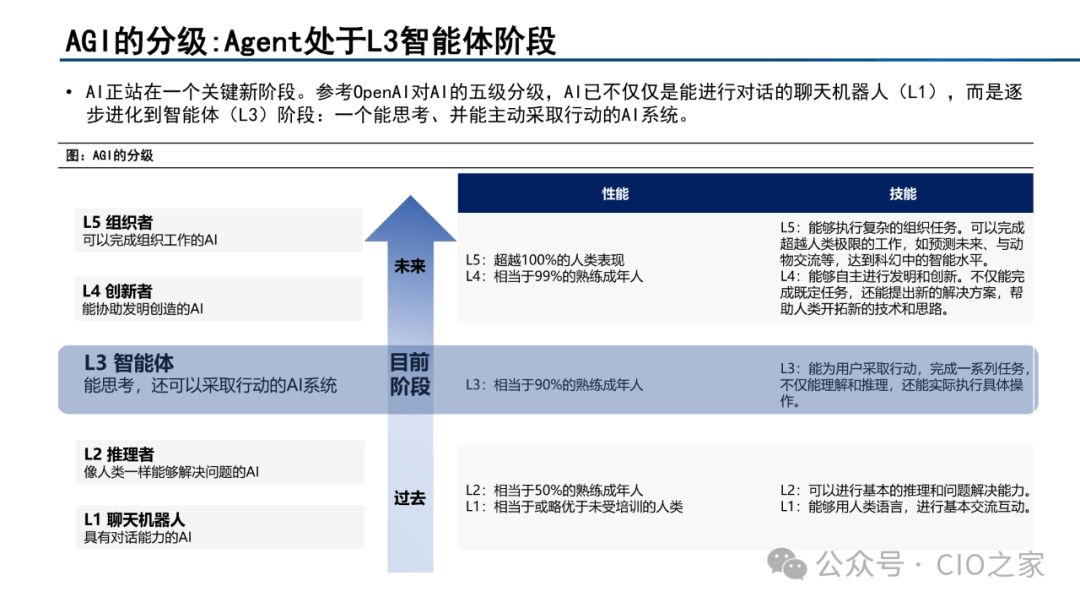

The AI Agent is gradually becoming the core direction of artificial intelligence development. Unlike traditional LLMs and automation, Agents possess “agency,” enabling them to actively perceive their environment, autonomously plan, and execute complex tasks, which is seen as a key milestone towards AGI.

Core Features of AI Agents

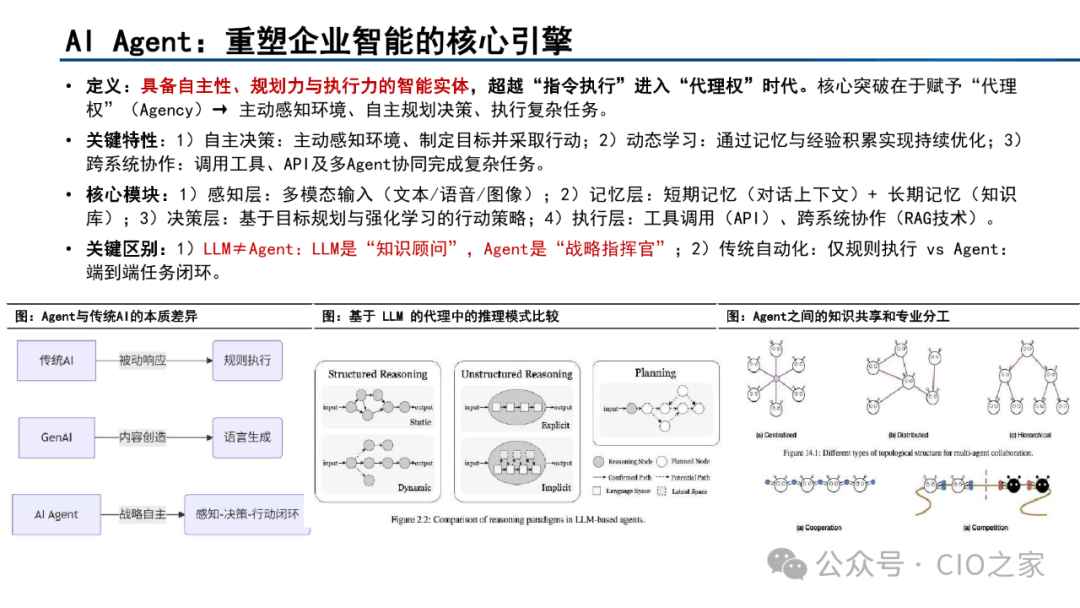

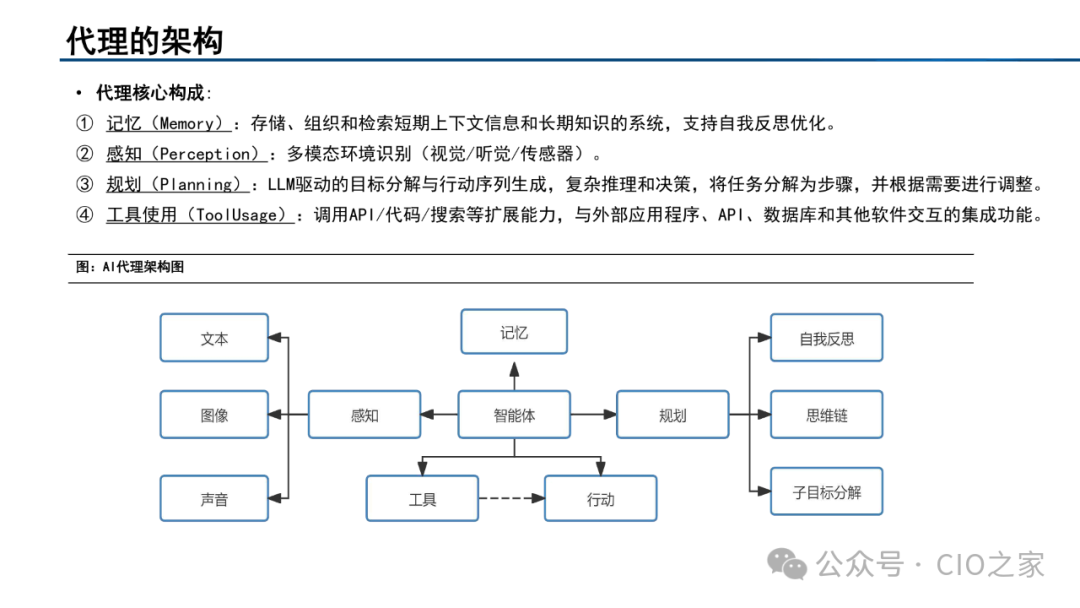

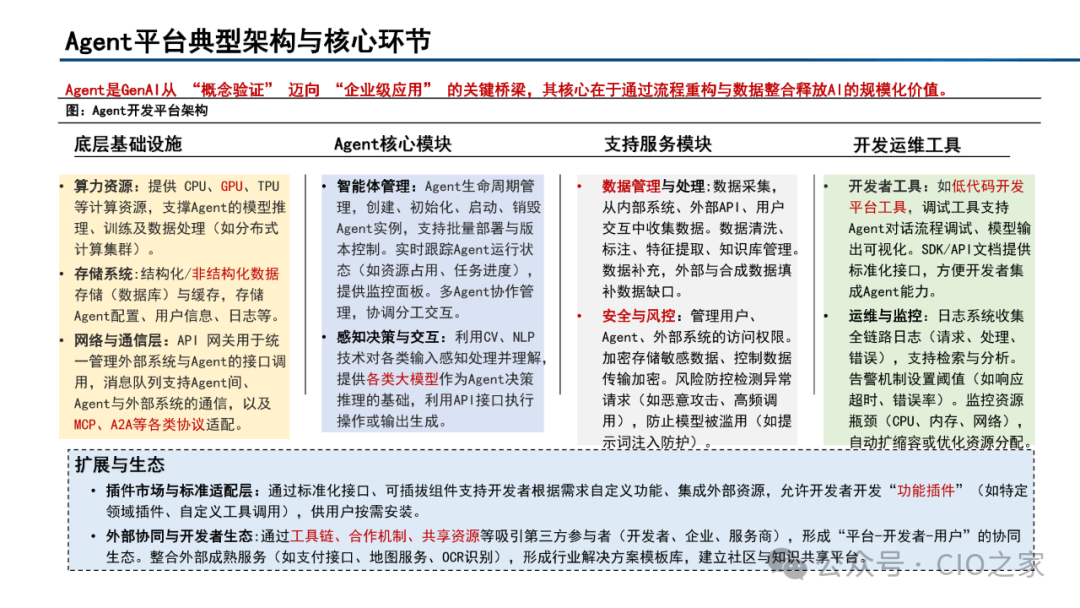

The essence of an Agent lies in its “proactivity.” It is not just a conversational assistant but also a “strategic commander” capable of completing end-to-end task loops. Its key capabilities include: autonomous decision-making, dynamic learning, and cross-system collaboration. The underlying architecture consists of four major modules: perception (multimodal input), memory (short-term and long-term storage), planning (goal decomposition and reinforcement learning), and execution (API calls and cross-system collaboration). This architecture allows the Agent to continuously evolve and optimize in complex scenarios.

Platforms and Ecosystems: Competition Between Giants and Domestic Manufacturers

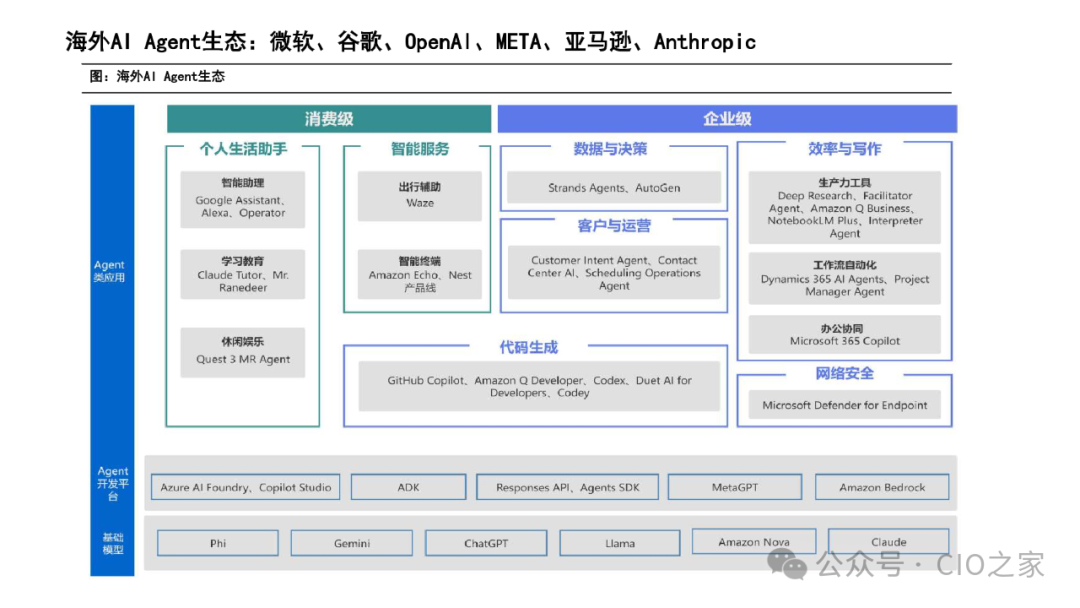

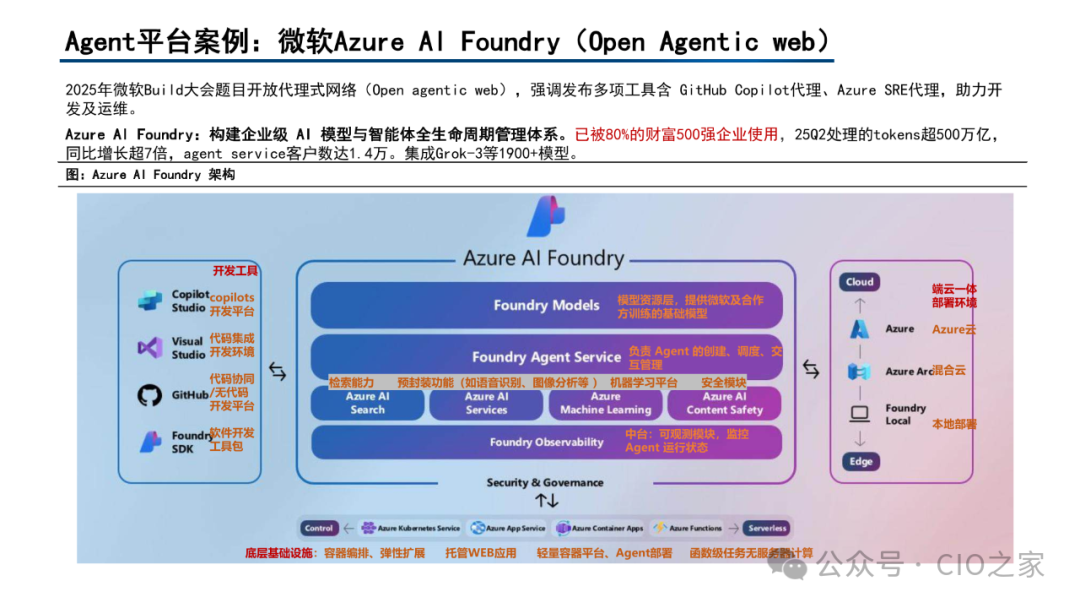

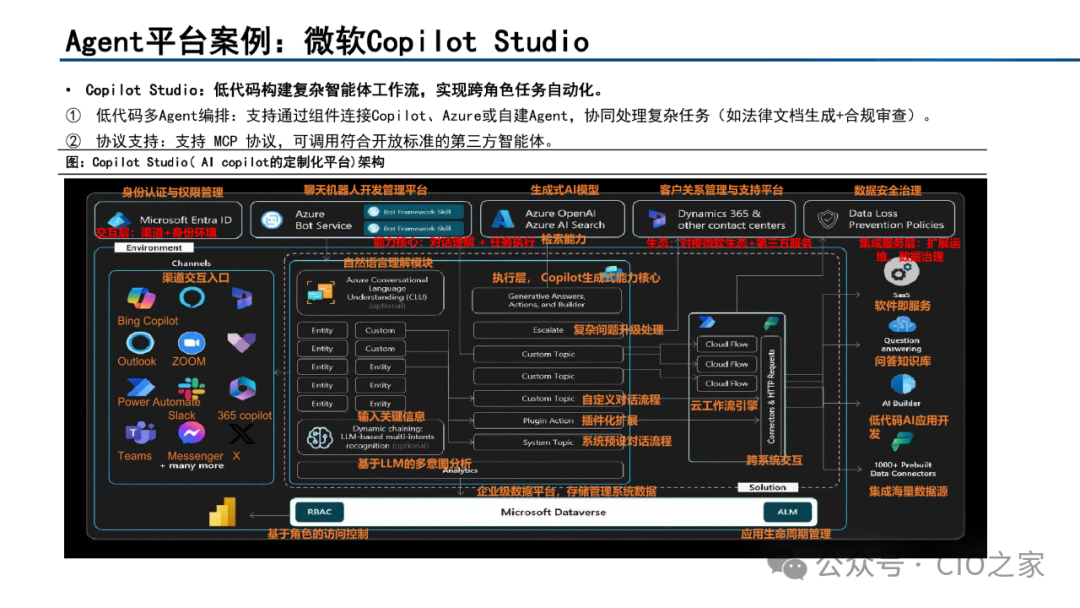

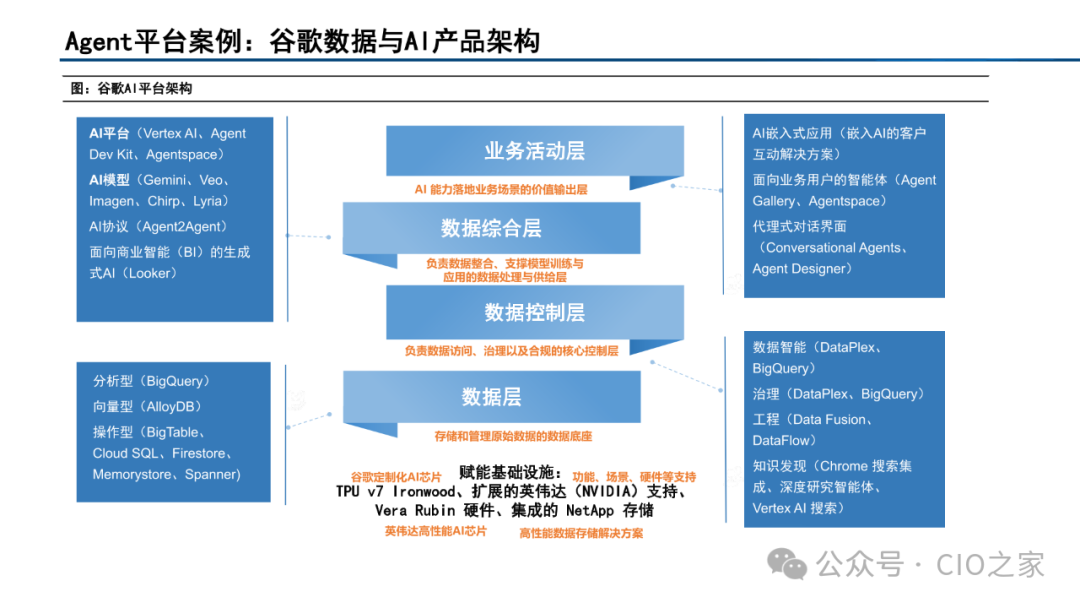

At the development platform level, overseas manufacturers have formed a differentiated landscape. Microsoft relies on Azure AI Foundry to build an enterprise-level full lifecycle management system, penetrating mainstream application scenarios of Fortune 500 companies with the most comprehensive model support and ecosystem integration capabilities. Google, on the other hand, maintains a lead in long context and multimodal capabilities with its Gemini series, but its ecosystem activity is relatively low; Amazon focuses more on computing power sales and convenient deployment, targeting the small and medium-sized enterprise market.

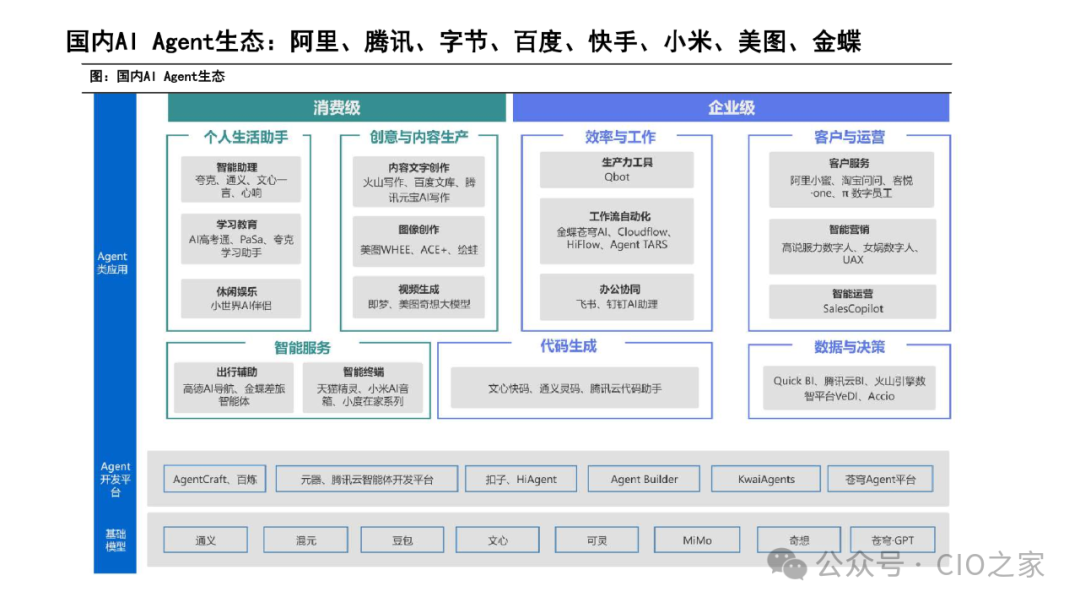

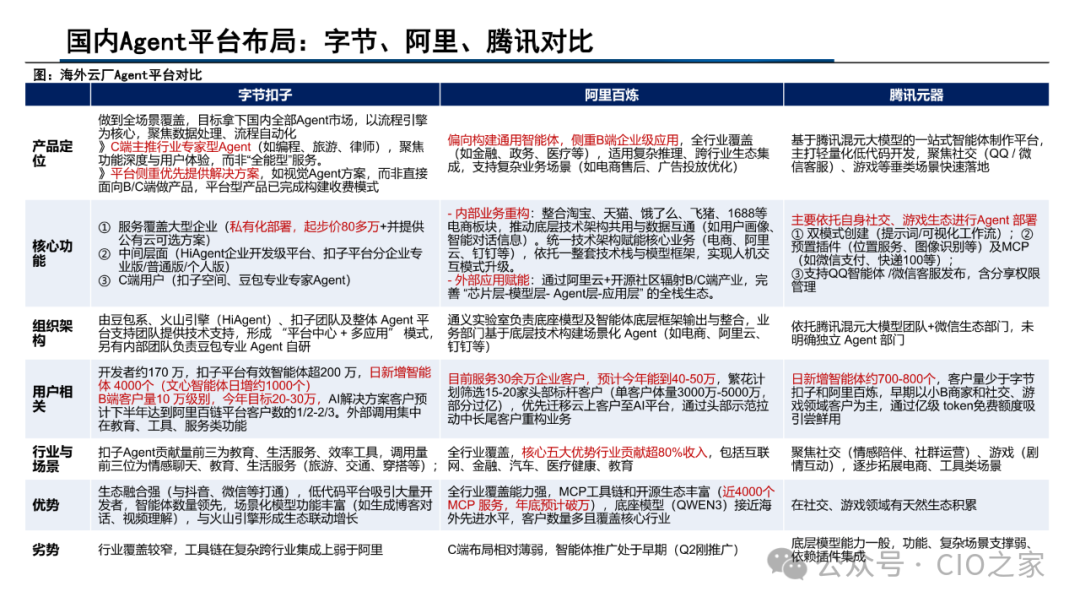

Domestically, ByteDance’s “Kouzi” platform leads in the number of intelligent agents, covering multiple scenarios for both C/B ends; Alibaba’s “Bailian” focuses on enterprise-level customers, building a full-stack ecosystem; Tencent’s “Yuanshi” targets lightweight implementations in social and gaming scenarios. Overall, domestic players pay more attention to industry scenarioization and ecosystem penetration.

Models and Inference: Rapid Evolution Driven by Computing Power

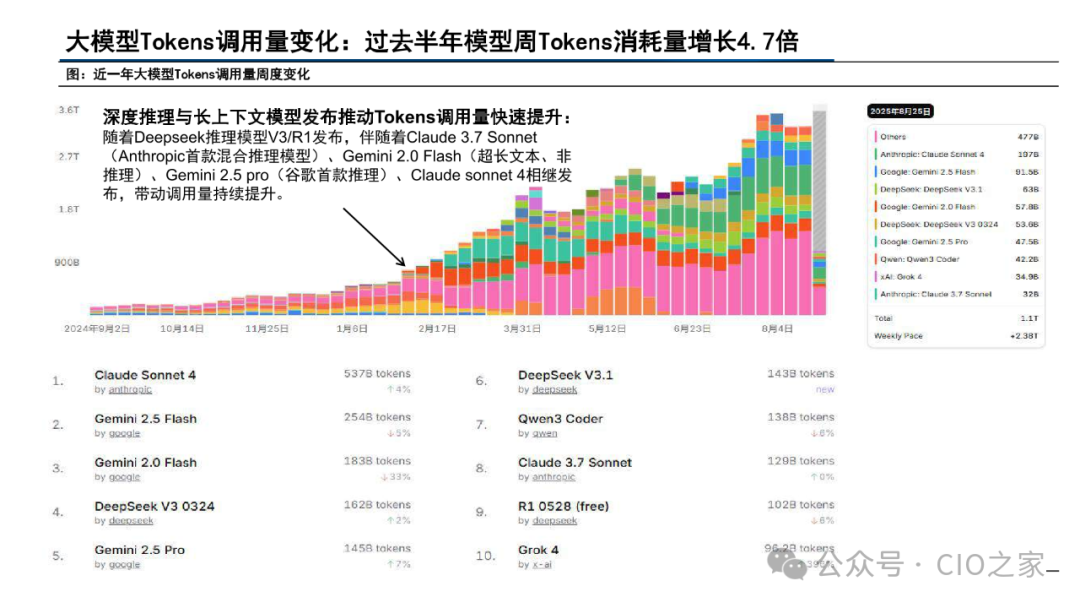

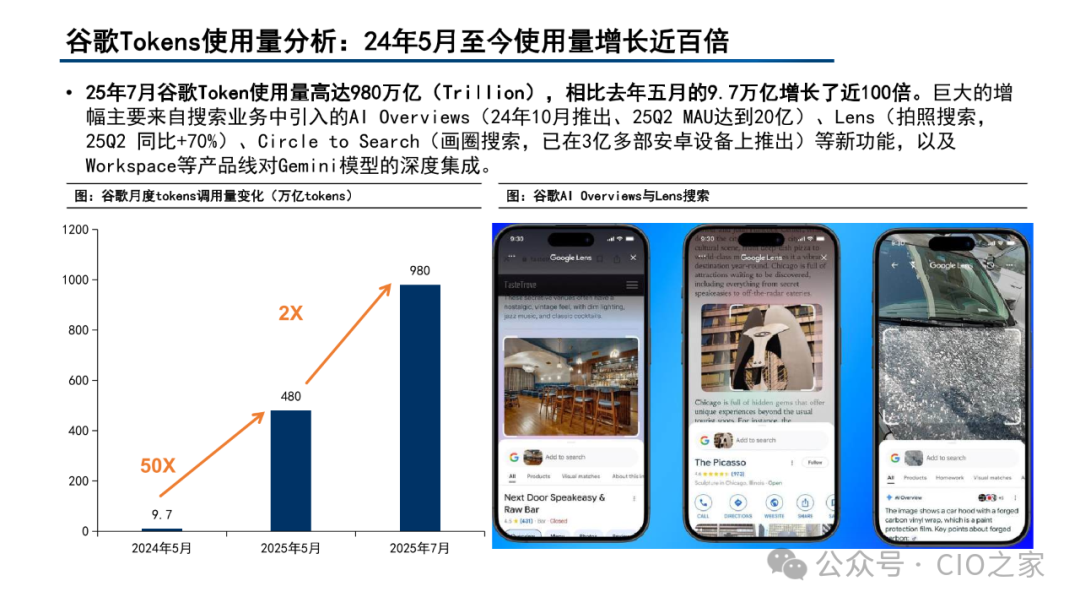

At the model level, the global market is showing differentiated competition. Google’s Gemini and Anthropic’s Claude occupy half of the API call market, with the former leading in multimodal and long-text tasks, while the latter excels in programming and rigorous scenarios. Domestically, DeepSeek and Alibaba’s Qwen series are steadily increasing their market share, with open-source strategies driving rapid diffusion. By 2025, Google’s monthly call volume reached 980 trillion, a hundredfold year-on-year increase, but over 90% of the demand comes from internal applications. This indicates that while the demand for large model inference is exploding, it is still primarily internal, and the external commercialization potential remains to be released.

Application Implementation: C-end Explosion and B-end Reconstruction

At the application level, a clear differentiation has formed on the C-end. ChatGPT and Gemini lead globally with 1 billion and 450 million MAUs, respectively; image generation (such as Midjourney) and programming assistance (such as Cursor, GitHub Copilot) have become the fastest-growing tracks. On the B-end, Microsoft’s Copilot family represents a monthly active user base exceeding 100 million, but implementation still faces challenges such as hallucinations, data security, and high costs—Agent invocation costs are 15 times that of LLMs. Meanwhile, the production cost of SaaS software is approaching zero, and traditional industry paradigms are being reconstructed.

Future Trends and Market Prospects

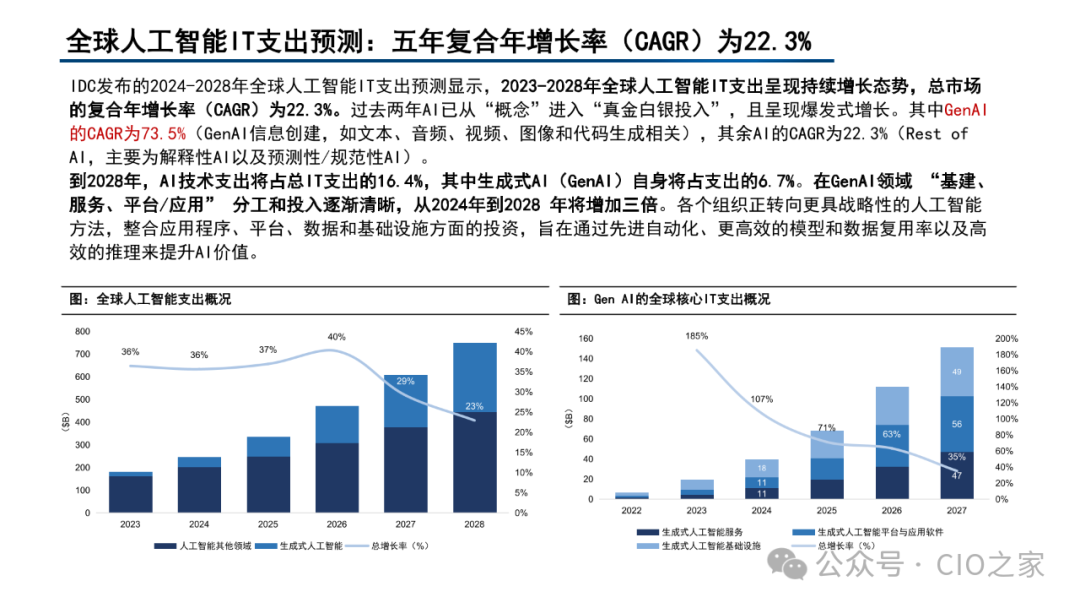

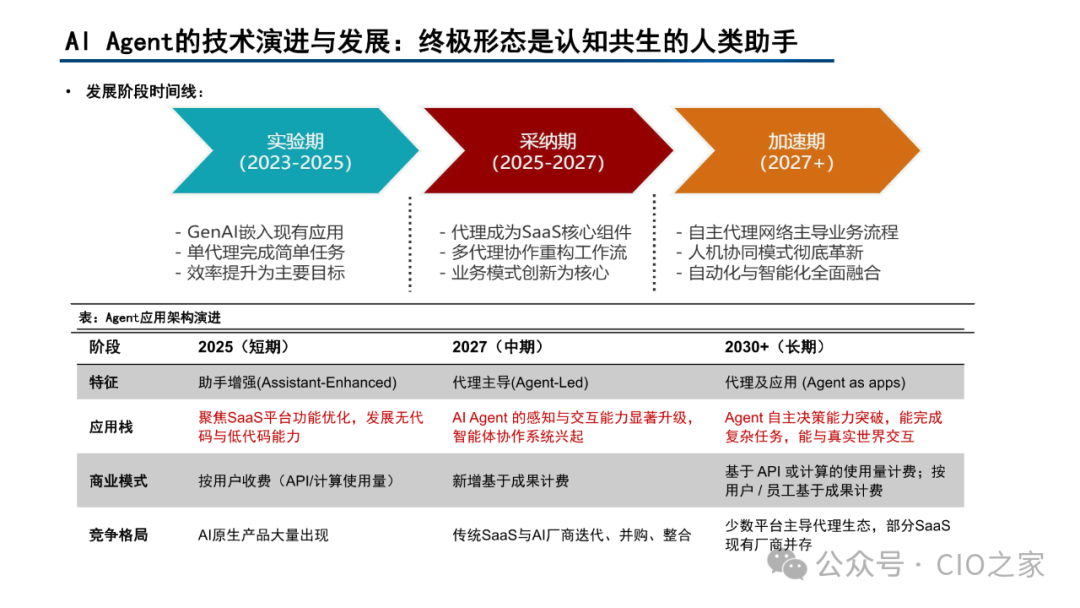

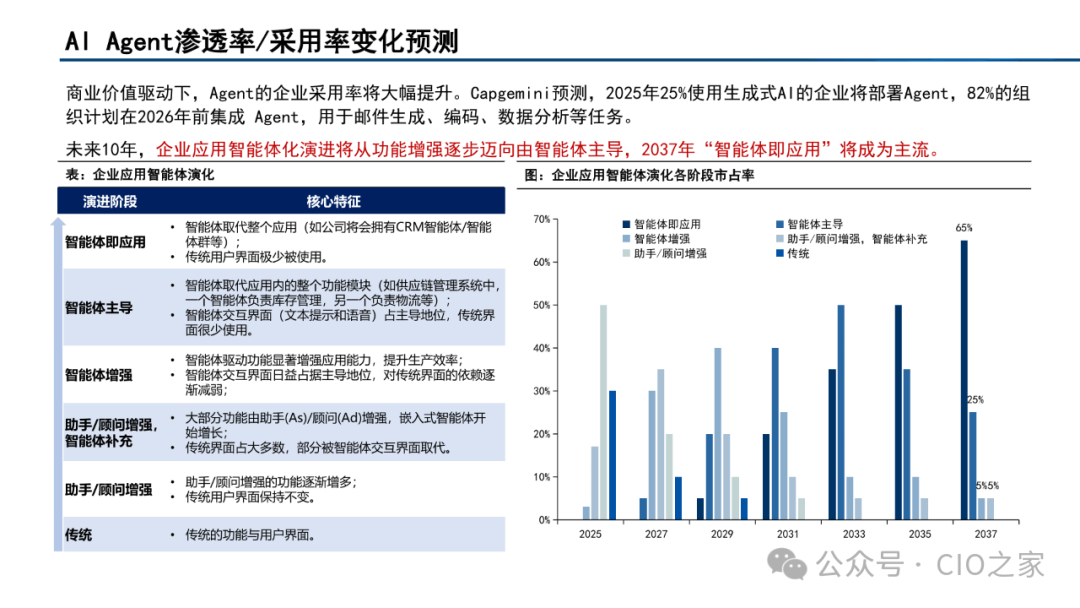

In terms of market size, IDC predicts that global AI IT spending will grow at a compound annual growth rate of 22.3% from 2023 to 2028, with GenAI reaching as high as 73.5%. CBINSIGHTS estimates that by 2032, AI Agent revenue is expected to exceed $100 billion, with an annual compound growth rate of nearly 45%. In terms of development path, the short term (2023-2025) will focus on embedding GenAI into existing applications, the mid-term (2025-2027) will see Agents becoming core components, and the long term (after 2027) will see autonomous agent networks gradually dominating business, ultimately evolving into a “cognitive symbiotic assistant” for humans.

The AI Agent is no longer a concept verification in the laboratory but a key engine for enterprise intelligent transformation. From underlying computing power, development platforms to application ecosystems, the competition between global giants and domestic manufacturers is accelerating. With the unification of protocol standards (MCP, A2A) and the decrease in application costs, Agents are expected to penetrate industries comprehensively in the next decade, becoming the core bridge connecting humanity with the intelligent era.

|

Reply with keywords to get more information |

| Intelligent Agent |

|

Download this document |

|

|

Long press to recognize the QR code to download related documents |

|

|

|

|

|

|

|

|

|

Related Articles |

| Is Traditional BI Dead? The Rise of AI Agents?The AI Agent Monetization Scam: A Carefully Designed B-end Cognitive HarvestHow Enterprises Choose the Right AI Agent PlatformFrom Smart to Reliable: Security Concerns and Defenses of AI AgentsUnderstanding Agent Protocols: MCP, A2A, ANP, AGORAWhy Current AI Agents Are All Talk and No ActionOperational Analysis Agent Practices Based on Label MetricsAI Agent Application Development Experience |