60s Quick Read:

1. OpenAI plans to purchase $300 billion worth of computing power from Oracle within five years, leading to a single-day market value surge of approximately $250 billion for Oracle. The unfulfilled performance obligations (RPO) for the first fiscal quarter of 2026 reached $455 billion (a year-on-year increase of 359%), confirming strong demand for AI infrastructure, with computing hardware being the first to benefit.

2. In the first half of the year, consumer electronics and semiconductors have rebounded, with AI computing catalyzing a “dual prosperity resonance period”; the second half of the year and next year’s consumer electronics peak season, combined with the release of new AI products at the edge, has led to active AI capital expenditures from major domestic and international companies, indicating a continued upward trend in the industry cycle and highlighting the value of allocation.

3. The central and local governments have introduced policies from multiple dimensions, including funding, taxation, technology, and talent, to build a supportive framework, optimize the business environment for enterprises, and promote rapid development and competitiveness in the industry.

On September 12, the semiconductor industry continued to rise.

It is reported that OpenAI has signed an agreement to purchase $300 billion worth of computing power from Oracle over approximately five years. Oracle’s stock surged 35.95% to a record high, with a single-day market value increase of about $250 billion. Additionally, according to Oracle’s performance data for the first fiscal quarter of 2026, the company’s unfulfilled performance obligations (RPO) have reached $455 billion, a year-on-year increase of 359%. The surge in Oracle’s RPO indicates strong demand for AI infrastructure, with AI being deployed on a large scale, and computing hardware will be the first to benefit.

Guotai Junan released a research report stating that NVIDIA’s next-generation Rubin CPX has split the computing load of AI inference at the hardware level, with memory upgrades providing faster transmission.

CITIC Construction Investment’s research report indicates that consumer electronics and semiconductors have continued to recover in the first half of the year, entering a new round of dual prosperity resonance period under further catalysis of AI computing, driving performance upward. Looking ahead to the second half of the year and next year, the consumer electronics peak season combined with the intensive release of new AI products at the edge, along with positive guidance on AI-related capital expenditures from major domestic and international companies, is expected to drive the fundamentals of the electronics industry positively, coupled with various favorable catalysts such as innovation upgrades, indicating a continued upward trend in the industry cycle and highlighting overall allocation value.

This report will comprehensively analyze the driving factors of the semiconductor equipment industry, delve into the current market development status and competitive landscape of the industry chain, and systematically sort out the development dynamics of core enterprises, presenting a complete picture of the semiconductor equipment industry to help readers accurately grasp the development trends of the industry.

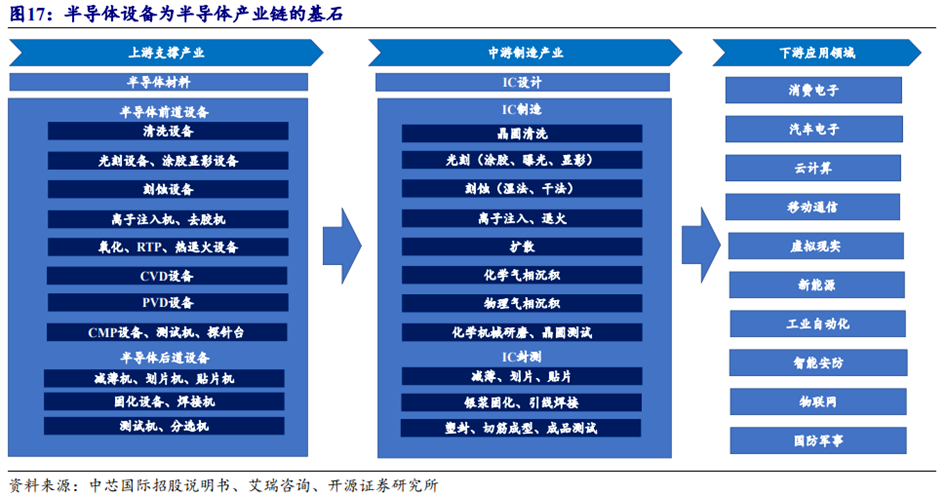

I. Industry Overview

As a core support field for integrated circuit manufacturing, semiconductor equipment can be clearly divided into two major segments based on the manufacturing process: front-end process equipment and back-end process equipment. Among them, front-end process equipment focuses on wafer manufacturing, covering 11 categories of equipment and more than 50 specific models, while lithography machines, etching machines, thin film deposition machines, ion implanters, chemical mechanical polishing (CMP) equipment, cleaning machines, front-end inspection equipment, and oxidation annealing equipment are the core technical devices supporting this segment; back-end process equipment is focused on packaging and testing, mainly including sorting machines, dicing machines, die bonders, and various testing equipment.

From a market structure perspective, wafer manufacturing equipment dominates the semiconductor equipment industry. According to SEMI (Semiconductor Equipment and Materials International), in 2023, the sales of this type of equipment accounted for as much as 90% of the overall semiconductor equipment market. Further segmentation shows that thin film deposition equipment, lithography equipment, and etching equipment, known as the “three pillar devices” of chip manufacturing, together account for over 60% of the market share; notably, due to their rapid technological iteration and broad application scenarios, thin film deposition equipment and etching equipment have significantly higher average annual growth rates than other categories of equipment.

The development of the semiconductor equipment industry exhibits a “dual driving” characteristic: on the demand side, technological innovation and the continuous expansion of end application scenarios jointly drive long-term growth in industry scale, but due to factors such as the product replacement cycle and market supply-demand balance, the industry’s prosperity will show significant fluctuations in the short to medium term. Historical data shows that global semiconductor annual sales form an “M”-shaped fluctuation cycle approximately every ten years, with each cycle’s growth driven by emerging application demands (such as past smartphones, current AI, and new energy vehicles); in the short to medium term, industry demand cycles exhibit a 4-5 year cyclical change.

From the perspective of end device types, the demand fluctuations for different chips are significantly different: memory chips experience the most severe demand fluctuations due to high market concentration and strong product homogeneity; logic chips follow; while analog chips, with their rich product categories (covering power management, signal processing, etc.), diverse downstream applications (industrial, automotive, consumer electronics, etc.), and long product life cycles, exhibit strong anti-cyclical capabilities.

In terms of technological evolution, the development of semiconductor chips has always followed Moore’s Law, with different types of chips having distinct evolution paths: analog chips focus more on performance stability and reliability, with relatively low requirements for process technology; logic chips and dynamic random-access memory (DRAM) continuously push for process miniaturization (e.g., iterating from 7nm to 3nm, 2nm); NAND flash chips are shifting towards 3D structures, with the number of stacked layers continuously breaking through (from dozens of layers to hundreds of layers). With the continuous advancement of technology nodes, the scale of equipment investment corresponding to unit capacity has significantly increased—this trend not only directly drives the steady expansion of the semiconductor equipment market scale but also gradually raises the low points of the industry cycle, becoming a core driving force for the long-term growth of the industry.

II. Market Status

1. Mainland China Remains the Core Market for Global Semiconductor Equipment

The global semiconductor equipment market scale continues to rise, with mainland China becoming a key growth pole due to strong investment momentum. According to SEMI data, the total sales of global semiconductor manufacturing equipment (OEM) are expected to exceed $125.5 billion by 2025, a year-on-year increase of 7.4%, setting a new historical high. From a regional perspective, mainland China has long occupied the forefront of global equipment spending, maintaining the first position with a 42.3% global share in 2024, far exceeding South Korea (17.5%) and Taiwan (14.1%), with equipment spending reaching $49.55 billion that year, a year-on-year increase of 35.4%, highlighting the strong development momentum driven by capital investment.

Although equipment spending in mainland China is expected to adjust to $38 billion in 2025 (a decline from the 2024 peak), it will still maintain a core position in the global market, fully reflecting the resilience of industrial development. In the competition among global equipment manufacturers, American companies still dominate, but Chinese enterprises have made breakthroughs: North Huachuang is the only Chinese company to enter the global Top 10, ranking sixth in 2024 after rising from eighth in 2023, marking the accelerated rise of Chinese semiconductor equipment companies.

2. The Process of Domestic Substitution of Semiconductor Equipment Shows Significant Differentiation

From a segmented perspective, domestic substitution presents a pattern of “partial breakthroughs and partial delays.” According to TrendForce statistics, the domestic substitution rate for de-bonding equipment has exceeded 80%, followed by cleaning equipment (50%-60%) and etching equipment (55%-65%), with thermal processing and CMP equipment (both 30%-40%) also making steady progress, becoming “advantageous areas” for domestic substitution.

In contrast, the domestic substitution rate for some high-difficulty equipment segments remains low, becoming a “short board” for the industry’s self-control: the domestic substitution rate for PVD equipment (10%-20%) and ion implantation equipment (10%-20%) is less than 20%; the breakthrough difficulty for CVD/ALD equipment and coating/developing equipment (both 5%-10%) is even greater; measurement/testing equipment (1%-10%) and lithography equipment (0%-1%) are in a “bottleneck” state. Breakthroughs in these low domestic substitution rate segments will be key to promoting the self-sufficiency of China’s semiconductor industry.

3. Domestic Equipment Companies Show High Growth, Highlighting Development Resilience

In recent years, domestic semiconductor equipment companies have performed well in revenue, profit, orders, and R&D investment, demonstrating strong growth potential.

High growth in revenue and profit: From 2019 to 2023, the combined revenue of 14 core domestic equipment companies increased from 13.81 billion yuan to 50.93 billion yuan, with a compound annual growth rate (CAGR) of 38.6%, significantly higher than the CAGR of 28.4% for the semiconductor equipment market in mainland China during the same period (from $13.45 billion to $36.59 billion); during the same period, the combined net profit attributable to shareholders increased from 1.59 billion yuan to 9.59 billion yuan, with a CAGR of 56.7%, reflecting the continuous improvement in profitability while expanding scale.

Abundant orders on hand: As of the end of the third quarter of 2024, the total contract liabilities of major companies in the equipment sector reached 18.39 billion yuan, nearly doubling from 9.87 billion yuan in the fourth quarter of 2021, and continuing to grow quarter-on-quarter, providing solid support for future performance growth.

Increased R&D investment: To catch up with overseas leaders, domestic manufacturers have continuously increased R&D investment, with the combined R&D expenses of 14 companies rising from 1.26 billion yuan to 7.28 billion yuan from 2019 to 2023, and the R&D expense ratio increasing from 10.8% to 14.3%, laying a foundation for product category improvement, technological iteration, and enhancement of core competitiveness.

4. Steady Expansion of Semiconductor Equipment and Parts Exports

China’s semiconductor equipment and parts exports show a trend of “continuous growth and market diversification.” From 2022 to 2024, the total export value increased from $4.09 billion to $5.21 billion, achieving steady growth; the growth momentum continued in 2025, with export amounts reaching $690 million in January-February, a year-on-year increase of 15.6%.

In terms of export destinations, the United States, India, and Singapore are the main markets in 2024, accounting for a total of 35% of the total exports; notably, Russia has become a region with significant export growth in 2024, reflecting the increasing recognition of Chinese semiconductor equipment in emerging markets and further optimizing the export market structure.

III. Driving Factors

1. Continuous Improvement of Policy System, Strengthening the Foundation for Industry Development

As a core strategic industry of the country, the semiconductor industry has received comprehensive policy support from central and local governments in recent years. Policies and regulations covering funding support, tax reductions, technological innovation incentives, and talent cultivation have been intensively implemented, establishing a solid policy support framework for the semiconductor and specialized equipment industry.

The implementation of these policies has not only created a better business environment for domestic semiconductor equipment companies but has also continuously strengthened key areas such as funding support for industrial development, assistance in technological R&D breakthroughs, and support for talent team building. Driven by this, the domestic semiconductor equipment industry has achieved rapid development, and the market competitiveness of domestic enterprises has significantly improved, with policies becoming the core driving force for the industry’s steady progress.

2. Tariff Pressure Accelerates Industry Transformation, Promoting Domestic Substitution Process

(1) Trade Friction Drives Accelerated Self-Control Layout

Since the implementation of the equal tariff policy by the Trump administration on April 9, the uncertainty of the tariff environment in the chip industry has significantly increased. The continuous escalation of U.S. sanctions against China’s chip industry has had a dual impact: on the one hand, it has restricted American manufacturers’ exports to China, and on the other hand, it has become a key driving force for accelerating the self-control process of China’s semiconductor industry.

The semiconductor equipment industry is the cornerstone of the chip industry, and the progress of domestic substitution directly relates to the safety of the domestic chip industry. In this context, achieving substitution for American manufacturers has become an inevitable trend in industry development.

(2) High Dependence of American Manufacturers on the Chinese Market, Broad Space for Domestic Substitution

Since 2020, the sales scale of American semiconductor equipment manufacturers in mainland China has continued to rise. In the 2024 fiscal year, the sales of the top three manufacturers, AMAT, LAM, and KLA, in mainland China reached $10.117 billion, $6.294 billion, and $4.197 billion, respectively, accounting for as much as 37%, 42%, and 43% of their respective revenues.

The market scale of over $20 billion for these three American manufacturers in mainland China provides a broad space for domestic equipment to substitute. From a technological perspective, domestic equipment has already achieved effective substitution in most segments of mature processes, and the substitution process in advanced process fields is expected to accelerate further.

(3) Significant Achievements in Multi-Point Layout of Domestic Equipment

Currently, the semiconductor equipment field has basically completed the layout for domestic substitution, with particularly prominent coverage in etching, cleaning, and thin film deposition. A number of leading enterprises in the industry, such as Shanghai Microelectronics, North Huachuang, and Zhongwei Company, have been cultivated.

However, the lithography segment’s lithography machines and coating/developing machines, as well as measurement/testing equipment, remain key technical challenges that domestic enterprises need to overcome. Overall, domestic equipment is in a critical stage of transitioning from “usable” to “well usable,” requiring extensive production line practice to optimize equipment consistency.

In terms of domestic process coverage, key equipment such as lithography machines and measurement equipment urgently need breakthroughs; etching and cleaning equipment have achieved mass production at the 28nm node, with rapid progress in some segments at the 5nm process. The China Semiconductor Industry Association has clearly pointed out that high-energy ion implanters and KrF lithography machines are still key directions for breakthroughs in current domestic semiconductor equipment.

3. A Wave of Wafer Factory Expansion is Coming, Releasing New Opportunities for Equipment Demand

TrendForce data shows that the current semiconductor market is experiencing a differentiation in demand between advanced processes and mature processes. Driven by the demand for AI servers, high-performance computing chips, and smartphone chips, the capacity utilization rates of advanced processes such as 5/4nm and 3nm are expected to remain fully loaded by the end of 2024; meanwhile, mature processes of 28nm and above are in a mild recovery phase, with average capacity utilization rates in the second half of 2024 expected to increase by 5%-10% compared to the first half.

Institutions predict that by 2025, domestic wafer foundries will become the core force for growth in mature process capacity, with the capacity of the top ten global mature process foundries expected to increase by 6%. A series of expansion plans, including TSMC’s Kumamoto JASM project in Japan, SMIC’s Shanghai Lingang and Beijing bases, Huahong Group’s Fab9 and Fab10, and Jinghe Integration’s N1A3, will gradually be implemented.

By the end of 2025, the capacity of mainland wafer foundries in the top ten global manufacturers is expected to exceed 25%, with the most significant new capacity in the 28/22nm segment. The large-scale capacity expansion of wafer foundries will directly drive a significant increase in upstream semiconductor equipment demand, bringing new growth opportunities for the industry.

IV. Industry Development Trends

1. Market Scale Expands Rapidly, with Mainland China’s Position Being Unparalleled

The rapid rise of generative AI, smart vehicles, the Internet of Things, and 6G technology has led to an explosive growth in chip demand, which has become the core driving force for the continuous expansion of the semiconductor equipment market scale. On July 22, 2025, SEMI clearly stated in its “Mid-Year Total Semiconductor Equipment Forecast Report” that the total sales of semiconductor manufacturing equipment (OEM) are expected to surge to $125.5 billion, achieving a year-on-year growth of 7.4%, setting a new historical record. Moreover, driven by strong forces such as advanced logic, memory technology iteration, and industrial technology migration, it is expected that by 2026, equipment sales will further rise to $138.1 billion, achieving three consecutive years of steady growth.

In the grand pattern of the booming global semiconductor equipment industry, mainland China, with its continuous expansion actions of domestic wafer foundries, is becoming increasingly critical in the global market. Although the sales in 2025 are expected to decline compared to the record of $49.5 billion set in 2024, it will still maintain its position as the leading market globally throughout the forecast period. For example, in the first quarter of 2025, global semiconductor manufacturing equipment sales increased significantly by 21% year-on-year, reaching $32.05 billion, marking the second-highest record in history. However, the sales in mainland China, although down 18% year-on-year to $10.26 billion, have maintained their position as the largest chip equipment market globally for the eighth consecutive quarter. It is worth noting that as Taiwan and South Korea significantly increase their investments in semiconductor equipment, the proportion of mainland China in the overall semiconductor equipment sales has narrowed from 47% in the same period last year to 32%.

2. Multiple Technological Breakthroughs Accelerate Domestic Substitution

(1) Cutting-Edge Technologies Drive Industry Transformation

The semiconductor manufacturing process is racing towards more advanced processes of 2nm and below, with EUV lithography machines becoming indispensable core equipment in high-end chip manufacturing. Meanwhile, HBM4 memory technology and Chiplet advanced packaging technology are also being updated and iterated at an astonishing speed, continuously injecting strong momentum for the enhancement of storage and computing performance. These breakthroughs in cutting-edge technologies are reshaping the competitive landscape of the semiconductor industry and imposing stringent requirements on key indicators such as the performance and precision of semiconductor equipment. For instance, to adapt to advanced processes of 2nm and below, semiconductor equipment must achieve qualitative leaps in precision control at the nanometer level, higher integration, and significant improvements in production efficiency to meet the new demands of industry development.

(2) Domestic Substitution Has a Long Way to Go

With strong support from national policies, the domestic substitution process of China’s semiconductor equipment has significantly accelerated. However, core equipment such as lithography machines still heavily rely on imports, and there is still a long way to go to achieve the goal of self-control in semiconductor equipment. For example, lithography machines have a very complex technical system, involving multiple top-tier technology fields such as ultra-precision optics and ultra-high precision mechanics, with a high technical threshold. If enterprises want to overcome these key technical challenges, they must further increase R&D investment, deepen cooperation with universities and research institutions, integrate various advantageous resources, and collaboratively carry out technological breakthroughs to gradually reduce dependence on foreign technologies.

(3) New Dimensions of Competition Are Expanding

Entering 2025, competition in the domestic semiconductor equipment field is showing two new trends:

On the one hand, the competition for service ecosystems is fully ignited. Domestic equipment manufacturers are actively laying out and building an integrated service system of “equipment-process-materials,” drawing on the successful experiences of international semiconductor equipment giants to provide customers with one-stop services covering the entire lifecycle of equipment. Moreover, manufacturers are also proactively collaborating with chip design companies to jointly develop customized solutions tailored to specific customer needs, enhancing customer stickiness and improving their overall competitiveness in the market. For example, some domestic equipment manufacturers have partnered with well-known domestic chip design companies to jointly develop chip manufacturing processes suitable for specific application scenarios, providing a complete set of solutions from equipment selection, process parameter optimization to material adaptation, not only accurately meeting customers’ personalized needs but also significantly enhancing customers’ reliance on their products and services.

On the other hand, cost advantages are becoming increasingly prominent. Due to factors such as Japan’s export controls, the costs of imported semiconductor equipment have surged by over 50%. In stark contrast, domestic equipment, relying on the advantages of a localized supply chain, has achieved remarkable results in cost control, with prices only 60%-70% of imported equipment. This outstanding cost-performance advantage is significantly changing the market procurement pattern, attracting more and more domestic semiconductor companies to turn their attention to domestic equipment. For example, in some mature process fields where equipment precision requirements are relatively low but cost sensitivity is high, domestic equipment is continuously expanding its market share, gradually encroaching on the market space of imported equipment.

In the face of the complex situation of global semiconductor industry chain restructuring, Chinese enterprises need to further strengthen upstream and downstream collaborative cooperation, steadily advance into high-end fields based on mature processes. With the help of policy support and continuous technological innovation, it is expected to achieve key technological breakthroughs in segmented fields, gradually narrowing the gap with internationally leading enterprises. At the same time, actively expanding international cooperation channels and striving to break through technological blockades and supply chain barriers will become important directions for promoting the sustainable development of China’s semiconductor equipment industry.

3. Material Innovations Are Flourishing, and Green Manufacturing Is Gaining Attention

The emergence of new semiconductor materials such as silicon carbide and silicon photonic chips brings hope for breaking through the performance bottlenecks of traditional silicon-based materials, likely becoming a new growth point for the semiconductor industry. For instance, silicon carbide possesses a series of excellent characteristics such as high breakdown electric field, high saturation electron drift velocity, and high thermal conductivity, showing extremely broad application prospects in fields such as new energy vehicles and 5G communications, thereby strongly promoting the innovative development of related semiconductor equipment.

At the same time, environmentally friendly processes and sustainable development concepts are increasingly gaining traction in the semiconductor industry. Semiconductor equipment companies are paying more attention to energy conservation and emission reduction during the production process, actively promoting the widespread application of green manufacturing technologies. Some companies have optimized equipment designs, introduced more efficient energy management systems, and significantly reduced equipment operating energy consumption; in terms of material selection for equipment manufacturing, they prioritize recyclable and low-pollution environmentally friendly materials to minimize negative impacts on the environment.

Although the semiconductor equipment industry has a broad prospect, it also faces severe challenges from rapid technological iteration and geopolitical risks. The rapid update and iteration of technology may render existing technologies and equipment obsolete in a short period, making it difficult for enterprises to recover their initial R&D costs; geopolitical conflicts may lead to supply chain disruptions and market access restrictions, severely affecting normal production and operation of enterprises. Therefore, enterprises must resolutely follow the path of innovation-driven development, continuously enhance the resilience and stability of the supply chain to maintain a foothold in the fierce market competition and stay ahead.

V. Industry Chain Analysis

1. Semiconductor Components: Broad Opportunities Under the Domestic Substitution Wave

(1) Industry Chain Positioning and Supply Model

Semiconductor components are located upstream of the chip manufacturing industry chain, providing critical support for semiconductor equipment and wafer foundries. These components first form modules and subsystems, which are then assembled into semiconductor equipment. At the same time, wafer foundries also directly purchase some components as replacement parts, and some consumable components need to be replaced regularly, which gives the components market continuous demand momentum.

(2) Domestic Substitution Process and Replacement Space

The improvement of the domestic substitution rate of semiconductor components is a key link in achieving self-control of the industry chain. Currently, the trend of domestic self-control is gradually extending upstream in the industry chain, with the core to solving the “bottleneck” problem being the completion of domestic substitution of semiconductor equipment components. In the mid-to-low-end component field, domestic manufacturers have the technical capability to substitute, but their market share remains low; in the high-end component field, there is still a certain gap compared to international advanced levels, but this also means that there is significant room for improvement in the future domestic substitution rate.

(3) Composition and Value Distribution of Components

Semiconductor equipment components cover seven major categories, including mechanical, electrical, mechatronic, gas/liquid/vacuum systems, instruments, and optics. Among them, the mechanical category accounts for the highest value proportion, reaching 20-40% of equipment costs, which can be further subdivided into metal and non-metal categories. The value proportions of electrical, mechatronic, and gas/liquid/vacuum systems all exceed 10%, with urgent domestic substitution demand for key components such as RF power supplies, EFEM, gas cabinets, and vacuum valves.

(4) Market Scale and Competitive Landscape

From a cost perspective, components account for about 90% of the operating costs of semiconductor equipment, with a market scale of about 40% of semiconductor equipment, and will grow in sync with the equipment market. The growth rate differences between equipment segments will also affect the market potential of various component categories. The global semiconductor components market is vast, with an estimated scale of about $33.5-35 billion (approximately 240 billion yuan) excluding direct purchases by wafer foundries; if including direct replacements by wafer foundries, the global market scale reached 386.1 billion yuan in 2022, with mainland China’s market at 114.1 billion yuan. In terms of competitive landscape, although dominated by American and Japanese companies, the diverse categories of components and the relatively fragmented market provide opportunities for new entrants to increase market share.

2. Semiconductor Equipment: Accelerating Catch-Up, Moving Towards High-End

(1) Lithography Machines: Monopoly and Breakthrough Coexist

Lithography machines are core equipment for chip manufacturing, and their technical level directly determines the process and performance of chips. Lithography costs account for about 30% of chip manufacturing costs, with time consumption accounting for 40-50%. Lithography machines mainly consist of key structures such as light sources, illumination systems, and mask stages, and can be classified into G-line, I-line, KrF, ArF (including ArFDry and ArFi, collectively referred to as DUV lithography), and EUV types based on the light source.

The global lithography machine equipment market is expected to reach approximately $31.5 billion in 2024, making it the largest segment of semiconductor equipment. The global shipment of lithography machines continues to rise, with ASML, Canon, and Nikon dominating the market. Among them, ASML holds an absolute advantage in high-end lithography machines, especially monopolizing the EUV field, with the first delivery of two new EXE (HighNAEUV) devices in 2024, leading the industry into a new era.

China is the largest market for semiconductor equipment and an important customer for ASML, but domestic lithography machines face a supply-demand imbalance. In 2023, the production of lithography machines in China was only 124 units, while the demand reached 727 units, with a domestic substitution rate of only 2.5%, and the technology of complete machines lags significantly behind overseas. The strengthening of export restrictions on advanced processes by the U.S., Japan, and the Netherlands makes the domestic production of lithography machines imperative. Shanghai Microelectronics, as a domestic manufacturer, has achieved mass production at the 90nm process and is actively developing 28nm immersion lithography machines.

(2) Etching Equipment: Growing Demand and the Path to Catch-Up

The core purpose of etching is to precisely cut the substrate or film according to design drawings, divided into wet etching and dry etching, with dry etching, especially plasma dry etching, being the mainstream technology. Plasma etching equipment uses active particles generated by plasma discharge to react with materials, achieving microstructure processing.

The global dry etching market is dominated by international giants, with Lam Research, Tokyo Electron, and Applied Materials accounting for 90.24% of the global dry etching equipment market in 2020. As the integrated circuit industry develops, the complexity requirements for etching processes continue to increase, and it is expected that the global market size for dry etching equipment for integrated circuit manufacturing will grow to $18.185 billion by 2025. In the development of advanced chip processes, trends such as multiple exposures and three-dimensional storage have made the importance of etching technology and equipment increasingly prominent, with the etching processes required for 7nm integrated circuits increasing 2.5 times compared to 28nm, and the demand for etching equipment in 3D NAND manufacturing has also significantly increased. Domestic manufacturers such as Zhongwei Company and North Huachuang are still in the catch-up stage, with significant development space ahead.

(3) Thin Film Deposition Equipment: Breakthroughs in Core Equipment

Thin film deposition equipment is one of the three core devices for chip manufacturing, classified into PVD, CVD, and ALD based on process principles, used to deposit nanometer-level films on substrates. PVD vaporizes materials through physical methods and deposits them; CVD forms solid deposits through chemical reactions; ALD deposits layer by layer in the form of monolayers, offering advantages such as precise control of film thickness.

In the CVD field, PECVD equipment is the most widely used, accounting for 33% of thin film deposition equipment; in the PVD field, sputtering PVD equipment is predominant. With the upgrading of chip processes and technologies, the number of thin film deposition processes and types of materials has significantly increased, and the requirements for thin film particles are also continuously rising. Meanwhile, the vertical development of NAND further drives the demand for thin film deposition equipment. It is expected that the global thin film deposition equipment market will reach $23.96 billion by 2025, with the domestic market exceeding $8.2 billion. The global market shows a highly monopolized pattern, mainly dominated by American Applied Materials, Lam Research, and Japan’s Tokyo Electron, while domestic manufacturers such as North Huachuang and Tuo Jing Technology have significant room for market share growth, with domestic manufacturers’ market share in 2023 being less than 20%.

(4) Measurement and Testing Equipment: Yield Assurance and Domestic Breakthroughs

Front-end measurement/testing is a key link in ensuring yield, reducing costs, and promoting process iteration in chip manufacturing. Measurement equipment is used to measure wafer structure dimensions and material properties, while testing equipment is used to identify surface defects on wafers. As processes develop towards finer line widths, higher requirements are placed on the precision, sensitivity, and stability of measurement and testing equipment.

The measurement and testing equipment market is showing trends such as improvements in optical detection technology, multi-system combinations, applications of big data algorithms, and increased equipment speed. In 2023, the global semiconductor testing and measurement equipment market size reached $12.83 billion, and it is expected that by 2025, the global measurement equipment market size will reach $15.73 billion, with the Chinese market size expected to reach $5.19 billion. Currently, foreign manufacturers such as KLA have long dominated the market, while domestic manufacturers such as Shanghai Jingce, Shanghai Ruile, and Zhongke Feice are actively laying out and gradually achieving technological breakthroughs in advanced processes, with promising prospects for domestic substitution in the future.

(5) Ion Implantation Equipment: Precise Doping and Domestic Breakthroughs

Ion implantation is one of the core processes in semiconductor manufacturing, achieving precise doping by injecting charged ions into semiconductor materials, defining the electrical characteristics of chips. Compared to thermal diffusion, ion implantation technology offers advantages such as single-sided collimated doping, good uniformity, and strong controllability, with important applications in solar cell manufacturing and other fields.

Ion implantation equipment can be divided into medium-low current, low energy high current, and high energy ion implanters, with high energy ion implanters being the most technically challenging. The global market size for ion implantation equipment is expected to reach 27.6 billion yuan in 2024, and is projected to rise to 30.7 billion yuan by 2030, with the domestic market space around 16 billion yuan. The global market is mainly dominated by foreign manufacturers such as AMAT, Axcelis, and Nissin, while domestic manufacturers such as Kaishitong and Zhongke Xinxin have made certain progress, and North Huachuang is entering this field, expected to break the international monopoly.

(6) Cleaning Equipment: Impurity Removal and Domestic Upgrades

Semiconductor cleaning equipment is used to remove impurities from wafer surfaces, ensuring chip yield and performance, with wet cleaning being the current mainstream technology, accounting for over 90% of cleaning steps in chip manufacturing, while dry cleaning is mainly applied in advanced processes. Wet cleaning includes various methods such as solution soaking and mechanical brushing, while dry cleaning mainly involves plasma cleaning and vapor-phase cleaning.

The global semiconductor cleaning equipment market is highly concentrated, with DNS, TEL, LAM, and SEMES accounting for over 90% of the market share in single-wafer cleaning equipment. As memory technology develops towards three-dimensional architectures, the demand for cleaning equipment continues to increase, with cleaning steps accounting for over 30% of chip manufacturing processes. Domestic manufacturers such as Shengmei Shanghai are actively developing differentiated technologies, accelerating the domestic substitution process.

(7) CMP Polishing Equipment: Key for Flattening and Domestic Development

CMP equipment is mainly used for global flattening treatment of wafers, ensuring smooth progress of subsequent processes through a combination of chemical etching and mechanical grinding. The equipment mainly consists of three units: wafer transport, polishing, and cleaning. CMP equipment is widely used in wafer material manufacturing, semiconductor manufacturing, and packaging testing.

The global CMP market is generally on an upward trend, expected to reach $3.2 billion in 2024, but the market is highly monopolized, with American Applied Materials and Japan’s Ebara accounting for over 90% of the global market share. As chip integration increases and processes shrink, the precision and integration requirements for CMP equipment continue to rise, providing significant room for domestic CMP equipment to grow.

(8) Semiconductor Testing Equipment: Performance Testing and Domestic Rise

Testing is an important link in semiconductor detection, applied in design and packaging testing, divided into CP wafer testing and FT chip finished product testing. Testing equipment mainly includes testers, probe stations, and sorting machines, with testers accounting for over 60% of the value.

It is expected that by 2027, the global semiconductor testing equipment market size will reach $10.68 billion, with the testing machine market size reaching $6.57 billion, and the SOC testing machine market size reaching $4.1 billion. The global market is mainly dominated by overseas giants such as Teradyne and Advantest, while domestic manufacturers are about to achieve volume production in high-end SOC and memory testing equipment.

(9) Packaging Equipment: Potential Track for Domestic Substitution

Traditional packaging equipment includes wafer thinning machines, dicing machines, and die bonders according to the process flow. Back-end packaging equipment accounts for about 6% of the semiconductor equipment market, and with the development of advanced packaging, the demand for traditional packaging equipment is expected to grow, which will also bring new demand for front-end wafer manufacturing equipment.

In various sub-segments of packaging equipment, markets for thinning machines, dicing machines, die bonders, and plastic packaging machines are all showing growth trends, but the global market is mostly dominated by foreign manufacturers. Although domestic manufacturers have gaps compared to overseas giants, there is enormous development potential in each sub-segment under the wave of domestic substitution.

VI. Related Companies in the Semiconductor Industry:

SMIC (688981): The company is a leader in China’s integrated circuit manufacturing industry and one of the world’s leading integrated circuit wafer foundry companies. Its main business is to provide chip manufacturing services to customers, offering 8-inch and 12-inch wafer foundry and technical services. According to the sales data of global pure wafer foundry companies in 2024, SMIC ranks second globally and first among Chinese companies.

Cambricon (688256): The first AI chip company on the Sci-Tech Innovation Board, a pioneer in the global smart chip field, and one of the few companies that fully master core technologies for general-purpose smart chips and basic system software. Its main business is the R&D, design, and sales of AI core chips used in various cloud servers, edge computing devices, and terminal devices.

Haiguang Information (688041): A leading domestic server CPU chip company established in 2014, mainly engaged in the R&D, design, and sales of high-end processors used in servers, workstations, and other computing and storage devices, including Haiguang general-purpose processors and Haiguang co-processors, with processor designs based on the x86 architecture, compatible with the mainstream X86 instruction set in the market.

002***: As a platform-type semiconductor equipment leader, it has successfully developed several high-end equipment with independent intellectual property rights, such as high-density plasma chemical vapor deposition HDPCVD, dual large-damascus CCP etching machines, and vertical furnace atomic layer deposition ALD, providing comprehensive equipment support for semiconductor manufacturing.

603***: A global leading CMOS image sensor chip design company headquartered in the United States, with R&D, operations, and markets spread globally. Its products are widely used in smartphones, automotive, security monitoring, and other fields, consistently ranking among the top three global suppliers of CMOS image sensors.

688***: A global leader in memory interface chips, focusing on providing high-performance, low-power chip solutions for cloud computing and AI fields, adopting a “Fabless” model, with its DDR5 memory interface chip technology leading globally, along with products such as the Jindai server platform.

… …

Scan to reply “8-Semiconductor Industry” to receive dragonhead stocks.

Disclaimer

All content and opinions produced by Shaanxi Jufeng Investment Consulting Co., Ltd. (hereinafter referred to as “Jufeng Investment Consulting”) depend on various market environment factors and internal factors of the company known to the authors of relevant research reports. Profit forecasts and target prices are based on a series of assumptions and premises, therefore, investors can only form a relatively comprehensive understanding of our expressed opinions based on the full information of the relevant targets in the research report.

The content produced by Jufeng Investment Consulting is merely a citation or retelling of part of the relevant target research report, and due to technical or other objective conditions, it is impossible to provide all the assumptions and premises on which various opinions are formed simultaneously, the relevant content may not fully or accurately express the views or opinions of the relevant research report, and is therefore for reference only. Investors should not rely on it. No one should use the information, opinions, and data contained in the content produced by Jufeng Investment Consulting as the basis for their investment decisions. The information, opinions, and data released by Jufeng Investment Consulting may no longer be accurate or valid due to changes in circumstances or other factors after the publication date of the research report, and Jufeng Investment Consulting does not commit to updating inaccurate or outdated information, opinions, and data. All information in the content produced by Jufeng Investment Consulting or expressed opinions are sourced from publicly available materials, and our company does not guarantee the accuracy and completeness of this information. The information or opinions expressed in the content produced by Jufeng Investment Consulting do not constitute operational advice for the buying and selling of the described securities.

The copyright of the relevant content belongs solely to our company, and no institution or individual may forward, reproduce, copy, publish, or quote it in any form without written permission.