01

Overall Market

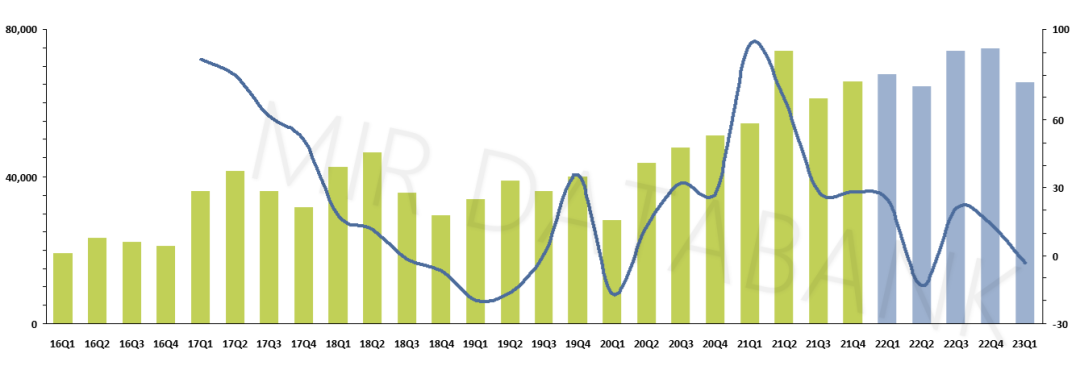

First Decline in Q1 Since 2020

In the first quarter of 2023, industrial robot sales decreased by approximately 3.3% year-on-year. Specifically, the sales decline was significant in January and February, with a narrowing decline in March. It is currently unclear when the market will achieve positive growth. This marks the first decline in the industrial robot market in Q1 since 2020.

We believe that the overall market decline in Q1 2023 is significantly affected by weak downstream demand, a situation that can be traced back to Q4 2022. At that time, although the quarterly overall market shipment data continued to show growth, the overall order growth rate began to narrow, indicating a rapid spread of the issue.

Quarterly Market Size of Industrial Robots from 2016 to 2023 (Shipments/Units)

(Data Source: MIR DATABANK)

A notable comparison is that in Q1 2022, the industrial robot market grew by as much as 20.5%. At that time, our assessment was that the supply chain began to tighten in the second half of 2021, leading to significant delays in delivery times for some robot manufacturers, with orders pushed to Q1 2022. This resulted in many robot manufacturers having orders in Q1 that exceeded those of the same period in 2021, and the overall downstream demand for industrial robots was relatively strong and showed high growth at that time. However, the situation has changed, and despite fulfilling some of the backlog from 2022 in Q1 2023, it is still difficult to compensate for the shortfall caused by shrinking market demand.

02

Short-term Decline in Demand for New Energy Vehicles, Lithium Batteries, and Medical Industries

Recovery in Electronics and Metal Products Industries Below Expectations

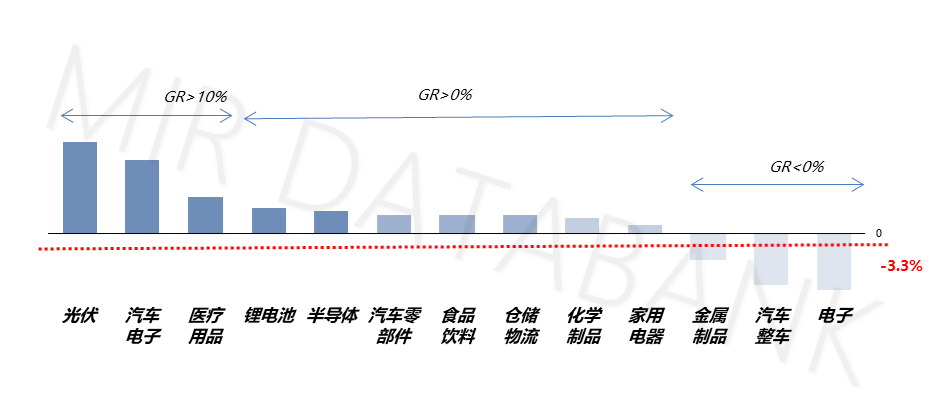

Looking specifically at downstream application industries, the main driving forces for industrial robots over the past two years, such as new energy vehicles, power batteries, and medical applications, have also seen a relative slowdown in demand growth in Q1 2023 (the average growth in downstream industries in Q1 2022 was around 30%). The general industrial *long-tail market shows signs of recovery, but it will take time to activate the market.

*General Industry: Refers to food processing, beverage manufacturing, wood processing, tobacco industry, leather processing, furniture manufacturing, printing industry, petroleum processing, metal smelting, mining, cement processing, etc.

Q1 2023 Industrial Robot Shipment Situation by Downstream Industry

(Data Source: MIR DATABANK)

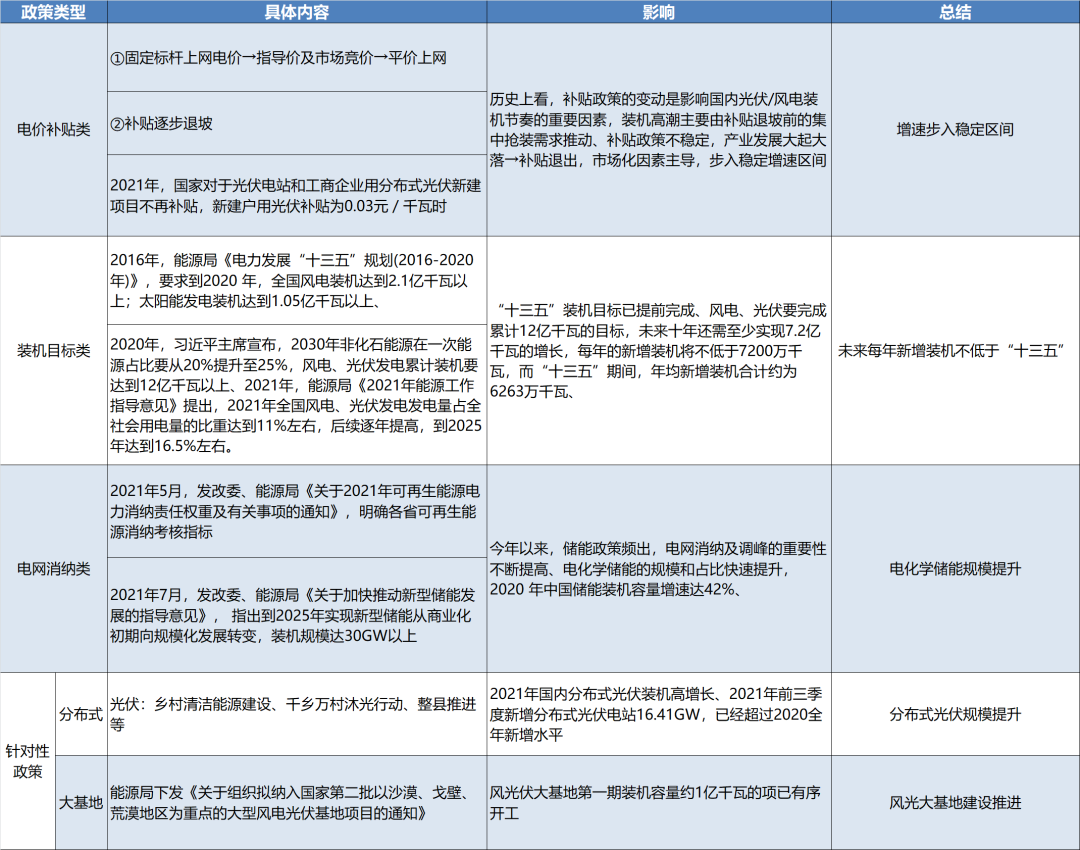

Despite most industries still being mired in difficulties, the energy storage (including lithium batteries) and photovoltaic markets continue to maintain high growth rates, mainly due to the following factors:

1. Policy Support

2. Increased Robot Penetration in Various Process Stages, such as further applications in cell synthesis, formation, and module assembly in energy storage battery manufacturing.

3. Demand Generated by New Technologies and Processes, such as EL testing (electroluminescence testing) in the photovoltaic field for loading and unloading, and applications in coating, laser transfer equipment loading and unloading, and stacking in photovoltaic module manufacturing are continuously expanding.

4. Export Growth, for example, in photovoltaics, domestic leading companies have been actively expanding into overseas markets, with Chinese companies occupying eight of the top ten global module manufacturers.

5. The Middle East is accelerating “de-dollarization,” with many countries strengthening cooperation with China in clean energy fields such as hydrogen energy, energy storage, wind power photovoltaics, and smart grids.

03

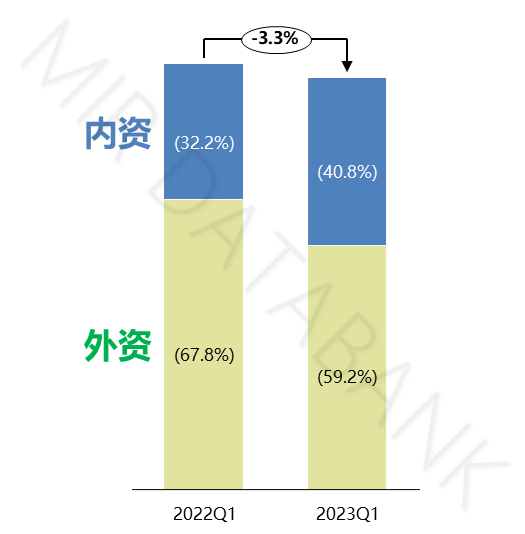

Acceleration of Domestic Substitution

Domestic Manufacturers’ Market Share Surpasses 40% for the First Time

In Q1 2023, leading domestic robot companies accelerated competition with foreign capital in fields such as lithium batteries, photovoltaics, and automotive parts, capturing market share, and began to penetrate the complete vehicle sector. The speed of domestic substitution has accelerated, resulting in a 23% increase in domestic market share, reaching 40.8%.

In contrast, foreign capital, which holds a significant share in the electronics industry, has seen order shrinkage, and demand in the new energy vehicle and lithium battery markets has further slowed, leading to a 16% decline in foreign market share, dropping to 59.2%, marking the first time foreign market share has fallen below 60%.

Comparison of Domestic and Foreign Market Shares in the Industrial Robot Market in Q1

(Data Source: MIR Rui Industrial)

The shift in market shares between domestic and foreign companies in Q1 precisely confirms that in the face of unclear market demand, price wars and internal competition will be inevitable trends. This chaotic situation is precisely what domestic manufacturers prefer, as they excel at quickly responding to customer needs in a tense environment, leveraging cost-effectiveness to penetrate specific markets. In such a rhythm, foreign companies often appear somewhat at a loss.

It is worth mentioning that the tight supply of industrial robots in 2022 led to most foreign manufacturers raising prices, and the panic buying by foreign agents resulted in significant stockpiling, which may lead to foreign manufacturers lacking a clear understanding of the actual needs of end users, hindering the healthy development of foreign brands. In contrast, domestic manufacturers, although their market share did not significantly increase in 2022, were able to sell products directly, with little stockpiling by agents. Therefore, domestic manufacturers were better positioned to understand market demand in Q1, leading to a noticeable increase in market share.

04

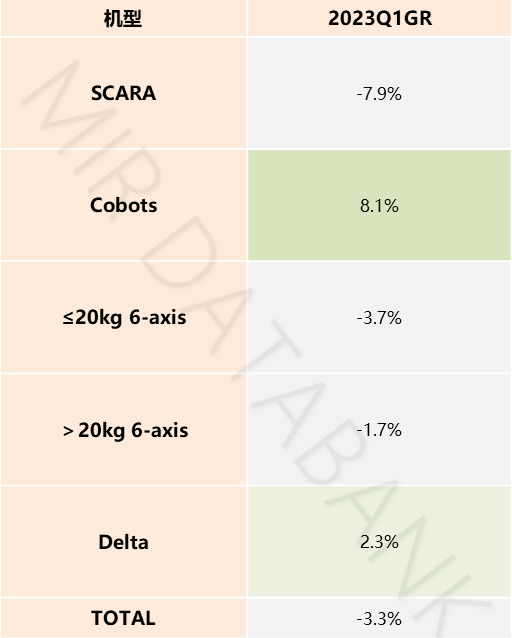

Performance of Various Models Below Expectations

From the perspective of different models, the overall weak demand in Q1 2023 has also negatively impacted the performance of various industrial robot models. Except for collaborative robots and Delta (parallel) robots, all other models experienced negative growth rates.

Comparison of Growth Rates of Various Industrial Robot Models in Q1 2023

(Data Source: MIR DATABANK)

Specifically, different models have been affected by different industries:

1. SCARA robots have seen negative growth due to weakness in the electronics industry and a slowdown in demand from lithium batteries and medical applications. Even though there is some incremental growth in markets such as photovoltaics, automotive electronics, and semiconductors, it is insufficient to provide comprehensive support. Notably, competition for general SCARA products has intensified, while demand for high-load and high-speed SCARA products remains relatively strong.

2. Although Cobots (collaborative robots) have a positive growth rate, their downstream industrial sectors such as metal products, electronics, and semiconductors are experiencing demand shrinkage. Non-industrial sectors such as catering, new retail, and health therapy are also significantly affected by reduced consumption, similar to SCARA robots, with a trend towards high-load collaborative robots.

Currently, in the collaborative robot field, domestic brands are further reducing prices, and leading manufacturers are approaching the countdown to listing. The influx of entrants into the commercial service sector is becoming a trend, with companies increasingly going overseas.

3. The ≤20kg 6-axis desktop models are experiencing weak market demand due to consumption fatigue and reduced investment in the electronics industry; the base-type and arc-welding ≤20kg 6-axis robots are also affected by shrinking exports, leading to demand in machining and arc-welding applications falling short of expectations.

4. For >20kg 6-axis robots, the number of domestic entrants continues to increase. Although demand in related fields such as new energy vehicles and power batteries is slowing, applications in energy storage and general industries such as liquor, glass, and food and beverage are continuously expanding.

5. The price of Delta (parallel) robots further decreased in Q1 2023, and some parallel manufacturers are crossing over into the SCARA market.

From the perspective of downstream industry demand, Delta (parallel) robots have seen some recovery in demand in the food and beverage and daily chemical sectors, with emerging markets such as photovoltaics, semiconductors, and lithium batteries accelerating penetration, although the current scale remains limited.

04

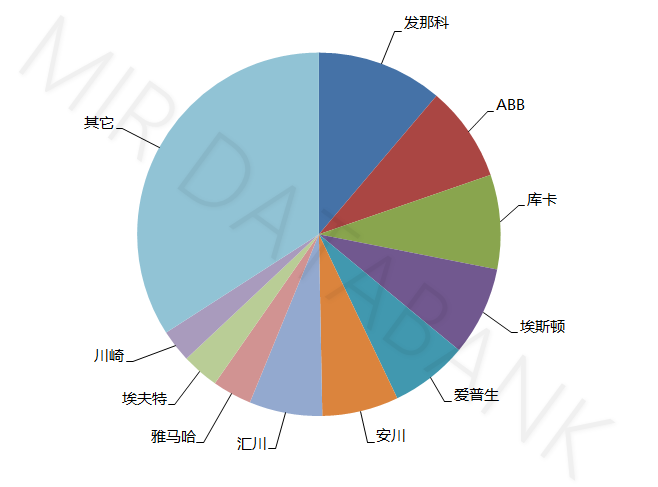

Market Landscape: Three Domestic Manufacturers Enter TOP 10 for the First Time

In Q1 2023, more than half of industrial robot companies experienced a year-on-year decline in sales, leading to a reshaping of the market landscape and accelerating industry reshuffling. For the first time, three domestic manufacturers have entered the TOP 10, namely Estun, Inovance, and Efort, with Estun (ESTUN) making its debut in the TOP 5.

Q1 2023 Pie Chart of China’s Industrial Robot Market Share

(Information Source: MIR DATABANK)

Through data comparison, we observe that a few leading domestic manufacturers currently have relatively optimistic orders, mainly from the photovoltaic, lithium battery, and other new energy-related industries. Orders from leading foreign manufacturers and remaining domestic manufacturers have significantly contracted.

Summary and Forecast

When summarizing the industrial robot market in 2022, some said it was the most challenging period in the past three years. However, this is not the case.

2023 marks the true beginning of challenges for the Chinese industrial robot market. This is because in 2022, the main contradictions faced by the industrial robot market came from the supply side, which were tangible, adjustable, and short-term. Starting in 2023 (specifically Q4 2022), the contradictions will gradually arise from the demand side, which are intangible, difficult to control, and may even be long-term.

MIR Rui Industrial, through observing the trajectory of the Chinese industrial robot market over the past decade, believes that the industrial robot market will enter a second adjustment period in 2023-2024, during which the Chinese industrial robot market will exhibit the following characteristics:

1. Competition for existing market share in the industrial robot sector will coexist with the positioning of segmented incremental markets;

2. The ranking battle among domestic manufacturers will intensify: in an environment of insufficient demand and strong competition, many second and third-tier domestic manufacturers will struggle to secure orders, with orders skewing towards first-tier brands;

3. End customers will place greater emphasis on product customization and improved services, while also demanding higher cost control, which will inevitably clarify the application demand logic for domestic industrial robots and force all (domestic) manufacturers to enhance their cost control capabilities, optimize resource integration, ensure self-control over key components, and build a community of interests with partners.

Despite facing fluctuations from periodic adjustments, we judge that industrial robots remain an “emerging” automation product, and growth will continue in the coming years.

In the context of sustained growth, the performance of different models, industries, and suppliers in the industrial robot market will still show structural differentiation. For example, in terms of models, SCARA and ≤20kg 6-axis robots will exit the high growth phase, while >20kg 6-axis and Cobots (collaborative robots) will enter a new growth stage.

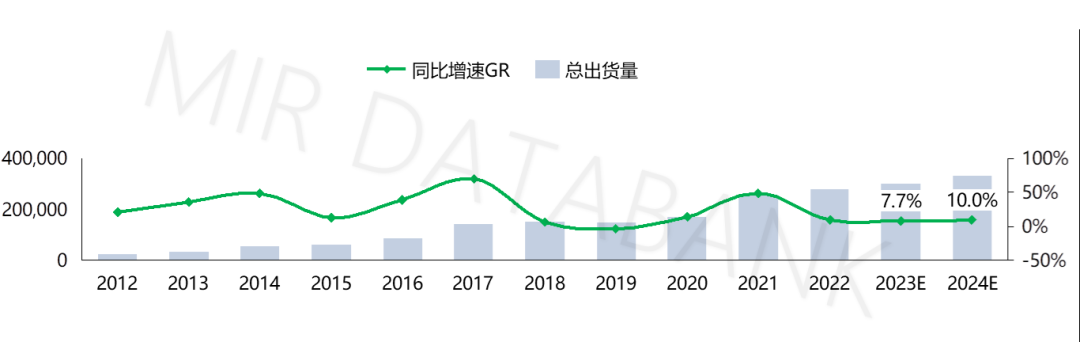

For the overall market, we believe that the market will remain under pressure in the first half of 2023, with a rebound expected in the second half, and the annual market growth rate will maintain around 7.7%.

Sales Scale of China’s Industrial Robot Market from 2010 to 2024 (Units)

(Data Source: MIR DATABANK)