This article studies the time window: September 1, 2024 — November 25, 2025

In the seemingly homogeneous PCB industry, the past 14 months have played out a tale of “ice and fire.” From September 1, 2024, to November 25, 2025, Dongshan Precision (002384.SZ) saw its stock price rise by 171.16%, while Huadian Shares (002463.SZ), also a leading PCB company, only increased by 90.24%. The difference of 81 percentage points is not merely a performance divergence, but a market vote on “identity recognition” and “growth paradigms.”

On the surface, Dongshan’s strength comes from its acquisition of optical module manufacturer Solstice and its planned H-share listing; Huadian, on the other hand, is steadily capitalizing on the AI server PCB boom. However, a deeper analysis reveals that the essence of this excess return is a complete transformation from “cyclical manufacturing” to “technological growth,” while Huadian remains anchored in a “high certainty but low elasticity” single track.

1. Business Structure: Diversified Synergy vs. Single Point Dependence

In the past year, Dongshan Precision has completed a crucial transformation: from a traditional manufacturer primarily focused on consumer electronics FPC to a technology platform covering three major sectors: new energy, optical communication, and consumer electronics.

·The new energy business has become the most stable growth driver. In the first three quarters of 2025, revenue reached 7.52 billion yuan, a year-on-year increase of 22.1%, with its share of total revenue rising from 23% in 2024 to 27.8%. Through the acquisition of the French GMD Group, the company has further penetrated the high-end automotive supply chain in Europe, with a per vehicle value reaching 15,300 yuan.

·The optical module business represents the largest potential. By September 2025, it completed the acquisition of a controlling stake in Solstice Optoelectronics, which has self-developed capabilities for 50G/100G EML high-speed optical chips and is already a core supplier for Oracle, expected to account for 500,000 units in Meta’s 800G optical module shipments (up 150% year-on-year). Although it has not yet been consolidated in the first three quarters, it will officially be included in the financial report starting in October, becoming a core increment for Q4 2025 and beyond.

·Consumer electronics FPC has seen a slowdown in growth (1.93% year-on-year in the first half of 2025), but as the world’s second-largest flexible circuit board manufacturer, its fundamentals remain solid, contributing 65% of revenue in 2024.

In contrast, Huadian Shares has almost entirely bet its growth on AI server PCBs. In the first three quarters of 2025, this business generated approximately 9.99 billion yuan in revenue, accounting for 73.9% of total revenue of 13.51 billion yuan. Although the growth rate was as high as 97% in the first half, it fell to 39.9% by the third quarter, clearly showing a slowdown trend under high base conditions. More critically, its product structure is highly concentrated—over half of the enterprise communication boards are high-speed switches, while AI servers account for less than a quarter.

In summary: Dongshan is “building multiple legs to walk,” while Huadian is “training one leg to perfection.” The former gains a growth premium, while the latter receives a certainty discount.

The business structures and development paths of the two companies can be summarized as follows:

|

Comparison Dimension |

Dongshan Precision |

Huadian Shares |

|

Business Structure |

New energy + optical modules + consumer electronics |

Highly dependent on AI server PCB |

|

Revenue Concentration |

Largest business segment < 35% |

AI server PCB > 70% |

|

Growth Driver |

Diverse business synergy growth |

Single business linear growth |

|

Risk Resistance |

Strong (business diversification) |

Weaker (single business dependence) |

|

Technical Barriers |

Covers multiple fields of PCB/FPC/optical modules |

Focus on high-end PCB manufacturing |

|

Customer Structure |

Multiple industry customers in consumer electronics + new energy + communication |

Concentrated among communication equipment manufacturers |

2. Financial Performance: Deep V Rebound vs. Steady Climb

The profit trajectories of the two companies show starkly different shapes.

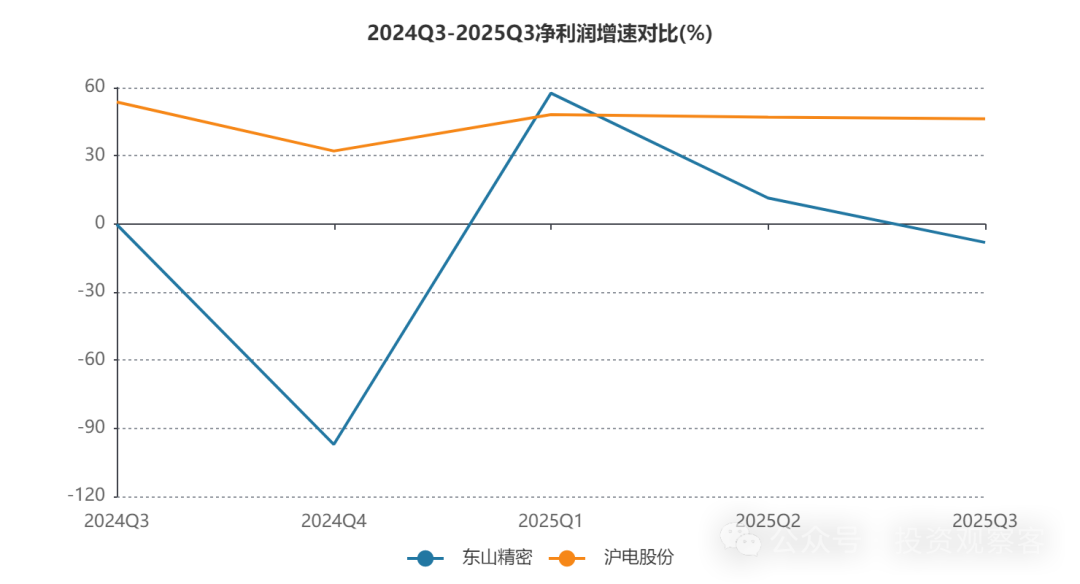

Dongshan Precision’s net profit has followed a typical “deep V” curve: in Q4 2024, it plummeted to 18 million yuan due to asset impairment and other factors, with market sentiment hitting rock bottom; however, it quickly rebounded to 456 million yuan in Q1 2025 (up 57.6% year-on-year), with a cumulative total of 1.223 billion yuan in the first three quarters, a year-on-year increase of 14.6%. Although the gross margin remains low at around 14% (far below Huadian’s 35%+), excluding the drag from LED and other businesses, the core segment’s profitability is recovering.

Huadian, on the other hand, has maintained a “slope-like” growth: in the first three quarters of 2025, net profit reached 2.717 billion yuan, a year-on-year increase of 47%, with quarterly growth rates stable between 30%-50%. High gross margins, high net profit margins, and strong cash flow reflect its pricing power and technical barriers in the high-end PCB field.

However, the capital market prefers “turning point stories.” The expectation gap created by Dongshan’s rebound from the trough is far more attractive for trading than Huadian’s linear growth. This explains why Dongshan’s net profit growth rate (2025E +163.6%) far exceeds Huadian’s (+47.3%), even though its absolute profit scale is still only half of the latter’s.

Core findings from the financial comparison:

|

Financial Indicator |

Dongshan Precision (Q3 2025) |

Huadian Shares (Q3 2025) |

Difference Analysis |

|

Revenue Growth Rate (YoY) |

+2.82% |

+39.92% |

Huadian’s growth rate significantly leads |

|

Net Profit Growth Rate (YoY) |

+130.2% |

+58.7% |

Dongshan’s higher growth rate is due to a rebound from a low base |

|

Gross Margin |

14.11% |

35.84% |

Huadian’s technical barriers lead to high gross margins |

|

Net Profit Margin |

4.60% |

20.62% |

Huadian’s profitability is strong |

|

Debt-to-Asset Ratio |

55.8% |

52.4% |

Both are at reasonable industry levels |

|

Cash Flow/Net Profit |

2.41x |

1.07x |

Dongshan’s profit quality has improved significantly |

The core finding of the financial comparison is that although Huadian Shares leads in static indicators such as revenue scale, profitability, and operational efficiency, Dongshan Precision has gained higher market attention and valuation uplift due to its stronger performance recovery elasticity and business transformation expectations. This “dynamic change surpassing static levels” market logic is key to understanding the price differences between the two companies.

3. Valuation Logic: Identity Switch from Cyclical Stocks to Growth Stocks

1. Market Positioning Differences

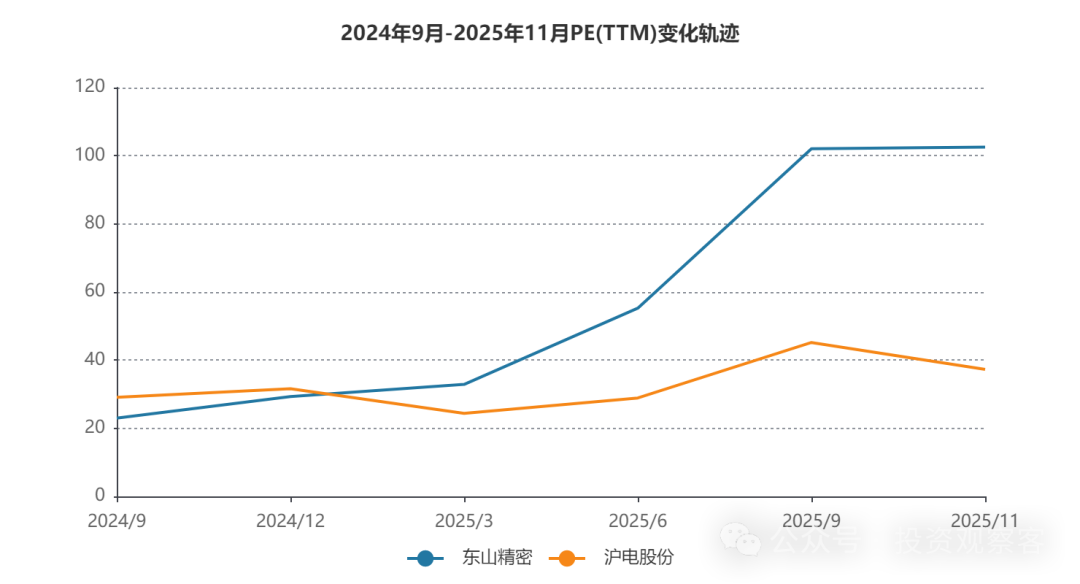

In early September 2024, Dongshan Precision’s PE (TTM) was only 22.97 times, and PB was 2.15 times, with the market viewing it as a typical consumer electronics cyclical stock, assigning it a traditional manufacturing valuation (PE 20-30 times). However, with the ramp-up of new energy and the realization of optical modules, investors began to reprice it using the valuation system of “AI + new energy” growth stocks, switching to a high-growth track (PE over 100 times). This cognitive shift from cyclical to growth has led to a non-linear increase in the valuation system. By November 25, 2025, its PE had soared to 102.5 times, and PB reached 5.53 times—a 346% expansion in valuation over 14 months.

In contrast, Huadian Shares’ valuation has consistently been positioned by the market as a “high certainty but low elasticity” industry leader, with valuation increases primarily reflecting linear performance growth, lacking the “paradigm shift” expectations similar to Dongshan Precision. Especially after Q3 2025, the market began to worry that AI server demand might peak, leading to a decline in valuation from its high point.

2. Profit Expectations

Changes in market profit expectations for the two companies further explain the rationality of the valuation differences:

Dongshan Precision’s net profit expectations have been systematically revised upward during the observation period. In September 2024, the market expected its 2025 net profit to be around 1.5 billion yuan (based on an expected 1 billion yuan in 2024 + 50% growth); by November 2025, the consensus expectation was raised to 2.862 billion yuan (up 163.6% year-on-year), with 2026 expectations at 4.010 billion yuan (+40.1%) and 2027 expectations at 5.030 billion yuan (+25.4%). This change in expectations reflects the market’s high optimism about its new energy and optical module businesses, with PE rising from 23 times to 103 times, matching the expected growth rate of net profit (CAGR of about 42% over the next three years).

Huadian Shares’ profit expectations have remained relatively stable. The actual net profit in 2024 was 2.587 billion yuan, with 2025 expectations revised from 3-3.2 billion yuan to 3.812 billion yuan (+47.35%), 2026 expectations at 5.496 billion yuan (+44.15%), and 2027 expectations at 7.358 billion yuan (+33.88%). The market assigned a PE from 29 times to 37 times, which is basically in sync with the future three-year net profit CAGR of about 41%, without the “excessive expectation premium” seen in Dongshan Precision.

Valuation Indicator Comparison Summary:

|

Valuation Indicator |

Dongshan Precision |

Huadian Shares |

Difference Analysis |

|

Initial PE (TTM) |

22.97x |

29.09x |

Dongshan’s valuation starting point is lower |

|

Final PE (TTM) |

102.54x |

37.27x |

Dongshan’s valuation increase is larger |

|

Initial PB |

2.15x |

6.22x |

Huadian’s asset quality is more recognized |

|

Final PB |

5.53x |

8.40x |

The PB gap between the two has narrowed |

|

PE Increase Rate |

+346.6% |

+28.1% |

Dongshan’s valuation elasticity is significant |

|

PB Increase Rate |

+146.9% |

+35.0% |

Dongshan’s asset value reassessment is stronger |

|

2025 Expected PE |

35.6x |

22.3x |

Dongshan’s growth premium is higher |

|

2026 Expected PE |

25.4x |

15.5x |

Dongshan’s long-term valuation remains high |

The core conclusion of the valuation analysis is that Dongshan Precision, through business transformation and performance turning points, has gained higher valuation elasticity; while Huadian Shares, although stable in performance as an industry leader, is limited by its single business structure and lack of a “second growth curve,” resulting in relatively limited valuation increases.

4. Strategic Events: Disruptive Mergers vs. Extensional Expansion

The catalytic effect of significant events further amplifies the differences in market reactions.

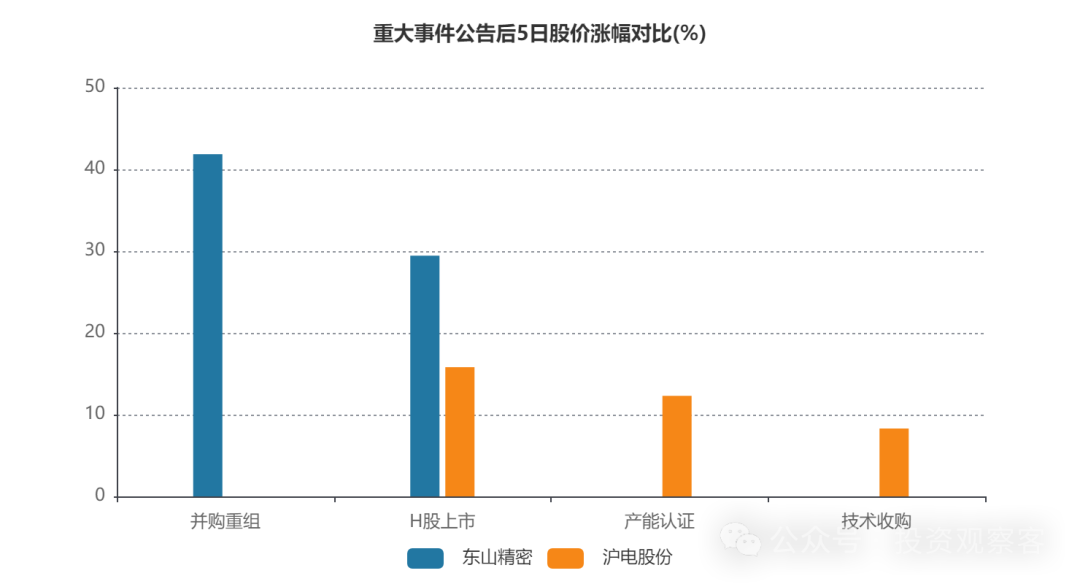

Dongshan Precision’s acquisition of Solstice is a paradigm-level leap. After the announcement, three key milestones (signing, payment, consolidation) cumulatively pushed the stock price up by 89.3%, accounting for over 52% of the total increase. Coupled with the H-share listing plan (aiming to raise 7 billion yuan for optical module expansion), the company not only broadened its financing channels but also clarified a “Chinese version of Coherent” story to international capital.

In contrast, Huadian’s production launch of its Thailand factory and H-share planning are more about the globalization extension of existing businesses. The market reaction has been tepid—after the H-share announcement, it only rose 15.8% in five days, far below Dongshan’s 41.2%. Investors clearly believe that without breakthroughs in new businesses, internationalization cannot support valuation leaps.

Dongshan Precision’s significant actions (such as the acquisition of Solstice Optoelectronics) have disruptive business potential, capable of changing the market’s perception of the company’s long-term value, thus gaining higher stock price feedback; while Huadian Shares’ strategic moves (such as the Thailand expansion) are more about scaling within an established track, leading to relatively limited market reactions. This strategic level difference is another key dimension to understanding the price performance divergence between the two companies.

|

Event Type |

Dongshan Precision |

Huadian Shares |

Difference Analysis |

|

Mergers and Acquisitions |

Acquisition of Solstice Optoelectronics (optical modules) |

Acquisition of Shengwei Technology equity (PCB technology) |

Dongshan’s acquisition opens up new tracks, while Huadian strengthens existing businesses |

|

Capital Market Actions |

H-share listing received enthusiastic response |

H-share listing reaction was tepid |

The market is more optimistic about Dongshan’s internationalization |

|

Capacity Expansion |

Global multi-site capacity layout |

Focus on Thailand base |

Dongshan’s layout is more diversified |

|

Technical Breakthroughs |

Achieved self-sufficiency in optical chip capabilities |

Enhanced PCB technology control |

Dongshan has higher technical barriers |

|

5-Day Post-Event Increase |

Highest single increase +41.86% (Solstice consolidation) |

Highest single increase +15.8% (H-share announcement) |

Dongshan’s event impact is stronger |

|

Cumulative Event Contribution |

Accounts for 52.2% of total stock price increase |

Accounts for about 25% of total stock price increase |

Dongshan relies more on event-driven growth |

5. Conclusion and Outlook: The Scissors Gap May Narrow

Dongshan Precision’s excess returns are the result of a resonance of four factors: business diversification, performance turning points, strategic mergers, and valuation reshaping. It has successfully convinced the market that this company is no longer just an FPC foundry but a technology platform at the intersection of AI and new energy.

Huadian Shares represents another path: focused, efficient, and strong in profitability, but lacking a second growth curve, making it difficult to achieve higher valuation elasticity.

Looking ahead to 2026, the probability of the scissors gap continuing to widen is decreasing:

·Dongshan needs to fulfill optical module orders (especially 1.6T) and maintain new energy growth; otherwise, high valuations will face a double whammy;

·If Huadian can break through in new fields such as CPO substrates and automotive radar, its valuation is expected to recover upwards.

Ultimately, the decisive factor in stock prices lies not in the K-line charts, but in the data centers of Meta, the battery packs of Tesla, and the yield curves of the laboratories of both companies.

#PCB #DongshanPrecision #HuadianShares #OpticalModules #HighEndPCBs #SuzhouListedCompanies

Previous research articles on the PCB industry:

PCB Industry Observation: High-end Capacity Expansion Soars, Ordinary Capacity Still in Price War

Comparative Analysis of Three Major PCB Industry Listed Companies in Guangdong: Shenghong Technology, Pengding Holdings, and Shennan Circuit