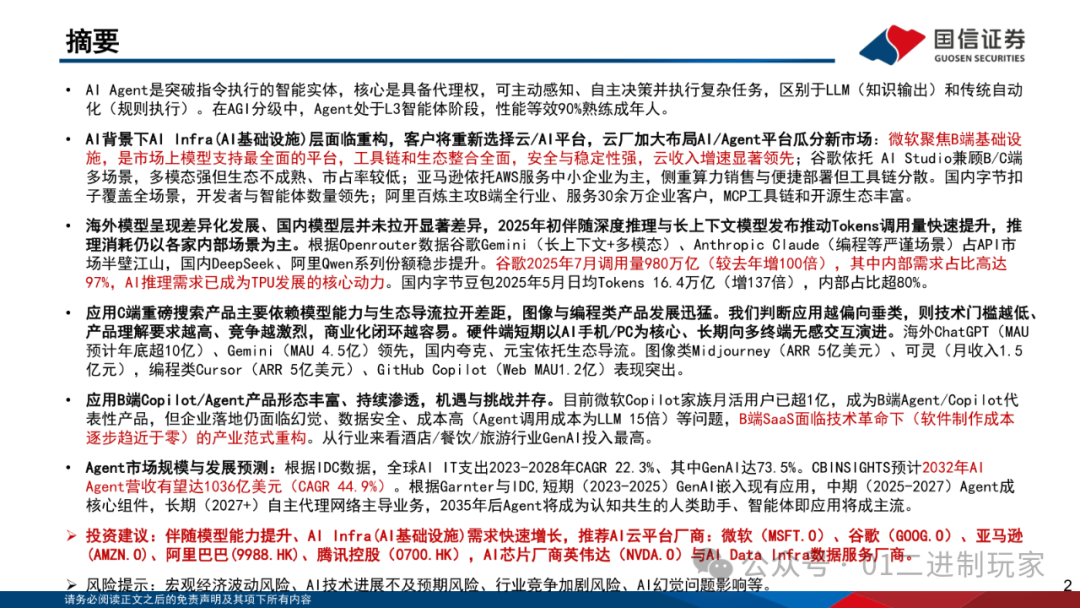

This report, published by Guosen Securities, focuses on the current status and development trends of AI Agent development platforms, models, and applications. It systematically analyzes the definition, technical architecture, market landscape, application progress, and future predictions of AI Agents. The report points out that AI Agents are intelligent entities with autonomous decision-making and execution capabilities, positioned at the L3 stage of AGI classification, with performance equivalent to that of 90% of skilled adults. In the context of AI, the AI infrastructure layer is facing reconstruction, with cloud vendors increasing their layout of AI/Agent platforms to capture new markets. Investment recommendations include AI cloud platform vendors, AI chip manufacturers, and AI Data Infra data service providers, with risk warnings including macroeconomic fluctuations and technological advancements falling short of expectations.Download method is at the end of the article.

Definition, Technology, and Development of Agents

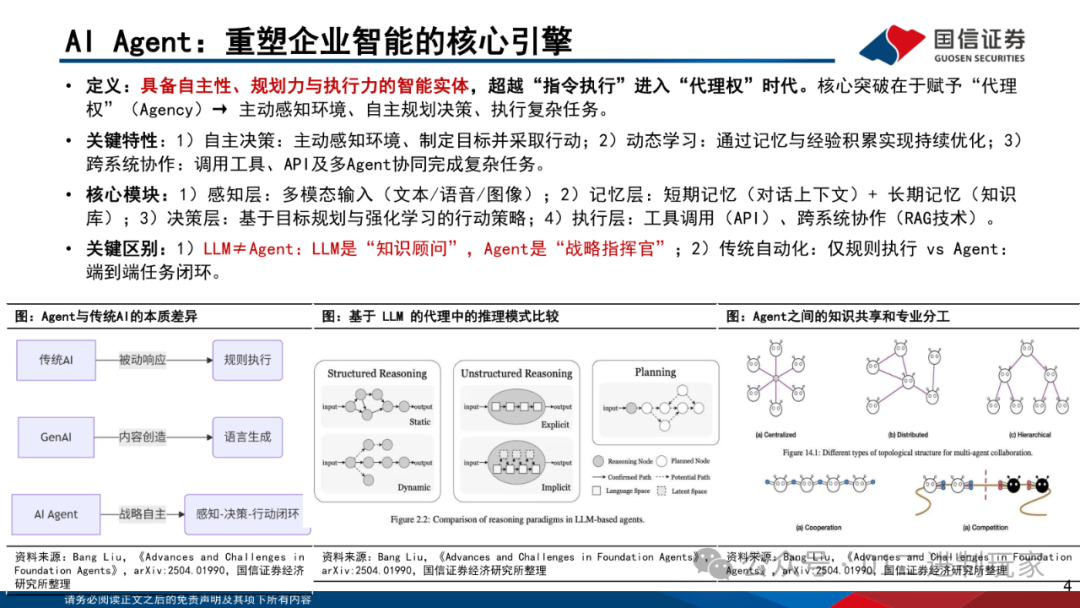

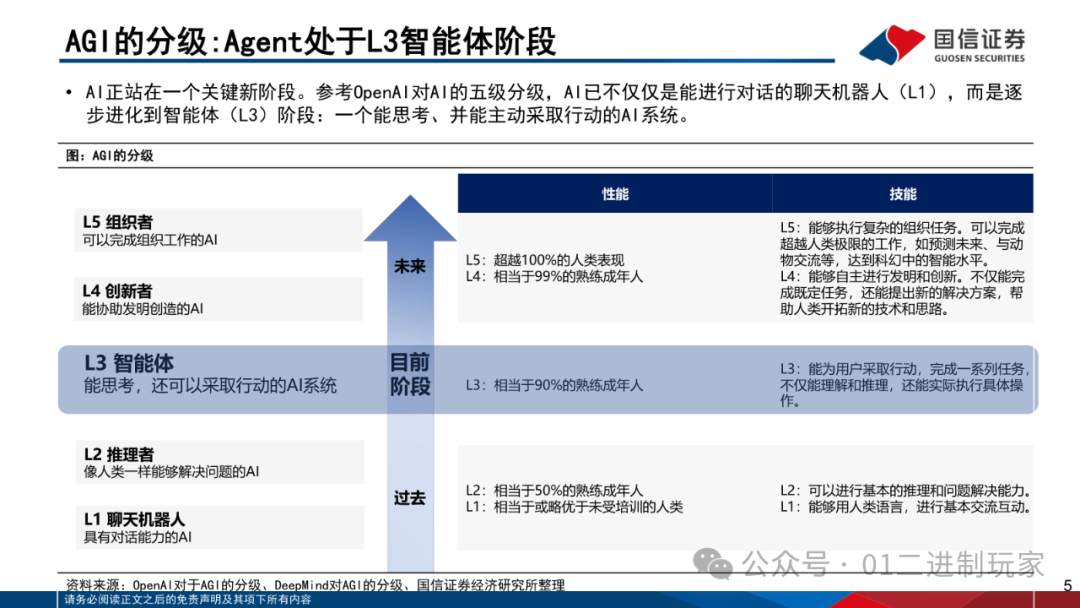

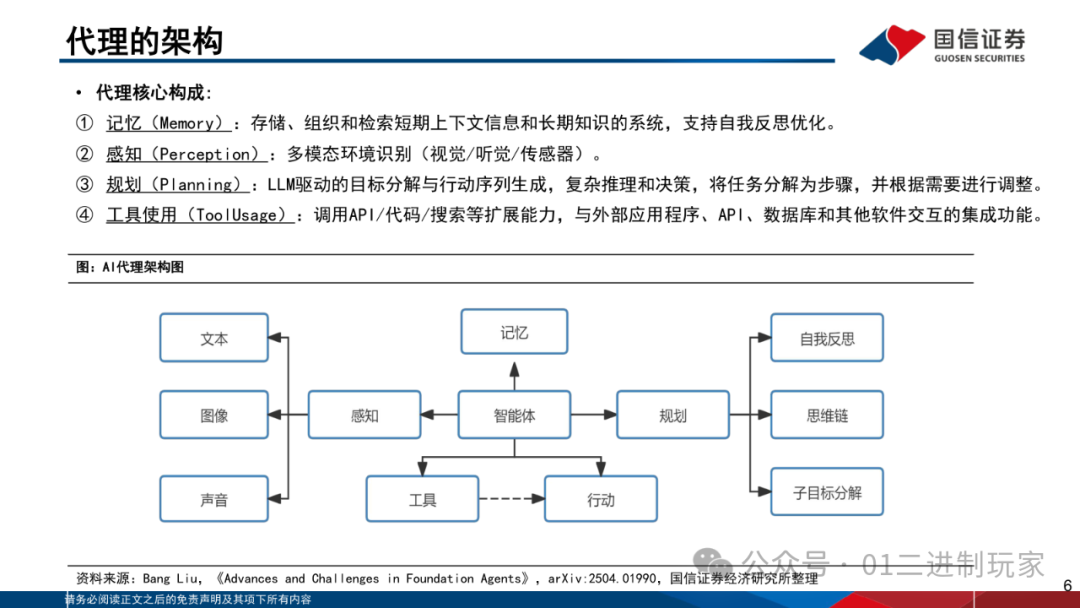

AI Agents are intelligent entities that break through command execution, with the core being the ability to act as agents, proactively perceive, make autonomous decisions, and execute complex tasks, distinguishing them from LLMs (knowledge output) and traditional automation (rule execution). In the AGI classification, Agents are at the L3 intelligent agent stage, with performance equivalent to that of 90% of skilled adults. Key features include autonomous decision-making, dynamic learning, and cross-system collaboration. The core modules encompass the perception layer, memory layer, decision layer, and execution layer. The essential difference between Agents and traditional AI is that LLMs are “knowledge consultants,” while Agents are “strategic commanders”; traditional automation only executes rules, while Agents achieve end-to-end task closure.

Layout of Agent Development Platforms

In the context of AI, the AI Infra layer is facing reconstruction, and customers will reselect cloud/AI platform providers. According to IDC data, 70% of surveyed enterprises will change or add cloud/AI platform suppliers, with only 17% believing that their current cloud providers can meet AI/ML/GenAI needs. Nearly half of enterprises rely on public cloud PaaS service providers for AI solution implementation. The key demands of PaaS platforms revolve around improving delivery efficiency in the GenAI application development process, with AI-driven workflow automation being the primary requirement. The main obstacles to the implementation of AI solutions are security and privacy issues (19%), followed by data quality (15%) and insufficient IT department capabilities (13%).

Model Layer and Tokens Call Volume Analysis

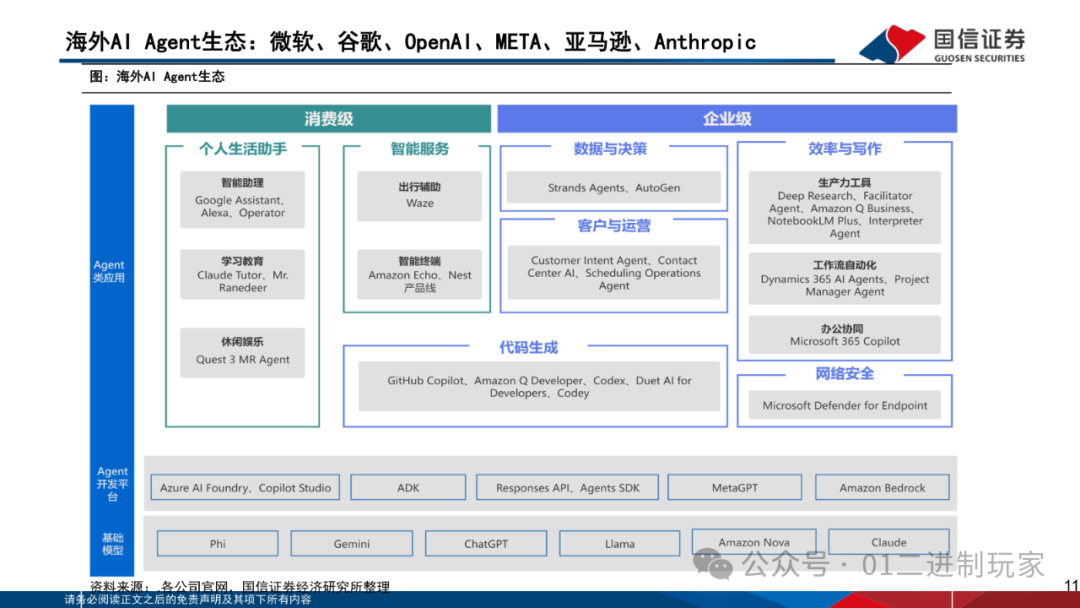

Overseas models show differentiated development, while domestic model layers have not shown significant differences. According to Openrouter data, Google Gemini (long context + multimodal) and Anthropic Claude (rigorous scenarios such as programming) account for half of the API market, while domestic DeepSeek and Alibaba’s Qwen series are steadily increasing their market share. Google is expected to have a call volume of 980 trillion by July 2025 (a 100-fold increase from last year), with internal demand accounting for as much as 97%. AI inference demand has become the core driving force for TPU development. Domestic ByteDance’s Doubao is expected to have an average daily token volume of 16.4 trillion by May 2025 (a 137-fold increase), with internal demand exceeding 80%.

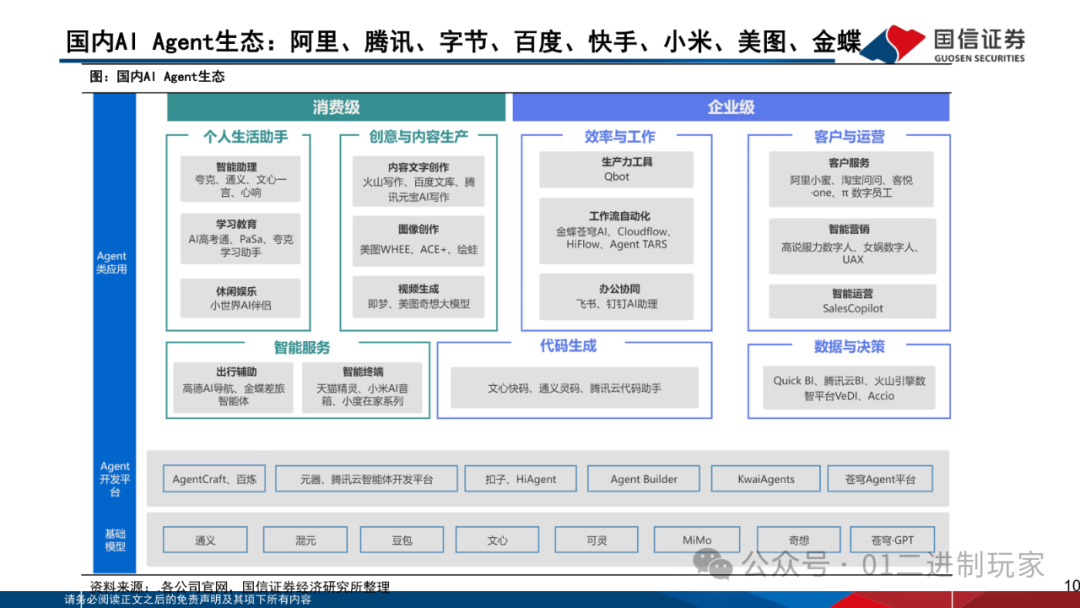

Progress of C-end and B-end Agents

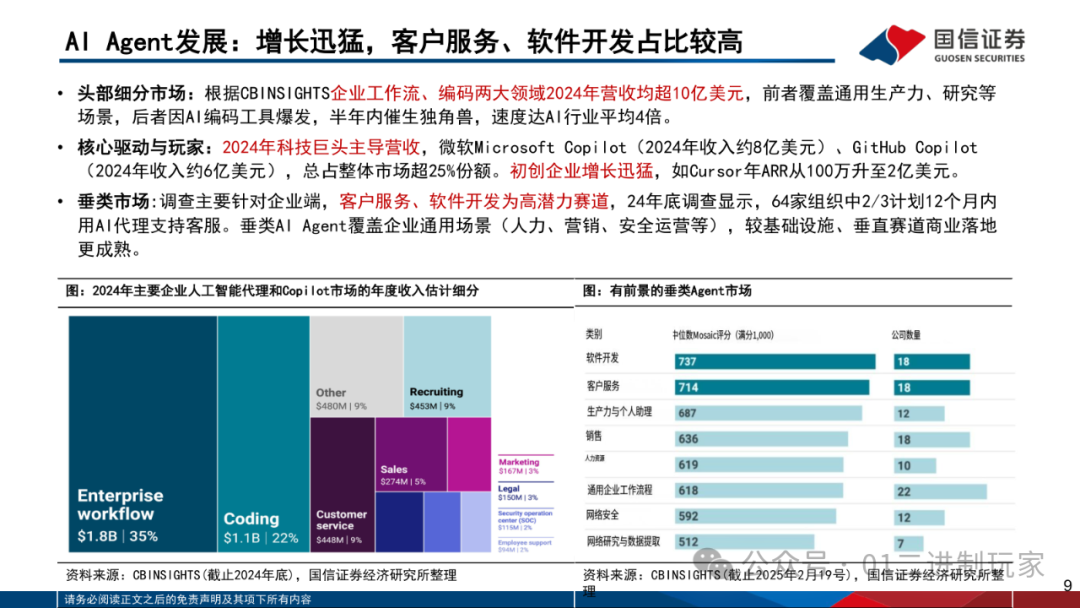

C-end heavyweight search products mainly rely on model capabilities and ecological drainage to create differences, with rapid development in image and programming products. The more specialized the application, the lower the technical threshold, the higher the product understanding requirements, the more intense the competition, and the easier the commercialization loop. In the short term, hardware will focus on AI smartphones/PCs, evolving towards multi-terminal seamless interaction in the long term. Overseas, ChatGPT (expected MAU to exceed 1 billion by the end of the year) and Gemini (MAU 450 million) lead, while domestic Quark and Yuanbao rely on ecological drainage. Image products like Midjourney (ARR $500 million) and Keling (monthly income $150 million), as well as programming products like Cursor (ARR $500 million) and GitHub Copilot (Web MAU 120 million) perform outstandingly.B-end Copilot/Agent product forms are diverse and continuously penetrating, presenting both opportunities and challenges. Currently, the monthly active users of Microsoft’s Copilot family have exceeded 100 million, making it a representative product of B-end Agents/Copilots, but enterprises still face issues such as hallucinations, data security, and high costs (Agent call costs are 15 times that of LLMs). B-end SaaS is facing a paradigm shift in the industry under a technological revolution (the cost of software production is gradually approaching zero). From an industry perspective, the hotel/restaurant/tourism sector has the highest investment in GenAI.

Market Space and Development Expectations for Agents

Global AI IT spending forecasts show that from 2023 to 2028, global AI IT spending will continue to grow, with a compound annual growth rate (CAGR) of 22.3% for the total market. Among them, GenAI has a CAGR of 73.5%, while other AI has a CAGR of 22.3%. By 2028, AI technology spending will account for 16.4% of total IT spending, with generative AI (GenAI) itself accounting for 6.7% of the spending.Investment recommendations, along with the improvement of model capabilities and the rapid growth of AI Infra (AI infrastructure) demand, recommend AI cloud platform vendors: Microsoft (MSFT.0), Google (GOOG.0), Amazon (AMZN.0), Alibaba (9988.HK), Tencent Holdings (0700.HK), AI chip manufacturer NVIDIA (NVDA.0), and AI Data Infra data service providers. Risk warnings include risks of macroeconomic fluctuations, risks of AI technology advancements falling short of expectations, risks of intensified industry competition, and issues related to AI hallucinations.

Some content screenshots, download method is at the end of the article

(This content is produced by Guosen Securities and others, copyright belongs to the author)

(This content is produced by Guosen Securities and others, copyright belongs to the author)

Data Download Method

Follow this public account and reply:

GX

to receive the complete data.

You may also be interested in these contents:

-

Must-read for college entrance examination volunteer filling, Tsinghua University AI tutorial “AI Empowering Education+: Guide to Using College Entrance Examination Volunteer Filling Tools” (Free PDF Download)

-

Peking University, Application of DeepSeek in Educational Scenarios (135 pages, Free Download)

-

Peking University DeepSeek Internal Seminar, 99 pages on DeepSeek and AIGC Applications (Free Download)

-

Peking University DeepSeek Internal Seminar, 80 pages on DeepSeek Prompt Engineering and Implementation Scenarios (Free Download)