By the 1980s, Japan seemed to be the main beneficiary of the U.S. supply chain strategy. Japanese trade and foreign investment surged. Tokyo’s role in the Asian economy and politics was expanding irreversibly. If Japan could quickly establish dominance in the chip industry, what could stop it from replacing the U.S. geopolitical advantage?

The Golden Age: The Victory of the National System and Craftsmanship (1970s–1980s)

Extreme quality and management philosophy once placed Japanese semiconductors at the pinnacle of the world.

“Chip Wars: The Battle for the World’s Most Critical Technology” by Chris Miller

In the 1980s, the Japanese semiconductor industry rapidly rose, once crushing American competitors with its superior product quality and strong industrial synergy, becoming the global semiconductor industry leader. However, within just over a decade, this seemingly unshakable industrial empire gradually fell into decline.

The 1980s were a hellish decade. Silicon Valley, which once thought of itself as the leader in the global tech industry, faced a survival crisis after 20 years of rapid growth: brutal competition from Japan.

The Transformation of Japanese Manufacturing: From Cheap to High Quality

In the early post-war period, “Made in Japan” was synonymous with “cheap.” However, Japanese companies, represented by Sony, successfully changed this image through high-quality products.

Akio Morita of Sony and his transistor radio became the first outstanding challenger to America’s economic dominance, inspiring Japanese entrepreneurs to aim higher. Japanese companies typically first successfully replicated American products, then manufactured and sold them at higher quality and lower prices.

Extreme Quality: Japanese Semiconductors Outperform American Rivals

At HP, engineer Anderson initially did not take Toshiba and NEC seriously, but after testing their chips, he found that the quality of Japanese products far exceeded that of American competitors.

The failure rate of Japanese chips in the first 1000 hours was no more than 0.02%, while the best American chips had a failure rate of 0.09%, and the worst even reached 0.26%. This meant that the failure rate of American chips could be more than ten times that of Japan. With higher reliability at the same performance metrics and price, Japanese chips gained a strong market competitive edge.

Government-Enterprise Collaboration: The Key Support for Japan’s Semiconductor Rise

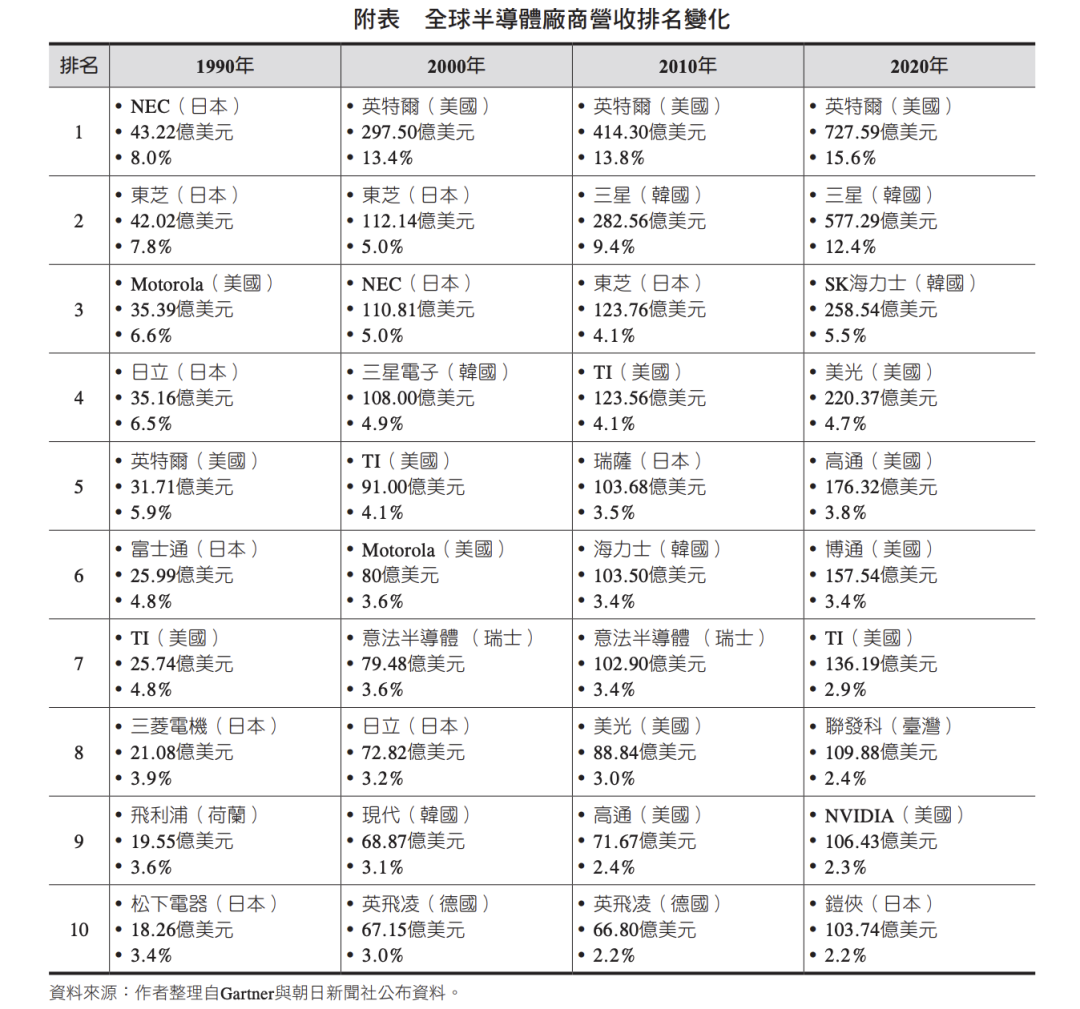

The key to Japan’s semiconductor rise was the collaborative effort between the government and enterprises. Unlike U.S. antitrust policies, the Japanese government actively promoted corporate cooperation, establishing the VLSI Technology Research Consortium in 1976, with the government providing nearly half of the R&D funding to focus on overcoming key technologies. In 1976, Japan’s Ministry of International Trade and Industry, along with five major companies including Toshiba and Hitachi, launched the Very Large Scale Integration (VLSI) Program, with the government funding 40% and mandating competitors to share patents, achieving breakthroughs in 1-micron process technology and filing over 1200 patents within four years. By 1986, Japan’s global market share of DRAM chips reached 80%, with the top three semiconductor companies in the world being Japanese. This model united dispersed companies into a cohesive force, forming a complete industrial chain from materials and equipment to manufacturing, with a yield rate (98%) far exceeding that of the U.S. (60%).

Japanese companies could obtain almost unlimited cheap loans from banks, allowing them to make crazy capital expenditures, even incurring massive losses to seize market share. In 1984, Hitachi’s capital expenditure in the semiconductor business was 80 billion yen (up from just 1.5 billion ten years prior), Toshiba’s increased from 3 billion to 75 billion, and NEC’s from 3.5 billion to 110 billion.

By 1990, Japanese companies accounted for more than half of the global investment in chip manufacturing plants and equipment, completely dominating the investment in chip manufacturing capacity.

In 1985, Japanese companies accounted for 46% of global semiconductor capital expenditures, while the U.S. was at 35%. By 1990, these numbers became even more imbalanced, with Japanese companies accounting for half of the global investment in chip manufacturing plants and equipment. Japanese CEOs were continuously building new factories as long as banks were willing to foot the bill.

Full Industry Chain: Japan Constructs a Complete Semiconductor Ecosystem

Japan’s semiconductor advantage was not only reflected in chip manufacturing but also in constructing a complete industrial chain ecosystem:

In the photolithography equipment sector, Nikon surpassed American GCA equipment through reverse engineering to become the market leader. The world’s leading lens manufacturers are Germany’s Carl Zeiss and Japan’s Nikon, although the U.S. also has some specialized lens manufacturers.

By the 1980s, Japan’s semiconductor industry had formed a complete industrial chain system from materials, equipment to design and manufacturing, and this vertically integrated model provided significant competitive advantages.

As Japanese giants tore apart the American high-tech industry, not only companies producing DRAM chips faced difficulties, but many of their suppliers also encountered similar problems.

From Prosperity to Decline: The Double Strangulation of External Siege and Internal Stagnation (1990s–2010s)

U.S. Counterattack: Three Strategies Restructuring the Industry Landscape

Harold Brown (former U.S. Secretary of Defense) wrote in an article: “High technology is foreign policy.” If America’s high-tech status is deteriorating, then its diplomatic policy status will also face risks.

In response to Japan’s offensive, the U.S. launched a multi-dimensional counterattack:

Trade Measures: In 1986, the U.S. imposed restrictions on Japanese chip exports through anti-dumping agreements (the “U.S.-Japan Semiconductor Agreement,” which is not explicitly mentioned in the book “Chip Wars,” and the references cite “The Impact of the 1986 U.S.-Japan Semiconductor Agreement”). Washington threatened to impose tariffs unless Japan stopped “dumping” (selling DRAM chips cheaply in the U.S. market).

Industry Alliances: The establishment of the Sematech technology alliance, with government and enterprises jointly investing in R&D. In 1987, a group of leading chip manufacturers and the U.S. Department of Defense formed a consortium called Sematech—half funded by the industry and half by the Pentagon.

Technology Transfer: U.S. chip companies transferred technology to South Korea, nurturing new competitors. As most DRAM producers in Silicon Valley were on the brink of bankruptcy, they almost unhesitatingly transferred top technologies to South Korea.

Paper: “The Impact and Implications of the U.S.-Japan Semiconductor Agreement on Japan’s Semiconductor Industry Competitiveness”

Japan’s Decline: Coexisting Internal Causes and External Pressures

Japan’s semiconductor decline has multiple causes:

Limitations of the Innovation Model: Overemphasis on manufacturing efficiency while neglecting fundamental technological innovation. As a Japanese journalist noted: “We do not have Dr. Noyce or Dr. Shockley.” Sony’s research director, renowned physicist Makoto Kikuchi, admitted: “Japan excels at implementation, while the U.S. excels at innovation.”

Closed Systems Struggling to Adapt to Change: The Japanese zaibatsu system struggled to adapt to the rapid iteration of innovation, while American startups were more agile.

Intensified External Competition: The rise of South Korea and Taiwan diverted resources from the industry. As the Japanese stock market crashed, Japan’s semiconductor dominance was already weakening. By 1993, the U.S. regained the top position in semiconductor shipments. In 1998, South Korea replaced Japan as the world’s largest DRAM producer, while Japan’s market share plummeted from 90% at the end of the 1980s to 20% in 1998.

Historical Insights: Balancing Technological Sovereignty and Global Cooperation

The rise and fall of Japan’s semiconductor industry provides important insights:

Industrial Policy and Capital Investment can quickly establish scale advantages, but mere manufacturing advantages are unsustainable; a technological innovation ecosystem must be built.

The global industrial chain is both cooperative and competitive; “high technology is foreign policy”—technological advantages are directly related to national strategic status.

The experiences of quality management and industrial chain integration remain valuable. In the current global semiconductor industry landscape, Japanese companies still maintain key advantages in materials (Shin-Etsu Chemical and SUMCO monopolize 60% of global silicon wafers; JSR and Tokyo Ohka dominate 90% of the photoresist market), and equipment (Tokyo Electron has an 87% market share in coating and developing equipment, and Nikon’s lithography machines achieve a precision of 1.5nm), which is a continuation of the technological foundation accumulated during its peak.

Although Japan’s semiconductor industry has not maintained absolute dominance, its development history reveals the eternal question of technological innovation and industrial balance: how to find a balance between open cooperation and technological self-reliance, and how to emphasize both manufacturing efficiency and innovation capability. These are issues worth pondering for semiconductor industries worldwide.

In the context of increasingly fierce global chip competition, the history of Japan’s semiconductor rise and fall is even more worthy of in-depth study and reference.