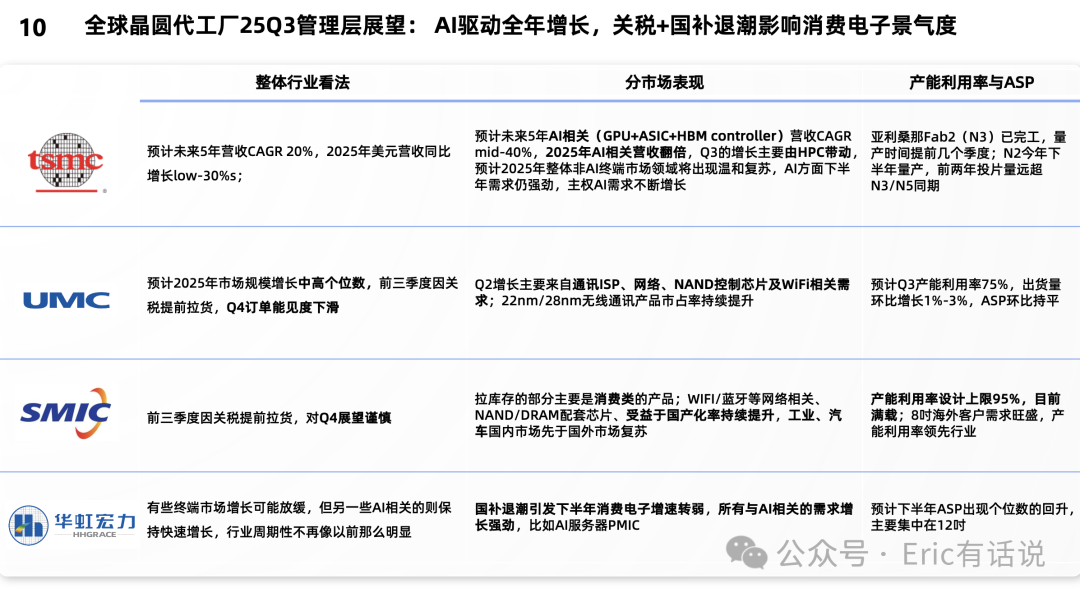

- Taiwan Semiconductor Manufacturing Company (TSMC):

-

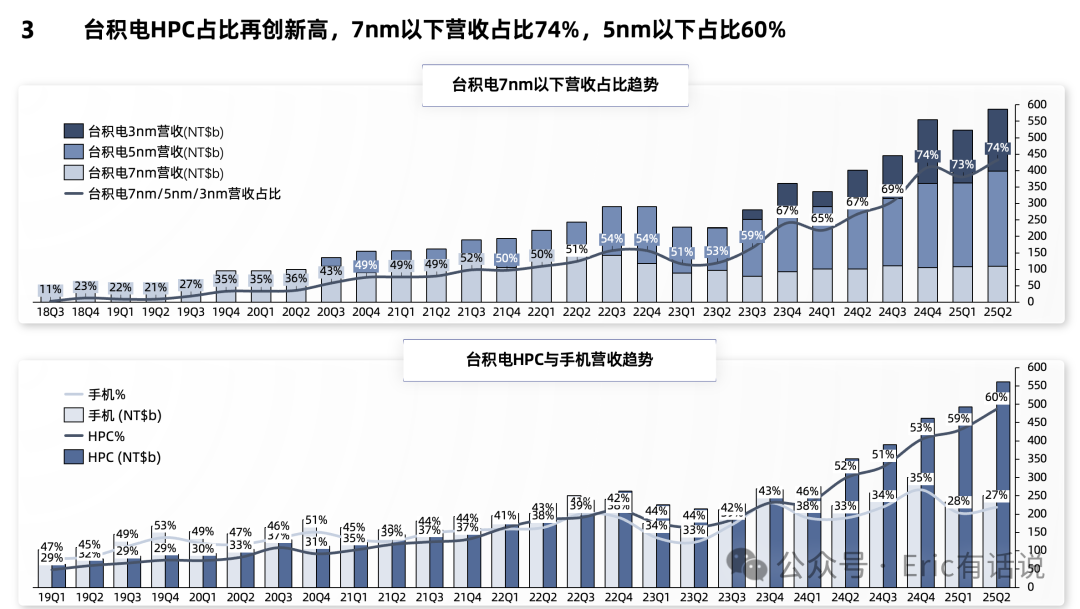

It is expected that in the next5 years, revenue will grow at a CAGR of20%, with a year-on-year growth oflow-30% in 2025 (up from mid-20% last quarter);

-

It is expected that in the next5 years, revenue related to AI (GPU+ASIC+HBM controller) will grow at a CAGR ofmid-40%, with AI-related revenue expected to double in 2025; the growth in Q3 will be primarily driven byHPC, and it is expected that the overall non-AI terminal market will see a moderate recovery in 2025; demand for AI remains strong in the second half of the year, with sovereign AI demand continuously increasing;

-

Arizona Fab 2 (N3) has been completed, with mass production ahead of schedule by several quarters; N2 is expected to begin mass production in the second half of this year, with the output in the first two years far exceeding that of N3/N5 in the same period;

- United Microelectronics Corporation (UMC):

-

It is expected that the market size will grow in the mid-single digits by 2025; the first three quarters saw a pull-in of orders due to tariffs, while Q4 order visibility is declining;

-

Q2 growth was primarily driven by communications, ISP, networking, NAND control chips, and WiFi related demand; the market share of 22nm/28nm wireless communication products continues to rise;

-

It is expected that Q3 capacity utilization will be at75%, with a quarter-on-quarter shipment growth of1%-3%, and ASP remaining flat quarter-on-quarter;

- Semiconductor Manufacturing International Corporation (SMIC):

-

Due to tariffs, there was a pull-in of orders in the first three quarters, and the outlook for Q4 is cautious;

-

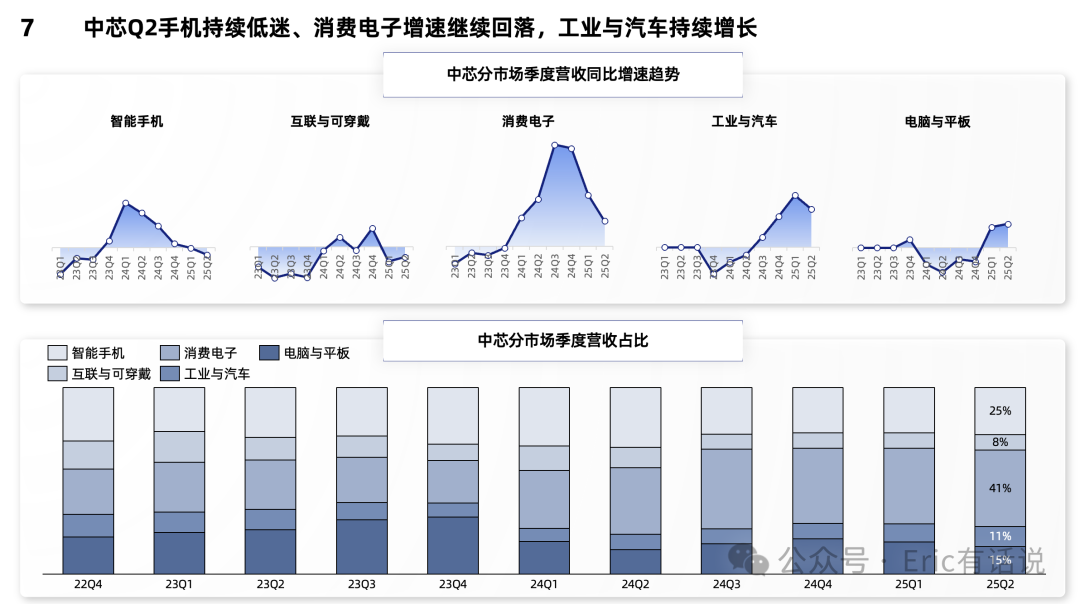

The inventory pull-in was mainly for consumer products; network-related products such as WIFI/Bluetooth, NAND/DRAM supporting chips are benefiting from the continuous increase in domestic production rates; the industrial and automotive domestic markets are recovering ahead of foreign markets;

-

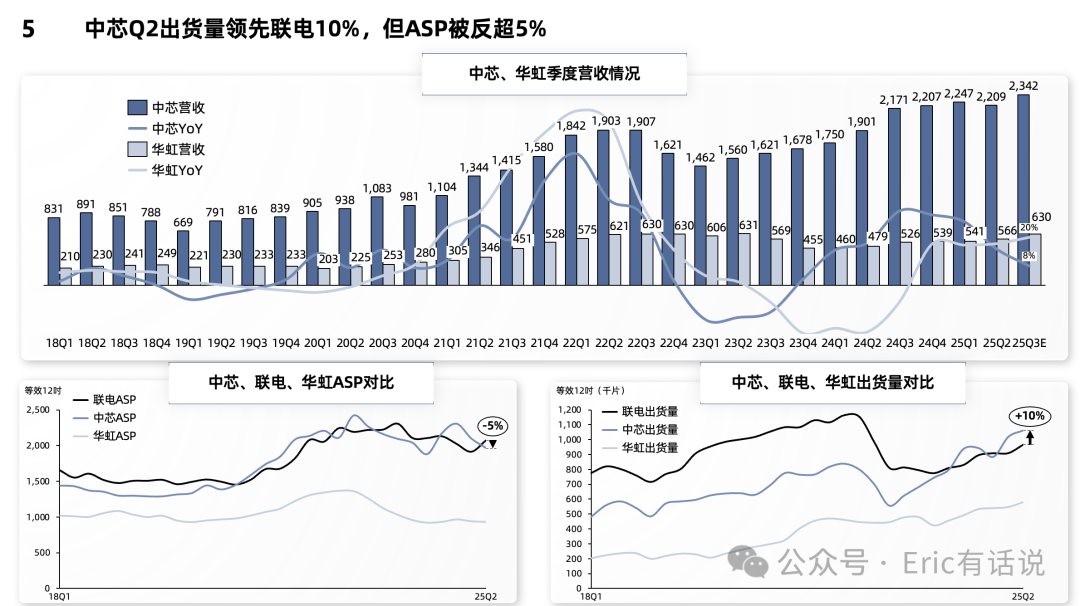

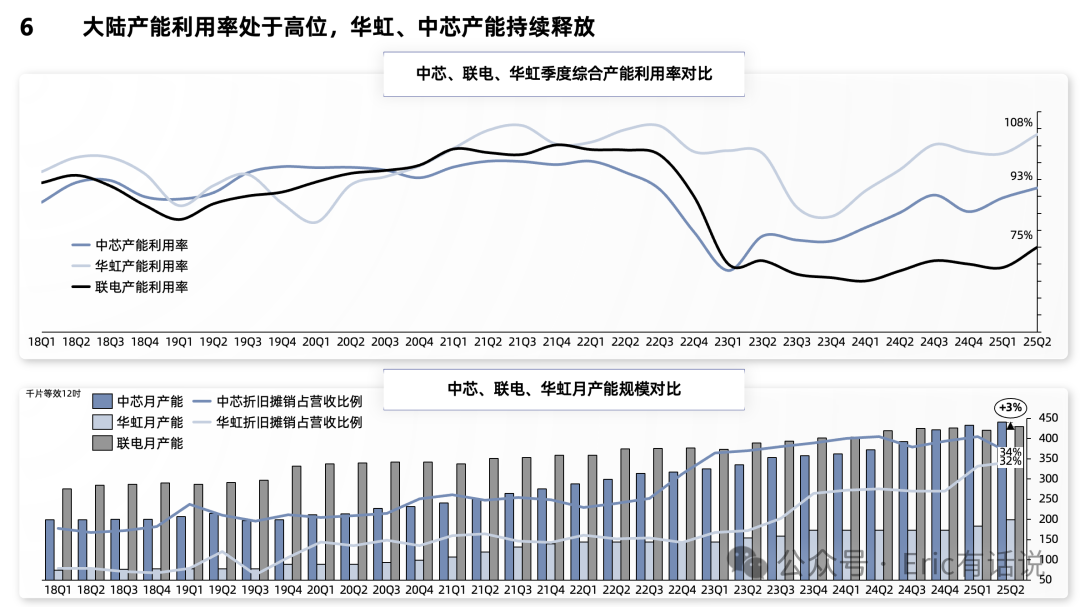

Capacity utilization is designed to be capped at95%, and currently, it is fully loaded; demand from overseas customers for 8-inch wafers is strong, with capacity utilization leading the industry;

-

Huahong Semiconductor:

-

Some terminal market growth may slow, but others related to AI continue to grow rapidly, with industry cyclicality no longer as pronounced as before;

The withdrawal of national subsidies has led to a slowdown in the growth rate of consumer electronics in the second half of the year; all AI-related demand is growing strongly, such as AI server PMIC;

-

It is expected that ASP will see a single-digit rebound in the second half of the year, mainly concentrated in 12-inch wafers;

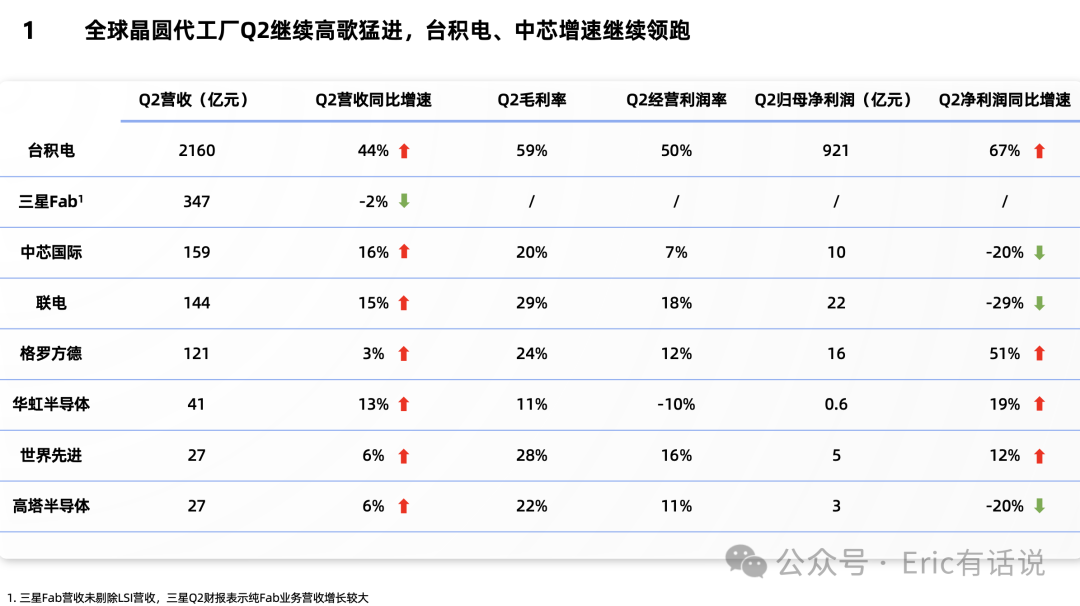

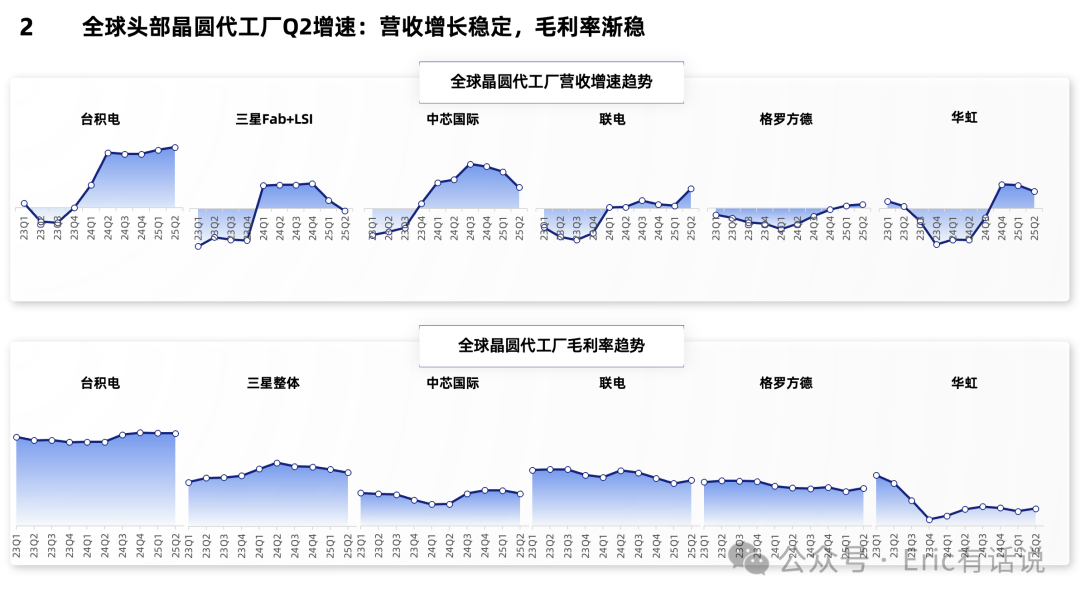

Overall, in Q2 2025, the world’s leading foundries continue to thrive, with Tier 1 advanced processes leading in growth, and Tier 2 mature processes returning to growth; in early 2025, AI remains the largest growth point in semiconductors, with general AI demand beginning to spread to mature process supporting chips. Uncertainties such as tariffs and the withdrawal of national subsidies have led to a slowdown in consumer electronics represented by mobile phones and PCs; benefiting from domestic substitution and the China for China strategy, SMIC and Huahong will continue to expand production, with 8-inch shipments being a major highlight for SMIC in Q2, as overseas customers rapidly increase their orders.

Previous articles on global foundries (from recent to older):

“Global Foundries Q1 2025: AI Drives Annual Growth, Low Visibility for Mobile Phones and PCs in the Second Half“

“Global Foundries Q4 2024: General AI Demand Continues to Spread, Automotive and Industrial Markets Expected to Begin Recovery“

“Global Foundries Q3 2024: General AI Demand Expected to Erupt, Mature Processes Begin to Benefit“

“Global Foundries Q2 2024: General AI Demand Erupts, Advanced Processes Gain, Mature Processes Benefit“

“Overview of Global Semiconductor Foundries Q1 2024“

“Overview of Global Semiconductor Foundries Q4 2023“

“Overview of Global Semiconductor Foundries and Wafer Factories Q3 2023“