Storm clouds are gathering in the tech world.

Full text: 4617 words, reading time approximately 10 minutes

Produced by the “Fengyan” in-depth reporting team, Phoenix Technology, Phoenix News Client

Special contributor to Phoenix Technology: 丨Yang Lei

Editor: 丨Yu Hao

WeChat editor: 丨Yang Qian

*This article is the fourth lecture of “Yang Lei’s Silicon Valley Observations: Insights into Technology and Human Life”, first published by Phoenix Technology.

A significant event has occurred in the tech world, quickly making headlines across major media outlets. The renowned American graphics processing unit (GPU) company Nvidia has announced its acquisition of the world-famous chip technology company ARM for a valuation of $40 billion.

This marks the largest transaction in the semiconductor industry, resulting in the emergence of a semiconductor giant!

This will have a tremendous impact on the entire IT industry, and it will also have significant potential implications for China’s technology sector.

Industry Background

Let’s briefly describe the landscape of the chip industry.

First, let’s introduce Nvidia. Nvidia is the inventor of the GPU and a leader in artificial intelligence computing, consistently dominating the GPU market. However, in recent years, they have rapidly expanded into core technology sectors such as artificial intelligence, data centers, and cloud computing. Its CEO, Jensen Huang, is a Chinese-American known as a superhero in Silicon Valley, with many legendary stories behind his success. Remarkably, Nvidia has developed so rapidly in recent years, especially with the rapid growth of artificial intelligence and its widespread application across various fields, that Nvidia’s chips are now directly challenging the dominance of Intel in the graphics processing domain. Nvidia’s GPU products are so powerful that there are reports of people cooking eggs using the heat emitted from their early products.

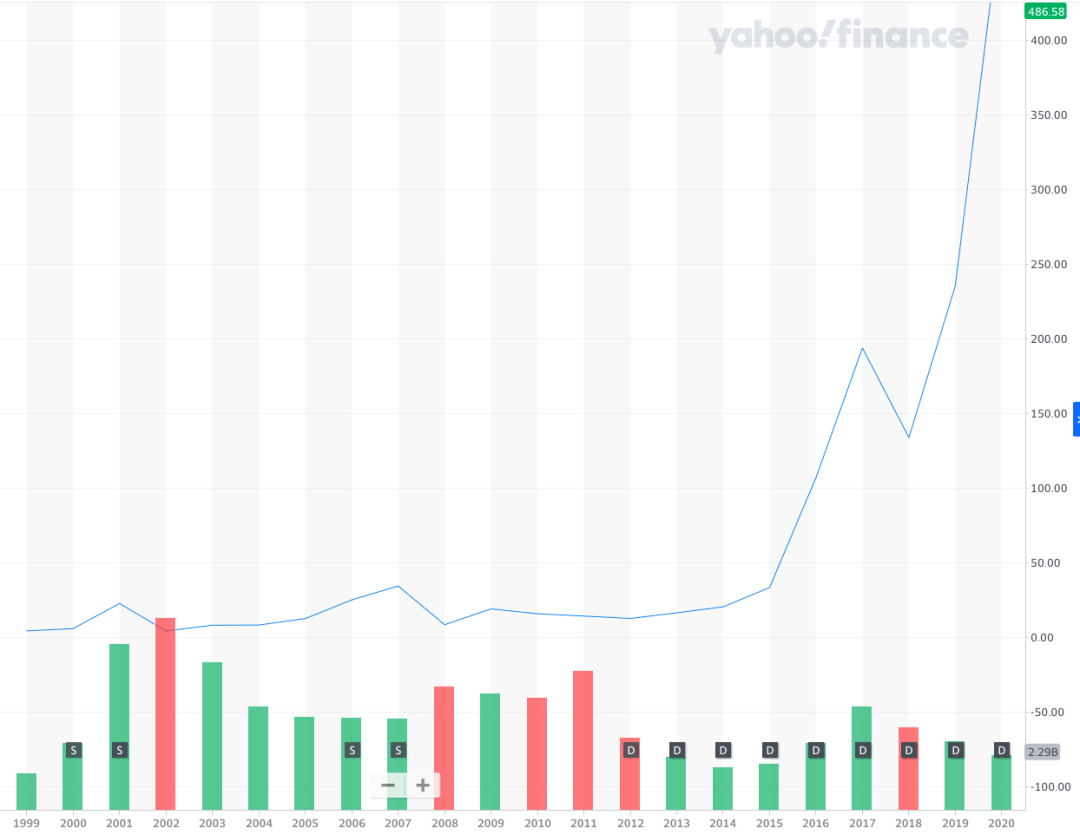

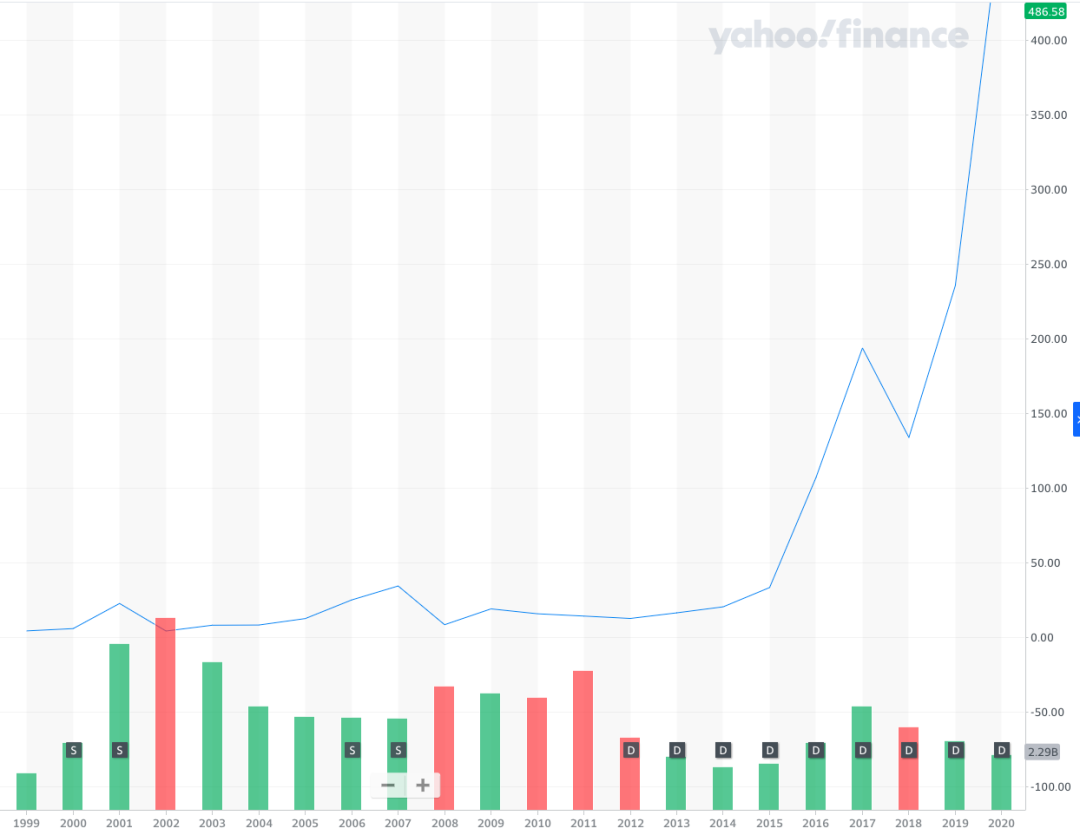

Over the years, Nvidia has surpassed the once absolute leader in semiconductor chips, Intel, in market capitalization, becoming the highest-valued company in the semiconductor industry. Its growth momentum is astonishing, with its stock price increasing 18 times over the past five years.

Nvidia’s stock price changes over the years. Source: Yahoo Finance

In contrast, ARM is a rather unique company. Originating from Cambridge, UK, ARM employs a technology called Reduced Instruction Set Computing (RISC) developed at the University of California, Berkeley. However, as a chip technology company, ARM has never sold chips to others and does not have its own manufacturing plants. Instead, it licenses its chip core architecture to industry “partners” who develop related processors and systems.

ARM’s licensing is generally divided into two types: architecture (instruction set) licensing and microarchitecture licensing.

ARM’s revenue primarily comes from licensing fees (License) and royalties (Royalty). Many devices in Samsung and Apple smartphones and tablets, as well as almost all devices produced by Qualcomm, contain ARM’s core technology. ARM’s technology is so powerful and energy-efficient that it is present in 95% of today’s smartphones, and its technology has been widely applied in Internet of Things (IoT) devices, automotive, home appliances, sensors, digital cameras, and edge computing in drones. There’s a little story: during the early development of ARM’s products, one day their engineers discovered that their chip (then called arm1) was running normally without being powered on! Researchers quickly found that the chip was being powered by a small amount of leakage current from the computer’s metal frame, allowing it to operate normally!

In 2016, Japan’s SoftBank acquired ARM for $32 billion. SoftBank’s president, Masayoshi Son, confidently hoped to leverage ARM to fully enter the IoT, 5G, and artificial intelligence sectors. However, this effort does not seem to have been very successful. If ARM’s current selling price is $40 billion, it would yield about 1.25 times the investment return in four years, which, from the perspective of return on investment, does not count as a successful transaction.

SoftBank CEO Masayoshi Son

It is also necessary to briefly mention Intel, a giant that has monopolized the semiconductor chip industry for 40 years. Intel’s core technology originates from its x86 architecture, and it is needless to say that Intel’s technology is ubiquitous across various industries, especially with its iconic jingle and the slogan “Intel Inside” making it a household name. Intel has powerful CPU capabilities. However, since the boom of the wireless mobile communications industry, ARM has penetrated every mobile communication terminal and edge computing sector with its unique technology and business model, due to its powerful functionality and particularly outstanding power efficiency, which has posed a significant challenge to Intel. Over the past few years, Intel and ARM have been fierce rivals; a simple analogy is that Intel is like a powerful giant truck that can easily haul a full load of ore uphill or take a group of children on vacation, but it consumes a lot of energy. In contrast, ARM is more like a sleek electric vehicle, very agile and energy-efficient. The market competition between Intel and ARM is primarily about penetrating each other’s markets. So far, neither side has made significant progress. Thus, the story returns to Nvidia’s acquisition of ARM. Interestingly, ARM, which originally aimed to compete with Intel, may now be subservient to Nvidia to directly compete with its long-time rival, Intel.

The Impact of the Merger

First, Nvidia’s acquisition of ARM will further shuffle and consolidate the chip industry.

Nvidia chips have always been used for data-intensive tasks, with typical applications including gaming on gaming computers, scientific research computing, artificial intelligence, autonomous driving, and even high-intensity computing for blockchain mining. The combination with ARM will help Nvidia enter a series of fields it has long desired to penetrate, such as smartphones, 5G, edge computing, wireless devices, IoT, and robotics.

From a technical perspective, Nvidia’s essence and core technology is that of a GPU (graphics processing unit) company, and its strength in CPUs is still considerably behind Intel and AMD, especially in complex computing and large data centers. For example, it recently lost a bid to Intel and AMD in a project from the U.S. Department of Energy. Therefore, the organic combination of ARM’s CPU technology and its team’s talent advantage will make Nvidia a super powerful company in the integration of CPU and GPU.

Nvidia founder and CEO Jensen Huang

Secondly, the combination of Nvidia and ARM undoubtedly creates a triopoly with Intel and AMD, making the competition in high-intensity servers and data centers even more fierce. With Nvidia’s strength and its graphics processing capabilities, ARM will also become more formidable in its wireless mobile terminal sectors.

The Impact on China’s Industry

The most concerning aspect of this potential merger for the domestic audience is the complex impact it will have on China’s current technology market. It is well known that China is a major producer of smartphones, and the core technology of most smartphones relies heavily on ARM technology. SoftBank revealed in 2018 that approximately 95% of all advanced chips designed in China are based on ARM technology, and China contributes 20% of ARM’s total sales. In the past, since ARM was a Japanese and British company, it was not subject to the sanctions and restrictions of the U.S. long arm jurisdiction in many areas. ARM China has also repeatedly stated, “We have never cut off supply and have always supported Huawei, including the release and continuous shipment of Huawei products. Secondly, our ARM China products are based on British architecture. It can be seen that our V8 architecture and subsequent architectures have been clearly defined, and these two products can continue to supply to Chinese customers, including Huawei, under legal and compliant conditions.” In May 2017, to accelerate ARM’s global strategy and support the further development and independent innovation of China’s IC industry, ARM signed a memorandum of cooperation with the Huanan Innovation Fund to establish a joint venture in Shenzhen, China, with Chinese control, where ARM would provide the core intellectual property, technical support, and training needed for chip design.

However, times have changed, and the situation is no longer the same. Recently, the U.S. has been tightening its technological suppression of China, targeting critical areas. And now ARM is set to become a fully American company.

When addressing the above issues, it becomes clear that the real problems are far more complex.

First, the architecture of chips is closely linked to operating systems. Currently, the mainstream operating systems for mobile devices are only Android (Google’s Android system) and iOS (Apple). Taking Huawei’s Kirin 980 chip as an example, the main components are the CPU and GPU Cortex-A76 and Mali-G76, which are microarchitecture licenses purchased from ARM. The Android system used on smartphones is tightly coupled with ARM architecture, not to mention the need for a series of development tools provided by ARM. Imagine if one day ARM were to cut off supply; it would be extremely difficult to support another currently non-mainstream microarchitecture and corresponding development tools (such as RISC-V) with the Android system. This is a fatal problem facing every smartphone manufacturer in China today! If we rephrase this issue, it would be: the U.S. has already dealt a heavy blow to Huawei by placing it on the entity list, meaning that U.S. technologies will be cut off or banned for Huawei. If the U.S. technology were to impose a blockade on all Chinese smartphone manufacturers, what kind of situation would they face? I believe many industry insiders do not wish to see this happen, and the impact would be unimaginable.

In fact, when discussing whether ARM would impose a ban on China’s industry, we must mention a recent message from the U.S. Department of Defense, which indicated that it might impose sanctions on China’s largest and relatively advanced wafer foundry, SMIC. It is well known that SMIC is China’s largest and most technologically advanced wafer foundry. However, most of SMIC’s main production equipment and materials come from the U.S. and other Western countries. If equipment and materials are cut off, it will severely impact the production of the next generation of chips. In the semiconductor industry, wafer manufacturers are akin to construction material suppliers in the construction industry; without building materials, it is very difficult to construct any kind of building, and without wafers (chips), it is impossible to produce any (high-end) smartphones or other electronic devices. In fact, when worrying about the sale of ARM, we should be more concerned about the future of chips, because as the saying goes, without the skin, where will the hair attach?

Industry Solutions

1. Import substitution is a necessary path. It is not difficult to imagine that China has already and will continue to see the emergence of more and more startups in various segments of the semiconductor industry. Given the current capital, talent, direction, and market conditions, the only remaining factors to catch up with the world’s advanced level are a good investment environment and time. This is a necessary path, and there are no other choices left.

2. Actively integrate into the global innovation network to enhance technological innovation capabilities through open cooperation. The more we face blockades, the more we need to adopt an inclusive and mutually beneficial attitude to engage with the world and attract top talent, particularly leveraging capital to go overseas for win-win investment cooperation.

3. Optimize domestic capital directed towards the semiconductor industry. The semiconductor industry, like many high-tech developments, does not necessarily progress faster with more money. In fact, unreasonable or unprofessional use of capital and investment can lead to a detrimental effect on the market, driving out good companies and entrepreneurs. Capital operations and industry development must involve deep participation from industry and investment experts.

4. Give up illusions. Academician Ni Guangnan of the Chinese Academy of Engineering stated in a media interview that incidents like “ZTE” and “Huawei” serve as a wake-up call for the entire nation, highlighting the shortcomings and necessities of the chip industry, which has a positive side. To break through this core technology, China must be prepared for a long-term commitment. This means that China must enter a second phase of “hiding its light and biding its time” in technological innovation development. The semiconductor industry indeed requires hard work and meticulous effort, and it may take many years or even a decade to catch up.

Possibility of Acquisition Failure

Although Nvidia has announced its acquisition of the British chip designer ARM from SoftBank Group, there are still some uncertainties surrounding this merger. First, this acquisition breaks ARM’s original market neutrality, which will complicate its relationships with current partners. Therefore, it may provoke backlash from the industry, especially from large companies like Apple and Samsung, which may react sensitively to the new landscape. On the other hand, relevant governments may use antitrust laws to oppose this merger, which poses a significant challenge to the success of the acquisition. Third, the UK government may be reluctant to see such a merger occur. As a high-tech company, ARM is one of the few outstanding companies in the UK IT industry and a source of national pride. Although the UK and the U.S. are like brothers, the situation will be different once this company is acquired by an American company. The reason is that SoftBank is merely a giant fund, and its acquisition was primarily a change of shareholders, more at the capital level. However, if ARM is acquired by Nvidia, according to industry norms, this company will gradually be absorbed and digested by the acquiring company over the years.

Yang Lei

September 14, 2020, in Silicon Valley

Author’s Biography: Yang Lei, currently residing in Silicon Valley/Beijing, is a partner at Huashan Capital Management and co-chair of the Silicon Valley High-Tech Innovation Association. He previously served as CEO of Palm Ling Tong and has over 25 years of cross-border investment and management experience in the technology sector between China and the U.S.

This article is authorized by iFeng Technology and published by Yiou. For article authorization requests, please contact the original source.

RECOMMENDED READINGS