In the process of AI development, early cloud AI became the dominant force in the industry due to its powerful computing power and centralized data processing capabilities. However, as application scenarios continue to expand, especially in fields such as the Internet of Things, autonomous driving, and industrial control, the limitations of cloud AI have gradually become apparent. According to research by the International Data Corporation (IDC), global spending on edge computing solutions is expected to approach $261 billion by 2025, with a projected compound annual growth rate (CAGR) of 13.8%, reaching $380 billion by 2028. The retail and service industries will account for the largest share of edge solution investments, making up nearly 28% of total global spending.This data clearly reflects that the focus of the industry is shifting from the cloud to the edge.

People are increasingly concerned that artificial intelligence is sliding into a bubble. A report released by the NANDA project at the Massachusetts Institute of Technology titled “The GenAI Gap: The State of Business AI in 2025” found that95% of companies have seen little to no productivity improvement after developing generative AI tools. Even OpenAI CEO Sam Altman admitted that investors may be overly excited about AI, comparing the current market to a bubble.

However, industry insiders believe that this criticism mainly targets the cloud-based AI market and software algorithms.

01Why is Edge AI Generation Needed?Currently, mainstream language models on the market, from OpenAI’s GPT, Google’s Gemini, Anthropic’s Claude, to popular domestic models like DeepSeek, almost all rely on AI cloud computing to complete generative tasks. This model, which depends on remote servers, can easily handle complex demands such as large-scale model training and high-resolution image synthesis due to its powerful computing power, and it is highly scalable—ranging from daily Q&A for individual users to large-scale enterprise deployments, it can flexibly adapt, providing an experience that is sufficient for ordinary users.

01Why is Edge AI Generation Needed?Currently, mainstream language models on the market, from OpenAI’s GPT, Google’s Gemini, Anthropic’s Claude, to popular domestic models like DeepSeek, almost all rely on AI cloud computing to complete generative tasks. This model, which depends on remote servers, can easily handle complex demands such as large-scale model training and high-resolution image synthesis due to its powerful computing power, and it is highly scalable—ranging from daily Q&A for individual users to large-scale enterprise deployments, it can flexibly adapt, providing an experience that is sufficient for ordinary users.

However, in enterprise-level applications or more complex scenarios, the shortcomings of the cloud model gradually become apparent: first, the latency is high, and the response speed of complex tasks is easily affected by network fluctuations; second, it is highly dependent on the network, and once disconnected, it cannot be used; most critically, there are data privacy risks—large amounts of raw data need to be uploaded to the cloud for processing, which not only increases bandwidth costs but may also lead to data breaches due to vulnerabilities in transmission or storage, which is particularly problematic for sensitive fields such as healthcare and finance.

It is precisely for this reason that the advantages of edge generative AI are beginning to emerge. It deploys generative capabilities directly on local devices—potentially our smartphones, surveillance cameras, or even autonomous vehicles and industrial machines, with data processing completed locally, ensuring that sensitive information does not leave the device, thus safeguarding privacy from the source. Meanwhile, the low-latency characteristics of edge AI are a “real-time scene savior”: autonomous driving requires millisecond-level road condition judgments, and industrial automation relies on immediate equipment fault warnings. These scenarios, which demand high response speeds, can all be precisely adapted by edge AI. More importantly, it does not require frequent data transmission, significantly reducing bandwidth requirements, and can operate independently even in remote areas without network access or in industrial workshops with weak signals, with stability and reliability far exceeding that of cloud models.

The technical prototype of edge intelligence can be traced back to the 1990s, when it appeared in the form of Content Delivery Networks (CDN). Its initial positioning was to provide network services and video content distribution to users nearby through servers distributed at the network edge, with the core goal of alleviating the load pressure on central servers and improving content transmission and access efficiency.

However, with the explosive growth of Internet of Things (IoT) devices and the widespread adoption of 4G and 5G mobile communication technologies, the global data generation volume has increased exponentially, gradually entering the zettabyte (ZB) era. Under this background, traditional cloud computing architectures have gradually revealed their shortcomings: data must be fully transmitted to the cloud for processing, which not only incurs high bandwidth consumption but also leads to high latency issues due to transmission distances, while data flowing across networks also brings risks of privacy breaches, making it difficult to meet the demands for real-time and security-sensitive scenarios.

Entering the 21st century, to address the pain points of cloud computing, the concept of edge computing was officially proposed. Its core idea is to move the data processing phase from the cloud to edge nodes close to the data source, significantly reducing the amount of data uploaded to the cloud by completing preliminary filtering, processing, and forwarding of data locally, thereby alleviating bandwidth pressure and reducing latency. However, at this stage, edge computing mainly focused on optimizing data processing workflows and had not yet integrated with artificial intelligence (AI) technologies, nor did it involve the deployment and application of AI algorithms.

It was not until after 2020, with the maturity of AI technologies (especially lightweight models and low-power computing technologies), that edge computing and AI began to deeply integrate, and “edge intelligence” emerged as an independent fusion technology. Its core feature is to deploy AI algorithms (including inference and training phases) on edge devices close to the data generation end (such as IoT terminals and edge servers), enabling real-time data processing and low-latency decision-making while avoiding the uploading of raw data to the cloud, thus safeguarding data privacy from the source.

Looking at the development history of edge intelligence, it can be clearly divided into three core stages: the first stage focuses on “edge inference,” where the model training process still relies on the cloud to complete, and the trained model is then pushed to edge devices to perform inference tasks; the second stage enters the “edge training” phase, leveraging automated development tools to achieve the full process of model training, iteration, and deployment at the edge, reducing reliance on cloud resources; the third stage, which is also the future development direction, is “autonomous machine learning,” aiming to enable edge devices to possess autonomous perception and adaptive adjustment learning capabilities, completing model optimization and capability upgrades without human intervention.

Of course, this does not mean that cloud AI will be replaced. In the face of complex tasks involving ultra-large-scale model training and cross-device collaboration, the powerful computing power of the cloud remains irreplaceable. The future trend is more likely to be a complementary relationship between “cloud + edge”: the cloud is responsible for the training and optimization of underlying models, while the edge is responsible for real-time deployment and data processing in local scenarios. The two work together to leverage the computing power advantages of the cloud while also considering the privacy and real-time aspects of the edge, ultimately promoting the safe and efficient integration of AI technology into various industries.

Data Source: Precedence Research Semiconductor Industry Overview

Data Source: Precedence Research Semiconductor Industry Overview

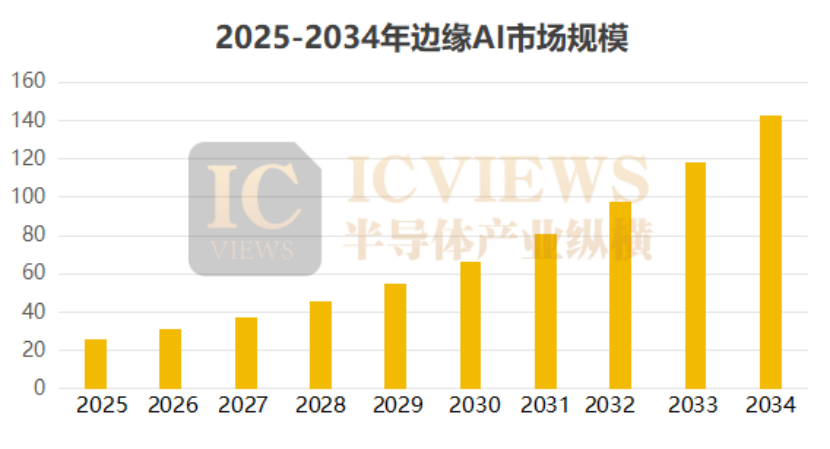

Market research firm Market data indicates that the global edge AI market is expected to exceed $140 billion by 2032, a significant increase from $19.1 billion in 2023. Precedence Research data shows that the edge computing market could reach $3.61 trillion by 2032 (CAGR 30.4%). This data indicates the vast development prospects of edge AI and explains why major companies are turning their attention to this new blue ocean.

02Major Companies Positioning to Seize Opportunities

02Major Companies Positioning to Seize Opportunities

In the edge AI chip race, major companies are fiercely competing. As the core hardware support for the development of edge AI, the chip field has shown a trend of simultaneous innovation in computing power and architecture in recent years.

Apple is actively laying out its self-developed edge AI chips in the iPhone series. For example, the newly released iPhone 16 series is equipped with the A18 chip, which is deeply optimized for AI functions. The A18 uses second-generation 3-nanometer technology, integrating a 16-core neural network engine, capable of 350 trillion operations per second. This powerful computing power allows Face ID recognition to be completed instantly, and Animoji generation is also incredibly smooth, with response speeds entering the millisecond era. At the same time, thanks to the chip’s local processing capabilities, data does not need to be uploaded to the cloud, fundamentally avoiding the privacy risks associated with cloud transmission and building a solid privacy defense for users.

NVIDIA, as a leader in graphics processing and AI computing, has also achieved remarkable results in the layout of edge AI chips. Its Jetson series edge AI chips are designed for edge devices such as robots, drones, and smart cameras. For example, the Jetson Xavier NX chip integrates 512 NVIDIA CUDA cores and 64 Tensor Cores, with a computing power of up to 21 TOPS (trillions of operations per second) while requiring only 15W of power, providing strong visual recognition and decision-making support for robots in complex and variable environments. In logistics and warehousing scenarios, mobile robots equipped with the Jetson Xavier NX chip can quickly identify goods and shelf locations, plan optimal paths, and efficiently complete cargo handling tasks, significantly improving logistics operation efficiency.

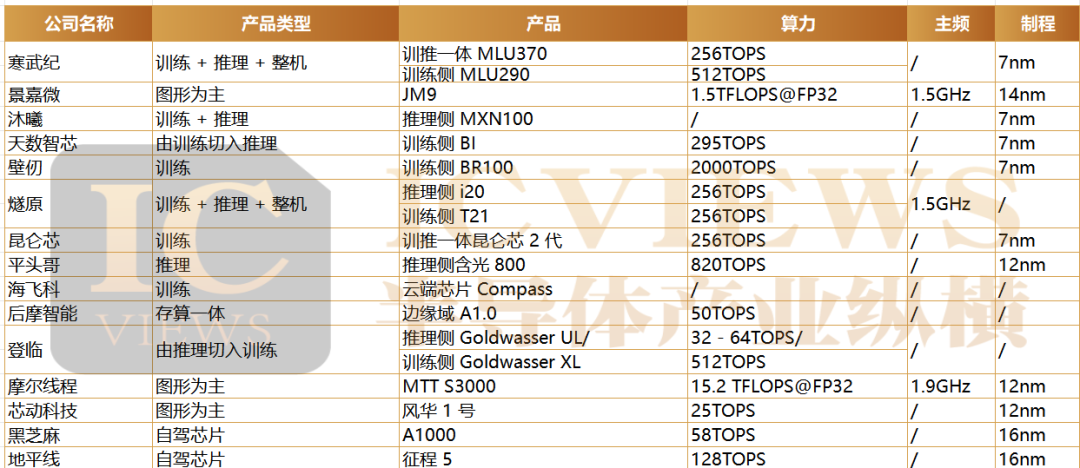

Domestic companies have also achieved impressive results in the field of edge AI chips. Yuntian Lifei launched the DeepEdge 10 series in 2022, designed for large edge models; the upgraded DeepEdge200 in 2024 adopts D2D Chiplet technology, paired with the IPU-X6000 accelerator card, compatible with nearly 10 mainstream large models such as Cloud Tian Book and Tongyi Qianwen, achieving real-time anomaly detection in smart security cameras, with a warning response time reduced to within 0.5 seconds.

Domestic AI computing chip companies’ main products Source: Minsheng Securities

Domestic AI computing chip companies’ main products Source: Minsheng Securities

On the evening of August 26, Yuntian Lifei announced its semi-annual report for 2025. The financial report showed that its operating income in the first half of 2025 reached 646 million yuan, a 123.10% increase compared to the same period last year; the net profit attributable to the parent company was -206 million yuan, a year-on-year loss reduction of 104 million yuan; the net profit excluding non-recurring items was -235 million yuan, a year-on-year loss reduction of 110 million yuan. Regarding the performance changes, the company stated that the increase in operating income compared to the same period last year was mainly due to the increase in sales revenue from consumer and enterprise-level scenario businesses. The reduction in losses was mainly due to the simultaneous increase in operating income and gross profit margin during the reporting period.

Data Source: Company Financial Reports Semiconductor Industry Overview

Data Source: Company Financial Reports Semiconductor Industry Overview

Faced with the reality of limited resources such as memory and computing power in edge devices, international tech giants like Google, Microsoft, and Meta are focusing on the research and optimization of lightweight large models to achieve efficient operation of large models on edge devices.

Google is actively exploring in this field, successfully lightweighting some large models through meticulous design of model architecture and fine-tuning of parameters. For example, its Gemini Nano model, optimized based on the Transformer architecture, significantly reduces the number of model parameters and computational complexity while maintaining high model performance, allowing it to run smoothly on edge devices such as smart security cameras, providing strong support for real-time video image analysis. In urban security monitoring networks, cameras deployed with the Gemini Nano model can identify pedestrians and vehicles in real-time, monitor abnormal behaviors, and issue timely alerts, effectively enhancing urban safety and prevention capabilities.

Microsoft has taken a different approach, launching the phi-1.5 model, which, although relatively small in parameter scale, is unique in its selection of training data. This model is trained on a carefully selected 27B token “textbook-level” dataset, demonstrating outstanding mathematical reasoning capabilities, surpassing some large models with hundreds of billions of parameters. In intelligent tutoring systems in the education sector, the phi-1.5 model can quickly and accurately answer students’ math questions, providing detailed problem-solving steps and ideas, assisting teachers in teaching, and improving teaching quality and efficiency.

03Where is the Breaking Point?

03Where is the Breaking Point?

Smart home devices are one of the most common application scenarios for edge AI. They allow smart home devices to move away from “single command execution” to “behavior prediction services.” Smart thermostats learn user routines and sleep cycles, adjusting temperatures based on outdoor weather dynamics, ensuring comfort while reducing energy consumption by 15%-20%, far superior to traditional devices. Devices like the Baidu speaker, leveraging edge AI, respond to high-frequency commands within 0.3 seconds and can link cross-brand devices to form scene services, such as the “homecoming mode” that automatically triggers lighting, temperature adjustment, and music playback, driving the penetration rate of smart home scene linkage in China to 38%, exceeding the global average level.

Wearable devices are another important area for edge AI. Smart glasses developed by Meta in collaboration with Ray-Ban achieve millisecond-level image recognition and local translation in cities like Shanghai, enabling real-time conversion of road sign text and recommendations for nearby stores, with cumulative shipments exceeding 2 million units. Chinese brands focus more on deep health management, with Huawei’s Watch GT series using edge AI to integrate heart rate, blood oxygen, and ECG data, achieving an accuracy rate of 85% in screening for sleep apnea syndrome, helping over 100,000 users detect health issues early; OPPO’s band adjusts intensity in real-time based on user exercise data, generating personalized plans, creating a closed loop of “collection – analysis – suggestion” for health management.

In the industrial sector, the combination of AI with IoT and robotics is driving factories from “single device automation” to “full-process intelligent collaboration,” achieving full-chain intelligence through edge AI’s real-time processing of production data, enabling “fault prediction, process optimization, and quality traceability”. In smart factories, robots are no longer just mechanical arms performing “repetitive single actions” but are now “intelligent production units” with “real-time decision-making capabilities.” Arm’s computing platform provides an “efficient data processing foundation” for industrial IoT. In industrial scenarios, a smart device generates over 10GB of sensor data daily (such as temperature, vibration, pressure). If all data were uploaded to the cloud for processing, it would not only consume a lot of bandwidth but also lead to data delays (which could take minutes). However, the edge computing capabilities of the Arm platform can achieve “local data filtering and analysis”—only uploading “anomalous data” (such as vibration frequency exceeding normal range) to the cloud while generating a “device health report” locally, reminding maintenance personnel to repair in a timely manner.

In the long run, the deep value of edge AI lies in promoting artificial intelligence from a “tool attribute” to a “scene attribute.” When intelligence no longer relies on remote support from the cloud but is embedded in specific scenes of life and production—from smart thermostats dynamically adjusting temperatures based on user habits to factory robots autonomously optimizing work paths, and wearable devices customizing health plans for users, artificial intelligence can truly integrate into the fabric of industries and daily life.

This transformation not only avoids the risk of technological bubbles but also allows the value of artificial intelligence to take root in practical applications.