The competition between China and the United States is essentially a technological struggle, with the core of this competition currently centered around semiconductors. This is why there is a comparison to Nvidia with Cambricon.The sequence of events:On September 12, local time, the U.S. Department of Commerce’s Bureau of Industry and Security (BIS) placed 23 Chinese entities on the export control “Entity List.”The Department of Commerce decided to initiate an anti-dumping investigation on imports of relevant analog chips originating from the United States starting September 13, 2025. The period for the dumping investigation is set from January 1, 2024, to December 31, 2024, while the period for the industry damage investigation is from January 1, 2022, to December 31, 2024. The products under investigation are described as: general-purpose interface chips (Commodity Interface IC Chip) and gate driver chips (Gate Driver IC Chip) using a process technology of 40nm and above.Why focus on analog chips? By 2024, China is expected to account for about 35% of the global analog chip market, making it one of the main sources of revenue for overseas analog chip manufacturers.The analog chip market is substantial, and domestically, it is gradually becoming self-sufficient.So, as semiconductors become the hottest direction in the market next week, how should we select stocks?I have a few thoughts:First, focus on core beneficial analog chip companies.I have mentioned before that in a bull market, we should pay attention to large-cap stocks, as they have more capacity to absorb market liquidity. This capacity can create a profit effect for large funds; buying 1 billion and achieving a 10% return is equivalent to doubling 100 million, but the former is much easier to achieve.

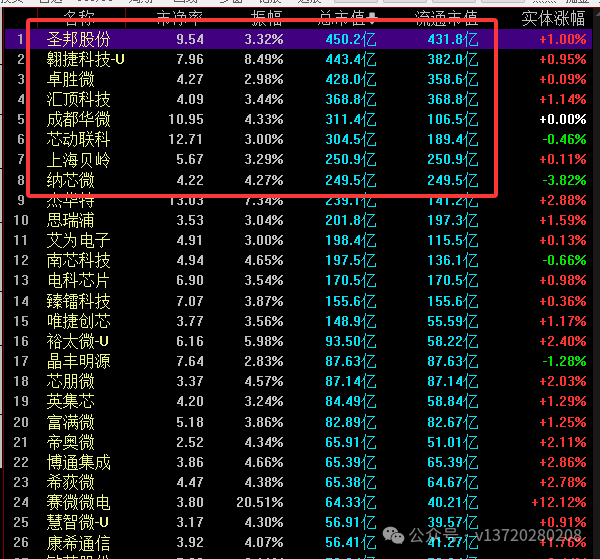

The competition between China and the United States is essentially a technological struggle, with the core of this competition currently centered around semiconductors. This is why there is a comparison to Nvidia with Cambricon.The sequence of events:On September 12, local time, the U.S. Department of Commerce’s Bureau of Industry and Security (BIS) placed 23 Chinese entities on the export control “Entity List.”The Department of Commerce decided to initiate an anti-dumping investigation on imports of relevant analog chips originating from the United States starting September 13, 2025. The period for the dumping investigation is set from January 1, 2024, to December 31, 2024, while the period for the industry damage investigation is from January 1, 2022, to December 31, 2024. The products under investigation are described as: general-purpose interface chips (Commodity Interface IC Chip) and gate driver chips (Gate Driver IC Chip) using a process technology of 40nm and above.Why focus on analog chips? By 2024, China is expected to account for about 35% of the global analog chip market, making it one of the main sources of revenue for overseas analog chip manufacturers.The analog chip market is substantial, and domestically, it is gradually becoming self-sufficient.So, as semiconductors become the hottest direction in the market next week, how should we select stocks?I have a few thoughts:First, focus on core beneficial analog chip companies.I have mentioned before that in a bull market, we should pay attention to large-cap stocks, as they have more capacity to absorb market liquidity. This capacity can create a profit effect for large funds; buying 1 billion and achieving a 10% return is equivalent to doubling 100 million, but the former is much easier to achieve. Ranked by market capitalization, the largest is Sanken Electric. If the market shows sustainability next week, it would be a good choice.

Ranked by market capitalization, the largest is Sanken Electric. If the market shows sustainability next week, it would be a good choice. Moreover, it fits the current market’s high-low switching model and belongs to the 300 index, providing considerable elasticity. However, considering the sustainability of this stock is insufficient, it is advisable to view it as a short-term opportunity and be cautious of risks.Second, invest in AI-related mainline products.

Moreover, it fits the current market’s high-low switching model and belongs to the 300 index, providing considerable elasticity. However, considering the sustainability of this stock is insufficient, it is advisable to view it as a short-term opportunity and be cautious of risks.Second, invest in AI-related mainline products. The hottest topic currently is AI. So, which AI chip has the highest correlation in the market recently? That would be GigaDevice’s storage solutions.Technically, it has not yet reached historical highs and has the potential for new highs, making it worth watching.What do the brokerage reports say?There is a significant expectation gap for customized storage: 3D stacking is not a lower-tier substitute for HBM; each has its own market strengths. The bandwidth is 5-10 times that of the existing HBM3e, making it particularly suitable for inference scenarios; the long-term value of inference cards: storage value = 10:2.5~3, with the 2028 market for computing chips estimated at 800 billion, and the customized storage market at over 200 billion. GigaDevice is the absolute leader, with almost all major manufacturers as partners, and combined with the traditional business’s volume and price increase, the company’s valuation system is expected to be restructured!The company’s main business can already support a market value of 100 billion, and the AI customized storage could add another 100 billion. This is a reference point.Third, focus on performance leaders.Who are the performance leaders?

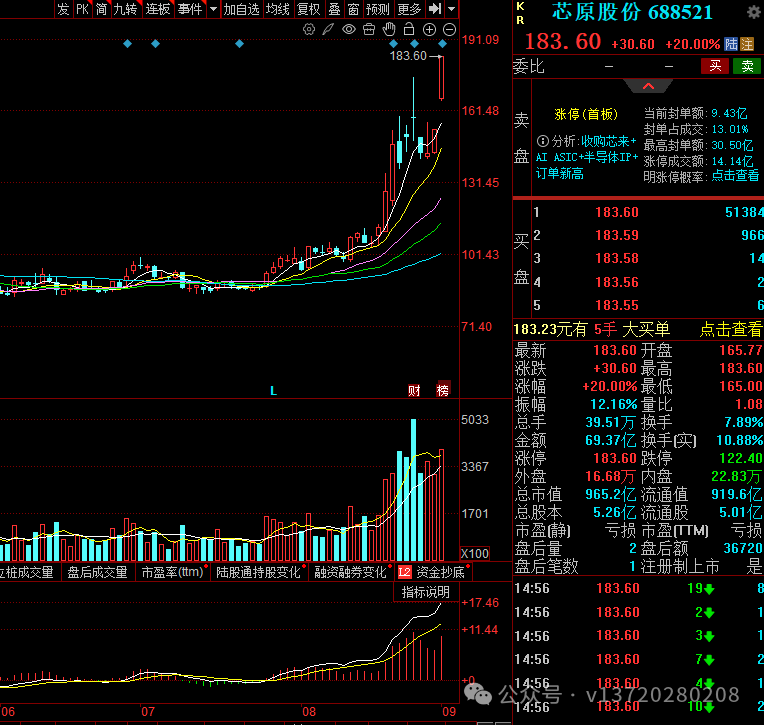

The hottest topic currently is AI. So, which AI chip has the highest correlation in the market recently? That would be GigaDevice’s storage solutions.Technically, it has not yet reached historical highs and has the potential for new highs, making it worth watching.What do the brokerage reports say?There is a significant expectation gap for customized storage: 3D stacking is not a lower-tier substitute for HBM; each has its own market strengths. The bandwidth is 5-10 times that of the existing HBM3e, making it particularly suitable for inference scenarios; the long-term value of inference cards: storage value = 10:2.5~3, with the 2028 market for computing chips estimated at 800 billion, and the customized storage market at over 200 billion. GigaDevice is the absolute leader, with almost all major manufacturers as partners, and combined with the traditional business’s volume and price increase, the company’s valuation system is expected to be restructured!The company’s main business can already support a market value of 100 billion, and the AI customized storage could add another 100 billion. This is a reference point.Third, focus on performance leaders.Who are the performance leaders? That would be Chipone Technology. As of September 11, 2025, Chipone Technology has signed new orders exceeding 1.2 billion, a significant year-on-year increase of 85.88%, setting a historical high for the company, with approximately 64% of the orders related to AI computing power. In terms of valuation, if major manufacturers develop their own chips and assuming a 50% market share after cooperation is finalized, this could lead to an annual revenue increase of 5 billion and a gross profit of 1 billion. Considering demand from other industries and clients could bring in another 1 billion annually, revenue could potentially quadruple by 2026. Based on optimistic valuations, 80 billion in revenue at a 20x PS ratio would yield a market value of 1.6 trillion, while the current market value is 965 billion. This is a reference point.Alright. These are my thoughts for your consideration.

That would be Chipone Technology. As of September 11, 2025, Chipone Technology has signed new orders exceeding 1.2 billion, a significant year-on-year increase of 85.88%, setting a historical high for the company, with approximately 64% of the orders related to AI computing power. In terms of valuation, if major manufacturers develop their own chips and assuming a 50% market share after cooperation is finalized, this could lead to an annual revenue increase of 5 billion and a gross profit of 1 billion. Considering demand from other industries and clients could bring in another 1 billion annually, revenue could potentially quadruple by 2026. Based on optimistic valuations, 80 billion in revenue at a 20x PS ratio would yield a market value of 1.6 trillion, while the current market value is 965 billion. This is a reference point.Alright. These are my thoughts for your consideration.