1. Analysis of Recent Market Performance in the Robotics Sector

Sector Index Correction: In the past two weeks, the humanoid robot sector has seen a significant correction. Two weeks ago, the humanoid robot index fell by 5.86%, underperforming the CSI 300 by about 1.9 percentage points; last week, the sector index dropped by 2.82%, underperforming the CSI 300 by about 1.74 percentage points.

Reasons for the Correction and Industry Background: The main reason for the sector’s correction is the substantial increase in previous periods, but recently the industry has lacked substantial catalysts, affecting market sentiment.

2. Progress and Innovations in Yushu Technology Products

Listing Guidance and Product Release Schedule: Yushu Technology entered the listing guidance period in July 2025 and completed it in just four months by October, exceeding expectations. During and after the listing guidance period, Yushu has continuously launched several new products. On July 25, the R1 humanoid robot was released, supporting development and modification, weighing approximately 25 kg, integrating multimodal large models for language and image processing, emphasizing lightweight and flexibility, with 26 degrees of freedom in joints, capable of performing complex movements, starting at a price of about 39,900 yuan, lower than most robots in the 200,000 to 500,000 yuan price range, thus lowering the barrier for the general public to own humanoid robots. In August, the interstellar hunting quadruped robot was released, weighing 37 kg, with a range of 20 km when unloaded, a maximum speed of 5 meters per second, and a climbing height of 1 meter; with a load of 30 kg, it has a range of over 3 hours, covering a distance of 12.6 km, equipped with two industrial laser radars. In October, the second full-size humanoid robot H2 was launched, standing about 1.8 meters tall and weighing 70 kg (H1 weighs 47 kg), with 31 degrees of freedom (an increase of over 60% compared to H1’s 19), distributed as 6 for each arm, 7 for each leg, 3 for the torso, and 2 specific function joints for controlling dynamic balance, supporting complex movements such as dance and martial arts, with smooth motion; it features a wide shoulder and narrow waist design, resembling human form more closely, and is equipped with a bionic face. On November 13, the wheeled dual-arm robot GED was launched, marking Yushu’s third general humanoid application solution.

Innovations of the GED Wheeled Robot: The GED wheeled robot consists of a body, data collection tools, model training, and inference tools, applicable in service, life, commercial, and industrial scenarios. Unlike Yushu’s previous humanoid robot technology route (biped design), the most significant change in GED is the abandonment of the biped design, replacing the lower body structure with wheels, marking its first wheeled dual-arm robot.

3. Comparison of Different Robot Technology Routes

Advantages and Disadvantages of Biped and Wheeled Robots: Biped robots face technical challenges: they need to simulate human-like gait, which is difficult to control; they have high energy consumption, require high dynamic balance, and may fall on uneven ground or when encountering small stones, demanding higher algorithm and dynamic balance capabilities; currently, applicable scenarios are not demanding, mainly targeting simple industrial or indoor environments, but they have advantages in complex terrains (such as climbing stairs or slopes). Wheeled robots have performance advantages: they have a more stable chassis, a lower center of gravity, walk smoothly, and are less likely to fall; they only need to overcome friction for movement, resulting in lower energy consumption and better range (for example, Yushu’s flagship wheeled robot is equipped with a 30-degree battery, allowing for 6 hours of continuous operation); they are suitable for simple industrial or indoor environments, with lower control difficulty (only requiring upper body control, while the lower body is managed by the wheeled structure).

Classification of Mainstream Manufacturers’ Technology Routes: Current mainstream manufacturers’ technology routes can be classified into five categories: the first category adheres to the biped technology route, with no plans for wheeled solutions in the short term, such as Tesla’s Optimus; the second category promotes biped robots first, then equips wheeled or chassis based on customer needs; the third category insists on wheeled solutions, as developing biped robots is costly, with no plans for biped in the short term; the fourth category mainly promotes wheeled robots, with future plans to expand into biped robots; the fifth category adopts a multi-form layout, launching both wheeled and biped robots, providing modular options based on customer and scenario needs. Among them, biped robots are considered the ultimate form due to their ability to replicate human form and possess the strongest scene generalization capability; wheeled and wheeled-legged solutions serve as a transition, being more cost-effective and applicable in simple industrial scenarios.

4. Trends in Robot Industrialization and Investment Recommendations

Outlook on Future Industrialization Processes: From the perspective of industrialization, wheeled or wheeled-legged robots are easier to deploy due to their low cost, suitable for the B-end; biped robots are challenging to develop but have strong scene generalization capabilities, suitable for the C-end. Both types of robots have their advantages and disadvantages, and in the future, a diverse range of multi-form solutions will emerge, complementing each other in various scenarios. The concept of embodied robots is more generalized, not limited to humanoid forms, as long as they are equipped with embodied intelligence. It is expected that by the end of 2025 to early 2026, various mainstream manufacturers will launch refined products; after mass introduction, costs will rapidly optimize, initially entering B-end scenarios, then accumulating data to feed back to the C-end.

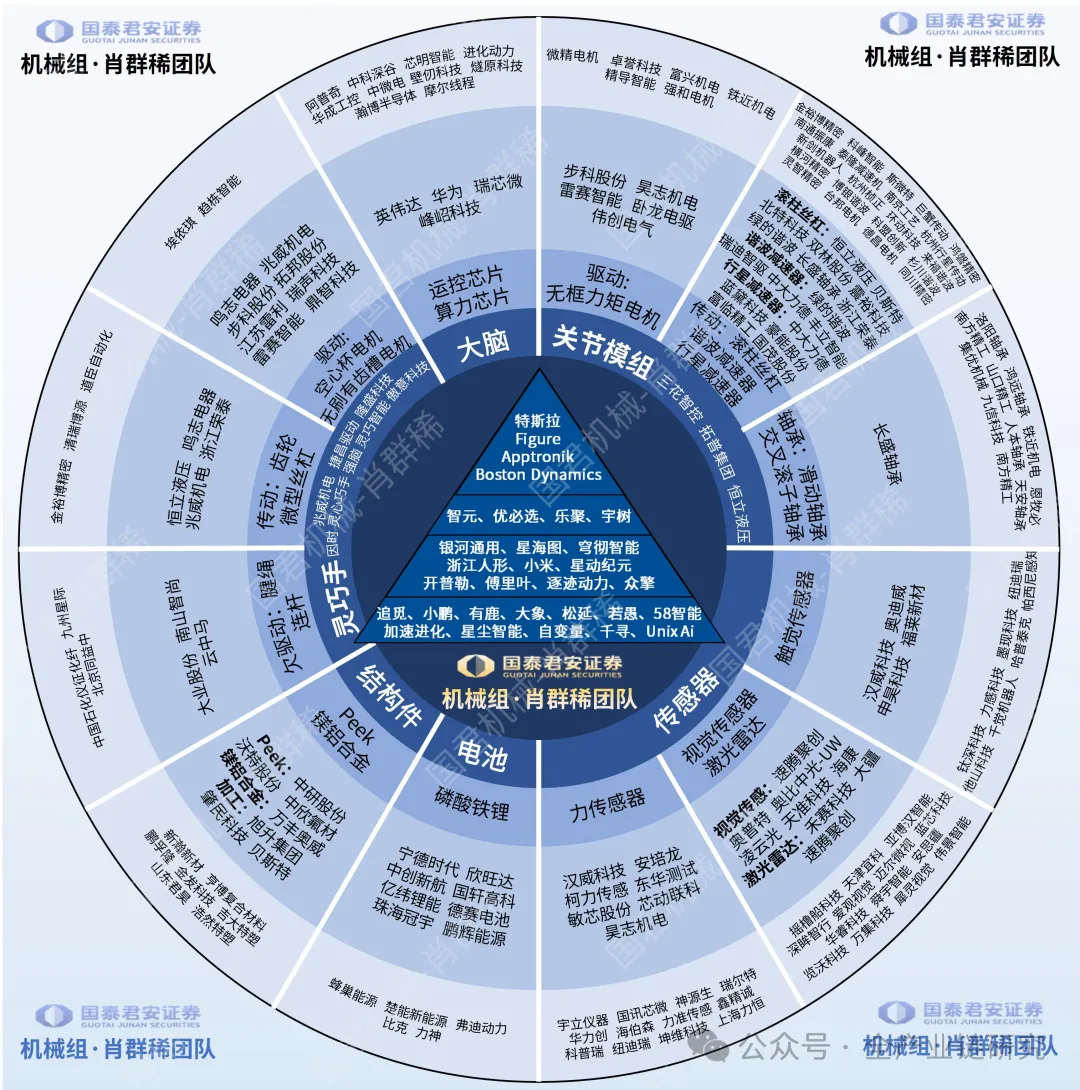

Key Investment Focus: Investment recommendations should focus on two types of entities: first, the main manufacturers, such as Xpeng, Xiaomi, and Changan Automobile; second, the core component sectors, as humanoid robots will bring specialized and incremental components, with significant market potential, such as sensors, servo motors, screws, and sensor cables, which hold future investment opportunities.