Once upon a time, Apple was the technological leader in the mobile phone and consumer electronics industry. Every technological innovation from Apple would have a significant impact on the supply chain! However, with the rapid development of AI, the iteration of NVIDIA’s GB100, 200, 300… Rubin series AI servers, has Apple become a thing of the past? Many Taiwanese PCB companies that thrived on Apple are now facing fierce competition from local PCB manufacturers in mainland China (such as Shenghong, Jingwang, Shengyi…), who are profiting immensely by relying on NVIDIA. Is Apple really in decline? Today, let’s discuss:

the impact of iPhone 17 on the PCB supply chain and response strategies.

Main content is as follows:

-

Innovation and Market Performance of iPhone 17: Introduces the design changes, key hardware upgrades, and market demand for the iPhone 17 series, analyzing initial market performance using data and tables.

-

Direct Impact on the PCB Industry: Analyzes the increase in PCB demand, changes in specifications, and cost impacts due to iPhone 17, including case studies and tables illustrating the technical layouts of various manufacturers.

-

Impact on Upstream Materials and Components: Discusses adjustments in materials, processes, and supply chains for exterior parts, structural components, and electronic hardware, using tables to compare different material properties.

-

Impact on Midstream Manufacturing and Downstream OEM: Explains the capacity adjustments, technical challenges, and supply chain management strategies of OEMs, analyzing channel changes and market competition patterns.

-

Strategic Responses and Future Directions of the Supply Chain: Summarizes the collaborative innovation, technological development paths, and sustainable development strategies of various segments of the supply chain, using tables to outline transformation directions.

-

Summary and Future Outlook: Summarizes the transformative role of iPhone 17 on the PCB supply chain and anticipates future trends in technology integration and development.

1、Innovation Features and Market Performance of iPhone 17

The iPhone 17 series was released in the autumn of 2025, bringing significant design changes and technological innovations that not only attracted widespread consumer attention but also had a profound impact on the global electronics supply chain. This series includes the base model, Pro model, Pro Max model, and the newly launched Air model, which, as a new category, focuses on a combination of lightweight design and high-end materials, replacing the previous Plus version. This series has significant upgrades in material selection, internal structure, and hardware configuration, indicating Apple’s strategic layout in the next generation of mobile device technology.

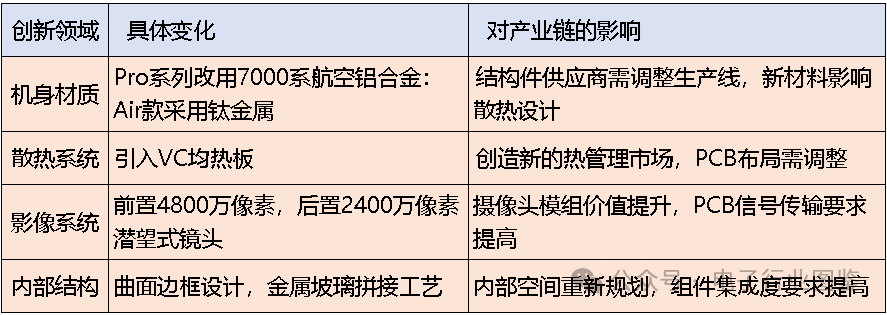

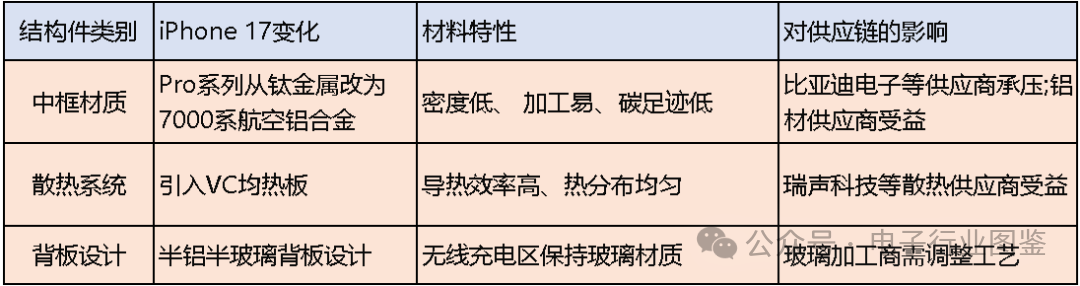

– Design Changes: One of the most notable changes in the iPhone 17 series is the significant adjustment in body materials. Pro and Pro Max models have abandoned the titanium solution used in the previous two generations, opting instead for a frame made of 7000 series aerospace aluminum alloy. This change, while slightly increasing the body weight (by about 8 grams), has actually improved structural strength by 15%, and is more advantageous in terms of cost and environmental protection. Analysis shows that aluminum’s carbon footprint is 67% lower than that of titanium, aligning closely with Apple’s goal of achieving carbon neutrality across its entire value chain by 2030. Meanwhile, the iPhone 17 Air continues to use titanium, forming a differentiated product strategy. In terms of design language, the iPhone 17 series introduces a curved edge design, using a glass and metal splicing material process to achieve a smoother transition between the device’s edges and back cover, presenting a sloped rather than traditional stepped structure, which not only enhances the visual aesthetics of the device but also improves grip comfort.

– Key Hardware Upgrades: In terms of the cooling system, the iPhone 17 Pro series introduces a VC vapor chamber as the core cooling solution for the first time, significantly enhancing the device’s sustained performance. In the imaging system, the Pro series is equipped with an upgraded periscope lens, with the front camera upgraded to 48 million pixels, and the rear main camera reaching 24 million pixels. This upgrade has driven a comprehensive increase in the average selling price of image sensors, modules, and lenses. In terms of core performance, the iPhone 17 series is equipped with a new generation application processor and larger memory capacity, supporting more complex AI computing and multimedia applications. These hardware upgrades not only enhance the phone’s performance but also impose higher requirements on the integration of internal components, cooling performance, and spatial layout.

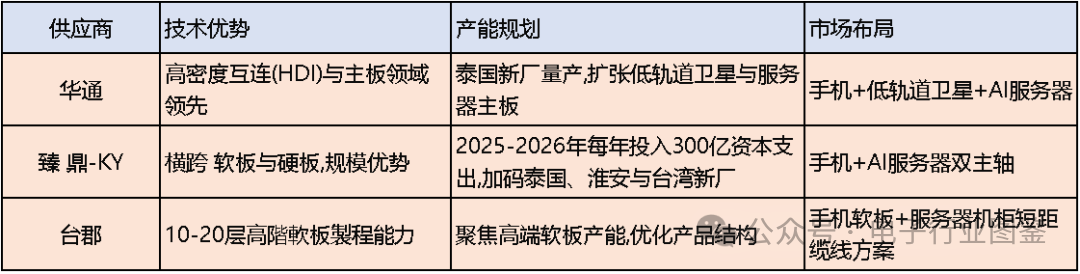

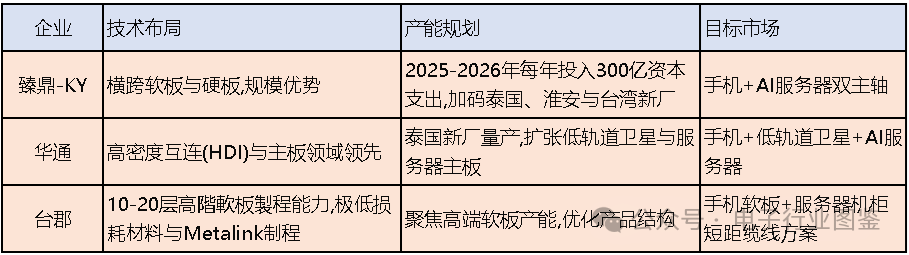

– Market Performance and Demand: From market feedback, the iPhone 17 series has shown strong demand since its launch, particularly performing well in the mainland Chinese market. According to a report from JPMorgan Chase, the iPhone 17 base model, Pro and Pro Max have sustained long delivery times, reflecting a tight market supply-demand situation. The institution has raised its forecast for iPhone production in 2025 to 251 million units, an annual growth rate of about 6%, with total iPhone EMS production expected to reach 147 million units in the second half of 2025, of which the iPhone 17 series accounts for 95 million units, a 3% increase compared to the same period in 2024 for the iPhone 16 series. This market performance has directly driven a surge in supply chain demand, especially in September 2025, when Apple’s attitude towards component procurement became “bold and proactive“, leading to the first wave of shipment peaks. This surge in demand has been particularly significant for the Taiwanese PCB supply chain, with major suppliers such as Huazhong, Zhendin-KY, and Taijun seeing significant revenue increases in September.

Table 1: Key Innovations of the iPhone 17 Series and Their Impact on the Supply Chain

The release of the iPhone 17 series not only represents the evolution of Apple’s products but also marks a new development stage for the mobile device supply chain. From material selection to internal structure, from cooling solutions to imaging systems, various innovations have brought new opportunities and challenges to the upstream and downstream supply chains, which will serve as the foundational background for the subsequent analysis in this article.

2、 Direct Impact on the PCB Industry

The release of the iPhone 17 series has had a significant impact on the PCB (Printed Circuit Board) industry, bringing important changes in demand quantity, technical specifications, and value chain positioning. As the “nervous system” of electronic devices, the performance of PCBs directly affects the efficiency and stability of the entire machine, and in the iPhone 17, the status of this core component has been further elevated.

2.1 Changes in PCB Demand Quantity and Specifications

– Surge in Demand and Revenue Growth: With the official launch of the iPhone 17 series in September 2025, Apple’s supply chain has welcomed a strong surge in demand. This phenomenon is particularly evident in the Taiwanese PCB supply chain. Huazhong, as an important supplier for Apple in the high-density interconnect (HDI) and mainboard fields, has seen its revenue changes fully reflect this trend. In July, Huazhong’s revenue was 5.995 billion yuan, rising to 6.562 billion yuan in August, reaching a nine-month high, and in September, driven by large-scale shipments, monthly revenue challenged a historical high of 7.4 billion yuan, bringing third-quarter revenue close to 20 billion yuan, with a quarterly increase of over 10%. Similarly, Zhendin-KY has also shown strong growth momentum, with revenue in July reaching 13.352 billion yuan, rising to 14.651 billion yuan in August, accumulating over 106.2 billion yuan in the first eight months, rewriting historical highs for the same period. This data clearly shows the positive pull effect of the iPhone 17 release on the PCB supply chain.

– Comprehensive Improvement in Specification Requirements: The performance upgrades of the iPhone 17 series have raised higher requirements for PCBs. To support more powerful computing capabilities, more efficient cooling performance, and more complex signal transmission, PCBs need to develop towards higher layers, higher density, and high-speed transmission. According to industry analysis, the iPhone 17 Pro series, due to the adoption of VC vapor chamber cooling design and upgraded imaging systems, has a more compact internal space, requiring PCBs to achieve a higher degree of integration within limited areas, which promotes the application ratio of arbitrary layer HDI (High Density Interconnector) and substrate-like PCBs. At the same time, to support high-speed data transmission, the demand for low dielectric loss (Low Dk) and low loss factor (Low Df) materials has significantly increased, which shows a trend of collaborative development with the technical requirements in the AI server field.

– Continuous Increase in Flexible Board Usage: The iPhone 17 series, especially the newly launched Air model, has further increased the use of flexible printed circuit boards (FPC) due to its more compact internal structure. This trend directly benefits manufacturers focused on flexible board production, such as Taijun. Although Taijun’s revenue in July and August remained around 1.9 billion yuan, showing a year-on-year decline, this is mainly due to some of its SMT assembly being transferred to other manufacturers, and the actual profit absolute value has not been affected. Notably, Taijun has the capability for 10-20 layer high-end flexible board processing, which allows it to not only meet smartphone demands but also gradually enter the server cabinet short-distance cable replacement solutions, laying the foundation for future development in the AI server market.

2.2 Technological Evolution and Cost Structure

– Increase in Technical Complexity: The performance requirements of the iPhone 17 have directly led to a leap in technical complexity for PCBs. The demand for high-speed transmission requires PCB designs to fully consider signal integrity issues, especially in high-frequency fields above 50 GHz, where the design and optimization of vias become key challenges. To address this issue, leading companies in the industry, such as OKI Circuit Technology, have launched high-frequency via simulation technology, which integrates high-precision manufacturing data, 3D electromagnetic field analysis, and production design optimization to help engineers predict actual via performance before manufacturing, reducing design cycles and improving signal integrity. The application of such technologies has become a necessary condition in the high-end PCB design of the iPhone 17.

– Changes in Cost Structure: With the increase in technical requirements for PCBs, their cost structure has also changed significantly. The use of high-end materials, more complex processing techniques, and stricter quality inspection standards have all increased the manufacturing costs of PCBs. However, from another perspective, these changes have also raised the average price and profit margins of PCB products. For example, Huazhong’s gross margin reached 18.24% in the second quarter of 2025, an increase of 1.07 percentage points quarter-on-quarter and 3.25 percentage points year-on-year, reflecting the profit potential of high-end PCB products. A report from Bank of America also pointed out that due to upgrades in cameras, cooling systems, and mechanical components in the iPhone 17 series, the average selling price of related PCBs and FPCs has increased.

– Adjustment of Capacity Layout: In response to the market opportunities brought by the iPhone 17, major PCB suppliers are actively adjusting their capacity layouts. Zhendin-KY has planned to invest 30 billion yuan in capital expenditures from 2025 to 2026, increasing capacity in Thailand, Huai’an, and Taiwan, focusing on AI servers and high-end PCB applications, forming a dual-axis pattern of “mobile + AI.” Huazhong continues to expand its low-orbit satellite and high-end server motherboard business and has started mass production at its new factory in Thailand to diversify risks and explore new markets. This strategy of capacity expansion and diversification is not only to meet the short-term demand of the iPhone 17 but also to prepare for the long-term diversification of electronic products.

Table 2: Technical Layout and Capacity Planning of Major PCB Suppliers for the iPhone 17 Series

2.3 Restructuring of the PCB Industry Value Chain

The release of the iPhone 17 has not only impacted the technology and demand of the PCB industry but has also triggered a restructuring of the industry value chain. Traditionally, PCBs mainly played a circuit connection role in electronic products, with a relatively limited value proportion. However, with the development of technologies such as AI and high-speed computing, PCBs have become a core link in releasing computing power performance. This trend is particularly evident in the iPhone 17 and the AI servers released simultaneously.

– Value Enhancement: The value enhancement of PCBs in the iPhone 17 mainly comes from two aspects: one is the price increase brought by specification upgrades, such as the application of high-layer HDI boards and SLP (substrate-like PCB) high-end products; the other is the increase in usage, especially in lightweight styles, where flexible boards and rigid-flex boards are used more to save space. This trend forms a synergistic effect with the AI server market, with estimates from CICC indicating that the AI PCB market size is expected to reach 5.6/10 billion USD in 2025/2026. Although domestic PCB manufacturers are accelerating capacity expansion, the efficiency of releasing high-end capacity will still lag behind the growth rate of demand, leading to a persistent supply-demand gap.

– Technological-Driven Value Distribution: In the PCB industry value chain, the technological content has become a key factor determining the profitability of enterprises. For example, Taijun’s development of ultra-low loss materials and Metalink processes lays the technological foundation for high-speed transmission applications, allowing it to maintain a competitive advantage in the high-end flexible board field. Similarly, Huazhong’s technological accumulation in high-density interconnect boards has made it a stable supplier of core PCBs for the iPhone 17. This technological barrier allows leading enterprises to achieve profit margins higher than the industry average and promotes the transformation of the PCB industry from labor-intensive to technology-intensive.

– Importance of Upstream Materials: With the increasing performance requirements of PCBs, the importance of upstream materials in the supply chain has significantly increased. The supply capacity and technical level of key materials such as high-end substrate materials, low roughness copper foil, and low dielectric loss fiberglass cloth directly restrict the product performance and delivery capabilities of downstream PCBs. For example, with the intensification of high-speed transmission and skin effect, low roughness HVLP4 copper foil has become mainstream, but each increase in production capacity reduces supply by about half, leading to long-term supply tightness, and bargaining power gradually shifting from downstream complete machines back to upstream materials. This change in value distribution in the supply chain has been particularly evident in the PCB supply chain of the iPhone 17.

Overall, the release of the iPhone 17 has significantly raised the technical threshold and value proportion of the PCB industry, driving the upgrade and restructuring of the supply chain. In this process, leading enterprises with technological advantages, capacity scale, and diversified layout capabilities, such as Huazhong, Zhendin-KY, and Taijun, are better positioned to seize market opportunities and achieve a virtuous cycle of performance growth and technological upgrades.

3 Impact on Upstream Materials and Components

The release of the iPhone 17 series has not only had a direct impact on the PCB industry but has also profoundly affected its upstream materials and components supply chain. From exterior parts, structural components to electronic hardware, many links are facing new technical requirements and market opportunities, and the entire supply chain is undergoing active adjustments and upgrades.

3.1 Adjustments in the Exterior Parts Supply Chain

As the components most directly perceived by users, the iPhone 17 series has brought significant changes, especially in panel glass and body materials. These changes have had a noticeable impact on related supply chain companies.

– Upgrades in Cover Glass: A report from Bank of America indicates that the cover glass of the iPhone 17 Pro series has undergone significant upgrades, with average prices increasing by over 50%. This change has provided related suppliers such as Lens Technology with a good opportunity for product value enhancement. The upgrade of cover glass is not only reflected in price but also in material performance and processing technology. With the introduction of curved edge design and glass-metal splicing material processes in the iPhone 17 series, the cover glass needs to achieve a smoother transition with the metal frame, which raises higher requirements for the strength, light transmittance, and curvature accuracy of the glass. This trend allows suppliers with high-end glass processing capabilities to receive more orders and higher profit margins.

– Material Technology Barriers: In the glass material field, ultra-thin glass fiber cloth has become a key strategic material. As the internal structure of smartphones becomes increasingly precise, the requirements for thermal management and mechanical stability continue to rise, making low thermal expansion coefficient glass fiber cloth almost indispensable in smartphones. This material can match the thermal expansion characteristics between chips and substrates, avoiding structural damage caused by temperature changes, while also having low dielectric loss, reducing energy loss in signal transmission. Therefore, it is widely used in the packaging of key components such as SoC chips, RF packaging substrates, camera modules, and batteries, ensuring the high performance and stable operation of the iPhone.

– Highly Concentrated Supply Chain: The technological barriers for this ultra-thin glass fiber cloth are extremely high, and currently, only a few companies globally, such as Honghe Technology in Shanghai, China, and Asahi Kasei in Japan, can mass-produce 0.03mm ultra-thin cloth and have passed Apple’s MFi certification. This highly concentrated supply pattern poses supply chain risks for Apple during the production of the iPhone 17. Reports indicate that due to the lack of this key material, Apple CEO Tim Cook is extremely anxious about the production progress of the upcoming iPhone 17 series, pressuring suppliers almost daily to expedite supply. This situation also reflects the strategic position of upstream core materials in the manufacturing of smart devices.

3.2 Changes in the Structural Components Supply Chain

The iPhone 17 series has particularly significant changes in structural components, especially in the adjustment of mid-frame materials and upgrades to the cooling system, which have multifaceted impacts on the structural components supply chain.

– Mid-frame Material Adjustment: The iPhone 17 Pro and iPhone 17 Pro Max no longer use the titanium solution from the previous two generations but have chosen a 7000 series aerospace aluminum alloy mid-frame. This adjustment has increased the body weight by about 8g, but the structural strength has improved by 15%, significantly enhancing the product’s practicality. In terms of material properties, the 7000 series aerospace aluminum alloy is a super-hard aluminum alloy, with tensile strength and corrosion resistance superior to ordinary aluminum alloys, suitable for high-strength demand scenarios. Apple’s choice of this material is mainly due to considerations of weight reduction, cost, and environmental protection: aluminum alloy has a lower density than titanium, helping to reduce body weight; the processing difficulty is lower, with a high yield rate, which can reduce production costs; aluminum’s carbon footprint is 67% lower than that of titanium, aligning with Apple’s goal of achieving carbon neutrality across its entire value chain by 2030.

– Cooling System Upgrade: The iPhone 17 Pro series introduces a VC vapor chamber cooling solution for the first time. This change creates new market space for cooling structural component suppliers. Compared to traditional graphite sheets or copper tube cooling solutions, vapor chambers have higher thermal conductivity and more uniform heat distribution, better meeting the cooling demands in high-power scenarios such as 5G and AI computing. This upgrade benefits suppliers of cooling solutions such as AAC. At the same time, due to the superior thermal conductivity of aluminum alloy (237 W/m·K) compared to titanium (17 W/m·K), it theoretically aids in heat dissipation, but in actual design, it still needs to be used in conjunction with vapor chambers.

– Supply Chain Pattern Adjustment: The changes in structural component materials have directly led to adjustments in the supply chain pattern. A report from Bank of America indicates that BYD Electronics faces pressure due to the downgrade of its shell from titanium to aluminum alloy. This reflects the dynamic nature of Apple’s supply chain—upgrades or downgrades of components can have asymmetric impacts on different suppliers. On the other hand, manufacturers such as Lianyi Intelligent Manufacturing and AAC, which have thermal management technology reserves, are expected to gain new growth opportunities by providing vapor chambers and other cooling components to enter the smartphone cooling market.

Table 3: Major Changes in Structural Components of the iPhone 17 Series and Their Impact on the Supply Chain

3.3 Changes in the Electronic Hardware Supply Chain

The hardware upgrades of the iPhone 17 series have also significantly impacted the electronic hardware supply chain, particularly in the fields of camera modules, acoustic components, and chip packaging.

– Camera Module Upgrades: The iPhone 17 Pro series has achieved significant upgrades in its imaging system, adopting a periscope lens, with the front camera upgraded to 48 million pixels, and the rear main camera reaching 24 million pixels. This upgrade has increased the average selling price of image sensors, modules, and lenses, benefiting optical component suppliers such as Cowell and Largan. In particular, Largan, as a core supplier of lenses for Apple, is expected to continue benefiting from lens specification upgrades in the coming product cycles. At the same time, Yujingguang is also favored by the market due to its diversified product portfolio, covering smart glasses, smart home, and new lens orders from American cloud service providers.

– Acoustic and Haptic Components: The iPhone 17 series has also seen upgrades in acoustic components, with the penetration rate of 68-70 decibel microphones increasing. This change benefits acoustic component suppliers such as AAC. At the same time, to achieve a thinner design, the design of camera, acoustic, and haptic components has become more compact, raising higher requirements for internal space utilization. This trend towards compact design requires electronic hardware suppliers to achieve the same or higher performance in smaller spaces, driving the development of miniaturized packaging technology and high-density integration technology.

– Changes in Chip Packaging Demand: With the improvement in processing performance of the iPhone 17, the requirements for chip packaging have also increased accordingly. In particular, the introduction of AI computing power has increased chip power consumption and heat generation, necessitating more advanced packaging technologies and cooling solutions. In this field, ultra-thin glass fiber cloth has become a key material for chip packaging due to its low thermal expansion coefficient and low dielectric loss characteristics. It can match the thermal expansion characteristics between chips and substrates, avoiding structural damage caused by temperature changes while reducing energy loss in signal transmission, ensuring the stable operation of high-performance chips. This demand further strengthens the strategic position of upstream high-end electronic fabric suppliers.

Overall, the release of the iPhone 17 series has driven technological upgrades and value restructuring in the upstream materials and components supply chain. In this process, suppliers with high-end material R&D capabilities, precision processing technologies, and diversified product layouts are better able to adapt to market changes and gain sustained growth momentum. At the same time, the strategic importance of the upstream supply chain has further highlighted, especially the stability and technological advancement of key material supplies, which directly affect the operational efficiency and competitiveness of the entire supply chain.

4、Impact on Midstream Manufacturing and Downstream OEM

The release of the iPhone 17 series has also had a profound impact on midstream manufacturing and downstream OEM processes, bringing new challenges and opportunities in capacity adjustments, technological upgrades, and supply chain management. This segment, as a key hub connecting upstream components and downstream brands, reflects the operational status and development trends of the entire supply chain.

4.1 Capacity Adjustments and Operational Strategies of OEMs

As the iPhone 17 series enters large-scale production in the second half of 2025, OEMs face multiple tasks of capacity adjustments, labor allocation, and quality control. The operational status of these factories directly relates to the market supply situation of the iPhone 17 series.

– Capacity Fluctuation Management: Historically, Apple’s supply chain typically experiences a capacity ramp-up phase before new product launches, but the situation for the iPhone 17 series is slightly different. In July and August 2025, Apple’s procurement of iPhone 17 components was relatively calm, leading to revenue declines for Apple supply chain manufacturers such as Huazhong, Zhendin-KY, Jingji, and Largan compared to the same period in 2024. However, starting in September, Apple’s attitude towards iPhone 17 component procurement became “bold and proactive,” with the first wave of component shipments peaking at the end of September. This front-low and back-high demand rhythm places higher demands on the flexibility of OEMs’ capacities, requiring them to quickly respond to fluctuations in production volume.

– Diversification Strategies in Supply Chain: To cope with geopolitical risks and cost pressures, Apple’s supply chain is accelerating its global layout. This trend is particularly evident in the PCB industry. Huazhong has initiated mass production at its new factory in Thailand to diversify risks and explore new markets. Zhendin-KY plans to invest 30 billion yuan in capital expenditures from 2025 to 2026 to increase capacity in Thailand, Huai’an, and Taiwan. This diversification of capacity layout is not only to cope with trade frictions but also based on comprehensive considerations of cost optimization and market expansion. Thailand, in particular, is becoming an increasingly popular choice for many Apple supply chain manufacturers due to its infrastructure in electronic manufacturing and relatively low labor costs.

– Capital Expenditure Strategies: In response to the market opportunities brought by the iPhone 17, major OEMs are increasing their capital expenditures. Zhendin-KY’s large-scale investment plan is a typical example, with a capital expenditure scale of 30 billion yuan per year from 2025 to 2026, which is quite rare in the PCB industry. These investments are mainly used to expand capacity in Thailand, Huai’an, and Taiwan, focusing on AI servers and high-end PCB applications. This large-scale investment reflects the optimistic judgment of leading OEMs about market prospects and demonstrates the strategic intent of leading enterprises to strengthen competitive advantages through counter-cyclical investments during technological upgrade cycles.

4.2 Manufacturing Technology Challenges and Upgrades

The product innovations of the iPhone 17 series have raised higher technical requirements for midstream manufacturing, particularly in precision processing, quality control, and process innovation.

– New Material Processing Challenges: The new materials and processes adopted in the iPhone 17 series pose new challenges for manufacturing. For example, the 7000 series aerospace aluminum alloy mid-frame used in the Pro series, while easier to process than titanium, still requires precise CNC processing and surface treatment technologies to ensure structural strength and aesthetic quality. At the same time, the glass and metal splicing material process introduced in the iPhone 17 series requires OEMs to develop new processing technologies and testing standards to ensure smooth transitions between different materials, maintaining consistent quality and aesthetics.

– Technological Upgrade Requirements: As the internal structure of the iPhone 17 becomes increasingly complex, the requirements for manufacturing precision continue to rise. For PCBs, the high-end HDI boards and rigid-flex boards used in the iPhone 17 impose stricter requirements on lamination alignment accuracy, line width, and spacing control. At the same time, to meet the demands of high-speed signal transmission, impedance control for PCBs needs to be more precise, which brings new challenges to material properties, etching precision, and surface treatment processes during manufacturing. These technical requirements drive technological upgrades in the manufacturing segment, requiring OEMs to continuously update equipment, optimize processes, and enhance employee training to meet the increasingly high manufacturing standards.

– Cooling System Integration Challenges: The VC vapor chamber cooling solution introduced for the first time in the iPhone 17 Pro series faces integration challenges with the mainboard, shell, and other components during manufacturing. The vapor chamber needs to make full contact with the chip surface to ensure thermal efficiency while not causing mechanical stress or short-circuit risks to other components. This precision assembly requires OEMs to develop new fixtures and installation processes and provide specialized training for employees. Additionally, reliability and durability testing for vapor chambers also requires the establishment of new standards and methods, increasing the complexity of the manufacturing segment and the difficulty of quality control.

4.3 Supply Chain Collaboration and Risk Management

The production of the iPhone 17 series involves hundreds of suppliers globally, and how to achieve efficient collaboration and risk management in the supply chain has become an important issue for OEMs and Apple.

– Addressing Supply Chain Bottlenecks: The key material shortages faced during the production of the iPhone 17 highlight the vulnerability of the supply chain. Reports indicate that due to the lack of key materials such as low thermal expansion coefficient glass fiber cloth, Apple CEO Tim Cook is extremely anxious about the production progress of the iPhone 17 series, pressuring suppliers almost daily to expedite supply. This shortage of key materials could lead to interruptions in the entire production process, posing extremely high demands on supply chain management. To address this challenge, Apple and its OEMs need to establish closer cooperative relationships with key material suppliers, even considering direct investments or supporting multiple suppliers to ensure stable material supplies.

– Inventory Management Strategies: The front-low and back-high demand characteristics exhibited by the iPhone 17 supply chain place higher demands on inventory management. OEMs need to reasonably plan raw material inventory during the uncertain initial stages of demand, avoiding excessive inventory that occupies funds while also preventing production delays due to insufficient inventory. This balance requires accurate demand forecasting and flexible supply chain coordination capabilities. As sales data accumulates and market feedback becomes clear, the supply chain needs to have rapid response capabilities to adjust production plans in a timely manner to match changes in market demand.

– Quality Control Systems: With the increasing complexity of the iPhone 17 series, the importance of quality control has further highlighted. This requires OEMs to establish stricter quality inspection systems and more comprehensive traceability mechanisms. For PCBs, the introduction of high-frequency via simulation technology allows engineers to predict actual via performance before manufacturing, reducing development time and minimizing costly prototype iterations. This close collaboration between design and manufacturing segments is crucial for ensuring consistency and reliability in mass production. OEMs need to share more production data with Apple, establishing real-time monitoring and feedback mechanisms to promptly identify and resolve quality issues during the production process.

Overall, the release of the iPhone 17 series has brought multiple challenges in capacity adjustments, technological upgrades, and supply chain management to midstream manufacturing and downstream OEM processes. In this process, OEMs with strong technical capabilities, efficient operational management, and global layouts are better able to adapt to market changes and gain competitive advantages. At the same time, collaboration and innovation between manufacturing, design, and materials segments are becoming increasingly important; only by establishing close cooperation mechanisms in the supply chain can they meet the increasingly complex challenges of product manufacturing.

5、Strategic Responses and Future Directions of the Supply Chain

In response to the market changes and technological challenges brought by the release of the iPhone 17, PCB upstream and downstream supply chain enterprises need to formulate targeted development strategies, making adjustments in technology layout, capacity planning, and supply chain collaboration to seize new opportunities and address new challenges. This section will comprehensively analyze the response strategies and development directions of various segments of the supply chain.

5.1 Collaborative Innovation Across Supply Chain Segments

In the context of increasingly complex electronic products, collaborative innovation between upstream and downstream supply chains has become particularly important. The technological upgrades of the iPhone 17 series require close cooperation between material suppliers, component manufacturers, OEMs, and brand owners to achieve seamless transitions from design to mass production.

– Deep Integration of Design and Manufacturing: In the face of the performance requirements of the iPhone 17 series for PCBs, the collaboration between design and manufacturing segments is crucial. The high-frequency via simulation technology launched by OKI Circuit Technology represents this trend, allowing engineers to predict actual via performance by integrating high-precision manufacturing data, 3D electromagnetic field analysis, and production design optimization before manufacturing. This design-manufacturing integration approach can significantly reduce development time, minimize costly prototype iterations, and ensure consistent signal quality in mass production. For PCB suppliers, actively participating in the design phase of customers and providing manufacturability design and process capability consulting has become a key means of enhancing competitiveness.

– Joint Development of Materials and Applications: The various new materials used in the iPhone 17 series, such as 7000 series aerospace aluminum alloy and low thermal expansion coefficient glass fiber cloth, require close cooperation between material suppliers and application manufacturers. This cooperation extends not only to product customization but also to fundamental research. For example, to meet the high requirements of AI servers for PCB performance, upstream and downstream of the supply chain are jointly promoting breakthroughs in materials, including the development and application of new materials such as M9, PTFE, and quartz cloth. Japan’s Nittobo has invested 15 billion yen to expand the production of T-glass, which is expected to achieve mass production by the end of 2026, tripling its current capacity, reflecting the enormous potential of the high-end PCB materials market.

– Cross-Industry Technology Integration: The technological innovation of the PCB industry chain increasingly relies on the integration of knowledge across industries. From the cable-free architecture of AI servers to the VC vapor chamber cooling technology in smartphones, and from low-orbit satellite communication to high-speed computing, technologies from different application fields are accelerating their cross-integration. For PCB companies, it is necessary to have the ability to integrate multi-field technologies, organically combining the technical standards, process requirements, and performance indicators of different industries to form innovative solutions. For example, Taijun’s gradual entry into server cabinet short-distance cable replacement solutions from the high-end flexible board processing capability in the smartphone field is a typical case of cross-industry technology application.

5.2 Technological Development Paths and Capacity Layout

In the face of market opportunities brought by the iPhone 17, the PCB industry chain needs to clarify technological development paths and optimize capacity layouts to maintain a leading position in fierce market competition.

– Dual-Track Technological Development: Leading PCB companies are adopting a “mobile + AI” dual-track development strategy. On one hand, they continue to deepen their focus on the smartphone market, seizing the technological upgrade opportunities brought by flagship products like the iPhone 17; on the other hand, they actively layout emerging fields such as AI servers and high-speed computing to lay the foundation for future growth. Zhendin-KY has clearly formed a dual-axis pattern of “mobile + AI”; Huazhong continues to expand its low-orbit satellite and high-end server motherboard business; Taijun possesses 10-20 layer high-end flexible board processing capabilities, gradually entering server cabinet short-distance cable replacement solutions. This dual-track development strategy helps enterprises balance short-term performance and long-term development, reducing dependence on a single product and enhancing risk resistance capabilities.

– Globalization of Capacity Layout: With the increasing uncertainty in the global trade environment, the globalization of capacity layout has become an important strategy for the PCB industry chain. Huazhong has initiated mass production at its new factory in Thailand, and Zhendin-KY is increasing capacity in Thailand, Huai’an, and Taiwan, reflecting this trend. Southeast Asia, especially Thailand, is becoming an important destination for the transfer of the PCB industry due to its good electronic manufacturing infrastructure, relatively low labor and land costs, and relatively neutral international political stance. This globalization of capacity layout not only helps to avoid trade barriers but also allows for closer proximity to regional markets, reducing logistics costs and time.

– Continuous Expansion of High-End Capacity: Although the overall PCB capacity is showing a surplus, high-end capacity remains in short supply. Reports from CICC indicate that although domestic PCB manufacturers are accelerating capacity expansion, the efficiency of releasing high-end capacity will still lag behind the growth rate of demand, leading to a persistent supply-demand gap. In response to this market opportunity, leading PCB companies are increasing their investments in high-end capacity. Zhendin-KY plans to invest 30 billion yuan in capital expenditures from 2025 to 2026, targeting the growth potential of the high-end PCB market. These investments are mainly focused on high-layer HDI boards, high-speed materials PCBs, and IC substrates, which have high technical barriers and profit margins, representing the main direction of PCB industry upgrades.Table 4: Technical Layout and Capacity Planning of Major PCB Industry Chain Enterprises

5.3 Sustainable Development and Supply Chain Security

In addition to addressing technological challenges, the PCB industry chain also needs to focus on strategic issues such as sustainable development and supply chain security, which are increasingly becoming important components of long-term competitiveness for enterprises.

– Green Manufacturing and Circular Economy: The iPhone 17 series reflects a focus on environmental considerations in material selection. The Pro series has switched from titanium to 7000 series aerospace aluminum alloy, one important reason being that aluminum’s carbon footprint is 67% lower than that of titanium, aligning with Apple’s goal of achieving carbon neutrality across its entire value chain by 2030. This trend requires supply chain enterprises to accelerate the promotion of green manufacturing and circular economy practices. Specific measures include: adopting environmentally friendly materials and processes, reducing energy consumption and waste generation; promoting water resource recycling and waste resource utilization; using renewable energy to reduce carbon emissions. These environmental measures are not only to meet the requirements of brands like Apple but also an inevitable choice for enterprises to fulfill social responsibilities and achieve sustainable development.

– Supply Chain Security and Resilience: The key material shortages faced during the production of the iPhone 17 highlight the importance of supply chain security. To address this challenge, industry chain enterprises need to take multiple measures: first, strengthen supply chain mapping for key materials to identify potential risk points; second, establish strategic partnerships with key suppliers to ensure priority supply; third, consider diversified procurement strategies to reduce dependence on a single supplier or region; fourth, establish safety stock to buffer against supply fluctuations. In these areas, Apple is actively restructuring its supply chain, but this may lead to significant cost increases, making the iPhone 17 the most expensive iPhone series ever.

– Talent and Innovation System Construction: In the face of rapidly changing market environments, talent and innovation system construction has become a core strategy for PCB industry chain enterprises. Companies need to attract and cultivate technical talents with interdisciplinary knowledge, establishing organizational capabilities for continuous learning and technological updates. At the same time, they need to build an open innovation system, integrating internal and external R&D resources, establishing close cooperation with universities and research institutions, and participating in industry technology alliances and standard-setting. For example, OKI Circuit Technology has addressed key challenges in high-speed PCB design through the development of high-frequency via simulation technology, which requires a solid theoretical foundation and years of technical accumulation, reflecting the importance of talent and innovation systems.

Overall, the release of the iPhone 17 series has driven comprehensive upgrades and strategic adjustments in the PCB industry chain. Enterprises need to formulate response strategies from multiple dimensions, including technology layout, capacity planning, supply chain collaboration, sustainable development, and innovation systems, to maintain competitive advantages in a changing market environment. With the rapid development of emerging applications such as AI and high-speed computing, the PCB industry chain is ushering in a new growth cycle, and those enterprises that can grasp technological trends and optimize resource allocation are expected to stand out in competition and share in market growth dividends.

6、Summary and Future Outlook

The release of the iPhone 17 series is not only the launch of a new product but also an important sign of technological evolution and pattern changes in the entire consumer electronics industry chain. Through the in-depth analysis of various segments of the industry chain in the previous sections, we can clearly see the multidimensional impact of the iPhone 17 on the upstream and downstream supply chains of PCBs and the response strategies of each segment. Based on this, this section will summarize the overall impact and forecast future development trends.

6.1 The Restructuring Role of iPhone 17 on the PCB Industry Chain

The technological innovations and design changes of the iPhone 17 series have had a profound restructuring effect on the PCB industry chain, which is reflected in both technological and industrial pattern and value distribution.

– Shift in Technological Orientation: The iPhone 17 series has pushed the PCB industry into the “three high era” of high frequency, high power, and high density. To meet the demands of AI computing power and high-speed transmission, PCBs are no longer just circuit carriers but have become the core link in releasing computing power. This shift requires comprehensive upgrades in design concepts, material selection, and manufacturing processes for PCBs. For example, to address the challenges of high-speed signal transmission, OKI Circuit Technology’s development of high-frequency via simulation technology allows engineers to predict actual via performance before fabrication; to meet cooling demands, the iPhone 17 Pro series introduces vapor chambers; to improve integration, the application of high-layer HDI boards and rigid-flex boards has become more widespread. These technological innovations collectively push the technical boundaries of the PCB industry to higher levels.

– Reconstruction of Value Distribution: The technological upgrades of the iPhone 17 series have led to a reconstruction of value distribution in the PCB industry chain. On one hand, high-end material suppliers capable of mass-producing ultra-thin glass fiber cloth, such as Honghe Technology and Asahi Kasei, and those producing T-glass, such as Japan’s Nittobo, occupy more favorable positions in the value chain due to high technological barriers and favorable competitive patterns. On the other hand, PCB manufacturing enterprises with technological advantages and scale effects, such as Huazhong, Zhendin-KY, and Taijun, have achieved revenue and profit growth through high-end products and advanced processing capabilities. In contrast, traditional low-end PCB capacities face increasing competitive pressure and profit margin squeeze. This change in value distribution encourages enterprises to increase R&D investment and transition to high-tech, high-value-added segments.

– Evolution of the Industry Ecosystem: The production and manufacturing of the iPhone 17 series show a trend of increasingly close collaboration within the industry chain. From joint development of materials, early participation in design, to real-time optimization of manufacturing processes, cooperation among various segments of the industry chain has become deeper and broader. For example, Apple and suppliers jointly address key material shortages, PCB manufacturers collaborate with equipment suppliers to develop high-frequency via simulation technology, and OEMs and brand owners optimize global capacity layouts together. This close collaboration improves the overall efficiency and innovation capability of the industry chain, raising the competitive threshold and shifting competition from individual enterprises to ecosystems.

6.2 Future Development Trends and Opportunities and Challenges

Based on the changes and impacts brought by the iPhone 17, we can anticipate future development trends in the PCB industry chain, identifying opportunities and challenges to provide references for strategic decision-making by industry chain enterprises.

– Accelerated Technology Integration: In the future, the development of the PCB industry chain will increasingly rely on the integration of multiple technology fields. From smartphones to AI servers, from low-orbit satellites to high-speed computing, technologies from different application fields will accelerate their cross-integration. For example, the cable-free architecture of the Rubin platform and the ASIC high HDI layer architecture are driving the PCB industry to become the core of computing power; the VC vapor chamber technology in smartphones may borrow from AI server cooling solutions; high-end flexible board processing capabilities can be used in both smartphones and gradually enter server cabinet short-distance cable replacement solutions. This technological integration brings broader market space for enterprises and requires them to possess cross-field technology integration capabilities.

– Reconstruction of Market Patterns: With technological upgrades and capacity adjustments, the market pattern of the PCB industry will face reconstruction. On one hand, leading enterprises are further strengthening their competitive advantages through large-scale capital expenditures and technological investments, such as Zhendin-KY planning to invest 30 billion yuan in capital expenditures from 2025 to 2026; on the other hand, specialized enterprises are establishing differentiated competitive advantages by deeply cultivating niche markets, such as Taijun focusing on 10-20 layer high-end flexible board processing capabilities. Meanwhile, upstream material suppliers, due to high technological barriers and large investment scales, are gradually enhancing their bargaining power, such as low roughness HVLP4 copper foil, where each increase in production capacity reduces supply by about half, leading to long-term supply tightness and gradually shifting bargaining power back to upstream materials. This change in pattern requires industry chain enterprises to clarify their positioning and formulate differentiated development strategies.

– Sustainable Development and Supply Chain Security Become Key Issues: In addition to technological and market factors, sustainable development and supply chain security will become key issues affecting the future development of the PCB industry chain. One important reason for Apple’s choice of 7000 series aerospace aluminum alloy is that aluminum’s carbon footprint is 67% lower than that of titanium, aligning with Apple’s goal of achieving carbon neutrality across its entire value chain by 2030. This trend requires supply chain enterprises to accelerate the promotion of green manufacturing and circular economy practices. At the same time, the key material shortages faced during the production of the iPhone 17 highlight the importance of supply chain security. In the future, enterprises need to seek a balance between efficiency and security, cost and resilience, establishing a more robust and sustainable supply chain system.

Looking ahead, with the rapid development of new technologies such as AI, IoT, and autonomous driving, the PCB industry chain is ushering in a new growth cycle. Reports from CICC suggest that AI computing power will drive simultaneous increases in both volume and price for PCBs, with the market size expected to continue expanding, and the AI PCB market size is expected to reach 5.6/10 billion USD in 2025/2026. This trend provides broad development space for PCB industry chain enterprises with technological advantages, capacity scale, and global layouts. At the same time, technological innovation, industry upgrades, and pattern reconstruction will also bring new challenges. Only those enterprises that can grasp technological trends, optimize resource allocation, and establish collaborative advantages can maintain competitive advantages and achieve sustainable development in a changing market environment.

The release of the iPhone 17 series marks a new development stage for the electronic industry chain. From material innovation to product design, from manufacturing processes to supply chain collaboration, various advancements have collectively driven the technological upgrades and value enhancement of the entire industry. In this process, PCBs, as core components of electronic products, have further highlighted their importance, expanding from traditional connectors to functional and structural components, becoming key links in releasing computing power and achieving innovation. With continuous technological advancements and an expanding market, the PCB industry chain is expected to usher in a broader development prospect.

Thank you for your attention and reading! Let’s make progress every day…Images & videos in this article are sourced from the internet or AI generation; please verify, and if there are any copyright issues, contact for removal!~ Some information is sourced from publicly available information on the internet, please delete if infringing ~

Thank you for your attention and reading! Let’s make progress every day…Images & videos in this article are sourced from the internet or AI generation; please verify, and if there are any copyright issues, contact for removal!~ Some information is sourced from publicly available information on the internet, please delete if infringing ~