Investment Logic:

- Performance has improved for eight consecutive quarters, with a breakout in Q2 2025, awaiting Q3 data;

- Successful product diversification, expected to become a platform enterprise;

- Increased usage of MEMS products in IoT and AI-related fields such as AI glasses and embodied intelligent robots, with the company actively expanding, etc.!

- Overall, the company’s growth mainly comes from two major sectors: “scaling existing business” and “landing emerging businesses,” covering three high-growth tracks: consumer electronics, automotive electronics, and AI/robotics.

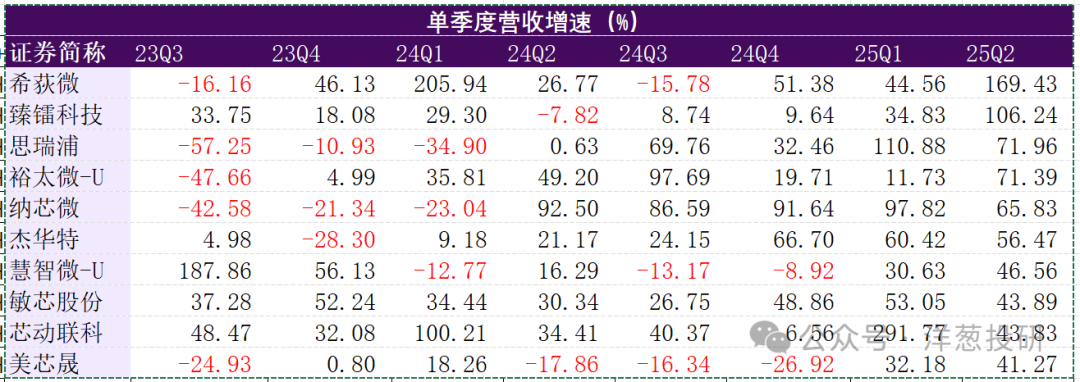

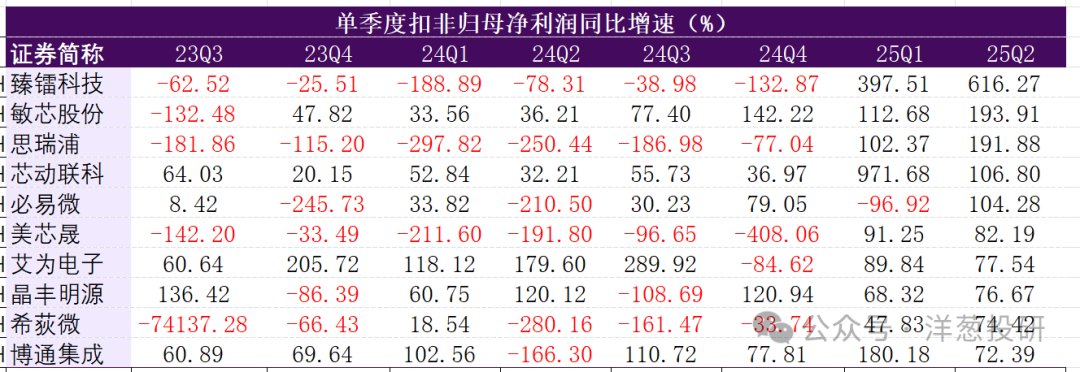

Recently, some indicators of the analog chip sector were compiled, and the protagonist of this article, Minxin Co., Ltd., has indeed performed quite well over the past two years.

It is evident that Minxin’s performance is continuously improving.I previously wrote an article about the MEMS niche in the military industry: Chip Dynamics breaks a 50-year monopoly! This “military MEMS leader” has an 85% gross margin and is positioned in the trillion-yuan humanoid robot track. After the research was published on August 12, the company encountered a semiconductor wave, with its stock price rising from 66 yuan to 88 yuan in a week, which is quite aggressive.Below is an analysis of Minxin Co., Ltd., which is positioned in consumer-grade MEMS products. This account will provide some simplified information; more details are welcome for discussion in the comments section. The information I have gathered has many limitations

It is evident that Minxin’s performance is continuously improving.I previously wrote an article about the MEMS niche in the military industry: Chip Dynamics breaks a 50-year monopoly! This “military MEMS leader” has an 85% gross margin and is positioned in the trillion-yuan humanoid robot track. After the research was published on August 12, the company encountered a semiconductor wave, with its stock price rising from 66 yuan to 88 yuan in a week, which is quite aggressive.Below is an analysis of Minxin Co., Ltd., which is positioned in consumer-grade MEMS products. This account will provide some simplified information; more details are welcome for discussion in the comments section. The information I have gathered has many limitations  .1. Company Overview

.1. Company Overview

1.Basic Information and Development History

|

Company Name |

Suzhou Minxin Microelectronics Technology Co., Ltd. |

|

Established/Listed |

Founded in 2008, listed on the Sci-Tech Innovation Board in August 2020 |

|

Share Capital |

Total share capital: 56.01 million shares, circulating share capital: 37.80 million shares |

|

Shareholders |

As of the first half of 2025, there are 0.7 million shareholders, with an average market value of about 550,000 yuan |

|

Actual Controller |

Li Gang (controls 24% of the company’s shares, directly holds 19.18% of the shares) |

|

Main Business |

Research and sales of various MEMS sensors |

Company Development History:

In 2007, Dr. Li Gang (born in 1975, undergraduate from University of Electronic Science and Technology, master’s in MEMS from Peking University, PhD in Electronic Engineering from Hong Kong University of Science and Technology) and the company’s technical team (two partners, Hu Wei and Mei Jiaxin, etc.) established Minxin Co., Ltd. in Suzhou as part of the first batch of leading talents in the Suzhou Industrial Park, receiving financial and policy support from the park.

In 2020, the company was listed on the Sci-Tech Innovation Board, raising 8.34 billion yuan with an issuance price of 62.67 yuan; in 2023, it completed a round of targeted issuance raising 126 million yuan at an issuance price of 54.99 yuan.

Minxin Co., Ltd. has four core subsidiaries, which constitute the main sources of the company’s revenue.

As one of the few listed companies in China that master the design and manufacturing processes of various MEMS chips, the company is committed to becoming an industry-leading MEMS chip platform enterprise.

The company has independent research and development capabilities and core technologies in all aspects of MEMS sensor chip design, wafer manufacturing, packaging, and testing, and can independently design ASIC chips that provide signal conversion, processing, or driving functions for MEMS sensor chips, achieving domestic production in all production processes of MEMS sensors. The company’s main product lines currently include MEMS acoustic sensors,MEMS pressure sensors, andMEMS inertial sensors, with the acoustic sensor chip shipment volume ranking third globally.

The company primarily focuses on the consumer electronics industry (such as mobile phones, computers, headphones, smartwatches, etc.), actively expanding into downstream markets such as automotive, industrial control, and medical.

The company has its own packaging and testing factory, while wafer foundry is done through companies like China Resources Microelectronics. Generally, MEMS processes do not have high requirements for manufacturing processes, many are micron-level processes, but have high customization requirements, which is why overseas giants adopt the IDM model.

The company’s revenue structure by product is as follows:

(1)Revenue Structure

The company’s main revenue sources areMEMS acoustic sensors and pressure sensors, with pressure sensors seeing a continuous increase in volume in recent years, also driving the overall gross margin of the company.

The company’s inertial sensors had a negative gross margin in 2023, but have been climbing since then, with revenue from inertial sensors approaching20 million yuan in the first half of 2025, and gross margin rising to17.38%. This segment competes with Chip Dynamics, but Chip Dynamics’ MEMS inertial sensors are high-performance products mainly used in the military sector.

Therefore, the company has transitioned from relying on a single acoustic sensor to developing multiple categories simultaneously, with pressure sensors now surpassing acoustic sensors as the main source of revenue.

(2)Customer Situation of Different Products:

MEMS acoustic sensor products are widely used in consumer electronics such as smartphones, tablets, laptops, smart homes, and wearable devices, with specific brands includingSamsung, Xiaomi, Transsion,OPPO and Lenovo, etc.

MEMS pressure sensor products are mainly applied in consumer electronics, automotive, and medical fields, with electronic blood pressure monitors’ main customers including Lixun Medical and Jiuan Medical.

MEMS inertial sensors (mainly triaxial accelerometers, IMUs, etc.) focus on the consumer electronics field, with major customers coveringleading consumer electronics brands andODMs (Original Design Manufacturers).

Minxin Co., Ltd. hasinitiated research and development in the field of robot sensors, but currently has not formed large-scale customer orders and is still in thetechnical project and sample testing stage.

Its subsidiaryZhihong Microelectronics (responsible for IMU product R&D and sales) has achieved breakthroughs in new models of IMUs for automotive and robotics applications, with significant revenue growth in the first half of 2025. However, the current customers in the robotics field are mainly early cooperatingODM manufacturers, and have not yet entered the supply chain of leading humanoid robot manufacturers (such as Tesla’sOptimus, and UBTECH’sWalker series).

3. Capacity Layout

(1)Suzhou Headquarters:3600㎡MEMS process line and1100㎡ R&D pilot line (6 inch wafer-level packaging, with a maximum monthly capacity of8000 wafers);

(2)Shanghai Zhangjiang Laboratory: Algorithm andASIC design center (low-power Σ-Δ ADC, smart TWS algorithms)

(3)Shenzhen Nanshan Office: Close to South China customers,48 hours rapid failure analysis response

4. Team Situation

In addition to the company’s founder, there are2 partners, both with technical backgrounds.

Mei Jiaxin (born in 1978) graduated from Peking University with a major in Microelectronics, responsible for leading the R&D of MEMS sensor chip design and manufacturing processes;

Hu Wei (born in 1976) graduated from Nanjing University with a major in Microelectronics and Solid Electronics, responsible for leading the R&D of MEMS sensor packaging and testing processes, but Hu Wei will leave in September 2024. The company promoted Yang Hongyuan from the marketing department to vice president to strengthen market promotion. Meanwhile, the original vice president Zhang Chenliang also left.

Hu Wei’s departure is indeed difficult for external personnel to understand, and there are channels indicating he is starting a business. After promoting Yang Hongyuan, the company’s revenue and gross profit have increased.

5. R&D and New Products

|

R&D Strategy |

Focus on2 cores: chip structure design and process implementation; Become an industry-leading MEMS chip platform |

|

Continuously progressing products with results |

Acoustic MEMS chips and sensors; Pressure sensor chips and sensors, modules; Inertial sensor chips; Pressure-sensitive sensor chips; Flow sensor chips; Microfluidic biological detection chips; MEMS optical sensors; Piezoelectric ultrasonic transducers PMUT; |

|

Technical Layout and Improvements |

MEMS multi-axis force sensors; MEMS microfluidic chips; MEMS optical sensors; MEMS inertial sensors; High signal-to-noise ratio digital MEMS microphone sensors; Bone conduction sensors; PMUT; MEMS speakers; Altimeter sensors |

More detailed product information is disclosed in the company’s semi-annual report.

2. Industry Overview

1. MEMS Product Overview

MEMS (Micro-Electro-Mechanical Systems) technology was invented in the 1980s and is a technology for manufacturing micro-mechanical electronic systems using silicon-based semiconductor manufacturing processes, initially applied in the automotive and military fields, with main products includingMEMS sensors and MEMS actuators.

MEMS processes are essentially a micro-manufacturing technology, and chips manufactured based on MEMS technology have characteristics of low power consumption, miniaturization, and intelligence.MEMS chips, as the forefront of connecting the real world and the digital world, are known as“chips that are more analog than analog chips”.

2. MEMS Product Development History and Applications

Before the advent of 4G networks, due to limited data transmission and carrying capacity of communication networks,the market demand for MEMS sensors was very limited, but since 2007, with the rapid popularization and development of consumer electronics represented by smartphones, the commercialization of MEMS has significantly accelerated. However,MEMS devices and downstream smart sensor markets are still in the early stages of development.

However,MEMS has greatly benefited from5G and the Internet of Things, with a significant increase in market demand for edge devices’ perception capabilities in the 5G era, whileMEMS devices’ low power consumption, high consistency, and miniaturization greatly meet this demand. At the same time, sensors are the core data entry point of the Internet of Things, and the development of the Internet of Things promotes the popularization of smart terminal devices, driving the growth ofMEMS demand.

3. MEMS Process Characteristics

MEMS production processes have the characteristics of“multi-category, high customization”, which to some extent limits large-scale development and brings development opportunities for Chinese enterprises.

MEMS sensor chips have diversified and low-power characteristics, and during the manufacturing and packaging processes, requirespecific processes, equipment, and materials, and have special requirements for wafer manufacturing and packaging production lines. Therefore, whether choosing a foundry model or building its own production line,MEMS sensor chip design companies must possess process R&D capabilities and professional skills to debug and operate related production lines.

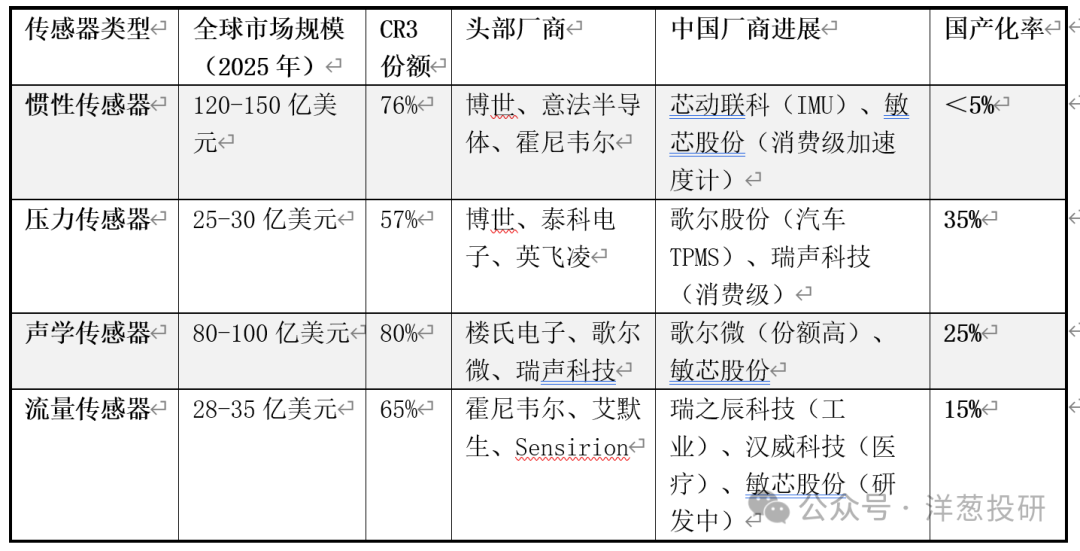

The market scale and competition situation of different product sensors are as follows:

4. Company Financials and Comparisons

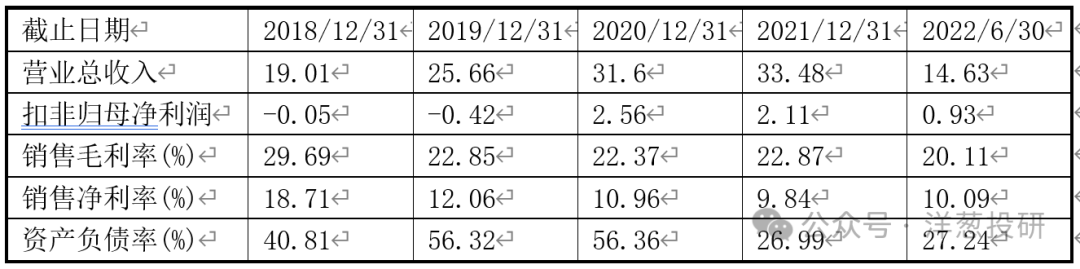

1.Basic Financial Situation of the Company

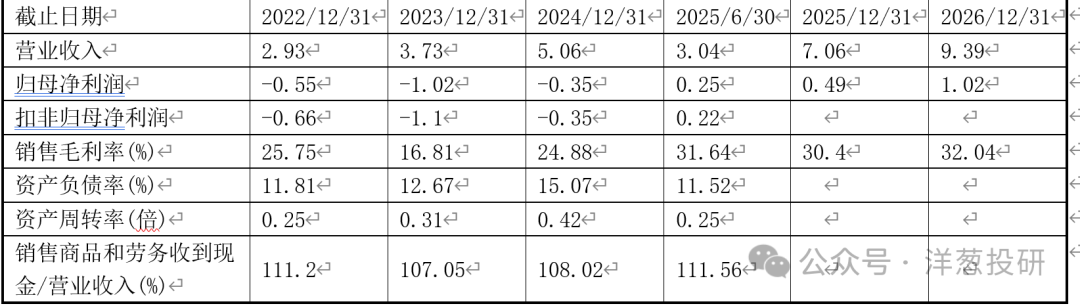

The company’s basic financial data is as follows:

Data for 2025-2026 is provided by Wind’s consensus earnings forecast. The company has seen steady revenue growth over the past three years, with gross margins gradually improving except for an anomaly in 2023. The company is expected to turn a profit in the first half of 2025, with gradual improvements in the future. The company’s debt-to-asset ratio is at a low level, and cash flow is in good condition.

The gross margin dropped significantly in 2023 due to

(1)Weak demand in consumer electronics, intense competition downstream, and the company actively lowered the prices of some products to gain market share and reduce inventory, which directly pulled down the gross margin. At that time, the company’s core business wasMEMS acoustic sensors, with gross margins dropping from about20% in 2022 to11.36% in 2023;

(2)The company’s IPO in 2020 raised funds for the“MEMS Sensor Technology R&D Center Construction Project” and the“MEMS Sensor Production Base Construction Project,” which were fully completed in 2023, gradually releasing production capacity. However, the fixed costs such as depreciation of fixed assets and amortization of intangible assets have significantly increased due to the commissioning of these projects.

2.Core Stock Comparisons

Currently, the main listed companies in the A-share market related to MEMS include Chip Dynamics, but Chip Dynamics mainly focuses on MEMS inertial sensors, with its core product being MEMS gyroscopes, primarily used in the military sector.

In the consumer-grade sector, Goertek (MEMS acoustic sensors) and Amperex (pressure sensors, etc.) are notable. Goertek is a subsidiary of Goertek Co., Ltd., which plans to split and go public, and withdrew its materials in 2023. The basic financial data is as follows:

Comparison between Amperex and Minxin Co., Ltd.:

① Basic Situation

Both Amperex and Minxin Co., Ltd. arelisted companies in the domestic sensor industry, with core businesses centered aroundMEMS sensors and related products, focusing on high-growth downstream fields such as automotive electronics, industrial control, and consumer electronics. The core difference between the two is that Amperex focuses on pressure sensors and temperature sensors, extending into torque sensors, oxygen sensors, and other fields; while Minxin Co., Ltd. focuses onMEMS acoustic sensors, pressure sensors, and inertial sensors, with a greater emphasis on penetration into consumer electronics andAIoT devices.

Amperex’s product matrix is centered on pressure sensors (accounting for about50%), temperature sensors (accounting for about40%), covering three major technical routes: ceramic capacitive, MEMS, and glass micro-melting, applied in automotive (thermal management systems, braking systems), home appliances (smart temperature control), and industrial control (pressure monitoring) scenarios.

② Financial Data Comparison

The following is a comparison of the first half of 2025 data

|

Indicator |

Amperex (301413.SZ) |

Minxin Co., Ltd. (688286.SH) |

|

Operating Revenue |

554 million yuan (YoY+34.44%) |

304 million yuan (YoY+47.82%) |

|

Gross Margin |

27.79% (YoY-3.04 percentage points) |

31.64% (YoY+10.21 percentage points) |

|

Net Profit |

42 million yuan (YoY+19.60%) |

25 million yuan (turning profit from loss YoY) |

Amperex’s gross margin decline is mainly due toprice pressure (intensified market competition) and accounting adjustments (some quality assurance costs included in expenses); while Minxin Co., Ltd.’s gross margin increase is due to an increase in the proportion of high-margin products (such as pressure sensors and inertial sensors) and cost reduction and efficiency improvement (release of production capacity from fundraising projects).

③ Comparison of IoT and Robotics Field Layouts

Amperex focuses on automotive electronics in the IoT field, with its temperature-pressure integrated sensor already in mass supply to BYD, Tesla (North America), and other automakers for thermal management systems; its oxygen sensors have entered the pre-installation market of leading domestic OEMs, benefiting from the implementation of the National VI emission standards. In addition, the company’s pressure sensors have been applied in industrial IoT (such as equipment pressure monitoring).

Minxin Co., Ltd. focuses on consumer electronics and AIoT in the IoT field, with its MEMS acoustic sensors (high signal-to-noise ratio, low power consumption) already entering the supply chains of multiple smartphone brands, adapting to the far-field pickup needs of AI smartphones; its pressure sensors (waterproof barometers) have been promoted toAI glasses, smartwatches, and other devices for environmental perception (such as altitude and pressure).

Amperex has core products in the robotics field, including torque sensors (based on MEMS silicon strain gauges + glass micro-melting technology), developed in collaboration with Tianji Intelligent, applied in collaborative robots and humanoid robot joint modules to achieve real-time torque feedback and safety control; its unidirectional force sensors have also been sampled to multiple robotics customers for precision assembly of industrial robotic arms.

Minxin Co., Ltd.: The core products in the robotics field are MEMS IMUs (Inertial Measurement Units) and three-dimensional force sensors, with the IMU currently being developed for automotive and robotics applications (such as balance control and navigation); the three-dimensional force sensor has been initiated for projects, used for fingertip sensing and environmental interaction in humanoid robots. In addition, the company’s MEMS acoustic sensors can be used for voice interaction in robots (such as voice command recognition).

5. Valuation Analysis

As of September 17, 2025, Minxin Co., Ltd. has a market value of 5.7 billion yuan, with a stock price of 101.46 yuan/share. The company’s historical valuation is as follows:

Since the company has just turned a profit, it is difficult to usePE for valuation.

Since there are no listed companies overseas that focus solely onMEMS sensors, such as the American MEMS giant InvenSense, which was acquired by Japan’s TDK in 2017; the main MEMS company in Europe is Bosch Automotive; and Japan has Murata Manufacturing (Murata) and ROHM, but sensors are just one of their departments.

The A-share PE is based on the analog chip sector, excluding companies with negative PE, and the rolling PE situation is as follows:

|

Stock Abbreviation |

PE (TTM) |

Stock Abbreviation |

PE (TTM) |

|

Shengbang Co., Ltd. |

99.45 |

Jingfeng Mingyuan |

673.57 |

|

Shanghai Beiling |

66.55 |

Juqian Technology |

50.43 |

|

Dian Ke Chip |

432.91 |

Nanchip Technology |

91.13 |

|

Broadcom Integration |

196.01 |

Chipeng Micro |

56.80 |

|

Huiding Technology |

51.60 |

Chip Dynamics |

98.88 |

|

Shengjing Micro |

148.63 |

Li Xinwei |

89.07 |

|

Yingjixin |

65.38 |

Aiwe Electronics |

63.93 |

|

Zhenlei Technology |

206.99 |

Saiwei Microelectronics |

76.44 |

|

Minxin Co., Ltd. |

226.30 |

|

|

|

Arithmetic Average |

158.47 |

||

|

Median |

91.13 |

The median PE and PS are91.13 times.

According to Wind’s consensus earnings forecast, the revenues for 2025 and 2026 are expected to be net profits of50 million and100 million, respectively. Based on the 2026 net profit target of100 million, the estimated market value is about9 billion yuan, corresponding to a stock price of about161 yuan.

Of course, the above estimates are quite arbitrary, just to find a reference, but I always feel that Minxin’s profits will explode faster; however, there has not been in-depth research on this, and I hope that experts can provide additional insights.

6. Core Highlights for the Company’s Future

The growth of Minxin Co., Ltd. mainly comes from“scaling existing business” and“landing emerging businesses”, covering three high-growth tracks: consumer electronics, automotive electronics, and AI/robotics.

1. Consumer Electronics: Scaling Up Pressure Sensors and Inertial Sensors

Consumer electronics are Minxin’s traditional base, but the rapid growth of pressure sensors and inertial sensors will become the core driver of short-term performance.

2. Emerging Scenarios: AI glasses and robotics sensors have long-term growth potential

Minxin’s long-term growth comes from the sensor layout in emerging scenarios such as AI glasses and humanoid robots, with high growth potential in these fields driving the company’s valuation increase.

AI Glasses: Exclusive Supplier of Microphones, Benefiting from the Explosion of AI Hardware

Minxin is theexclusive supplier of microphones for Rokid Glasses (the leading domestic AI glasses brand), with its high signal-to-noise ratio, low power MEMS microphones providing critical technical support for Rokid Glasses’“auditory center”. As AI glasses become more popular (Canalys predicts that by 2028, global AI smartphone shipments will account for54%, and AI PC shipments will reach205 million units), Minxin’s AI sensors (such as bone conduction microphones and ultrasonic ToF sensors) will see continued growth in demand.

Humanoid Robots: Comprehensive Sensor Layout, Seizing Industry Opportunities

Minxin has initiated R&D projects for six-dimensional force sensors, robot IMUs, and glove-type pressure and temperature sensors, covering core needs for robot motion control (such as posture stability and gait coordination) and environmental perception (such as object recognition and grasping). With the explosion of the humanoid robot market (GGII predicts that the global market size will exceed20 billion dollars by 2030), Minxin’s robotics sensors are expected to penetrate the supply chains of leading customers like Tesla’sOptimus and UBTECH, becoming a core barrier for long-term growth. (This is purely speculation, as no relationship between Minxin and Tesla has been found.)

3.Technology and Platformization: Fully Controllable Supply Chain, Building Competitive Barriers

Minxin’s fully controllable supply chain (chip design, wafer manufacturing, packaging, and testing) is its core competitive advantage.

7. Conclusion

As one of the leading domestic consumer-gradeMEMS companies, the company has already developed the capability for diversified products, and its future development is expected to be more stable; at the same time, the downstream application scenarios of MEMS continue to expand, and with the development of AI hardware and the robotics industry, Minxin is expected to continue to benefit.

However, attention should be paid to whether the departure of core technical personnel affects R&D monitor the reduction of major shareholders, and keep an eye on the R&D and marketization progress of new products.

In terms of themes, AI glasses + robotics. The most direct should still be theRokid glasses, and attention should be paid to their sales data.

The company has seen pressure orders whenever there is a recent surge; could it be that the management has unfinished business?

Welcome to discuss and correct!

Note: The above is only a record of personal investment thoughts and does not constitute investment advice.Welcome to like and follow this account, and may it hit the limit tomorrow!

Please open in the WeChat client