The semiconductor industry is thriving,according to a McKinsey study,with an expected annual growth rate of6% to 8% by 2030, with annual revenue projected to reach$1 trillion. The industry will have to double semiconductor production to keep up with future demand, but most manufacturing plants (commonly known as fabs) are already operating at full capacity. To increase supply, many companies have announced plans to build new fabs, with some already in the construction phase. In the process of coordinating the push for microelectronics revival, the U.S. is becoming a hotspot for fab construction.

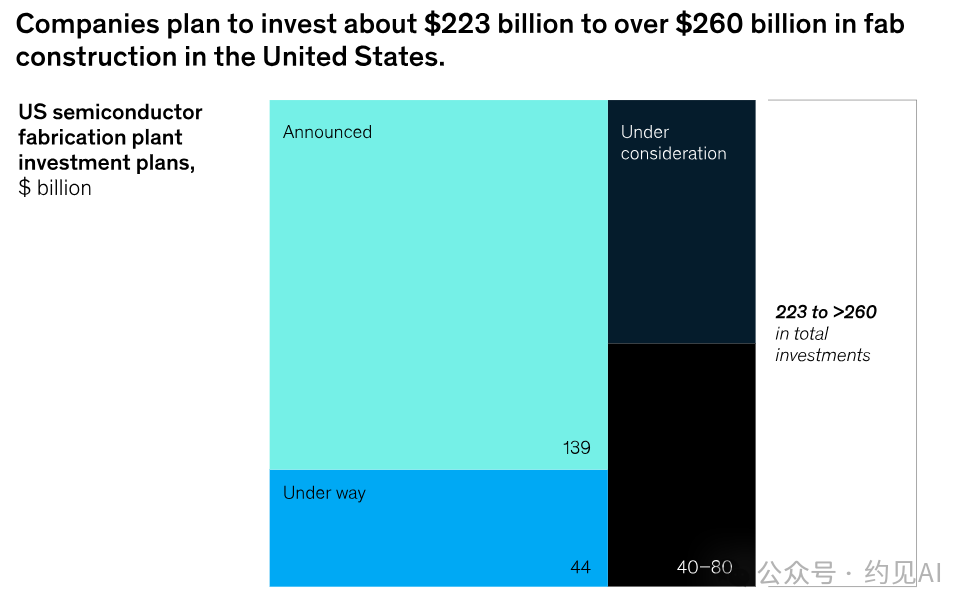

By 2030, the total value of semiconductor projects in the U.S. that are underway, announced, or under consideration is estimated to be$223 billion, exceeding $260 billion.

However, the current economic outlook is prompting several semiconductor companies to slow down capital deployment. Coupled with a strong outlook for future demand, this creates a dilemma: companies may decide to invest throughout the cycle to avoid future supply shortages while trying to manage cash flow constraints. Building fabs in the U.S. may also present challenges different from those in other countries. Some projects have already experienced delays related to labor and material shortages. More importantly, fluctuations in raw material commodity prices are injecting another layer of uncertainty into the construction process. What are the potential solutions for companies looking to continue building fabs in the U.S. amid all this uncertainty? A combination of creative financing, more thoughtful design, greater prefabrication, and better negotiation, scheduling, and cost control strategies.

The Construction Boom of U.S. Fabs

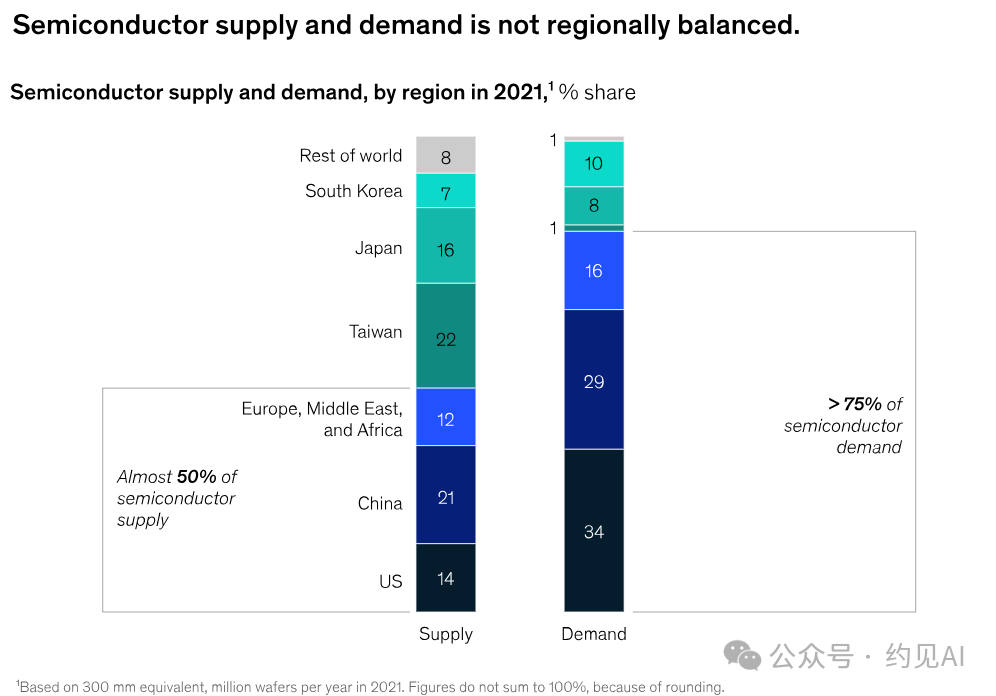

For years, chip manufacturing has been consolidated in Southeast Asia and China. According to a statement from the White House, U.S.-made semiconductors currently account for only about12% of the global total, down from30% three decades ago.

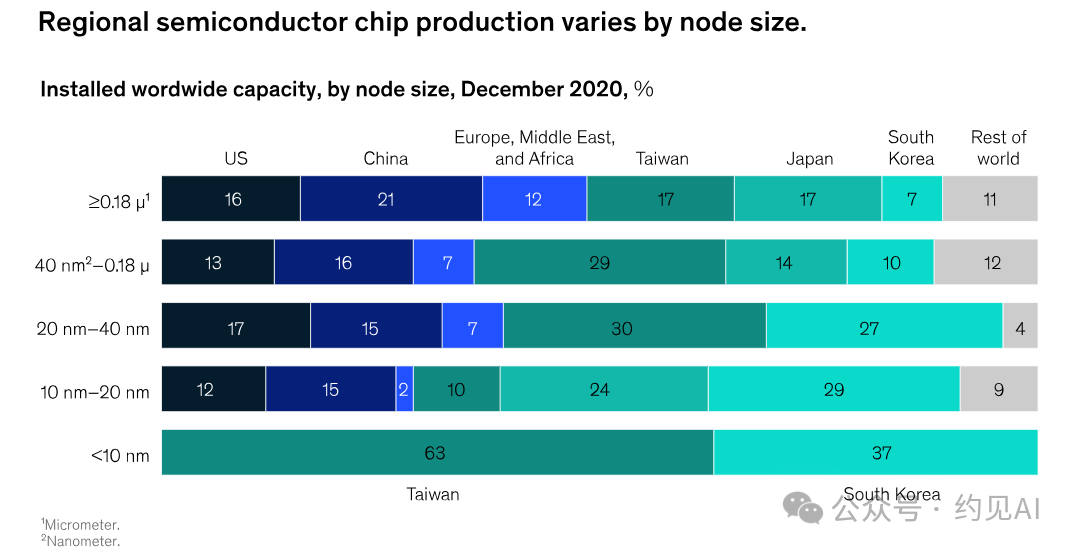

Depending on node size, cutting-edge chips (those with a node size smaller than10 nanometers) are primarily produced in East Asia, although some fabs outside the region are now ramping up production.

When supply chains are functioning well, companies have little incentive to establish new fabs outside Southeast Asia. However, due to the disruptions in the supply chain caused by the pandemic, challenges in chip output and distribution, the drought in Taiwan in 2021, and geopolitical issues have complicated matters. These considerations have prompted companies to develop new interest in diversifying fab locations and exploring sites in the U.S. At that time, the availability of subsidies was one of the main considerations when evaluating potential new sites.

In the U.S., the total investment for new fabs ranges from$223 billion to $260 billion, with approximately$183 billion attributed to projects that are underway or announced; the remainder involves projects still under consideration.

Most investments are directed toward specific geographic clusters. For example, Arizona and Texas are attracting investments because they already have a fab ecosystem, and local governments have historically provided incentives and helped coordinate the process. In addition to large incentives, Ohio is becoming an ideal location, announcing over $20 billion in investments for a fab in Columbus, while New York is offering incentives to encourage fab construction. Other states attracting investments include Indiana, New Mexico, Oregon, Utah, and Virginia.

The Major Challenges Facing U.S. Fab Construction

Semiconductor fabs are complex, capital-intensive projects at any location. However, in the U.S., fab construction is not common, and there is a high demand for construction talent across various industries, which may present semiconductor companies with more challenges than usual. Many of the issues they face fall into one of the following categories.

Shortage of Construction Talent

The U.S. has not seen large-scale fab construction for over 20 years, and there are few builders with the experience, capability, and expertise required to deliver these specialized projects. Compounding this issue, semiconductor companies must compete with companies in multiple industries, including residential construction, for various types of construction workers—from earthwork specialists to skilled electricians. Once the fabs are built and operational, they will also face competition for a very different type of talent: the technical staff required for fab operations.

The Semiconductor Industry’s Increased Focus on Sustainability

Many of the most important customers are looking to reduce emissions in the supply chain. However, many semiconductor companies have yet to clearly articulate their sustainability goals, with only about 60 out of approximately 2000 companies committing to emission targets.

Semiconductor manufacturing may come under particular scrutiny from end customers due to its high emissions associated with the final product. For example, over 70% of the lifecycle emissions associated with certain mobile phones are related to the manufacturing of the phone itself and the chipsets. As end customers increasingly focus on achieving net-zero emissions, it is expected that more semiconductor companies will commit to more ambitious and actionable emission targets.

Fab owners can also consider the accessibility of renewable energy resources more carefully when deciding where to build new main fabs, as typically 45% of emissions are related to electricity.

Complexity of the Supply Chain

A typical semiconductor production process may involve steps across five or more countries/regions and three or more global shipments. Due to industry consolidation, labor cost dynamics, and technological complexity, there are regional bottlenecks at nearly every step of the value chain. To enhance supply chain resilience, semiconductor companies may consider building or moving various parts of the value chain closer to new fab locations. Construction and operational material procurement strategies may need to be updated. Capital expenditures will extend beyond fab construction, as creating a true ecosystem will require additional infrastructure and suppliers.

Performance Management and Execution Difficulties

Under normal circumstances, delivering large or major capital projects on time and within budget is challenging. Current disruptive forces—commodity price fluctuations, inflation, supply chain disruptions, and an overheated labor market—make projects even more complex, and semiconductor companies may encounter obstacles even when following best construction practices throughout the project lifecycle. For example, too many projects have suffered delays in the delivery of critical long-lead mechanical, electrical, and plumbing systems, even when purchase orders were placed well in advance and confirmed by suppliers. More importantly, an overheated labor market may reduce productivity as companies struggle to find enough qualified construction workers, making it even more difficult to deliver facilities on time and within budget.

The Impact of Government Attitudes

The U.S. CHIPS and Science Act, signed into law by President Biden in 2022, is one of the Biden administration’s most significant domestic achievements. As a political opponent, Trump has inevitably criticized it. This is the norm in U.S. bipartisan politics.

Trump has repeatedly criticized the act. His most typical remarks label the CHIPS and Science Act as a“gift to chip companies” and “nonsense.” He believes that:

It wastes taxpayer money: He views this massive subsidy as a “gift” to profitable chip companies that would invest even without government funding.“Fat” political opponents: He specifically criticized Intel for investing in states like Arizona, which have Democratic senators strongly supporting this act. He believes this is using taxpayer money to create political achievements for opponents.

It distorts “America First”: While the act aims to promote “Made in America,” Trump sees it as an inefficient, wasteful form of “big government” intervention that contradicts his principles of tax cuts and deregulation to attract investment.