Storage, as a core branch of the semiconductor industry, serves as the “data granary” for electronic devices. However, training AI large models requires processing billions of images and trillions of data points, leading to a dual bottleneck of “insufficient capacity and lagging speed” in traditional storage. In this context, High Bandwidth Memory (HBM) has become a necessity for AI, while 3D NAND flash memory is racing towards 1000 layers. The storage industry is entering a period of accelerated technological iteration and reshaping. This article will break down core categories, analyze industry cycles, and focus on the breakthrough paths of Chinese enterprises.

Storage, as a core branch of the semiconductor industry, serves as the “data granary” for electronic devices. However, training AI large models requires processing billions of images and trillions of data points, leading to a dual bottleneck of “insufficient capacity and lagging speed” in traditional storage. In this context, High Bandwidth Memory (HBM) has become a necessity for AI, while 3D NAND flash memory is racing towards 1000 layers. The storage industry is entering a period of accelerated technological iteration and reshaping. This article will break down core categories, analyze industry cycles, and focus on the breakthrough paths of Chinese enterprises. 1. The Storage Industry: The Backbone of the Semiconductor Industry

1. The Storage Industry: The Backbone of the Semiconductor Industry

1. Market Position: A Core Pillar Second Only to Logic Circuits

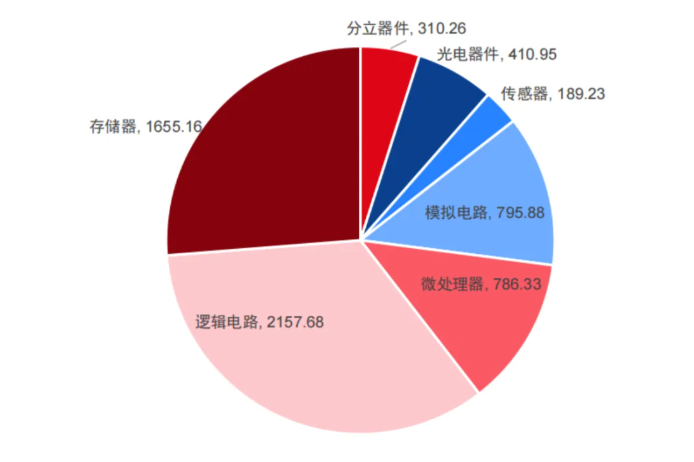

The semiconductor industry is divided into four main categories: integrated circuits, optoelectronic devices, etc., among which integrated circuits include memory and logic circuits. According to WSTS data, the global semiconductor market sales are expected to reach $630.549 billion in 2024, with storage chips accounting for $165.516 billion, representing 26.2% of the market share, far exceeding analog circuits and microprocessors, second only to logic circuits—every $4 of semiconductor products globally includes $1 from storage chips.

2. Core Types: Functional Division of Volatile and Non-Volatile Storage

Based on data retention characteristics after power loss, storage chips can be divided into two categories:

- Volatile Storage: Data is lost when power is off, used for temporary storage

- SRAM: Extremely fast but costly and low capacity, suitable for CPU cache;

- DRAM: Moderate speed, large capacity, low cost, is the core of DDR memory and mobile operating memory.

- Non-Volatile Storage: Data is retained when power is off, used for long-term storage

- Flash Memory: Mainstream category, NOR Flash stores small data (e.g., boot programs), NAND Flash has large capacity (suitable for SSDs and mobile storage);

- EEPROM/PROM: Very small capacity, used for storing settings like router parameters.

Among them, DRAM and NAND Flash are the absolute main forces, accounting for 41.68% and 58.26% market share respectively in 2024, together monopolizing nearly 99% of the market.

3. Global and Chinese Markets: Demand-Driven Scale Expansion

- Global Market: Expected to reach $165.516 billion in 2024, WSTS predicts it will increase to $189 billion in 2025 (year-on-year +13%), with AI data storage demand as the core driving force.

- Chinese Market: Expected to reach 259.1 billion yuan in 2023, with an average annual growth rate exceeding 20% from 2018 to 2023, DRAM accounting for 56% and NAND Flash over 40%. As the largest consumer electronics and data center market globally, China has become a core demand area for storage chips.

4. Core Application Scenarios: From Consumer End to AI Servers

|

Scenario |

NAND Flash Capacity Share (2023) |

DRAM Capacity Share (2024E) |

Core Applications |

|

Mobile Phones, Tablets |

34% |

34% |

128GB Storage (NAND), 8GB Operating Memory (DRAM) |

|

Computers |

26% (Consumer SSD) |

15% |

DDR Memory Modules (DRAM), SSD (NAND) |

|

Servers / Data Centers |

14% (Enterprise SSD) |

32% |

AI Servers (requiring HBM + high-capacity DRAM) |

2. DRAM: The Speed Race in the AI Era

1. Subcategories: Technological Differentiation for Scenario Adaptation

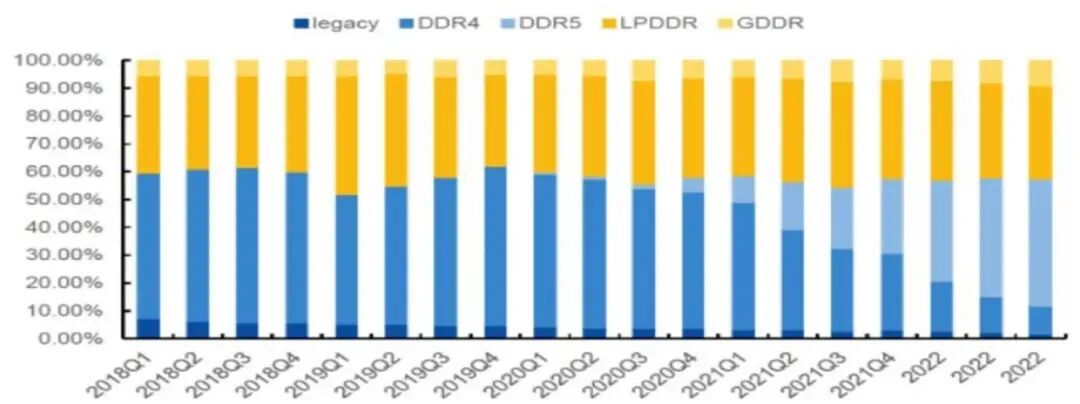

- DDR: Double Data Rate Synchronous DRAM, suitable for desktops and servers, evolving from DDR1 to DDR5, with transmission speeds increasing from hundreds of MT/s to 6400MT/s, DDR5 has become mainstream for new computers and servers.

- LPDDR: Low Power DDR, aimed at mobile devices, with LPDDR5X achieving transmission speeds of 8533MT/s, balancing performance and battery life.

- GDDR: Graphics DDR, suitable for graphics cards, with GDDR6X bandwidth exceeding 1TB/s, meeting the needs of AAA games and graphic design.

Yole data shows that DDR and LPDDR together account for 90% of DRAM applications.

2. Technological Evolution: From 2D Shrinking to 3D Stacking

- Process Shrinking: Since 2016, focus has been on 10nm level iterations, with the current mainstream being 1γ (Micron) and 1c (Samsung / SK Hynix) processes. In June 2025, Micron will launch the sixth generation of 10nm level LPDDR5X, achieving capacity enhancement and power reduction.

- 3D DRAM: To address the bottleneck of process shrinking, density is increased through multi-layer stacking and vertical interconnection. SK Hynix proposes to apply 3D DRAM to processes below 10nm by 2055, with the density advantages of 3D Super-DRAM suitable for AI server scenarios.

3. HBM: The Key to Breaking the “Memory Wall” in AI

- Technical Principle: By stacking DRAM chips in 3D, using through-silicon vias and micro-bump technology for vertical connections, and closely packaging with GPU in 2.5D, the data transmission distance is reduced from centimeters to hundreds of micrometers, with HBM3E bandwidth exceeding 1TB/s (10 times that of traditional DRAM) and lower power consumption.

- Manufacturing Process: Die preparation (through-silicon via processing) → Die-to-Wafer stacking (micro-bump connection) → Integration with GPU packaging, currently mainstream 8-layer stacking, with future upgrades to 12/16 layers.

- Market Competition: SK Hynix (leading in HBM3E/HBM4, expected to occupy 60% of the 3D NAND 3E 8Hi share by 2026), Micron (supplying 12-layer HBM4 samples), and Samsung (not yet entering the Nvidia supply chain) dominate the market.

- Future Prospects: Yole predicts a compound annual growth rate of 33% for HBM before 2030, with revenue exceeding 50% of total DRAM revenue, with AI as the core growth engine.

4. Market Landscape: Three Giants Dominate 95% of the Market

Data from Q1 2025 shows that SK Hynix surpassed Samsung for the first time with a 36.7% share, while Samsung held 35.6%, and Micron was third with 22.9%, with the three giants accounting for a total of 95.2%. High barriers (hundreds of billions in investment for a single production line and rapid technological iteration) have led small and medium-sized manufacturers to only occupy niche markets.

5. Next Generation DDR6: Commercial Launch in 2027

JEDEC will complete the DDR6 draft by the end of 2024, planning for platform certification in 2026 and commercial use in servers in 2027, with transmission speeds reaching 8800-21000 MT/s, complementing HBM (DDR6 for general devices, HBM for AI).

3. NAND Flash: The Second Half of the Capacity Race

1. Generational Evolution: Balancing Capacity and Performance

|

Type |

Storage Density (per cell) |

Erase/Write Lifespan |

Core Features |

Applicable Scenarios |

|

SLC |

1 bit |

100,000 times |

Fast speed, high cost |

Industrial control, aerospace and military |

|

MLC |

2 bits |

10,000 times |

Balanced performance |

High-end industrial products |

|

TLC |

3 bits |

3,000 times |

High cost-performance ratio, most popular |

Consumer SSDs |

|

QLC |

4 bits |

1,000 times |

Large capacity, low cost |

Cloud storage, surveillance storage |

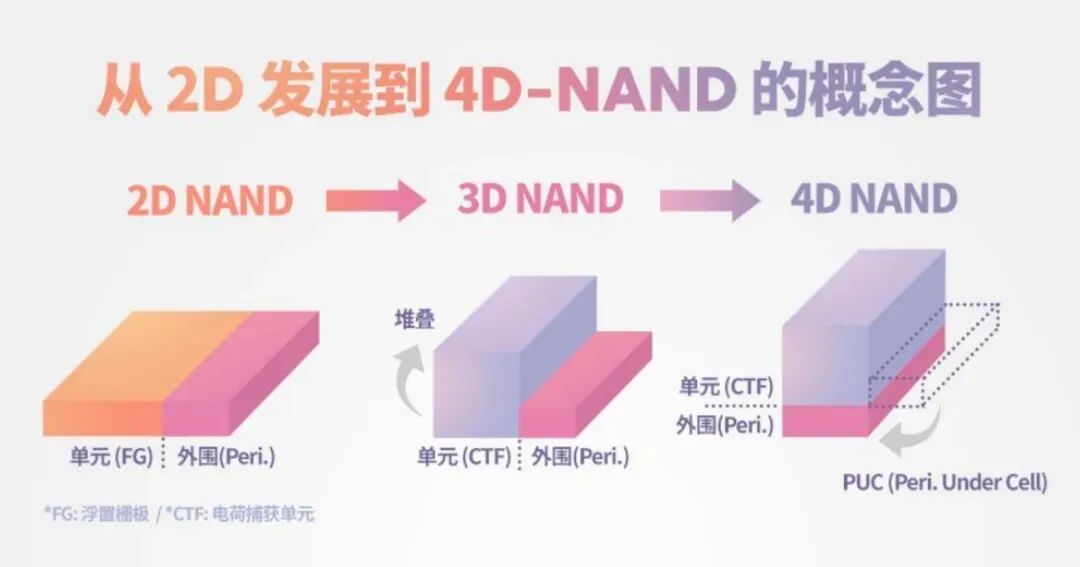

2. 3D NAND: The Stacking Revolution from 24 Layers to 1000 Layers

- Technical Value: By replacing 2D shrinking with vertical stacking, 300-layer products have a capacity more than 10 times that of 2D NAND, while reducing cell interference and improving reliability, currently fully replacing 2D NAND.

- Layer Breakthrough: From 24 layers in 2014 to 276-321 layers in 2024, Kioxia plans to achieve 1000 layers by 2027, with storage density reaching 100 Gbit/mm².

- 4D NAND: SK Hynix will launch 321-layer 4D NAND in 2024, placing peripheral circuits below the storage cells, increasing density by 10%-20%, not through dimensional upgrades but through architectural optimization.

3. Market Landscape and Price Trends

- Competitive Landscape: In Q3 2024, Samsung (32.9%), SK Hynix + Solidigm (19.1%), Kioxia (17.0%), Micron (12.4%), and Western Digital (9.9%) together accounted for 91.3%, with Yangtze Memory Technologies (200 layers + X4 series) accelerating its catch-up.

- Price Increase: In H1 2025, Samsung and others will reduce low-margin production capacity, coupled with demand from AI servers and Nvidia’s Blackwell chip, TrendForce predicts a 5%-10% quarter-on-quarter increase in contract prices in Q3 2025, with enterprise SSDs leading the price rise.

4. Future Trends: Layer Count, Scenarios, and AI Integration

- Continuous Layer Breakthrough: 1000-layer products will achieve single-chip 10Tb+ and SSD 100TB+;

- Scenario Expansion: Automotive-grade (high temperature and vibration resistance), industrial-grade demand growth exceeds consumer-grade;

- Technological Innovation: The rise of storage-compute integrated architecture reduces transmission latency.

4. Chinese Storage Enterprises: The Path of Breakthrough from 0 to 1

1. Yangtze Memory Technologies (NAND Flash Leader)

- Model and Products: IDM model, covering 3D NAND wafers, SSDs, etc., suitable for mobile phones, servers, and other scenarios;

- Core Technology: Xtacking technology, separating the manufacturing of storage arrays and peripheral circuits before bonding, with significant speed and power advantages in the fifth generation products;

- Progress: Mass production of 128 layers in 2021 → mass production of 200 layers + X4 series in 2024, with significant cost-performance advantages in the consumer market, entering the domestic server supply chain.

2. ChangXin Memory Technologies (DRAM Breakthrough)

- Business Focus: Focused on DDR4/DDR5, LPDDR4/LPDDR5, applicable to consumer electronics and servers;

- Development History: Started construction in 2017 → mass production of DDR4 in 2019 → completion of phase two in 2022, with rapid capacity expansion;

- Technological Breakthrough: Achieved mass production at the 10nm process level, with DDR5 transmission speeds reaching 4800 MT/s, completing the leap from 0 to 1.

3. Supporting Enterprises in the Industry Chain

- Lanqi Technology: Leading in DDR5 memory interface chip technology, benefiting from the increasing penetration of DDR5;

- GigaDevice: Leader in NOR Flash, expanding into niche DRAM and MCU, covering consumer electronics and industrial fields;

- Jiangbo Long: Leading in storage modules (Lexar brand), with a 72.48% year-on-year revenue growth in 2024;

- Bawei Storage: Combining storage products with advanced packaging and testing capabilities, supporting SiP packaging;

- DeYi Microelectronics: Core manufacturer of AI storage control chips, suitable for AI mobile phones / PCs / server needs..

About Us

Follow: Yosoar

Kunshan Yosoar New Materials Co., Ltd. (referred to as “Yosoar”) was established in 2005, focusing on the agency of international high-precision instruments and equipment, deeply cultivating the industrial testing field for nearly 20 years, and is an important strategic partner of Zeiss (Germany) coordinate measuring machines, scanning electron microscopes, and other equipment in the Chinese market. For many years, the company has adhered to the principle of “technology as the source, management as the support, and users as the goal,” helping customers complete project innovation and implementation more quickly, accurately, and efficiently, achieving a win-win situation for both Yosoar and its customers. Contact: 4001500108

WeChat ID丨Yosoar

Website丨www.cmm-yosoar.com