Warm reminder: This analytical article is for learning and reference purposes only and does not constitute investment advice.

1. Northern Huachuang: As a benchmark platform in the domestic semiconductor equipment field, the company is the only enterprise to achieve full coverage of the four core equipment categories: etching, thin film deposition, cleaning, and oxidation diffusion. Among its core products, the PVD (Physical Vapor Deposition) equipment has surpassed the 28nm metal gate process and achieved mass production, successfully filling the domestic technology gap, and has now stably entered the core production lines of leading wafer fabs such as Yangtze Memory Technologies and SMIC.

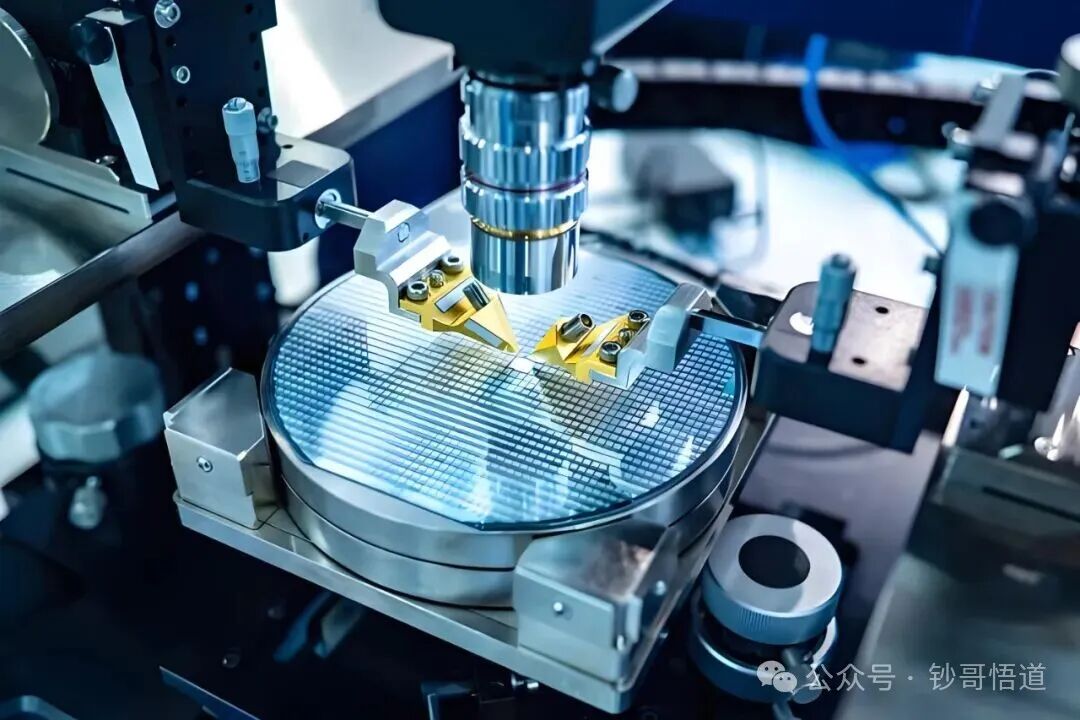

2. Zhongwei Company: Dominating the etching equipment sector, it is the only domestic company to achieve mass production of 5nm etching equipment, with etching precision reaching 100 picometers—equivalent to one-third of the diameter of a human hair. The market share has shown remarkable performance, with the domestic market share of CCP etching equipment soaring from 25% in 2022 to 60% in 2023, and the market share of ICP equipment reaching as high as 75%. Additionally, it has become the only certified domestic etching machine supplier for TSMC, with its technology level on par with global leader Lam Research, maintaining a global market share ranking of fourth.

3. Huahai Qingke: A key enterprise breaking the monopoly of foreign manufacturers in the CMP (Chemical Mechanical Polishing) equipment field, it is also the only domestic manufacturer to achieve mass production of 12-inch CMP equipment. The CMP process is a core step in chip manufacturing for achieving “surface flattening,” with extremely high technical barriers. The company’s equipment is compatible with advanced processes of 28nm and above, directly meeting the mass production needs of mainstream wafer fabs such as SMIC and Yangtze Memory Technologies.

4. Shengmei Shanghai: Demonstrating unique competitiveness in the global cleaning equipment field, it is the only company to achieve mass production of both megasonic cleaning equipment and single-wafer slot-type combination cleaning equipment, with its technical strength recognized by leading manufacturers such as TSMC and SMIC. Its cleaning equipment spans the entire chip manufacturing process and has environmental advantages—reducing the use of chemical reagents through process optimization, precisely aligning with the current trend of green development in the semiconductor industry.

5. Hu Silicon Industry: A “disruptor” in the domestic silicon wafer field, it is the only 300mm silicon wafer supplier certified by international mainstream wafer fabs, with products successfully integrated into the supply chain systems of companies like TSMC and Hua Hong. As the mainstream substrate for global chip manufacturing, the company’s certification breakthrough signifies that the quality of domestic silicon wafers has officially reached international standards, completely breaking the long-standing monopoly of Japan’s Shin-Etsu Chemical and SUMCO in the global market.

6. SMIC: The “ballast stone” in the domestic wafer foundry field, it is also the only local company to achieve mass production of 14nm FinFET technology, providing critical manufacturing support for domestic chip design leaders such as Huawei HiSilicon and Zhaoyi Innovation. In the first half of 2025, the performance was strong, with revenue reaching $4.456 billion, a year-on-year increase of 22%, and net profit growth as high as 35.6%, with capacity utilization consistently exceeding 100%. On the technology front, the yield of the 14nm process has stabilized at over 90%, narrowing the technology gap with industry leader TSMC to 2-3 years.

7. Huada Jiutian: A core enterprise solving the “bottleneck” problem of EDA tools, it is the only domestic EDA tool supplier covering the entire process of analog/RF circuit, successfully breaking the monopoly of the two giants Cadence and Synopsys. EDA tools are known as the “mother of chips,” and the toolchain built by the company achieves full-process autonomy from front-end design to back-end verification, currently deeply serving mainstream wafer fabs such as SMIC and Hua Hong, highlighting its strategic value.

8. Changdian Technology: Holding a significant position in the advanced packaging field, it is the only company to achieve mass production of 4nm Chiplet packaging, with technology widely applied in high-end fields such as AI chips and server chips. Chiplet technology significantly enhances chip performance and integration by “stitching together” chips with different functions into a system-level chip, and the company’s 4nm packaging yield has exceeded 99%, with its technology level on par with international giants like TSMC and Intel.

9. Huicheng Co., Ltd: A “specialized and innovative” small giant in the display driver packaging and testing field, it is also the only company to achieve mass production of 12-inch wafers in display driver packaging and testing, with core competitiveness in mastering key technologies for gold bump manufacturing. Its developed photomask coating equipment can support 28nm processes, with optical precision reaching sub-micron levels, not only meeting its own production needs but also directly participating in the localization process of core components for lithography machines.

Risk Warning:All content in this article is based on personal research and does not constitute a basis for others’ operations. The companies mentioned are based on static analysis of the industry and company fundamentals, not dynamic trading guidance. The stock market has risks, and investment should be cautious.