hanging over them, have to seek alternative paths. On one hand, they are compelled to seek listings on the Hong Kong Stock Exchange to obtain funds and lift repurchase obligations; on the other hand, they are looking for listed companies or state-owned enterprises as financial backers for acquisitions, with companies lacking self-sustaining capabilities willing to bear significant valuation differences to avoid becoming burdensome liabilities.

At the same time, the state is promoting the establishment of a unified national market, focusing on rectifying the disorderly competition among enterprises. The capital market policies have also relaxed merger review processes, encouraging “strong chain and supplement chain” strategies, with banks, large funds, and local state-owned assets providing acquisition loans and bottom-line funding, leading to a wave of mergers and acquisitions in the past two years, dramatically changing the industry landscape.

In June 2024, Naxinwei announced its intention to acquire 79.31% of Maigeen for 793 million yuan in cash. Four months later, the adjusted plan was to acquire 100% of Maigeen’s shares for 1 billion yuan, with the industrial change completed in December of the same year. The original controlling shareholder, Xirui Technology, divested Maigeen, receiving over 600 million yuan in cash, providing ample funds for its subsequent acquisition of the listed company Anche Detection.

Through the acquisition of Maigeen, Naxinwei added magnetic switches, magnetic angle sensors, and magnetic encoders to its existing product lines of current sensors and wheel speed sensors. Among the more than 3,300 products provided by Naxinwei, Maigeen contributed over 1,000 varieties, allowing Naxinwei to achieve comprehensive coverage of all categories of magnetic sensors. In the first half of 2025, Naxinwei’s revenue grew by 79.49% year-on-year, with Maigeen significantly contributing to its sensor business. Technically, the company achieved complete coverage of Hall, AMR, and TMR technology categories; from a customer perspective, this acquisition strengthened its resources among key customers, expanded its customer base, optimized sales channels, and reduced sales costs; from a supply chain perspective, this acquisition leveraged scale effects to further enhance raw material procurement cost advantages.

In March 2025, Shengbang Co., Ltd. acquired 67% of Ganrui Intelligent for a total valuation of 240 million yuan, thus achieving control and consolidation of Ganrui Intelligent. Shengbang is a leading domestic analog chip enterprise, covering signal chain and power management categories, widely covering downstream markets such as consumer electronics, industrial, automotive, and communications. Ganrui Intelligent fills the technical gap in the sensor field for Shengbang, especially in automotive-grade chips. Shengbang will accelerate its layout in the fields of new energy vehicles and smart automotive electronics, and this acquisition will help achieve the company’s goals of exploring high-end technologies and products in industrial and automotive chips, third-generation semiconductors, high-power power supplies, new energy, and energy storage.

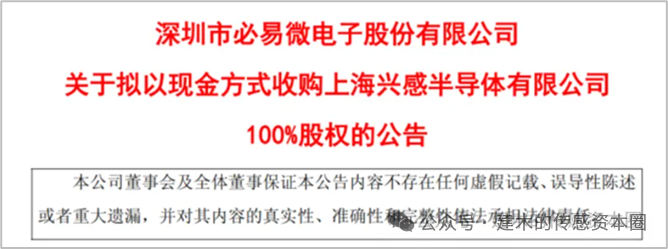

On August 5, 2025, Biyimi Electronics plans to acquire 100% of Shanghai Xingan Semiconductor Co., Ltd. for 295 million yuan in cash. Biyimi was listed on the Sci-Tech Innovation Board in 2022, focusing on the research, design, and sales of analog and mixed-signal chips, with its product line expanded to include AC-DC, DC-DC, driver ICs, protection ICs, linear regulators, battery management, and has also expanded into amplifiers, analog-to-digital converters, sensors, isolation and interface signal chain chips, and microcontrollers. This acquisition is a strategic decision by Biyimi to deepen its core business layout, broaden its technological boundaries, and enhance its system-level solution capabilities, facilitating the integration of resources in products, technology, market, and supply chain.

The aforementioned acquisition cases illustrate that the most common path for investors in magnetic sensor chip companies to exit is to seek acquisition by analog chip listed companies, which can achieve collaborative sharing in supply chains such as wafers and packaging/testing, while rapidly expanding the product categories of listed companies and enhancing their technical strength and revenue scale. For leading listed companies, industrial capital integration and strategic reinforcement have become important paths to consolidate their positions, achieve expansion, and manage market value.

However, as sensor chips are a special category within integrated circuits, their requirements in terms of material and process selection, circuit design, application development, and algorithm development differ significantly from traditional analog or digital chips. Therefore, the successful development of sensor chips is essentially a test of the comprehensive capabilities of design companies.

Because of this, although analog chip manufacturers have strong synergies in acquiring magnetic sensor chip companies, they still need to deeply understand the essential differences between magnetic sensor chips and analog chips, as well as the specific application scenarios of magnetic sensors, to more effectively achieve the expected goals of merger integration.

06 Review and Outlook: Integration, Innovation, and Trends (2025 and Beyond)

Looking back at the development path of China’s magnetic sensor industry over the past thirty years, a clear thread emerges:

This is an epic leap fromtechnology introduction todomestic substitution and then tocapital integration.

In the early 1990s, research institutions sowed the seeds of the industry, while the reformed institutions and the first batch of entrepreneurs in the 2000s opened the ice-breaking journey of commercialization. The “golden decade” of the 2010s benefited from returnees and foreign enterprises’ personnel entrepreneurship, market dividends, and capital support, giving rise to a number of “invisible champions” that emerged in niche fields. By the 2020s, under the combined catalysis of the registration system dividend, domestic substitution strategy, and chip shortage wave, the industry welcomed its shining moment, with leading enterprises successfully going public and obtaining capital tickets to compete with international giants.

However, after the feast, the cycle arrives. When IPOs tighten, capital retreats, and the market shifts from incremental to stock, the dispersed competitive landscape has become the biggest constraint on the industry. Thus, industry mergers and acquisitions are no longer an option but a necessity for survival and development.

The series of mergers and acquisitions between 2023 and 2025 mark the formal transition of the magnetic sensor chip industry from the “blooming flowers” of its youth to the “stronger stronger” integration period.

For the future, we can clearly see several trends:

Deepening integration, emergence of giants. The current wave of acquisitions has just begun, and true integration has yet to come. In the coming years, we will see more listed companies acquiring small and medium-sized enterprises in niche fields, as well as mergers between listed companies and mergers between non-listed enterprises. In an intensely competitive environment, small and medium-sized enterprises must either seek support from larger companies or band together to survive.

As with the development laws of all things, the initial wave of mergers and acquisitions inevitably involves disorder and chaos. The current mergers and acquisitions have not substantially alleviated the industry’s internal competition; they have merely transformed the homogeneous competition among small enterprises into competition among more influential leading enterprises. Without effective regulation and industry self-discipline, the vicious competition among giants will bring even more severe harm.

Foreign magnetic sensor chip companies’ development history tells us that China does not need so many homogeneous players; this industry will gradually form a hierarchical structure led by a few platform giants, supplemented by several “specialized and innovative” enterprises.

Convergence and integration of technology routes. Hall, AMR, GMR, and TMR technologies will not replace each other but will find optimal solutions in different application scenarios. The future competition focus will be on how to integrate multiple technologies to provide“chip + algorithm + application” integrated solutions. Chip companies that rely solely on a single technology route and a limited product line may find survival increasingly difficult.

Application scenarios drive innovation. The next round of industry growth will no longer be driven by general-purpose chips but will be defined by the demands of cutting-edge scenarios such as robotics, artificial intelligence, high-end industrial automation, and new energy. Whether companies can position themselves in these high-growth tracks will determine their status in the next industry cycle.

The barriers for new entrants are rising. As industry barriers solidify, new entrants will find it difficult to find opportunities in traditional red ocean markets. Future new players are more likely to emerge from disruptive technologies or extremely niche new application scenarios, starting a new industry cycle from corners that giants do not pay attention to.

As observers and participants, we stand at the crossroads of an era:

For entrepreneurs, it is essential to abandon the obsession with independent listings and view “being acquired” as a successful exit path; alternatively, they should consider how to leverage technological innovation and funding to develop independently, not seeking dominance but rather becoming a complementary support to giants, which may open a new industry cycle and become the giants of tomorrow.

For buyers, in addition to market value management, they should also consider what the original intention of the acquisition is, whether true integration and empowerment have been achieved after the acquisition, and whether the potential and synergy of the target have been released. Whether the integrated enterprise promotes healthy industry development or accelerates internal competition. We believe that buyers who genuinely reflect on these issues will not fare poorly in the future.

The story of China’s magnetic sensors, like the story of the entire Chinese technology industry, is one of imitation and substitution in the first half, fierce competition and rise in the middle, and integration and leadership in the latter half.

This grand journey of magnetic cores is far from over; it has merely entered another exciting new chapter.

All content in this article is compiled from publicly available information, aiming to record the changes in the magnetic sensor chip industry, paying tribute to the industry’s pioneers, and hoping to inspire thoughts on how to promote healthy industry development.

If there are any omissions or errors, please feel free to communicate and correct.