Introduction: Your Phone Contains a “Circuit Highway”

When you are scrolling through short videos, playing games, working remotely, or even using navigation while driving, have you ever thought about how all these smart experiences rely on a seemingly ordinary yet crucial “board”?

It is called a Printed Circuit Board (PCB), which serves as the “skeleton” and “nervous system” of electronic products. Without it, chips cannot function, sensors cannot communicate, and the entire digital world would come to a halt.

In recent years, with the explosion of AI servers, new energy vehicles, and 5G base stations, the PCB industry, which had been quiet for years, has quietly warmed up, even being referred to as the “ballast of the electronics industry” by insiders.

In this article, we will deeply analyze this “low-key yet indispensable” core sector.

PART.1Industry Overview: What is PCB?

PCB (Printed Circuit Board) is a fundamental carrier used to support and connect electronic components. In simple terms, it is the process of “printing” copper wires on an insulating substrate to form a current path, allowing chips, resistors, capacitors, and other components to work together.

Depending on the number of layers, materials, and applications, PCBs can be classified into:

-

Rigid Boards (such as mobile phone motherboards)

-

Flexible Boards (FPC, used in foldable screens, camera modules)

-

Rigid-Flex Boards (combining strength and flexibility)

-

High-Frequency and High-Speed Boards (used in 5G and AI servers)

-

HDI Boards (High-Density Interconnect, used in high-end mobile phones)

In summary: PCBs are the “infrastructure” of all electronic devices, with a low technical threshold but rapid iteration, and demand is rigid and irreplaceable..

PART.2Industry Chain Overview: From Resin to Complete Machines, Interconnected

The PCB industry chain is clearly divided into three segments:

-

Upstream: Raw material suppliers include copper-clad laminates (CCL), copper foil, fiberglass cloth, resin, dry film, etc. Among them, copper-clad laminates account for about 40% of the cost and are the core material.

-

Midstream: PCB manufacturers are responsible for complex processes such as design, etching, drilling, electroplating, and testing, where technology, yield, and scale determine competitiveness.

-

Downstream: End application fields cover communications (5G/base stations), consumer electronics (mobile phones/computers), automotive electronics (smart cockpits/electronic control), servers (AI/HPC), industrial control, and medical applications.

China is already the world’s largest PCB producer, accounting for over 50% of global output, but high-end products still rely on companies from Japan, South Korea, and Taiwan.

PART.3Policy Planning: National Strategy Support, Accelerating Domestic Substitution

Although PCBs are part of traditional manufacturing, they have been included in several national-level strategies:

-

“14th Five-Year Plan for Intelligent Manufacturing Development”: Promoting the intelligent upgrade of the electronic circuit industry, supporting the R&D of high-layer, high-frequency, and high-speed PCBs.

-

“Action Plan for the Development of Basic Electronic Components Industry”: Clearly enhancing the self-supply capacity of high-end PCBs.

-

Local Policies: Guangdong, Jiangsu, Jiangxi, and other regions are building PCB industry clusters, providing land, tax, and environmental protection support.

Especially in the context of the Sino-U.S. technology competition, supply chain security has become a core demand—leading clients like Huawei and BYD are accelerating the introduction of domestic PCB suppliers, opening up growth space for local companies.

PART.4Market Outlook: AI and Automotive Dual-Drive, Industry Welcomes Structural Recovery

According to Prismark’s forecast, the global PCB market is expected to grow at a compound annual growth rate of about 5.3% from 2024 to 2028, but there are significant differences in sub-sectors:

-

AI Server PCBs: The value of a single unit is 3-5 times that of ordinary servers, benefiting from the ramp-up of new platforms like NVIDIA’s GB200, with an annual growth rate exceeding 30%.

-

Automotive PCBs: The number of boards used in smart electric vehicles is 3-5 times that of fuel vehicles (ADAS, domain controllers, 800V high-voltage systems), and the global automotive PCB market is expected to exceed $12 billion by 2025.

-

Consumer Electronics: Although overall demand is weak, foldable screens and AR/VR are creating new demand for FPC/HDI.

Meanwhile, after the inventory clearance in 2022-2023, the industry is entering a replenishment cycle starting in 2024, coupled with the benefits of technological upgrades, high-end PCBs are entering a “window period of simultaneous volume and price increase”.

PART.5Upstream: Material Constraints, Domestic Substitution in Progress

The core upstream material is copper-clad laminate (CCL), which is made by pressing copper foil, fiberglass cloth, and resin together.

-

Copper Foil: The process for lithium battery copper foil differs from that for PCB copper foil, and high-end low-roughness copper foil still relies on Japanese companies like Mitsui Mining & Smelting and Furukawa Electric.

-

Resin System: High-frequency and high-speed PCBs require PTFE (polytetrafluoroethylene) or modified epoxy resin, which is monopolized by American and Japanese companies.

-

Domestic Breakthroughs: Companies like Shengyi Technology, Nanya New Material, and Huazheng New Material have achieved mass production of mid-to-high-end CCL, gradually replacing Rogers and Panasonic.

Trend: Materials determine the performance ceiling of PCBs; whoever controls high-end CCL controls pricing power..

PART.6Midstream: Manufacturing Dominance, Technology + Scale Build Moat

PCB manufacturing is a typical “capital-intensive + high-tech” industry, with three key points:

-

Product Positioning: Low-end boards compete on cost, while high-end boards compete on technology (e.g., over 20 layers, line width < 50μm).

-

Customer Binding: Entering the supply chains of Apple, Tesla, and NVIDIA is equivalent to obtaining a “golden ticket”.

-

Automation Level: A 1% improvement in yield can increase gross margin by 0.5-1 percentage points.

Current Landscape:

-

Taiwanese Companies: Unimicron and Kinsus dominate high-end HDI and substrates;

-

Japanese and Korean Companies: Ibiden and Samsung Electro-Mechanics excel in packaging substrates;

-

Mainland China: Companies like Unimicron (AI servers), Jingwang Electronics (automotive), and Dongshan Precision (FPC) are rapidly rising.

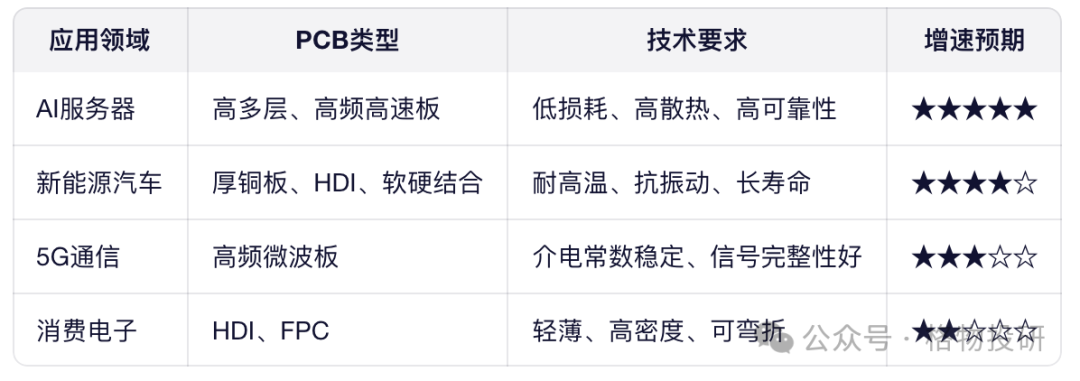

PART.7Downstream: Application Scenarios Determine Growth Ceiling

Different downstream sectors have varying requirements for PCBs:

It is evident that AI and automotive have become the strongest growth engines for the PCB industry.

PART.8Future Trends: Four Directions Reshaping the Industry Landscape

-

AI-Driven High-End Development: AI server PCBs can have 30-40 layers, with unit prices exceeding ten thousand yuan, presenting extremely high technical barriers.

-

Automotive Electronics Wave: L3+ autonomous driving requires a large number of domain controllers, with the PCB value per vehicle exceeding a thousand yuan.

-

Green Manufacturing Upgrades: Lead-free, halogen-free, and low wastewater processes are becoming standard, with environmental compliance as an entry threshold.

-

Regional Supply Chains: Accelerated factory establishment in North America and Southeast Asia, with Chinese manufacturers adopting “going global + localization” as a new strategy.

The future winning hand: Whoever can serve both the AI and automotive super tracks will be able to navigate through cycles..

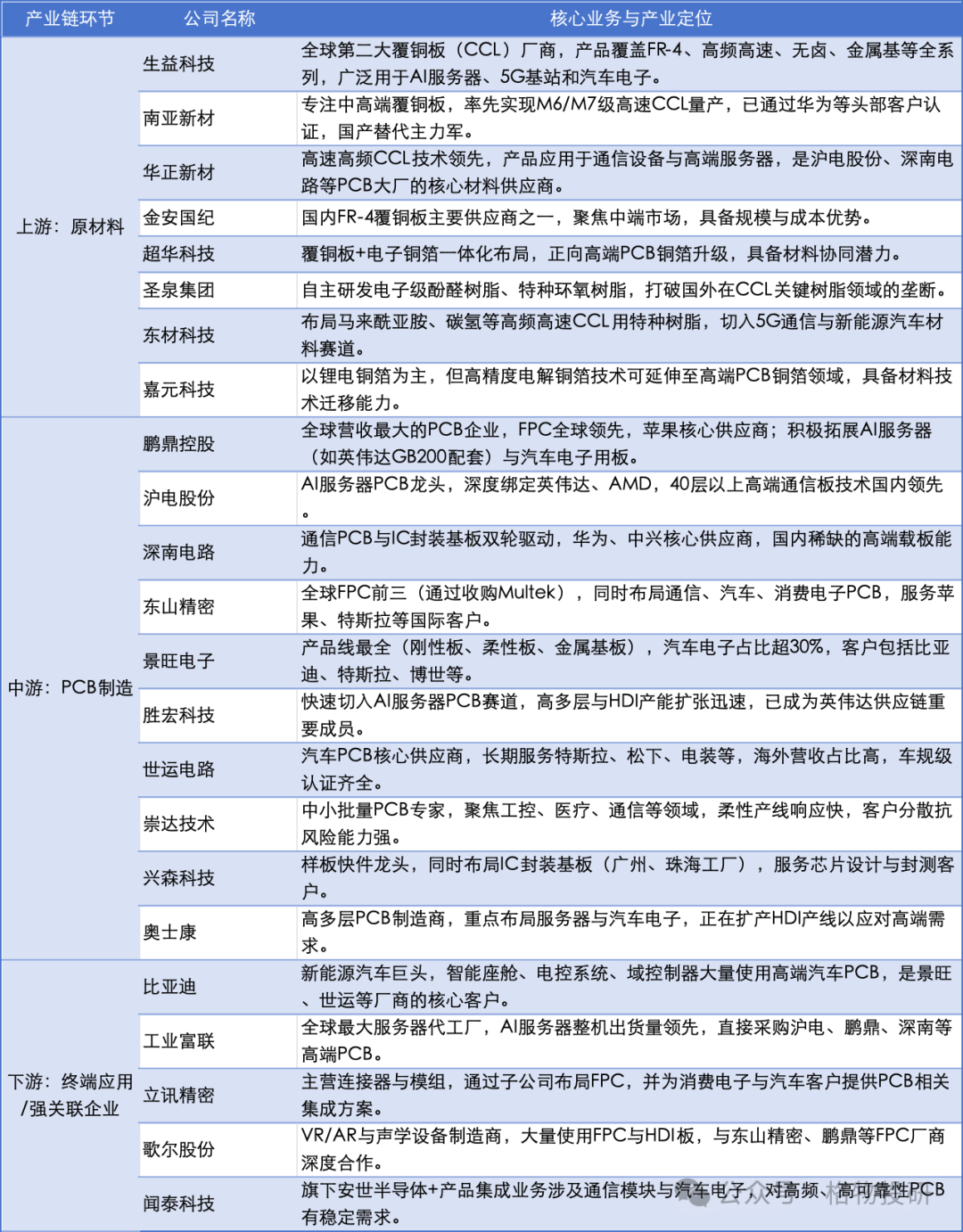

PART.9Core Companies: Who is Seizing the Next Generation PCB Heights?

The representative companies in the upstream, midstream, and downstream of the PCB industry chain are summarized in the table below:

These companies in the midstream manufacturing segment are transforming from “contract manufacturers” to “technology partners,” directly competing with international giants in the high-end market.

Conclusion:

PCB is not a sunset industry, but rather the “new infrastructure” of the intelligent era.

Many people think that PCBs are part of traditional manufacturing and are destined to be marginalized. However, the reality is quite the opposite—in the current arms race for AI computing power, the wave of automotive intelligence, and the acceleration of the Internet of Everything, PCBs, as the physical foundation of electronic systems, are experiencing unprecedented technological upgrades and value reassessment.

It may not be glamorous, but it is crucial; it may seem silent, yet it carries the pulse of the entire digital civilization.

The next time you pick up your phone or sit in a smart car, think about that invisible circuit board that is quietly changing the world.

Disclaimer: The companies listed in this article are based on publicly available information and do not constitute any investment advice. Investment carries risks, and decisions should be made cautiously.

#PCB #PrintedCircuit #AIServer #HighEndManufacturing #DomesticSubstitution