Among the four main hardware components in the perception layer of autonomous driving, cameras are undoubtedly the one with the highest certainty for future growth. With their high performance combined with low cost, cameras are indispensable hardware for achieving autonomous driving, whether using a pure vision solution or a multi-sensor fusion approach, and there is a clear trend of increasing average installation per vehicle.

Following the previous article on the LiDAR sector, this article will cover the applications and industry chain of in-vehicle cameras, from lenses to modules, identifying high-value and certain segments along with corresponding investment opportunities.

Table of Contents

1. Camera Classification and Composition

2. Industry Chain

3. Market Development

1. Camera Classification and Composition

First, let’s look at some basic classifications and components of cameras. Cameras are hardware commonly used in daily life, and in the automotive industry, performance is typically measured by indicators such as field of view (FOV), detection distance, resolution, signal-to-noise ratio, frame rate, and dynamic range.

Field of View (FOV) refers to the spatial range that the camera can cover. A larger field of view allows the camera to capture image information from a broader area. The size of the field of view depends on the lens focal length; the shorter the focal length, the larger the field of view. Generally, 40 – 60° is the standard field of view, 60 – 110° is wide-angle, and greater than 110° is ultra-wide-angle, with fisheye cameras capable of achieving 180° or 220° angles.

Resolution is a core performance indicator of the camera, referring to the ability to resolve details of the subject being captured. The higher the resolution, the clearer the image. Common resolutions include:1.3MP (1280*960), 2MP (1920*1080), 5MP (2560*2048), 8MP (3200*2400).

Dynamic Range refers to the range of brightness values that can be displayed normally for the brightest and darkest objects in the same scene. A larger dynamic range indicates clearer image layers, which is crucial for recognizing dark and bright information. Low dynamic range (LDR) typically ranges from 40 – 60dB, while high dynamic range (HDR) is generally 100dB and above. HDR can better identify details in bright and dark areas in scenes with strong contrast, such as in backlighting or when entering and exiting tunnels.

Additionally, detection distance is also very important for autonomous driving algorithms. With a fixed camera resolution, a shorter focal length results in a larger field of view but a shorter detection distance.

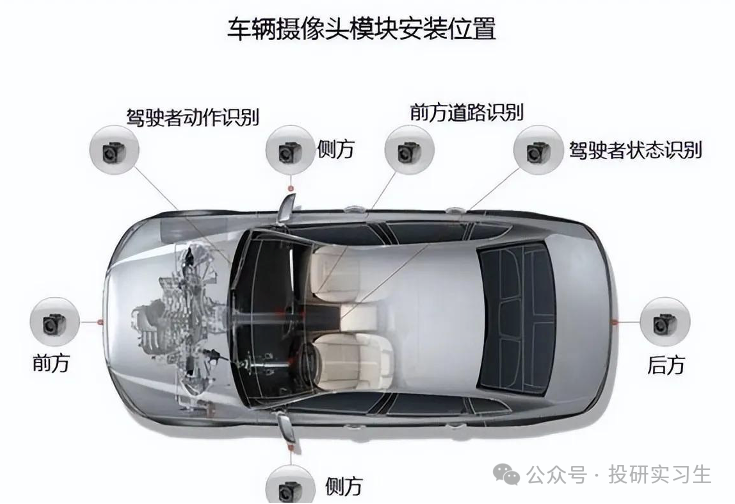

In terms of application scenarios in vehicles, cameras are mainly divided into two types: those inside the vehicle and those outside. The interior cameras are primarily responsible for smart cockpit functions, while exterior cameras are used for driver assistance or autonomous driving. Interior cameras are further divided into DMS (Driver Monitoring System) and OMS (Occupant Monitoring System), which are installed inside the vehicle (e.g., above the rearview mirror, in the center of the steering wheel) to capture images of the driver and passengers for intelligent monitoring. DMS and OMS can detect the driver’s state (e.g., fatigue) and facilitate human-machine interaction (e.g., gesture control).

The cameras used in autonomous driving generally refer to those installed outside the vehicle, which can be further divided into front view, side view, surround view, rear view, and electronic rearview mirror (CMS). Among these, front view, side view, and rear view are mainly used for driving assistance, while 360° surround view and rear view are used for parking assistance.

In driving assistance, the front view camera is key to perception functions, responsible for forward collision warning (FCW), pedestrian collision warning (PCW), lane departure warning (LDW), lane keeping assist (LKA), automatic emergency braking (AEB), and adaptive cruise control (ACC).

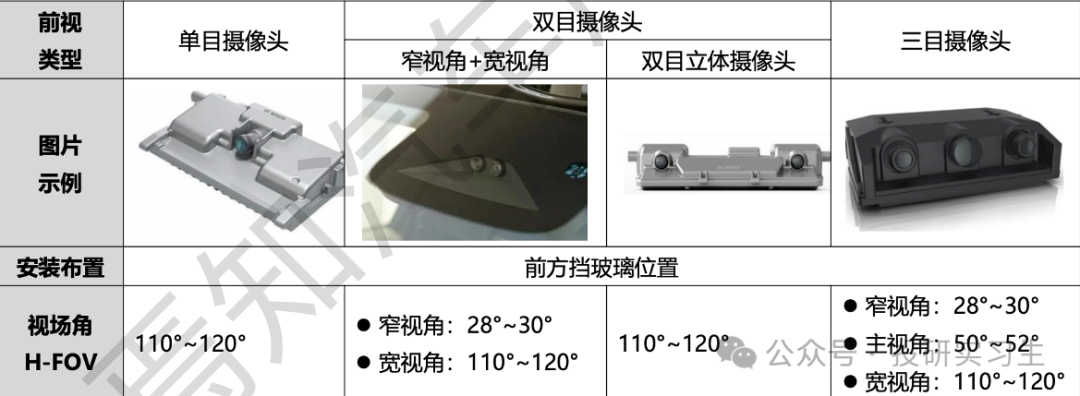

The front view camera typically consists of 1-3 cameras, with solutions including integrated front view units and standalone camera modules connected to independent controllers. The front view does not require a very high field of view but needs a higher resolution for clear identification; industry-leading technology has achieved mass production of 8 million pixels.

Depending on the number of lenses, they can be classified as monocular, binocular, and trino cameras. Monocular and binocular cameras are primarily in integrated forms, while binoculars can also be a combination of two monocular cameras (narrow angle + wide angle). Trino cameras consist of three camera modules with different fields of view, and the data must be input to the intelligent driving domain controller for processing.

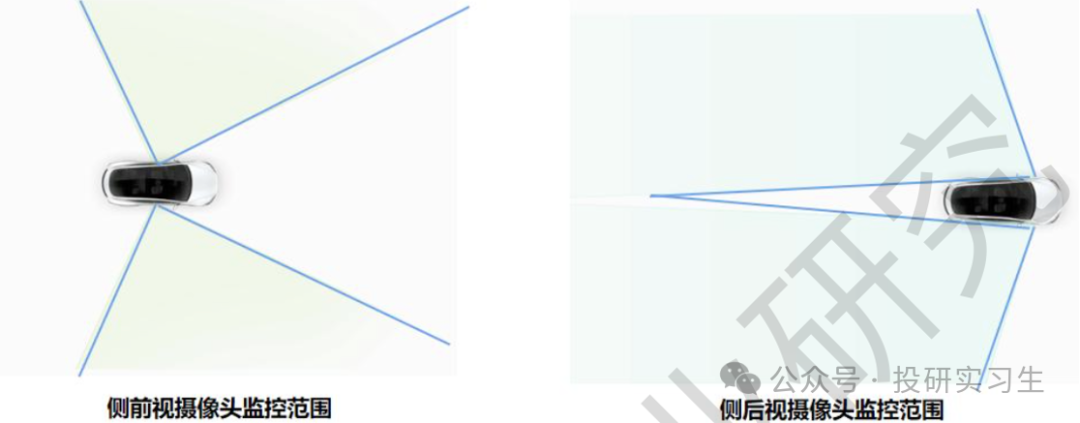

Side view and rear view cameras are mainly used for monitoring vehicles on the side and rear. Side view and rear view cameras typically require a resolution of 2-3MP, with a detection distance of 80-100 meters, but they require a wide angle for broader detection. Side view cameras are generally composed of four cameras surrounding the vehicle, while rear view cameras require 1-4 cameras installed at the rear.

The cameras used for parking assistance mainly include rear view and 360° surround view, with the latter typically composed of four ultra-wide-angle fisheye cameras stitched together to display a bird’s-eye view on the vehicle’s central control screen.

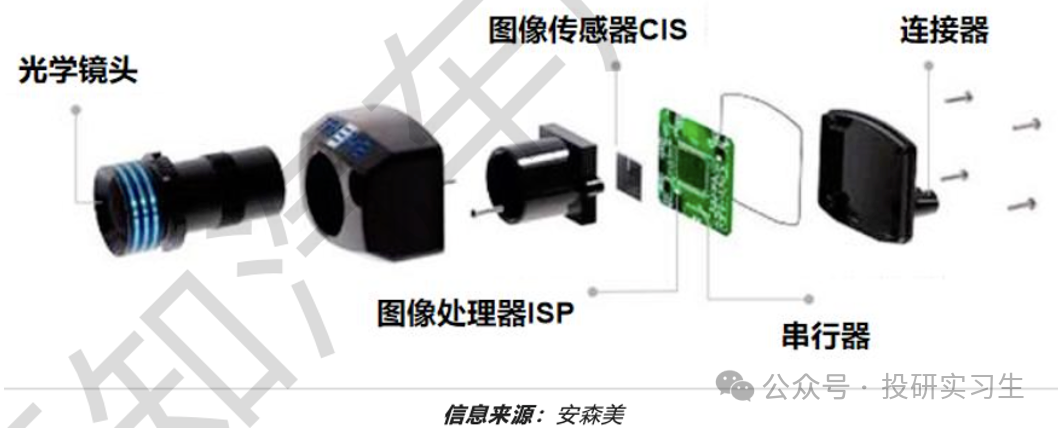

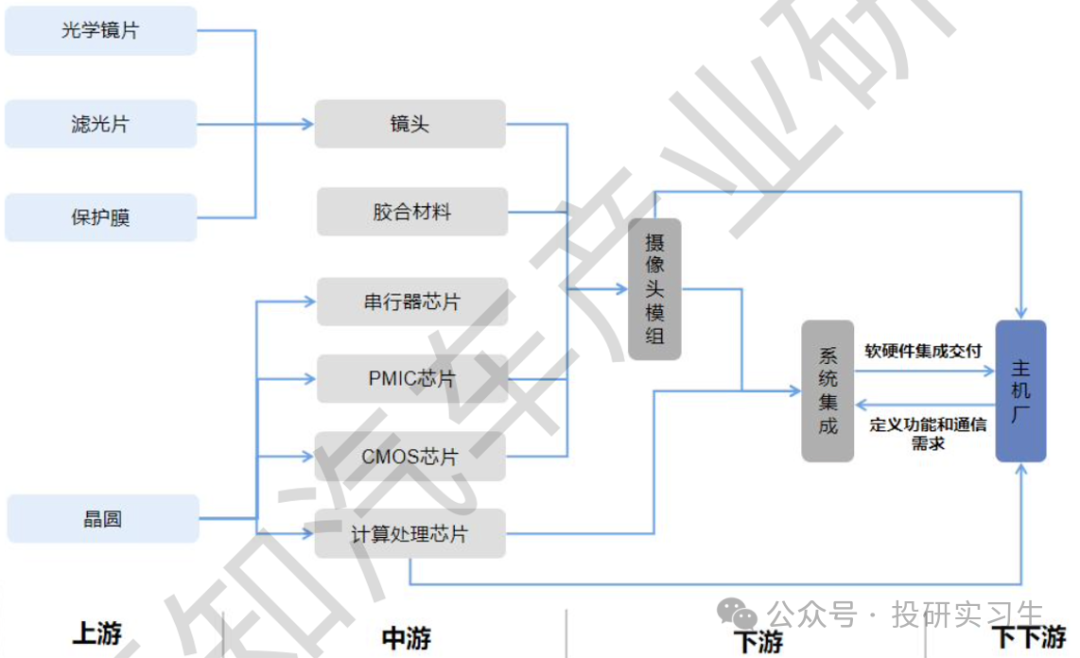

The above is the classification of in-vehicle cameras. Next, let’s discuss their composition. In-vehicle cameras are generally shipped in module form, with a module including optical lenses, image sensors (CIS), image signal processors (ISP), serializers, and connectors.

The optical lens consists of multiple lens elements and filters, and the lenses can be categorized into plastic (P) and glass (G) based on material, thus optical lenses can be divided into all-glass and glass-plastic hybrid types. Glass lenses outperform plastic lenses in terms of light transmittance, wear resistance, and other areas, but they have lower mass production yields and higher costs. Front view and side view cameras often use all-glass lenses, while surround view and interior cameras typically use glass-plastic hybrid lenses.

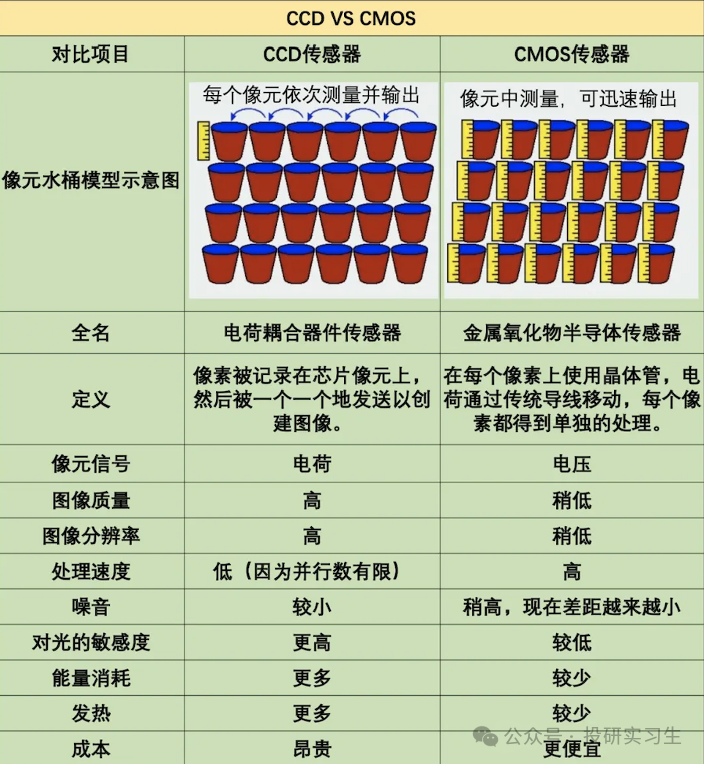

The image sensor (CIS) is used to convert light signals into electrical signals, a process that mainly consists of two steps: first converting light signals into charge signals, and then converting charge signals into voltage signals. Depending on the different methods used in the second step,CIS is divided into CMOS and CCD types.

CCD was the mainstream sensor in early cameras, but it has now been largely replaced by CMOS. The core difference between CCD and CMOS is that CMOS has an independent circuit for each pixel, allowing for parallel processing of all pixels, resulting in faster speeds. CCD, on the other hand, follows a serial processing route, processing pixels one by one in a specific order.

Due to the fast processing speed, low power consumption, and low cost of CMOS, CCD has gradually been phased out by CMOS sensors. As the performance requirements for in-vehicle cameras continue to rise, CMOS is also moving towards high resolution and high dynamic range (HDR).

The image signal processor (ISP) is used for further processing of the RAW format data output from the CMOS, including image scaling, automatic exposure (AE), automatic white balance (AWB), automatic focus (AF), image denoising, etc., ultimately converting it into RGB and YUV format data. In the past, ISPs were often packaged as independent chips along with other modules in the camera module, but with the trend of miniaturization and lightweighting of cameras, ISPs are gradually being integrated into CMOS chips, which significantly improves signal transmission latency.

However, as vehicles transition from a distributed ECU architecture to a centralized domain controller architecture, the main control chip SoC generally integrates the ISP module directly, supporting the processing of RAW data from multiple cameras. As a result, camera modules no longer require an ISP and serve only as information collection devices. Therefore, most front view and rear view cameras no longer have ISPs, but surround view cameras still integrate ISPs because they are directly connected to the vehicle system for 360° imaging display and do not participate in autonomous driving algorithms.

Additionally, the signals processed by the CMOS and ISP are based on the MIPI/CSI standard parallel signals, which have a short transmission distance, so a serializer is needed to convert them into serial signals suitable for long-distance transmission.

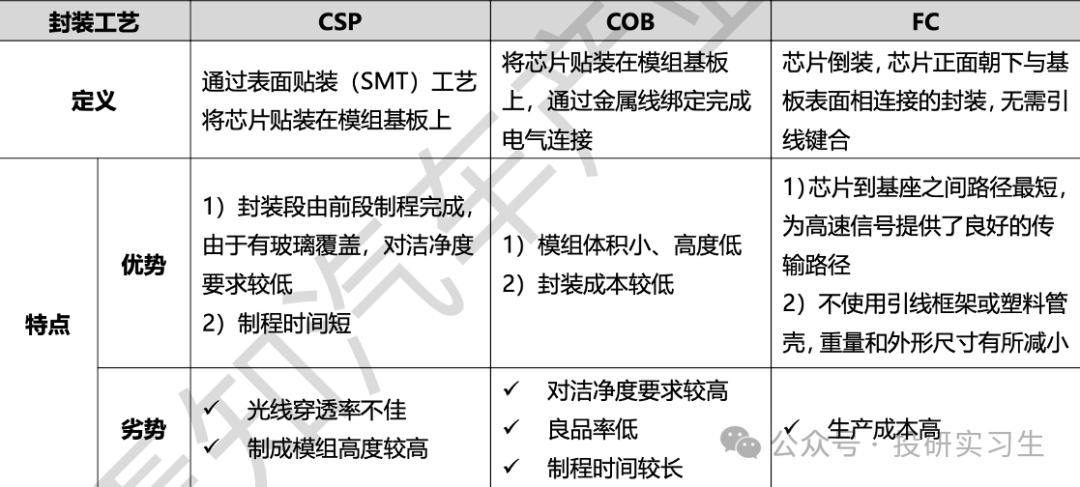

Finally, there are different packaging processes for camera modules. Currently, CSP packaging is the main mode, while high-resolution cameras with over 5 million pixels often use the smaller and more cost-effective COB technology for packaging. The CSP route is a surface mount technology (SMT) that mounts the chip onto the module substrate; COB technology uses wire bonding to mount the chip onto the module substrate.

2. Industry Chain

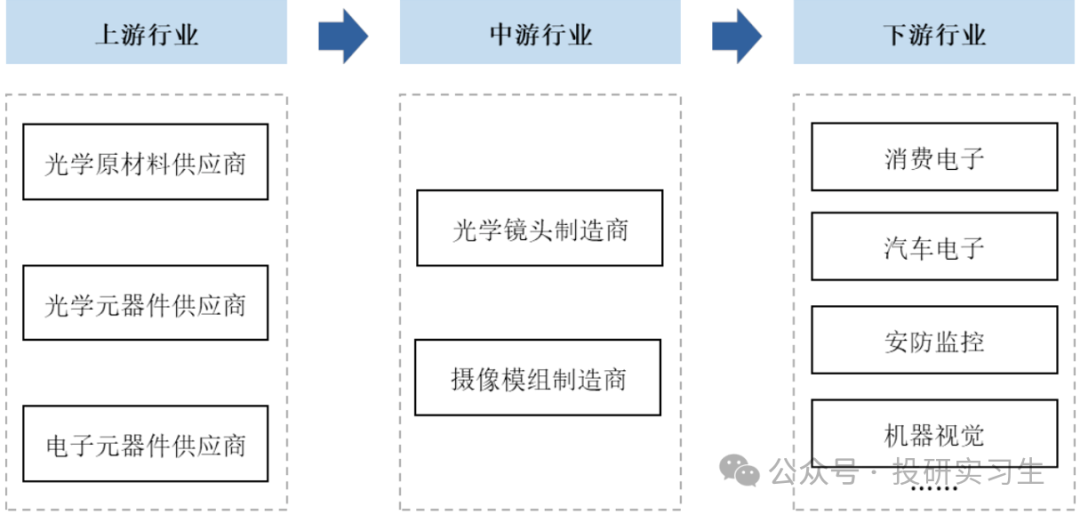

The in-vehicle camera is positioned in the midstream of the optical industry chain, which can be divided into optical lens manufacturers and camera module manufacturers, with modules being the final shipping form. Some manufacturers focus on lens production, while others adopt an integrated layout to produce both lenses and modules. The downstream industries for cameras are very diverse; in-vehicle cameras are just one branch, with others including consumer electronics (such as smartphones), security monitoring, robotics, etc.

The upstream of the optical industry can be divided into optical direction and electronic (chip) direction, with the former responsible for hardware related to optical imaging, including lenses and optics, and the latter responsible for various signal processing chips, such as CMOS and ISP. From the upstream perspective, components of lenses such as lens elements, filters, protective films, and wafer manufacturing can be considered as upstream.

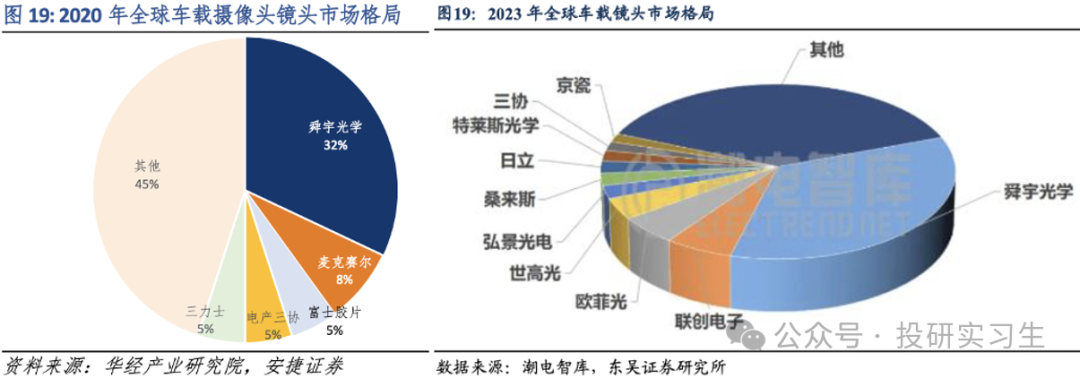

In the past, optical lenses and lenses were dominated by Japanese and Korean companies, but in recent years, with domestic companies achieving technological breakthroughs and deepening industrialization, domestic companies have captured a major share of the lens and lens market. According to data from 2020, Sunny Optical held an absolute share of 32% in the global automotive lens market, followed by Maxell at 8%. By 2023, Sunny Optical’s share continued to expand, with domestic companies such as Lens Technology, OFILM, Hongjing Optoelectronics, and Telesis Optical appearing in the top ranks.

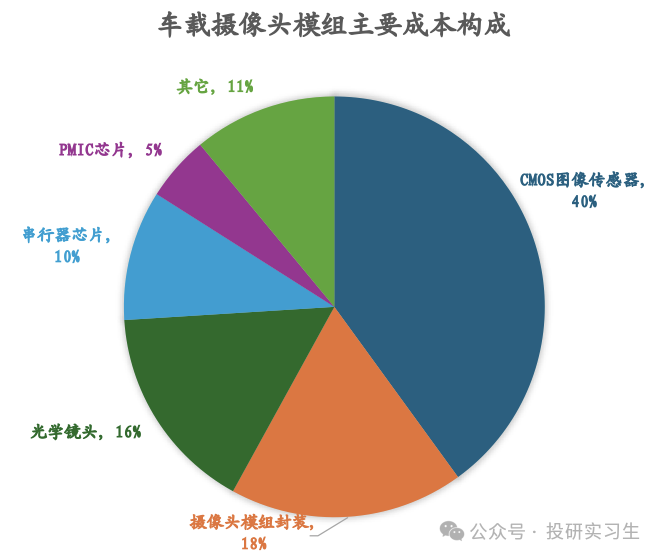

In terms of cost composition, the most valuable part of the in-vehicle camera module is the image sensor, followed by the cost of module packaging and optical lenses, accounting for 40%, 18%, and 16%, respectively.

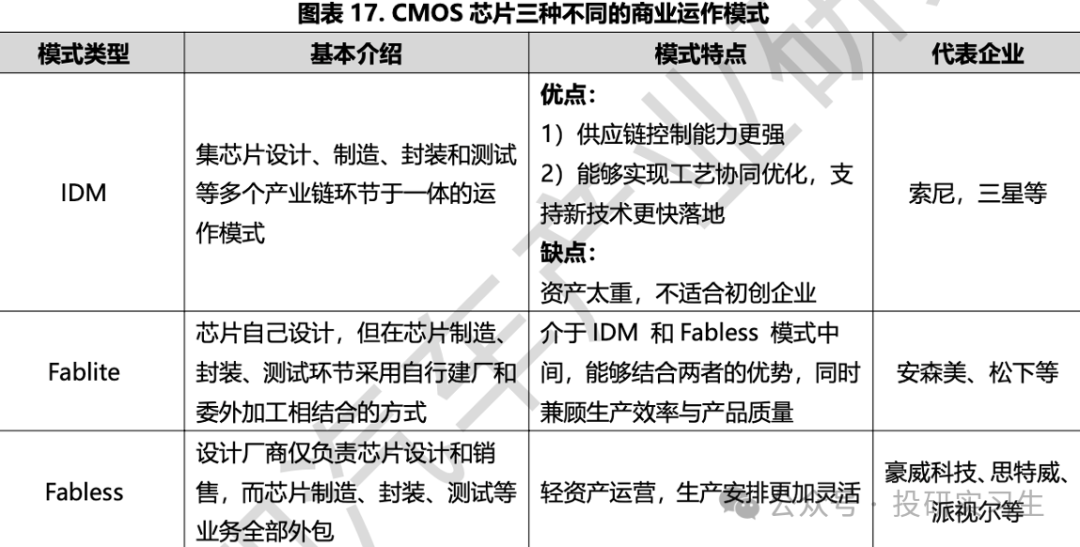

As a type of chip, the supply chain model for automotive CMOS is consistent with that of semiconductors, and companies can be divided into IDM, Fab-lite, and Fabless three models. The IDM model is an integrated layout where all processes from chip design to manufacturing, packaging, and testing are completed by one company; in the Fabless model, manufacturers are only responsible for chip design, while manufacturing and other processes are completed by foundries. Fab-lite is positioned between IDM and Fabless, offering higher flexibility. In the high-end chip manufacturing sector, the Fabless model is mainstream, but automotive CMOS is primarily dominated by the IDM model.

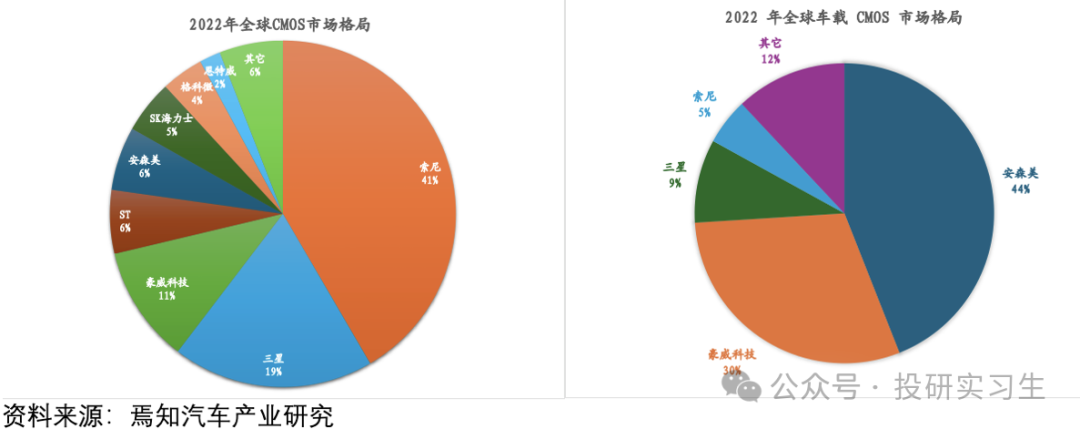

The CMOS market is highly concentrated, dominated by companies such as Sony, Samsung, and OmniVision. However, the application fields for CMOS are numerous; Sony focuses on cameras and smartphones, Samsung on smartphones, and OmniVision excels in security and automotive applications, while the American automotive semiconductor giant ON Semiconductor is a leader in the automotive CMOS field. In 2022, ON Semiconductor held a 44% share of the automotive CMOS market, followed by domestic OmniVision and South Korea’s Samsung.

OmniVision was previously a publicly listed company on NASDAQ, but was privatized after being acquired by Chinese investors such as CITIC and Huachuang in 2016, becoming Beijing OmniVision. In 2018, Will Semiconductor acquired Beijing OmniVision.

In the downstream of the industry chain, camera modules are the delivery form from suppliers to vehicle manufacturers. Camera module manufacturers are currently mostly traditional automotive Tier 1 suppliers, such as Bosch and Magna. As established core automotive suppliers, these companies provide camera modules along with domain controllers and other components as a complete solution to automakers, thus having barriers in system integration capabilities, automotive-grade verification, supply chain management, and customer relationship management.

However, as software plays an increasingly important role in smart vehicles, traditional Tier 1 manufacturers are choosing to abandon some low-profit hardware production, giving optical manufacturers the opportunity to enter the camera module production sector. Therefore, more and more optical lens and lens manufacturers are starting their camera module businesses.

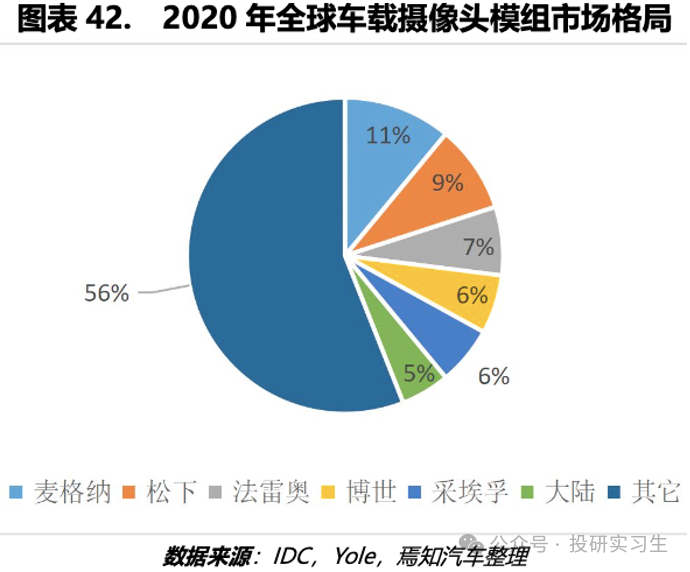

From the global market landscape of automotive camera modules in 2020, traditional Tier 1 suppliers still occupy a major position, with Magna holding a 56% share, followed by Panasonic at 9% and Valeo at 7%.

3. Market Development

The above discusses the classification, composition, and value and competitive landscape of various segments of the industry chain for in-vehicle cameras. Next, let’s look at the market space, penetration rate, and development trends for cameras.

The trend of automotive intelligence and automation is the basis for the increase in the average number of cameras installed in vehicles, whether relying on a pure vision route or a multi-sensor fusion solution, cameras are an indispensable and cost-effective hardware component of the autonomous driving perception module.

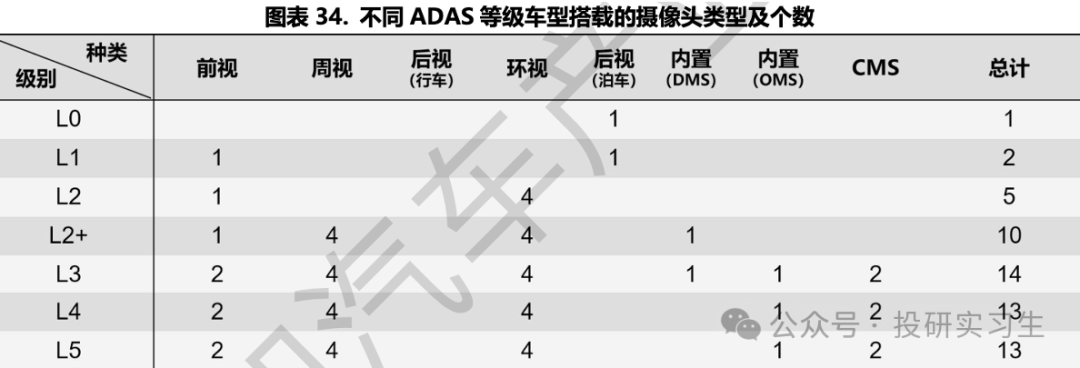

In the past, before autonomous driving, vehicles only needed a rearview camera for reversing, and many vehicles were equipped with ultrasonic radar without any cameras. With the enhancement of driving assistance levels, cameras have been installed in various aspects of vehicles, such as the current mainstream L2+ level requiring an average of 10 cameras per vehicle, indicating that there is still room for growth in the number of cameras installed as the level of autonomous driving increases.

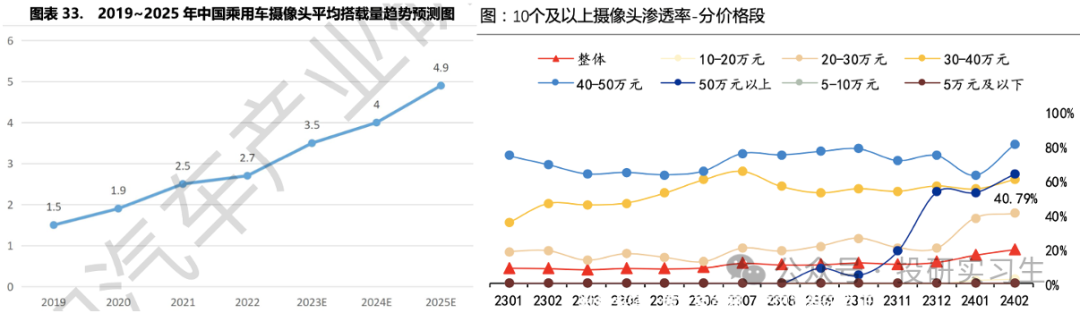

From the perspective of the entire Chinese passenger car market, it is expected that the average number of cameras installed will reach 4.9 by 2025, doubling compared to five years ago. From another set of data, by early last year, the penetration rate of vehicles with more than 10 external cameras was approaching 20%, with an accelerating trend in vehicles priced above 200,000 yuan.

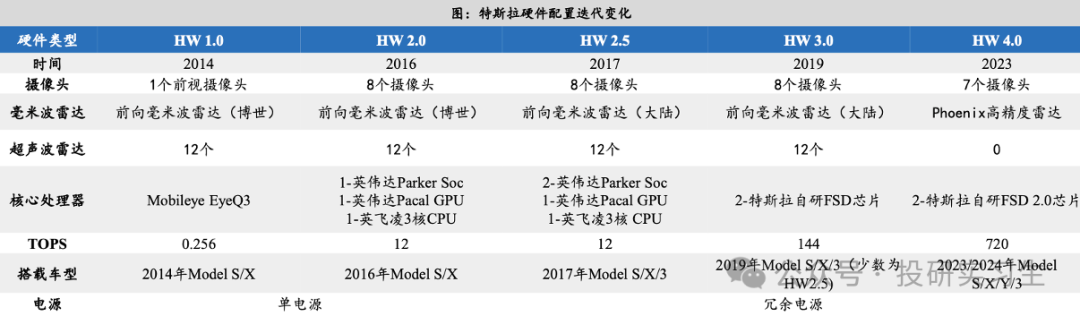

Specifically, Tesla adopts a pure vision route, with its hardware configuration evolving from 1 camera + millimeter-wave and ultrasonic radar in the HW1.0 era to 7 cameras in the HW4.0 era of 2023. Although the number of cameras has decreased from 8 in HW3.0 to 7 in HW4.0, the front camera has changed from a trino to a binocular configuration, while the pixel count has increased from 1.2 million to 5 million, and the maximum detection distance has increased from 250 meters to 424 meters.

Besides Tesla, the leading domestic high-level assisted driving models also adopt multi-sensor fusion solutions, such as Wenjie, Xiaopeng, and Li Auto models, all equipped with more than 10 cameras.

In addition to the increase in the number of cameras installed per vehicle driven by the impact of autonomous driving, the shipment volume of in-vehicle cameras will also be driven by the growth in sales of smart vehicles and overall passenger vehicle sales. According to estimates from Yiou Intelligence, the total sales of passenger vehicles in China are expected to grow at a compound annual growth rate of 3.8% from 2019 to 2025, while the penetration rates of new energy vehicles and smart electric vehicles are expected to rise from 4.7% and 14.1% to 47.4% and 80.1%, respectively, with the smart electric vehicle market expected to grow by 34.8% this year.

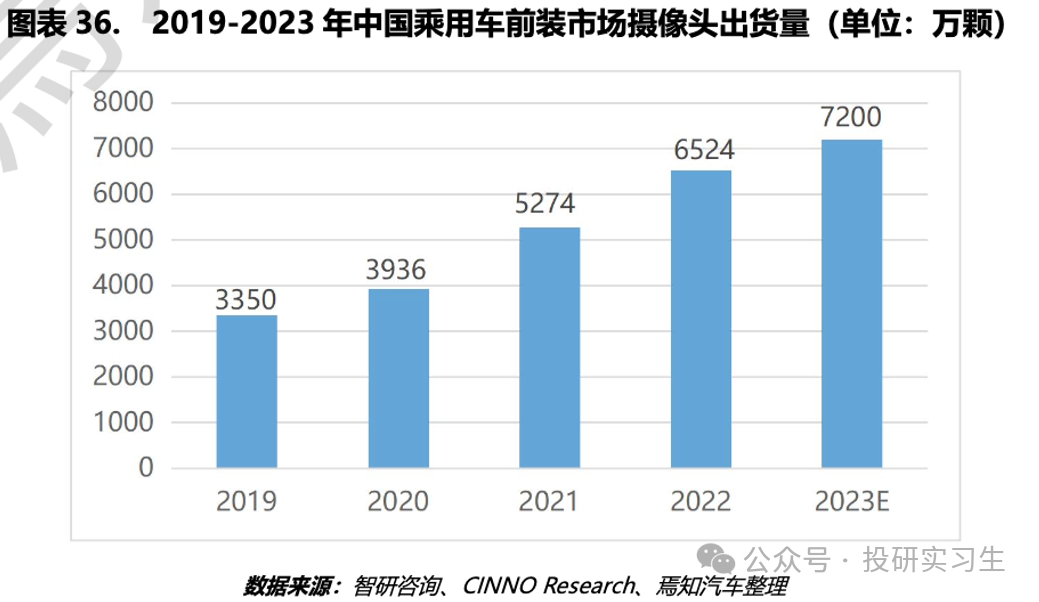

Against the backdrop of rapid market growth and increasing penetration rates, the shipment volume of in-vehicle cameras in China has maintained an average annual growth rate of 21% from 2019 to 2023, and it is expected that by 2025, the total number of in-vehicle cameras installed in domestic passenger vehicles will exceed 100 million, with a compound annual growth rate (CAGR) of 17% from 2022 to 2025.

In summary, the in-vehicle camera market has experienced a rapid growth phase and is beginning to enter a mature phase. However, driven by the development of autonomous driving and the opening of new markets, the future growth trend for cameras is very clear. In terms of classification and composition, high-resolution, wide-angle, and high-dynamic-range camera products will become mainstream. Meanwhile, front view cameras may gradually abandon the trino solution to adapt to cost control considerations; side view and surround view cameras may be replaced by ultra-wide-angle fisheye cameras, further expanding the vehicle’s field of view.

In terms of modules, there is a clear trend of de-ISP for cameras. The ability of the main control chip SoC to integrate ISP modules is increasing, which helps optimize the structure of camera modules, reduce costs, and improve signal transmission efficiency.

In the industry chain, domestic companies have gradually emerged in the field of optical lenses and lenses, breaking the previous dominance of Japanese and Korean companies; at the same time, while the automotive CMOS market remains highly concentrated, the landscape is constantly changing, with local companies striving to increase their market share. In terms of market development, driven by the increase in autonomous driving levels and the growth in smart vehicle sales, the number of cameras installed per vehicle continues to rise, and the market scale continues to expand rapidly.

Disclaimer: This article does not constitute investment advice and is for learning and reference purposes only!

References:

· Yan Zhi – Industry Analysis Report on In-Vehicle Cameras

· Hongjing Optoelectronics Prospectus

· Anjie Securities – Sunny Optical Technology (2382.HK) Leading the Optical Track, Starting a New Engine for Automotive Business

· Great Wall Securities – Haon Automotive Electronics -301488 – Focusing on Intelligent Driving Perception Track, “Vision + Ultrasonic + Millimeter Wave” Multi-Line Driving High Growth

· Tianfeng Securities – Automotive Parts Industry Penetration Rate Data Tracking ~24M2: Under the Trend of Intelligence, the Penetration Rate of LiDAR/HUD/Cameras/Electric Doors Increases

· Huafu Securities – Intelligent Driving Industry Special: NOA Rapid Penetration, Suggesting Attention to Opportunities in the Intelligent Driving Industry Chain

· Guosen Securities – Computer Industry Automotive Intelligence Series Special Report on Decision-Making (3): Tesla FSD Continuous Upgrades, Accelerating the Landing of Intelligent Driving

Welcome to follow

Investment Research Intern