In recent years, industries such as new energy vehicles, photovoltaics, and wind power have continued to expand. Coupled with the gradual implementation of new technologies like wide bandgap semiconductor materials, power semiconductors have become a key area of market focus.

In recent years, industries such as new energy vehicles, photovoltaics, and wind power have continued to expand. Coupled with the gradual implementation of new technologies like wide bandgap semiconductor materials, power semiconductors have become a key area of market focus.

Fuji Economic noted in a report earlier this year in April: The power semiconductor market will be impacted by inventory accumulation in 2024 . Demand is expected to recover starting in the second half of 2024, with inventory anticipated to return to normal levels in the second half of 2025.

So how is the recovery of power semiconductors currently? With the performance disclosures of leading domestic power semiconductor companies, the market direction is gradually becoming clear.

Power semiconductor companies,

Who are the top performers?

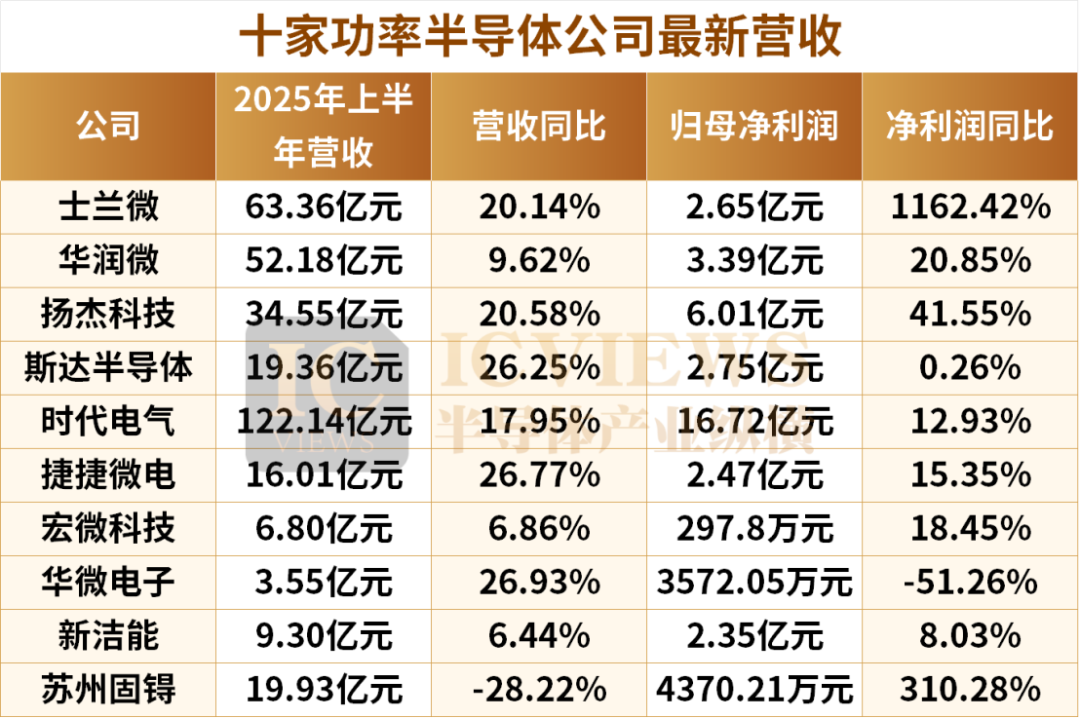

Among the ten power semiconductor companies mentioned above, the standout performer is Silan Microelectronics.

The company’s revenue for the first half of the year was 6.336 billion yuan, a year-on-year increase of 20.14%; net profit attributable to shareholders was 265 million yuan, a year-on-year increase of 1162.42%.This achievement is attributed to the company’s continuous expansion in high-barrier markets such as large home appliances, automotive, and new energy, as well as the full-capacity production of subsidiaries Silan Integrated and Silan Jixin..

Among the ten companies, only one experienced a year-on-year decline in revenue—Suzhou Goodix, but the company saw a net profit increase of over 300%; Huayi Electronics saw a year-on-year decline in net profit but an increase in revenue.

Power semiconductors include power semiconductor discrete devices (including modules) and power IC etc. Among them, power semiconductor discrete devices can be classified into diodes, thyristors, and transistors based on device structure. Among power semiconductor discrete devices, transistors represented by MOSFET and IGBT account for the largest share, nearly 30%. From the current market demand perspective, silicon-based MOSFET, silicon-based IGBT and SiC are the main products of power semiconductor discrete devices.

Currently, Chinese power semiconductor companies are still in the early stages, and while the market concentration is relatively low, it is rapidly growing.

Upon detailed analysis of the financial reports of the ten power semiconductor companies, I found two high-frequency terms: “automotive” and “SiC.”

Silan Microelectronics:SiC business revenue surged 80%

Silan Microelectronics’ revenue from power semiconductors and discrete device products reached 3.008 billion yuan, a year-on-year increase of about 25%, with revenue from automotive and photovoltaic applications of IGBT and SiC (modules, devices) increasing by over 80% year-on-year.

In the first half of 2025, Silan Microelectronics’ electric vehicle main motor drive module shipments based on the second-generation SiC-MOSFET chip reached 20,000 units, with positive client feedback and a continuous increase in customer numbers. Additionally, the company’s next-generation products are about to ramp up, and Silan Microelectronics’ fourth-generation SiC chips and modules have been sent for customer evaluation, with power modules based on the fourth-generation SiC chips expected to ramp up in the second half of 2025. This will help enhance the company’s technological competitiveness in the SiC field and meet market demand for high-performance SiC products.

Currently, Silan Mingjia has formed a monthly production capacity of 10,000 pieces of 6-inch SiC-MOSFET chips, providing strong production support to meet market demand..

It is reported that Silan Microelectronics is actively engaging in deeper cooperation discussions with several leading domestic new energy vehicle companies and Tier 1 suppliers for next-generation models. The focus is mainly on its upcoming mass production of fourth-generation SiC power modules and automotive-grade MCU, high-voltage drive chips, and other products..

Star Semiconductor: Half-Year Performance Driven Mainly by New Energy Business,SiC Enters Mass Production Ramp-Up Stage

Star Semiconductor’s financial report shows that the new energy industry revenue for the first half of the year was 1.213 billion yuan, a year-on-year increase of 52.82%. In the first half of the year, the company’s new energy vehicle business benefited from a year-on-year sales increase of 40%, achieving a revenue growth of 25.80%.

Additionally, the company’s SiC project has completed construction and entered the mass production ramp-up stage, with multiple models being targeted for production, which may accelerate volume in the second half of the year.

China Resources Microelectronics, Yangjie Technology:SiC Product Sales Growth

China Resources Microelectronics stated that during the reporting period, SiC and GaN power device sales revenue achieved rapid growth year-on-year.. In terms of business structure, the share of the general new energy field (automotive and new energy) has increased to 44%, becoming the largest application pillar, while consumer electronics account for 38%, and industrial and communication equipment each account for 9%. The company is seizing opportunities in automotive electrification and intelligence, photovoltaic energy storage, and the recovery of consumer electronics, achieving rapid growth in core customer orders.

Yangjie Technology also stated that during the reporting period, the company continuously increased the promotion of products such as MOSFET, IGBT, SiC in automotive electronics, artificial intelligence, industrial, and clean energy markets, resulting in a rapid increase in overall orders and shipments compared to the same period last year..

From the perspective of the global power semiconductor market, the recovery of international power semiconductor leaders seems to be relatively delayed.

Global power semiconductors,

Different Sensations

Once upon a time, Japanese manufacturers maintained strong competitiveness in the power semiconductor field. According to market research firm Omdia data, in 2021, among the top ten global power semiconductor market share rankings, Mitsubishi Electric, Fuji Electric, Toshiba, Renesas, and Rohm once occupied five seats..

Among them, Mitsubishi Electric ranked fourth, Fuji Electric followed closely in fifth, Toshiba ranked sixth, and Renesas and Rohm ranked ninth and tenth respectively, with these five companies holding over 20% of the market share.

However, in just three years, the advantage of these Japanese giants has significantly diminished. By 2024, only three Japanese manufacturers remain on the global power semiconductor market TOP10 list, and each has a global market share of less than 5%.

These chip giants have also undergone significant changes in their layout strategies, such as Rohm reducing SiC investments, slowing down some factories’ SiC mass production plans; Renesas has officially announced its withdrawal from the SiC market. Japan’s power leaders seem to have not kept up with this wave.

In today’s power semiconductor field, Infineon’s market position is considered a “benchmark”. Its power semiconductor shipments account for nearly 40% of the global market share, maintaining the top position for many years..

However, entering 2025, this German giant’s attitude reveals a clear conservatism. As early as the end of last year, Infineon’s CEO Jochen Hanebeck stated, “Except for artificial intelligence, our terminal markets currently have almost no growth momentum, and the cyclical recovery has been delayed. Therefore, we are prepared for a sluggish operating performance in 2025.”

From the performance data released by Infineon, this conservative expectation is also reflected.

In the second fiscal quarter of fiscal year 2025 (ending March 31, 2025), its revenue slightly decreased by 1% to 3.591 billion euros, although it met analyst expectations, but operating profit was 318 million euros, lower than 496 million euros in the same period of fiscal year 2024 (from January 1, 2024, to March 31, 2024).

In the third fiscal quarter (ending June 30, 2025), revenue was 3.704 billion euros, a year-on-year increase of 3%; profit was 668 million euros, a year-on-year increase of 11%; profit margin was 18.0%.. Additionally, Infineon expects revenue for this fiscal year to be around 14.6 billion euros, slightly lower than the previous year.

In summary, whether it is the rapid growth of domestic power semiconductor companies or the strategic adjustments and performance fluctuations of international giants, they reflect that the power semiconductor market is undergoing profound changes. Under the intertwining of demand recovery, technological iteration, and reshaping of competitive patterns, the development path of this market is gradually becoming clear, presenting the following five major trends.

Power semiconductors,

Five Major TrendsFirst, AI is driving the rapid development of power semiconductors. Data centers are a significant potential application area for power semiconductors. Within data centers, server rack power is rising above 100kW, driving the demand for power density to exceed 100W/cubic inch. The demand for high-power power supplies (PSU) ranging from 5.5kW to 12kW and battery backup units (BBU) is surging, creating an urgent need for wide bandgap semiconductor materials such as GaN and SiC.

Second,SiC applications are expanding beyond the automotive sector..

The explosion of the electric vehicle market has accelerated the application of SiC, but this is far from the end.

In the high-power track, as system power continues to increase, distribution voltage is also rising, and SiC is expected to bring more surprises.

For example, the rollout of DC fast charging networks, renewable energy generation and storage systems, and innovations in industrial power supplies have all become new focal points.

Third, GaN is poised for takeoff.

Entering 2025, GaN is showing greater commercial prospects.

Its current handling capacity, breakdown voltage, and on-resistance are comparable to those of SiC, while having lower capacitance. This significantly increases switching speed, leading to smaller power conversion systems. With lower process costs and smaller chip sizes, GaN’s costs are expected to be on par with silicon.

In addition to low-power AC-DC conversion applications, the industry is also expanding GaN’s power capabilities to 10-15 kilowatts. This presents opportunities for AI servers, telecommunications, satellite power supplies, and onboard chargers for electric vehicles. To further expand industrial applications and ultimately solve the inverter issues for electric vehicles, higher rated voltages such as 1200V or 1700V are needed.

There are many opportunities ahead for GaN.

Fourth, China continues to invest in power semiconductors.

China is continuously investing in power semiconductors, promoting the synchronized advancement of various links in the industry chain. Chip design companies are thus expanding their R&D teams, wafer manufacturing capacity is steadily increasing, and packaging and testing technologies are continuously optimized. With this industrial foundation, application fields are continuously expanding, and the demand for power semiconductors in scenarios such as new energy vehicle electronic control systems, photovoltaic inverters, and energy storage converters is growing year by year, thereby accelerating product iteration speed.

Industry insiders have indicated that in the localization process of power semiconductor devices, the localization of ordinary diodes and transistors has basically reached its end, and domestic companies have nearly completed their layout and implementation in this field..

In terms of powerMOS devices, the localization of mid-to-low-end application fields (i.e., scenarios with low performance requirements for MOS) has also been basically completed, and domestic manufacturers have entered a price competition stage. However, in high-end application fields such as servers and AI, domestic materials still cannot fully match foreign products in performance, which will become a key direction for localization advancement in the coming year or two.

IGBT and IGBT modules are in a different situation. The trend of localization for IGBT discrete devices is already very evident, and in applications where industrial requirements are not stringent, localization has basically been completed; however, for manufacturers with higher profit or performance considerations, the localization of discrete devices has not yet been realized. Meanwhile, the current localization rate of IGBT modules is still relatively low, thus, IGBT modules will become a key area for localization advancement in the next 3-5 years, representing a blue ocean.

Fifth, the upgrade of power semiconductor wafer sizes.

The power semiconductor industry is undergoing a significant transformation in wafer sizes to improve performance, cost, and scalability. Notably, most wafer foundries are developing advanced 12 inch wafers and have transitioned their mature BCD processes to 12 inch, thus avoiding upgrades on more expensive 8 inch wafers. Integrated device manufacturers (IDM) have also transitioned some of their silicon capacity, including BCD, HCMOS, IGBT, and MOSFET technologies to 12 inch wafers.

As applications such as electric vehicles and renewable energy systems require higher efficiency and power density, SiC technology is transitioning from 6 inch wafers to 8 inch wafers. This transition allows for more devices to be produced per wafer, thereby reducing costs and increasing production volume. It is expected that by 2025 , 8 inch SiC wafers will account for over 13% of production, and by 2030 will account for 59%.

With the continuous advancement of electrification and the increasing emphasis on sustainable development issues, the power semiconductor industry is facing tremendous opportunities.

Editor: Wang Peng