With the accelerated transformation of global advanced manufacturing, ceramic 3D printing is gradually moving from scientific research exploration to industrial application. According to the latest market research, 2025 will be a critical turning point for ceramic additive manufacturing (AM): the technology is maturing, applications are gradually being implemented, and the combination of capital and policy drivers is leading to profound changes in the industry landscape.

With the accelerated transformation of global advanced manufacturing, ceramic 3D printing is gradually moving from scientific research exploration to industrial application. According to the latest market research, 2025 will be a critical turning point for ceramic additive manufacturing (AM): the technology is maturing, applications are gradually being implemented, and the combination of capital and policy drivers is leading to profound changes in the industry landscape.

1. Market Size and Growth Drivers

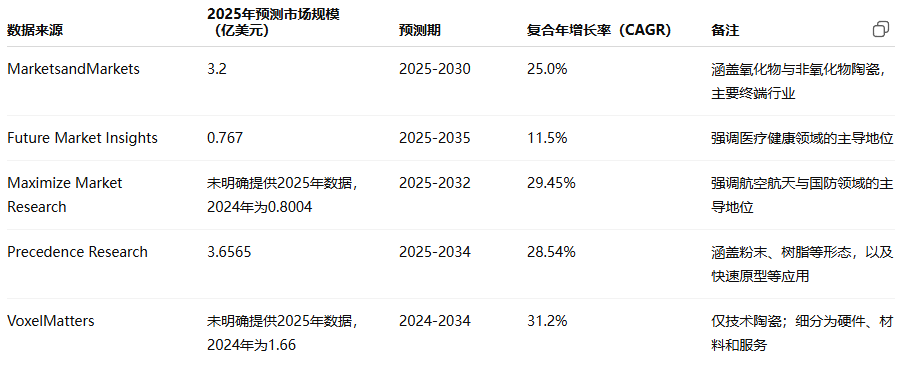

The ceramic 3D printing market is still in the early stages of rapid growth. There are significant differences in the forecast data from different organizations: the lower limit of the market size for 2025 is estimated at $76.7 million, while the upper limit exceeds $360 million. However, regardless of the numerical differences, research institutions generally believe that the compound annual growth rate will be between 11% and 30%. In other words, in the coming years, ceramic 3D printing will remain one of the fastest-growing segments in the additive manufacturing industry.

The fundamental reason for the differences in forecasts lies in the varying statistical criteria—some reports only cover technical ceramic applications, while others include equipment, materials, and services. However, the differences themselves signal an important message: the industry landscape has not yet solidified and is still in a stage of “self-definition”. This means that new entrants still have the opportunity to seize a place before standards and leadership structures are fully formed.

It is noteworthy that research institutions like SmarTech predict that after 2025, ceramic 3D printing will experience exponential growth. Once this critical point is crossed, the market size may expand several times within a few years. For companies looking to establish a presence, now is a key window for strategic investment.

Table 1: Comparison of Global Ceramic 3D Printing Market Size and CAGR Forecasts (Note: Different reports may have varying statistical criteria and base years; this table aims to show the general consensus on industry growth rather than precise comparisons of absolute values)

2. Regional Landscape: Europe Leads, Asia-Pacific Rises

Currently, Europe is in a leading position in the ceramic 3D printing market, primarily due to the concentration of globally renowned equipment manufacturers such as Lithoz, Admatec, and the strong demand from the aerospace and defense industries provides a stable market foundation. North America follows closely, with medical, automotive, and tool manufacturing being the main application directions.

In contrast, the Asia-Pacific region is considered the fastest-growing market in the future, especially China. Predictions indicate that China’s annual compound growth rate is expected to exceed 15%. The driving forces come from three aspects:

-

A complete manufacturing system;

-

Continuous government investment in “Industry 4.0” and smart manufacturing;

-

A rapid pace of technology adoption.

For new entrants, the Asia-Pacific region is both a potential market and the area with the most intense competitive pressure and innovation activity.

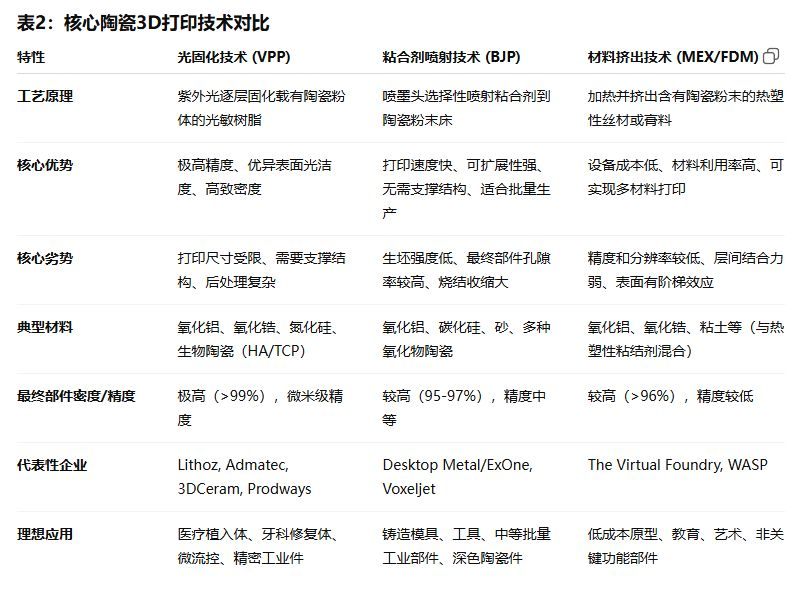

3.Three Major Technological Paths

Ceramic 3D printing technology routes are diverse, but currently, three trends are the most representative:

1. Photopolymerization (VPP): A Synonym for High Precision

Photopolymerization is known for its excellent precision and smooth surface quality, making it particularly suitable for high-value fields such as dental, medical implants, and precision electronics. By 2024, its equipment revenue is expected to account for nearly 80% of the market.

-

Limitations: Limited forming size, complex post-processing

2. Binder Jetting (BJP): The Path to Mass Production

The advantages of BJP technology are its fast speed and strong scalability, making it suitable for mass production without the need for support structures, enabling spatial stacking printing. However, challenges include the fragility of the green body and significant shrinkage during sintering.

-

Applications: Casting molds, tools, and dark ceramic parts such as silicon carbide

3. Multi-material and Composite Materials: The Frontier of Functional Integration

Through multi-material printing and ceramic matrix composites (CMCs), functional gradient structures and extreme environment applications can be achieved. For example, the leading edge components of hypersonic vehicles in aerospace are being printed using CMC.

-

Limitations: High cost, low maturity

The conclusion is:there is no absolute superiority in technology selection; precision-oriented applications can choose VPP, efficiency-driven applications are more suitable for BJP, while those pursuing differentiation can explore multi-material printing.

Table 2: Comparison of Core Ceramic 3D Printing Technologies

4.Two Core Application Areas

1. Aerospace: A Performance-Driven High-End Market

The value of ceramic 3D printing in the aerospace field lies not in cost reduction but in breaking performance bottlenecks.

-

Ceramic Cores: Honeywell has reduced the production cycle from several months to 7 weeks using photopolymerization technology.

-

High-Temperature Components: Silicon nitride and CMC printed combustion chambers and turbine blades can significantly improve engine efficiency.

-

Hypersonic Applications: CMC maintains strength at extreme high temperatures, making it a key material for future strategic weapon platforms.

This field has extremely high barriers, requiring certifications from FAA, EASA, etc., and the capital and talent requirements are also very stringent. However, once entered, the competitive moat is very solid.

2. Medical Dentistry: A Revolution in Scalable Customization

Healthcare is another major pillar of ceramic 3D printing, with market shares close to those of aerospace.

-

Personalized Implants: Printing orthopedic and cranial repair implants based on patient imaging data improves surgical success rates.

-

Dental Restorations: SprintRay achieves “same-day restorations,” greatly enhancing patient experience.

-

Surgical Guides and Tools: Assisting precise surgical operations.

The medical market also has strict regulatory requirements (such as FDA 510(k) approval), but for manufacturers with quality management and material certification experience, this presents a rare competitive advantage.

5.Conclusion

Ceramic 3D printing is at a critical juncture, transitioning from “exploration” to “application.” It is not a replacement for traditional manufacturing but a high-end manufacturing solution. For traditional ceramic manufacturers, the challenge lies in how to leverage additive manufacturing to expand capability boundaries and create “certified high-reliability complex ceramic components.” The market turning point in 2025 is approaching, and those who can first overcome the barriers of post-processing and certification are likely to occupy a core position in the industry landscape over the next decade.

Click “Read Original” to enter the official website

Click “Read Original” to enter the official website