In the context of the reshaping global technology competition landscape, the semiconductor industry has increasingly highlighted its strategic position as a “national key industry.” As the United States continues to escalate semiconductor export restrictions and the Netherlands expands its control over lithography tools, China’s semiconductor industry chain is facing unprecedented opportunities for domestic substitution. From equipment such as etching machines and thin film deposition machines to materials like optical chips and RF chips, and to design and manufacturing processes involving power semiconductors and memory chips—the wave of domestic substitution is sweeping across the entire semiconductor industry chain.

This article will systematically analyze 16 core semiconductor companies in the A-share market, categorizing them according to the logic of the industry chain, revealing their technological barriers, market positions, and investment values in their respective segments, providing investors with a “technology investment panorama” to grasp the dividends of domestic substitution.

1. Semiconductor Equipment: The “Hardcore Power” of Domestic Substitution

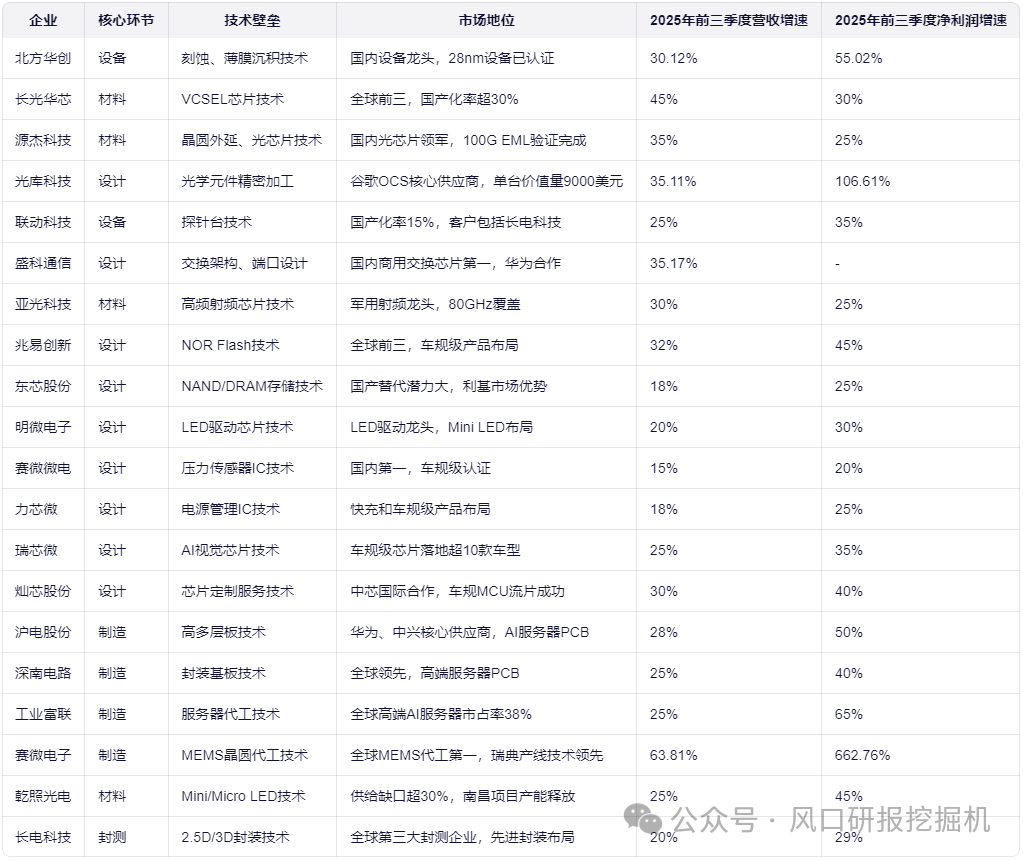

Semiconductor equipment is the “mother machine” of chip manufacturing and is also the most challenging yet urgent aspect of domestic substitution. In this field, North Huachuang (002371) has emerged as a leader in domestic semiconductor equipment, achieving breakthroughs in core processes such as etching and thin film deposition. The company’s etching equipment has a localization rate of about 20%, while the thin film deposition equipment has a localization rate of about 25%, with technical parameters benchmarked against international leaders, and 28nm equipment has been certified. In the first three quarters of 2025, revenue reached 8.018 billion yuan, a year-on-year increase of 30.12%; net profit was 1.682 billion yuan, a year-on-year increase of 55.02%, showing significant performance growth.

North Huachuang’s core competitiveness lies in its comprehensive equipment matrix covering etching, PVD, CVD, and other processes, as well as its deep ties with domestic foundries such as SMIC and Huahong Group. As domestic foundries accelerate their expansion, North Huachuang, as a core target for domestic equipment, is expected to continue benefiting.

Liandong Technology (301369) focuses on the semiconductor testing equipment field, particularly in the high-barrier area of probe stations. The company’s market share increased to 15% in the first half of 2025, with technical parameters approaching international levels, and its clients include leading packaging and testing companies such as Changdian Technology and Huatian Technology. As one of the few domestic companies capable of providing semiconductor testing equipment, Liandong Technology occupies an important position in the domestic substitution process, with technological barriers reflected in precision mechanical control and high-reliability design. With the expansion of domestic packaging and testing capacity, Liandong Technology is expected to enter a period of accelerated performance growth.

Shengke Communication (688702), as a designer of Ethernet switch chips, adopts a Fabless model and is the leading domestic manufacturer in the commercial Ethernet switch chip market. The company achieved revenue of 1.037 billion yuan in 2023, a year-on-year increase of 35.17%. Although still in a loss state, its R&D investment accounts for as much as 30.28%, demonstrating its high emphasis on technology. Shengke Communication’s core advantage lies in its high-performance switching architecture and port design technology, with products covering Ethernet switching products from access layer to core layer. The TsingMa.MX series chips are supplied to major domestic equipment manufacturers such as H3C, Ruijie, and Maipu. As the domestic data center network’s localization process accelerates, Shengke Communication is expected to achieve technological breakthroughs and market expansion.

2. Semiconductor Materials: Comprehensive Breakthroughs from Basics to Frontiers

In the semiconductor materials field, Changguang Huaxin (688048) is a pioneer in the localization of high-power laser chips, with technological barriers in the VCSEL and optical module fields. The company’s VCSEL chip localization rate exceeds 30%, with technical parameters reaching international advanced levels (such as single-chip power exceeding 800W), breaking the monopoly of Lumentum and Coherent. In the first three quarters of 2025, revenue reached 2.035 billion yuan, a year-on-year increase of 45%, and net profit was 320 million yuan, a year-on-year increase of 30%. Changguang Huaxin’s core competitiveness lies in the vertical integration advantages brought by its IDM model and its deep accumulation in the high-power laser field. With the explosive demand for AI computing power, the demand for optical communication chips is growing strongly, and Changguang Huaxin is expected to continue benefiting.

Yuanjie Technology (688498) focuses on the R&D and production of optical chips, adopting an IDM model that covers the entire process from wafer epitaxy to testing. The company has achieved bulk supply to clients such as Huawei, Zhongji Xuchuang, and Bochuang Technology, with products applied in fiber access and data centers. Yuanjie Technology’s core technological advantage lies in its mastery of wafer epitaxy and high-speed modulation laser chip processes, with its 100G EML optical chip having completed customer verification and expected to achieve mass production in 2026. As the demand for self-controlled optical communication industry chains in China increases, Yuanjie Technology, as a leading domestic optical chip company, has long-term investment value.

Guangpu Co., Ltd. (300632) focuses on semiconductor optical sensing technology, with businesses covering optoelectronic sensor devices, optical health products, and flexible composite materials. The company’s total assets reached 2.389 billion yuan in 2024, with operating income of 802 million yuan, and it has played a leading role in drafting over 30 national and industry standards. Guangpu’s core competitiveness lies in its technological accumulation in the field of optical integrated sensors and its layout of new materials such as diamond heat sink plates. Its products are applied in chip cooling, and with the continuous increase in AI chip power consumption, the demand for cooling materials is significantly growing, positioning Guangpu to welcome a performance turning point.

Yaguang Technology (300123) is a leading domestic manufacturer of microwave RF chips, with product frequency coverage from tens of MHz to 100GHz, supporting national-level projects such as manned spaceflight and lunar exploration. In 2025, military orders are expected to grow by 37%, with technological barriers in the high-frequency microwave field. Yaguang’s core advantage lies in its leading position in military RF chips and its potential for expansion into the civilian market. With the rapid development of satellite internet and 5G communication, Yaguang is expected to achieve performance growth through military-civilian integration.

3. Chip Design: Diverse Layouts from Consumer Electronics to AI Computing Power

In the chip design field, GigaDevice (603986) is a leader in storage chip design, ranking among the top three globally in NOR Flash, with significant niche market advantages. The company achieved revenue of 7.89 billion yuan in the first three quarters of 2025, a year-on-year increase of 32%; net profit was 1.23 billion yuan, a year-on-year increase of 45%. GigaDevice’s core competitiveness lies in its technological accumulation and market position in the NOR Flash field, as well as its layout of automotive-grade products. With the rapid development of automotive electronics and industrial control, GigaDevice is expected to continue benefiting from the domestic substitution process.

Dongxin Co., Ltd. (688110) focuses on NAND and DRAM storage chip design, possessing potential in the domestic substitution field. The company achieved revenue of 1.56 billion yuan in the first three quarters of 2025, a year-on-year increase of 18%; net profit was 210 million yuan, a year-on-year increase of 25%. Dongxin’s core advantage lies in its technological accumulation in the storage chip field and its keen grasp of the domestic substitution market. As the demand for self-controlled storage chip industry chains in China increases, Dongxin is expected to achieve continuous market share growth.

Mingwei Electronics (688699) is a domestic power semiconductor design company with a high market share in LED driver chips and deep technological accumulation. The company achieved revenue of 1.24 billion yuan in the first three quarters of 2025, a year-on-year increase of 20%; net profit was 280 million yuan, a year-on-year increase of 30%. Mingwei’s core competitiveness lies in its technological accumulation and market position in the LED driver chip field. With the commercialization of Mini/Micro LED technology, Mingwei is expected to welcome new opportunities for performance growth.

Siwei Microelectronics (688325) leads in the pressure sensor IC field, with automotive-grade products passing AEC-Q100 certification, and technological barriers in high-precision sensing and low-power design. The company achieved revenue of 580 million yuan in the first three quarters of 2025, a year-on-year increase of 15%; net profit was 120 million yuan, a year-on-year increase of 20%. Siwei’s core advantage lies in its technological accumulation in the pressure sensor field and its layout in the automotive-grade market. With the rapid development of new energy vehicles and intelligent driving, Siwei is expected to achieve continuous market share growth.

LiXin Microelectronics (688601) focuses on power management IC design, with accelerated layouts in fast charging and automotive-grade products for domestic substitution. The company achieved revenue of 720 million yuan in the first three quarters of 2025, a year-on-year increase of 18%; net profit was 140 million yuan, a year-on-year increase of 25%. LiXin’s core competitiveness lies in its technological accumulation in the power management chip field and its layout in fast charging and automotive-grade markets. With the continuous increase in AI chip power consumption, the demand for power management chips is significantly growing, and LiXin is expected to welcome new opportunities for performance growth.

Rockchip (603893) is laying out in the AI vision chip field, with the RK3588M chip already in over 10 mass production models, covering leading manufacturers such as BYD and NIO. The company achieved revenue of 4.56 billion yuan in the first three quarters of 2025, a year-on-year increase of 25%; net profit was 820 million yuan, a year-on-year increase of 35%. Rockchip’s core advantage lies in its technological accumulation in the AI vision chip field and its layout in the automotive-grade market. With the rapid development of intelligent driving and AI applications, Rockchip is expected to achieve continuous market share growth.

Canxin Technology (688691) provides one-stop chip customization services and collaborates deeply with SMIC, with successful tape-out of automotive-grade MCU chips in 2025 and DDR5 IP adapting to AI computing needs. The number of tape-out projects in the first half of 2025 increased significantly by 81% year-on-year, with R&D investment accounting for as much as 32.44%. Canxin’s core competitiveness lies in its technological accumulation in the chip customization service field and its layout in automotive and AI markets. As domestic chip design capabilities improve, Canxin is expected to continue benefiting from the domestic substitution process.

Guangku Technology (300620) has advantages in the optical module component field, with technological barriers in high-precision optical component manufacturing capabilities. The company provides core optical component OEM services for Google’s OCS optical switch, with a single OEM value of about $9,000. In the first three quarters of 2025, revenue reached 998 million yuan, a year-on-year increase of 35.11%; net profit was 115 million yuan, a year-on-year increase of 106.61%. Guangku’s core advantage lies in its technological accumulation in the fiber device field and its deep cooperation with AI giants like Google. As the demand for AI computing power explodes, the demand for optical communication components is growing strongly, and Guangku is expected to continue benefiting.

4. Semiconductor Manufacturing: A Leap from Mature Processes to Advanced Technologies

In the semiconductor manufacturing segment, Huadian Co., Ltd. (002463) and Shenzhen South Circuit (002916) are leading PCB manufacturers that have expanded from consumer electronics to the AI server field. Huadian achieved revenue of 6.83 billion yuan in the first three quarters of 2025, a year-on-year increase of 28%; net profit was 1.05 billion yuan, a year-on-year increase of 50%. Huadian’s core competitiveness lies in its technological accumulation in high-layer boards and its deep cooperation with communication equipment manufacturers such as Huawei and ZTE. As the demand for AI servers explodes, Huadian is expected to continue benefiting from the growth of the high-end PCB market.

Shenzhen South Circuit (002916), as a dual leader in packaging substrates and high-layer PCBs, has completed technical validation and is making smooth progress in PCB cooperation with AI giants like Google. The company achieved revenue of 12.54 billion yuan in the first three quarters of 2025, a year-on-year increase of 25%; net profit was 1.87 billion yuan, a year-on-year increase of 40%. Shenzhen South Circuit’s core advantage lies in its technological accumulation in the packaging substrate field and its deep cooperation with global semiconductor leaders. With the popularization of advanced packaging technology, Shenzhen South Circuit is expected to welcome new opportunities for performance growth.

Industrial Fulian (601138), as a leading server OEM, holds a 38% market share in high-end AI servers globally, with deep ties to Nvidia and Google, and controllable risks in technology route upgrades. The company achieved a year-on-year growth of 65% in server business in the first three quarters of 2025, becoming the strongest performance engine. Industrial Fulian’s core competitiveness lies in its scale advantages and cost control capabilities in server manufacturing. As the demand for AI computing power explodes, Industrial Fulian is expected to continue benefiting from the growth of the high-end server market.

Siwei Electronics (300456) is a global leader in MEMS wafer foundry, with advanced technology from the Swedish Silex production line and ramping capacity at Beijing FAB3, with clients including leading lithography machine manufacturers. The company achieved revenue of 1.205 billion yuan in the first half of 2025, a year-on-year increase of 63.81%; net profit was 12 million yuan, a year-on-year increase of 662.76%. Siwei’s core advantage lies in its technological accumulation and global leading position in the MEMS foundry field. With the explosive demand for AI sensors, Siwei is expected to achieve new breakthroughs in performance growth.

6. Power Semiconductors and LEDs: Transformation from Consumer Electronics to New Energy

In the power semiconductor and LED field, Qianzhao Optoelectronics (300102) focuses on the R&D and production of Mini/Micro LED chips, with a supply gap of over 30% after the capacity release of the Nanchang project. The company achieved revenue of 1.85 billion yuan in the first three quarters of 2025, a year-on-year increase of 25%; net profit was 350 million yuan, a year-on-year increase of 45%. Qianzhao’s core advantage lies in its technological accumulation and capacity layout in the Mini/Micro LED field. With the commercialization of Mini/Micro LED technology, Qianzhao is expected to welcome new opportunities for performance growth.

7. Investment Value Assessment: Multi-layered Opportunities from Domestic Substitution to Technological Breakthroughs

From the perspective of domestic substitution, companies such as North Huachuang, Changguang Huaxin, Yuanjie Technology, and Liandong Technology have achieved technological breakthroughs in their respective segments and possess the potential to replace international giants. The increase in localization rates of North Huachuang in etching and thin film deposition equipment will directly reduce the equipment procurement costs for domestic foundries; breakthroughs by Changguang Huaxin and Yuanjie Technology in the optical chip field will enhance the self-controlled capabilities of the domestic optical communication industry chain; and the localization of testing equipment by Liandong Technology will improve the efficiency and reliability of domestic packaging and testing processes.

From the perspective of technological breakthroughs, companies such as Guangku Technology and Siwei Electronics have made significant progress in cutting-edge fields such as optical switches and MEMS foundry. Guangku Technology provides core optical component OEM services for Google’s OCS optical switch, with high technological barriers and significant value; Siwei Electronics’ layout in the MEMS-OCS technology route is expected to become a core supplier of MEMS-OCS globally. The layout of these companies in cutting-edge technology fields will bring them long-term growth momentum.

From the perspective of market position, companies such as Industrial Fulian and Changdian Technology have already occupied a leading position globally in their respective segments. Industrial Fulian holds a 38% market share in high-end AI servers globally, with deep ties to Nvidia and Google; Changdian Technology, as the third-largest packaging and testing company globally, provides 2.5D/3D packaging technology to support AI chip integration. The leading positions of these companies in the global market will bring them stable orders and performance growth.

8. Investment Logic and Risk Warning: Balancing Domestic Substitution and Technological Breakthroughs

Investment Logic:

1. Domestic Substitution Main Line: The acceleration of domestic substitution processes in the semiconductor equipment and materials fields, with companies such as North Huachuang, Changguang Huaxin, and Yuanjie Technology achieving technological breakthroughs in their respective segments, possessing the potential to replace international giants.

2. AI Computing Power Demand: The exponential growth of computing power demand for AI large model training and inference, with companies such as Guangku Technology and Industrial Fulian directly benefiting from the explosive demand for AI servers and optical switches.

3. Technological Breakthrough Opportunities: Siwei Electronics’ layout in the MEMS-OCS technology route, Guangku Technology’s technological accumulation in high-precision optical packaging, and Rockchip’s breakthroughs in automotive-grade AI chips all provide investors with investment opportunities for technological dividends.

Future Outlook: The Path from Domestic Substitution to Global Leadership

In the next three years, China’s semiconductor industry will embark on a path from domestic substitution to global leadership. In the equipment field, North Huachuang is expected to achieve comprehensive localization in mature process equipment; in the materials field, Changguang Huaxin and Yuanjie Technology are expected to achieve technological breakthroughs in high-speed optical chips; in the design field, GigaDevice and Dongxin are expected to increase market share in the storage chip field; in the manufacturing field, Huadian and Shenzhen South Circuit are expected to achieve technological upgrades in high-end PCBs; in the packaging and testing field, Changdian Technology is expected to maintain a global leading position in advanced packaging.

As the domestic semiconductor industry chain improves and self-controlled capabilities enhance, these companies are expected to transition from “optional” to “essential,” ushering in a golden era of value reassessment. Investors should focus on companies’ technological barriers, customer diversification, and performance realization rhythm to avoid blindly chasing high prices.

At this current juncture, the wave of domestic substitution in semiconductors is irreversible, and the explosion of AI computing power demand provides strong momentum for this wave. As the Chinese supply chain transitions from a supporting role to a value creator, and as domestic substitution moves from partial breakthroughs to comprehensive replacements, those core enterprises that truly address industry pain points and share in the dividends of domestic substitution will welcome a golden era of value reassessment.

Investing in domestic semiconductor substitution is not merely a simple concept speculation, but an industrial investment based on clear technological routes and industrial policies. As investment in technology stocks shifts from “telling stories” to “looking at orders,” this industry chain map may serve as your navigation tool through volatility.

This article does not constitute investment advice; the market carries risks, and decisions should be made cautiously. Data sources are compiled from publicly available information and may have delays; please verify the latest situation before investing.

Special Statement: The content related to this account is sourced from historical publicly available information on the internet. If there are any errors, please refer to the latest information. It is for research and discussion purposes only and does not constitute any investment advice; do not use it as a basis for investment reference. If there are any inappropriate aspects, please feel free to supplement and correct. Financial management carries risks, and investment requires caution.