Click the blue text to follow us

On November 9, 2023, the ‘Light Storage End Information’ Industry Development Status and Prospect Analyst Forum was successfully held in Zhuhai, Guangdong, co-sponsored by the Zhuhai Municipal Government, the Guangdong Provincial Department of Industry and Information Technology, the China Electronics Technology Group Corporation, and the China Photovoltaic Industry Association.

Zhao Zhanxiang, Partner and Chief Technology Officer of Yunxiu Capital, was invited by the China Photovoltaic Industry Association to attend the forum and deliver a keynote speech titled ‘2023 Analysis of Power Semiconductors and Third-Generation Semiconductors in China’.

The following is a transcript of the report:Author | Zhao Zhanxiang, Sun Zhipeng Zhu YanfeiYunxiu Capital Semiconductor & New Materials Group

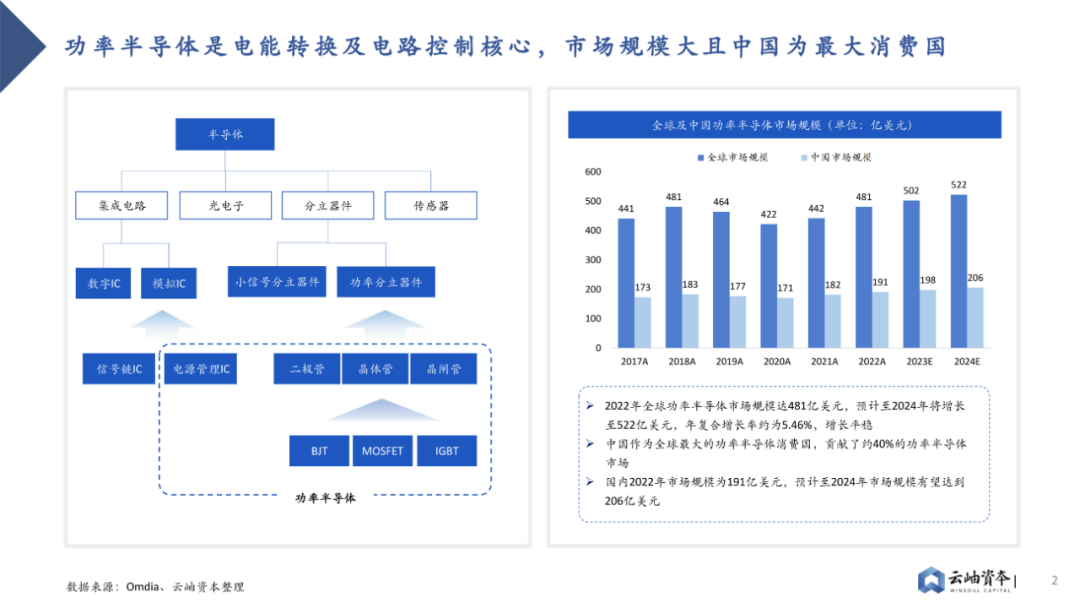

Power SemiconductorsPower semiconductors, also known as power electronic devices, are one of the core components in the electronics industry chain, capable of achieving power conversion and circuit control, primarily playing roles in power conversion, power amplification, power switching, line protection, reverse flow, and rectification within circuits. Power semiconductors include discrete power semiconductor devices and power ICs. According to Omdia statistics, the global power semiconductor market size reached $48.1 billion in 2022 and is expected to grow to $52.2 billion by 2024, with a compound annual growth rate (CAGR) of approximately 5.46%, showing steady growth. As the world’s largest consumer of power semiconductors, China contributes about 40% of the power semiconductor market.

Power SemiconductorsPower semiconductors, also known as power electronic devices, are one of the core components in the electronics industry chain, capable of achieving power conversion and circuit control, primarily playing roles in power conversion, power amplification, power switching, line protection, reverse flow, and rectification within circuits. Power semiconductors include discrete power semiconductor devices and power ICs. According to Omdia statistics, the global power semiconductor market size reached $48.1 billion in 2022 and is expected to grow to $52.2 billion by 2024, with a compound annual growth rate (CAGR) of approximately 5.46%, showing steady growth. As the world’s largest consumer of power semiconductors, China contributes about 40% of the power semiconductor market.

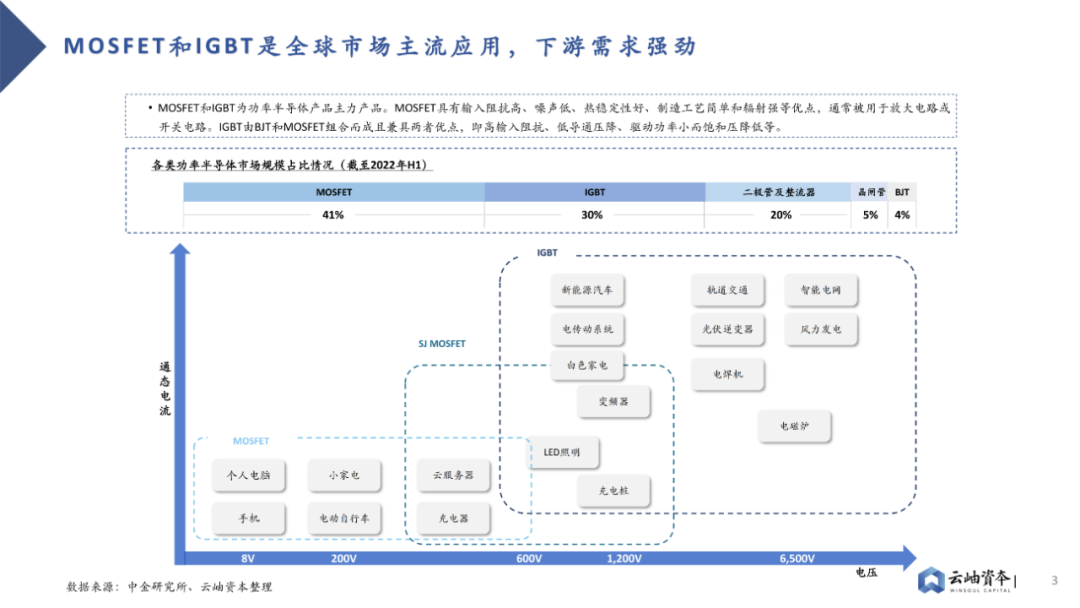

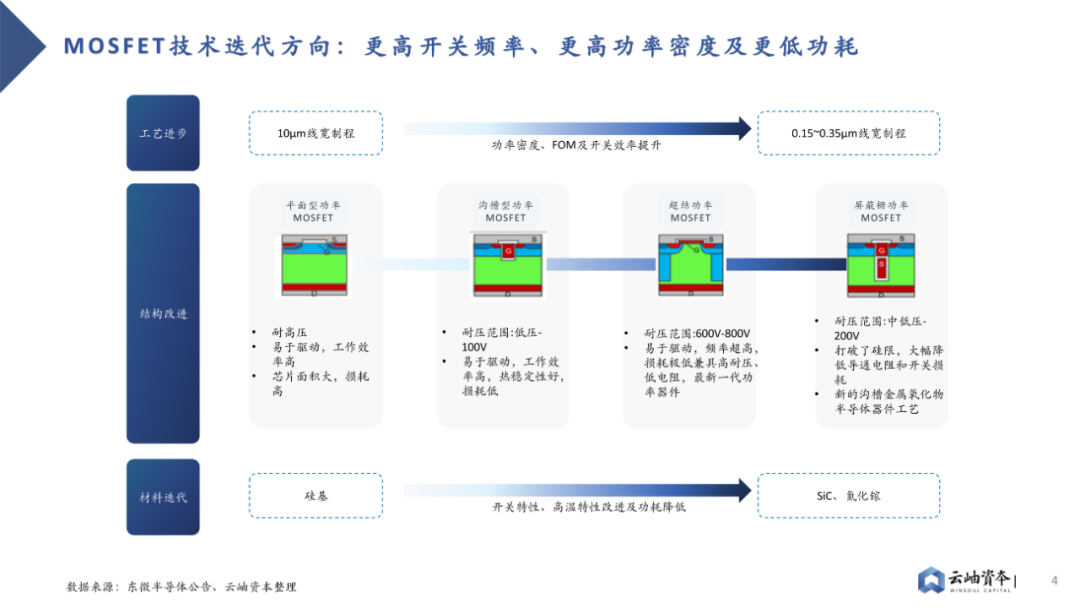

MOSFETs and IGBTs are the main products of power semiconductors, as of the first half of 2022, they accounted for 41% and 30% respectively. MOSFETs have advantages such as high input impedance, low noise, good thermal stability, simple manufacturing processes, and strong radiation resistance, and are typically used in amplification or switching circuits. IGBTs are composed of BJT and MOSFET, combining the advantages of both, such as high input impedance, low conduction voltage drop, low driving power, and reduced saturation voltage. Currently, MOSFETs and IGBTs are widely used in consumer electronics, new energy vehicles, and photovoltaics. MOSFETs can be classified into planar MOSFETs, trench MOSFETs, shielded gate SGT MOSFETs, and super junction SJ MOSFETs based on different processes. They can also be divided into N-channel and P-channel types, i.e., N-MOSFETs and P-MOSFETs. Since the advent of MOSFETs in the 1970s, products have continuously iterated, with iteration mainly focusing on process, design (structural changes), process optimization, and material changes to achieve high performance—high frequency, high power, and low loss.

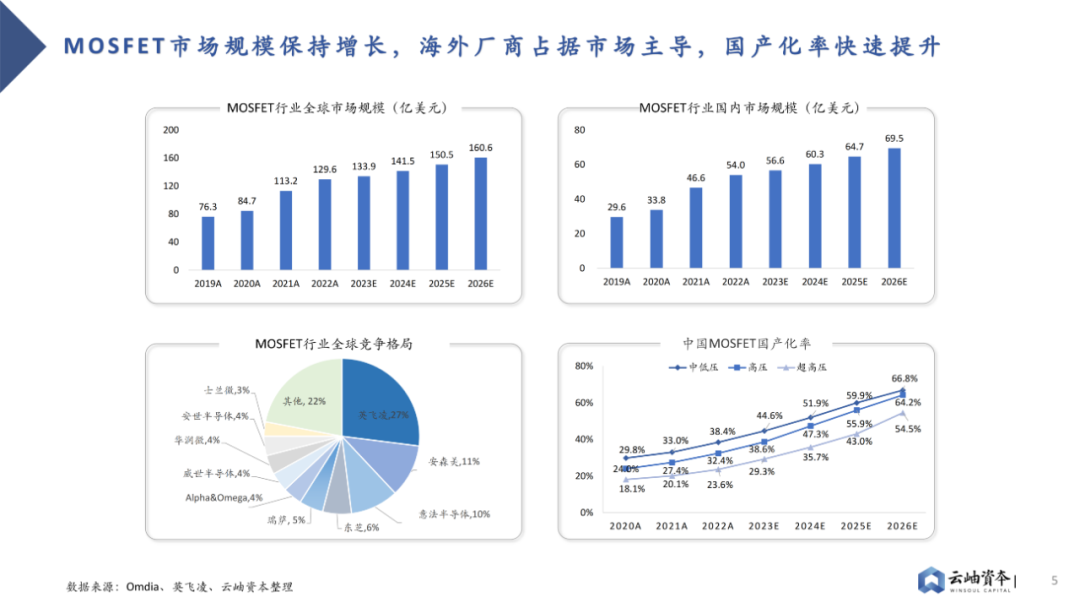

MOSFETs can be classified into planar MOSFETs, trench MOSFETs, shielded gate SGT MOSFETs, and super junction SJ MOSFETs based on different processes. They can also be divided into N-channel and P-channel types, i.e., N-MOSFETs and P-MOSFETs. Since the advent of MOSFETs in the 1970s, products have continuously iterated, with iteration mainly focusing on process, design (structural changes), process optimization, and material changes to achieve high performance—high frequency, high power, and low loss. MOSFETs have broad application prospects, and the market size is continuously growing. According to Yole’s forecast, by 2026, the global MOSFET (including discrete devices and modules) market size is expected to reach $16.06 billion, with a CAGR of 11.2% from 2019 to 2026. By 2026, the domestic MOSFET market size will reach $6.95 billion.The global MOSFET market is still dominated by overseas giants from Europe, the US, and Japan, with a stable competitive landscape among leading manufacturers, Infineon being the leading supplier of MOSFET devices globally. However, in recent years, the market share of overseas giants has shown a downward trend, with a significant trend towards localization. Domestically, Huazhu Micro, Silan Micro, New Clean Energy, Dongwei Semiconductor, and Yangjie Technology rank in the top five, but the leading effect is relatively weak. In the future, with the increase in downstream demand and industry attention, the speed of localization replacement is expected to accelerate further.

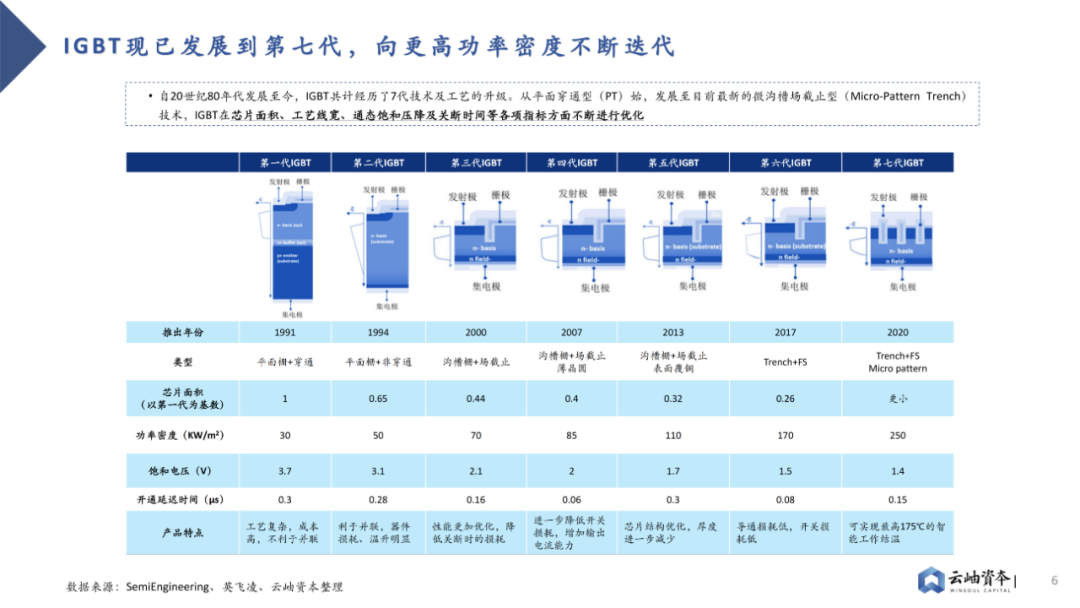

MOSFETs have broad application prospects, and the market size is continuously growing. According to Yole’s forecast, by 2026, the global MOSFET (including discrete devices and modules) market size is expected to reach $16.06 billion, with a CAGR of 11.2% from 2019 to 2026. By 2026, the domestic MOSFET market size will reach $6.95 billion.The global MOSFET market is still dominated by overseas giants from Europe, the US, and Japan, with a stable competitive landscape among leading manufacturers, Infineon being the leading supplier of MOSFET devices globally. However, in recent years, the market share of overseas giants has shown a downward trend, with a significant trend towards localization. Domestically, Huazhu Micro, Silan Micro, New Clean Energy, Dongwei Semiconductor, and Yangjie Technology rank in the top five, but the leading effect is relatively weak. In the future, with the increase in downstream demand and industry attention, the speed of localization replacement is expected to accelerate further. Since its inception, IGBTs have continuously undergone technological iterations, mainly focusing onreducing switching losses and creating thinner structures. Its vertical structure, gate structure, and silicon wafer processing technology have been continuously upgraded and improved, experiencing seven major technological evolutions, with various indicators continuously optimized during the evolution. Currently, IGBT chips have evolved to the seventh generation of fine trench gate field stop IGBTs, but considering costs, the most widely used are still fourth-generation IGBT products.

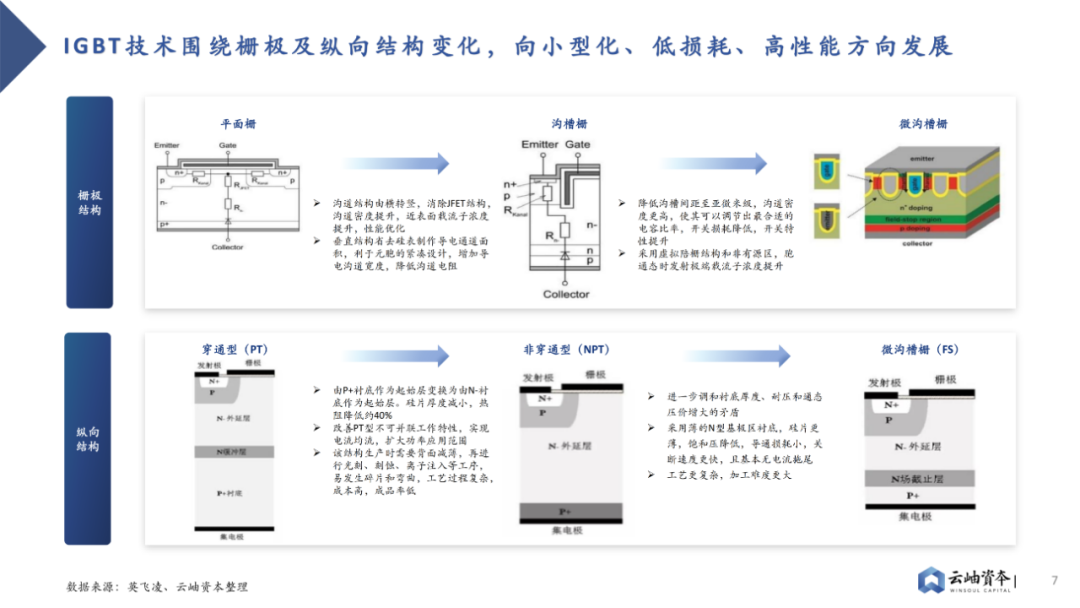

Since its inception, IGBTs have continuously undergone technological iterations, mainly focusing onreducing switching losses and creating thinner structures. Its vertical structure, gate structure, and silicon wafer processing technology have been continuously upgraded and improved, experiencing seven major technological evolutions, with various indicators continuously optimized during the evolution. Currently, IGBT chips have evolved to the seventh generation of fine trench gate field stop IGBTs, but considering costs, the most widely used are still fourth-generation IGBT products.

IGBT technological iterations mainly revolve around two levels. Firstly, regarding the front MOS structure,IGBT has undergone development from Planar (planar gate) to Trench (trench gate) to Micro Trench (micro trench gate), with switching losses continuously decreasing. At the same time,regarding the body structure, IGBT has experienced development from PT (punch-through) to NPT (non-punch-through) to FS/SPT/LPT (soft punch-through), with gradually increasing voltage resistance, decreasing saturation voltage drop, decreasing static and dynamic losses, and continuously shrinking chip size.

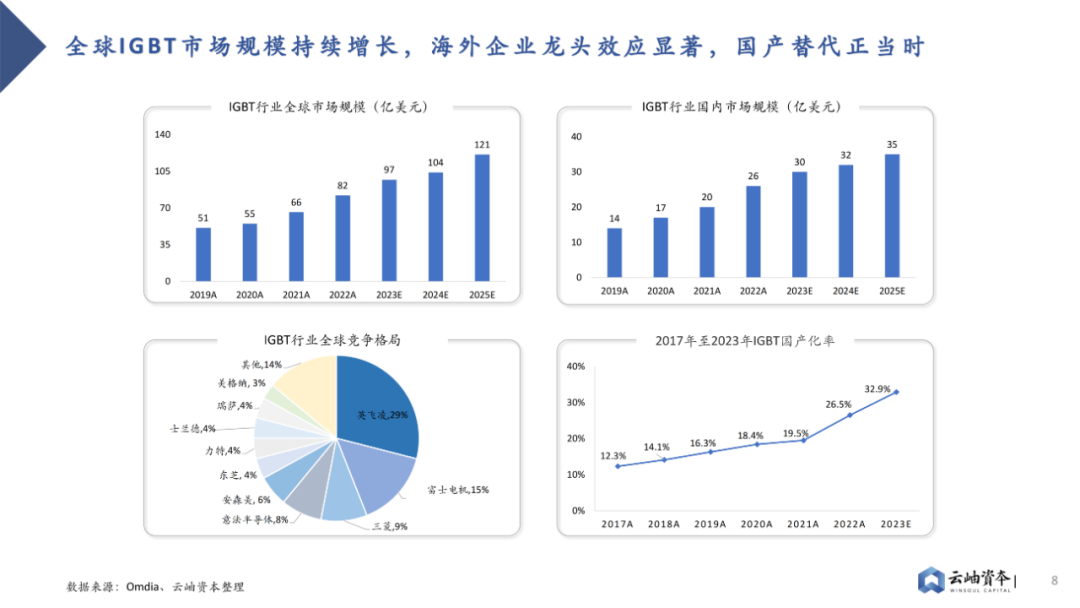

The global IGBT market size continues to grow. According to Yole’s forecast, by 2026, the global IGBT market size will reach $12.1 billion, with a CAGR of 13.1% from 2019 to 2026. China is the largest consumer market for IGBTs globally, and it is predicted that by 2026, the domestic IGBT market size will reach $3.5 billion.

The global IGBT market is mainly occupied by European and Japanese manufacturers, and there is still significant space for localization. According to Omdia data, in the field of discrete device IGBTs in 2021, the global leader Infineon held nearly 30% market share, with Infineon, Fuji Electric, and Mitsubishi Electric collectively accounting for over 50% of the market. Among domestic manufacturers, Silan Micro, Star Semiconductor, and Times Electric are developing rapidly.Currently, the localization rate of IGBTs is low, but with the development of downstream industries such as new energy and photovoltaics and the requirements for self-controllable domestic industrial chains, the localization rate will further increase.

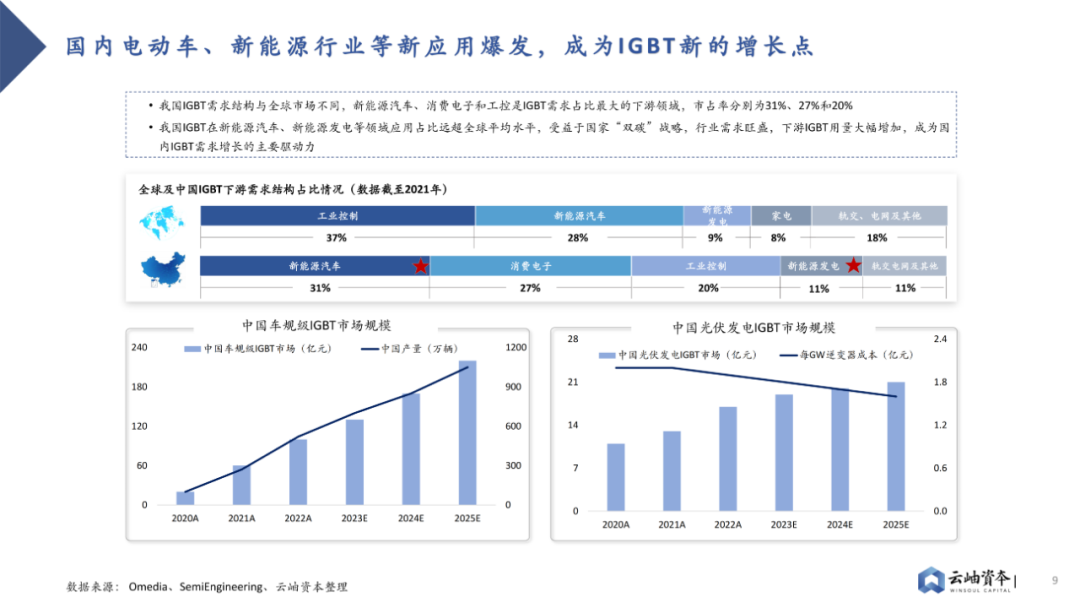

From the perspective of downstream IGBT demand structure, China’s IGBT demand structure differs from the global market, with new energy vehicles, consumer electronics (including home appliances), and industrial control being the three largest downstream fields, accounting for 31%, 27%, and 20%, respectively.China’s application of IGBTs in the new energy field far exceeds the global average, mainly benefiting from the national ‘dual carbon’ strategy, with strong demand in the new energy sector, leading to a significant increase in the use of IGBTs, which is the main driving force behind the growth of IGBT demand in China.

From the perspective of downstream IGBT demand structure, China’s IGBT demand structure differs from the global market, with new energy vehicles, consumer electronics (including home appliances), and industrial control being the three largest downstream fields, accounting for 31%, 27%, and 20%, respectively.China’s application of IGBTs in the new energy field far exceeds the global average, mainly benefiting from the national ‘dual carbon’ strategy, with strong demand in the new energy sector, leading to a significant increase in the use of IGBTs, which is the main driving force behind the growth of IGBT demand in China. Automotive-grade IGBT modules are core components of electric vehicle motor controllers, high-voltage chargers, air conditioning systems, and other electrical components, directly controlling the conversion of direct and alternating current in drive systems while also responsible for motor frequency control. Therefore, the technical level of automotive-grade IGBTs affects the torque, maximum output power, and power release speed of electric vehicle drive systems. Additionally, IGBTs are used as switching elements in smart charging piles. IGBT modules account for about 10% of the cost of electric vehicles and about 20% of the cost of charging piles.Automotive-grade IGBT products have extremely high reliability requirements, mainly reflected in the dimensions of product technology and packaging technology. Currently, automotive-grade IGBT products must meet new automotive standards LV324/AQG324, standards from the China IGBT Alliance and the Zhongguancun Wide Bandgap Alliance, as well as customer certification standards.Generally, the certification cycle lasts 3-5 years.

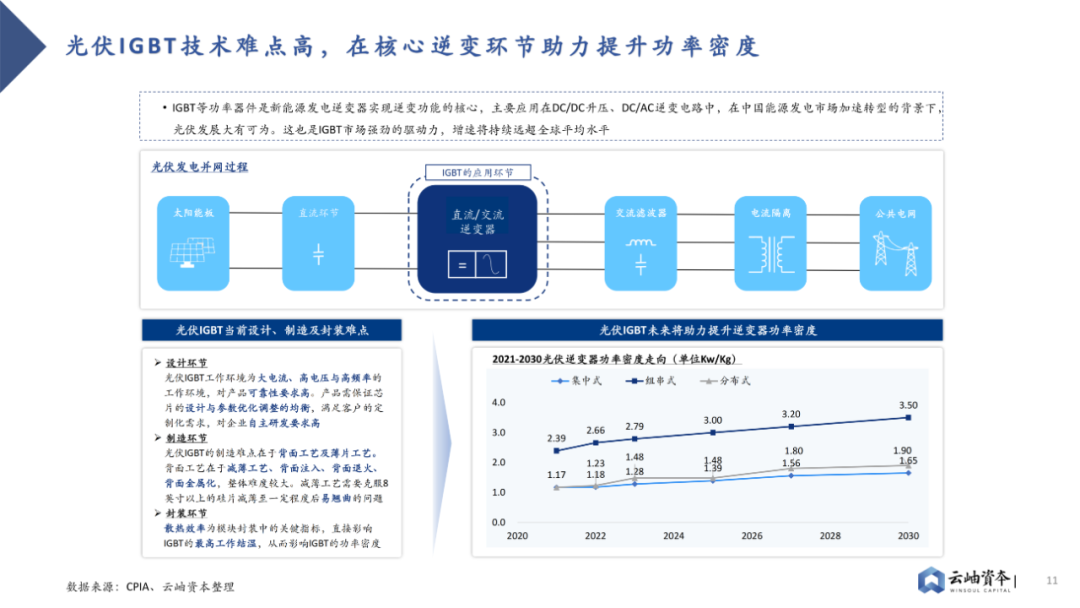

Automotive-grade IGBT modules are core components of electric vehicle motor controllers, high-voltage chargers, air conditioning systems, and other electrical components, directly controlling the conversion of direct and alternating current in drive systems while also responsible for motor frequency control. Therefore, the technical level of automotive-grade IGBTs affects the torque, maximum output power, and power release speed of electric vehicle drive systems. Additionally, IGBTs are used as switching elements in smart charging piles. IGBT modules account for about 10% of the cost of electric vehicles and about 20% of the cost of charging piles.Automotive-grade IGBT products have extremely high reliability requirements, mainly reflected in the dimensions of product technology and packaging technology. Currently, automotive-grade IGBT products must meet new automotive standards LV324/AQG324, standards from the China IGBT Alliance and the Zhongguancun Wide Bandgap Alliance, as well as customer certification standards.Generally, the certification cycle lasts 3-5 years. IGBT is the ‘heart’ of photovoltaic inverters, with rapidly increasing market demand in the photovoltaic field. IGBT power devices, as core semiconductor components of photovoltaic inverters, wind power converters, and energy storage converters, play roles in rectification and inversion of electric energy to achieve functions such as AC grid connection for new energy generation and charge and discharge of energy storage batteries.Photovoltaic IGBTs require high reliability and stability, and high-performance IGBTs can help improve the power density of photovoltaics.

IGBT is the ‘heart’ of photovoltaic inverters, with rapidly increasing market demand in the photovoltaic field. IGBT power devices, as core semiconductor components of photovoltaic inverters, wind power converters, and energy storage converters, play roles in rectification and inversion of electric energy to achieve functions such as AC grid connection for new energy generation and charge and discharge of energy storage batteries.Photovoltaic IGBTs require high reliability and stability, and high-performance IGBTs can help improve the power density of photovoltaics.

Third-Generation Semiconductors

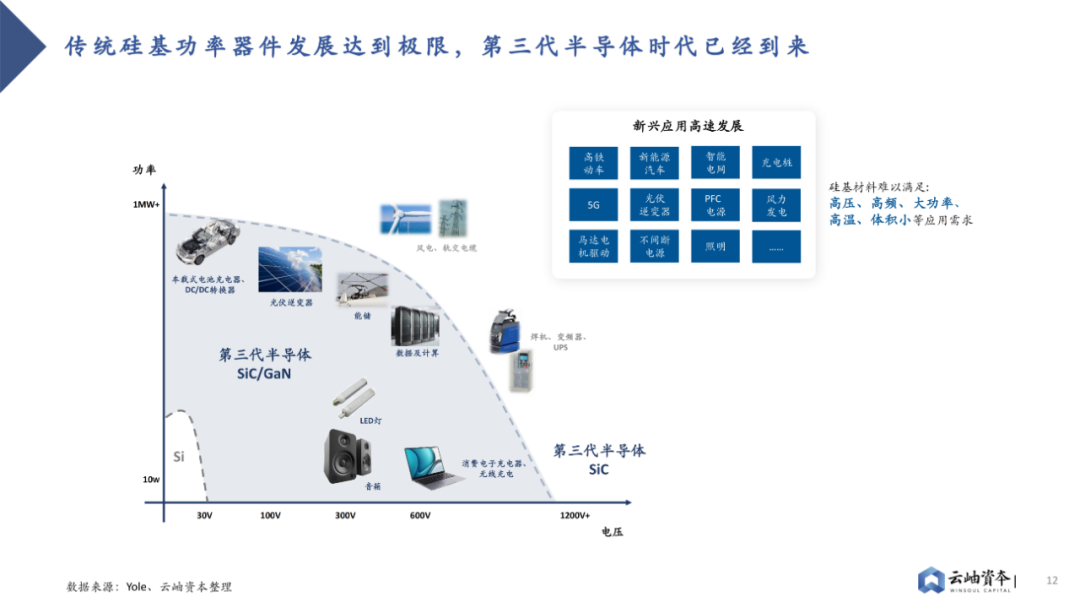

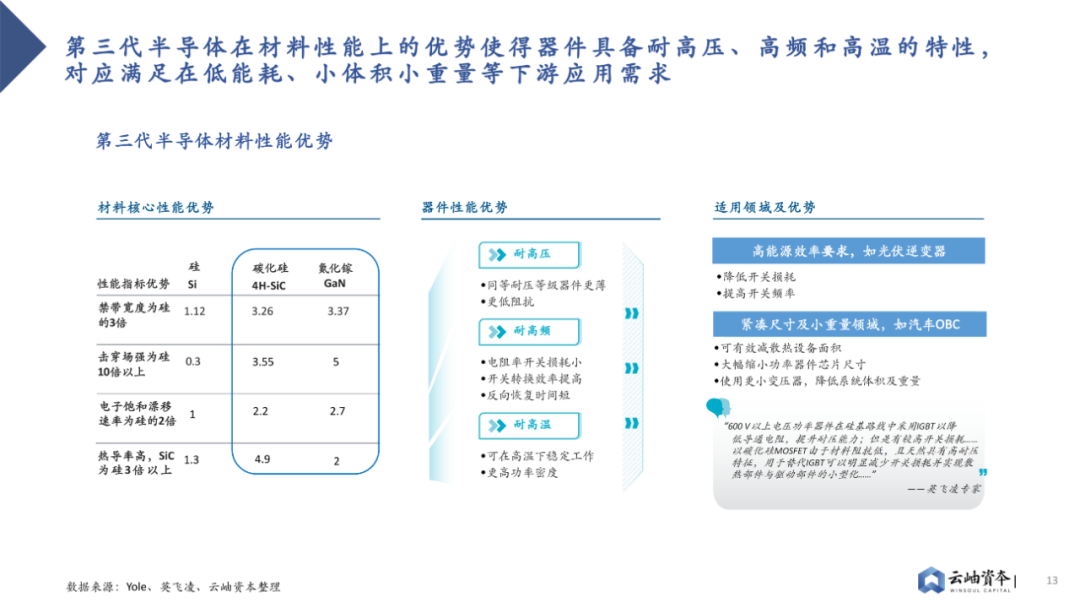

The development of traditional silicon-based power devices has reached its limits, and the era of third-generation semiconductors has arrived.Third-generation semiconductors are represented by wide bandgap semiconductor materials such as silicon carbide (SiC) and gallium nitride (GaN), characterized by superior performance including high frequency, high efficiency, high power, high voltage resistance, high temperature resistance, and strong radiation resistance, which are key core materials supporting the continuous development of industries such as new energy vehicles, photovoltaic energy storage, high-speed rail transit, smart grids, and the new generation of mobile communications. Compared to first and second-generation semiconductor materials, third-generation semiconductor materials have a wider bandgap, higher breakdown electric field, higher thermal conductivity, higher electron saturation velocity, and higher radiation resistance, making them more suitable for the production of high-temperature, high-frequency, radiation-resistant, and high-power devices. Currently, the most mature applications of third-generation semiconductor materials and devices are SiC and GaN semiconductor materials, while research on materials such as zinc oxide, diamond, and aluminum nitride is still in its infancy.

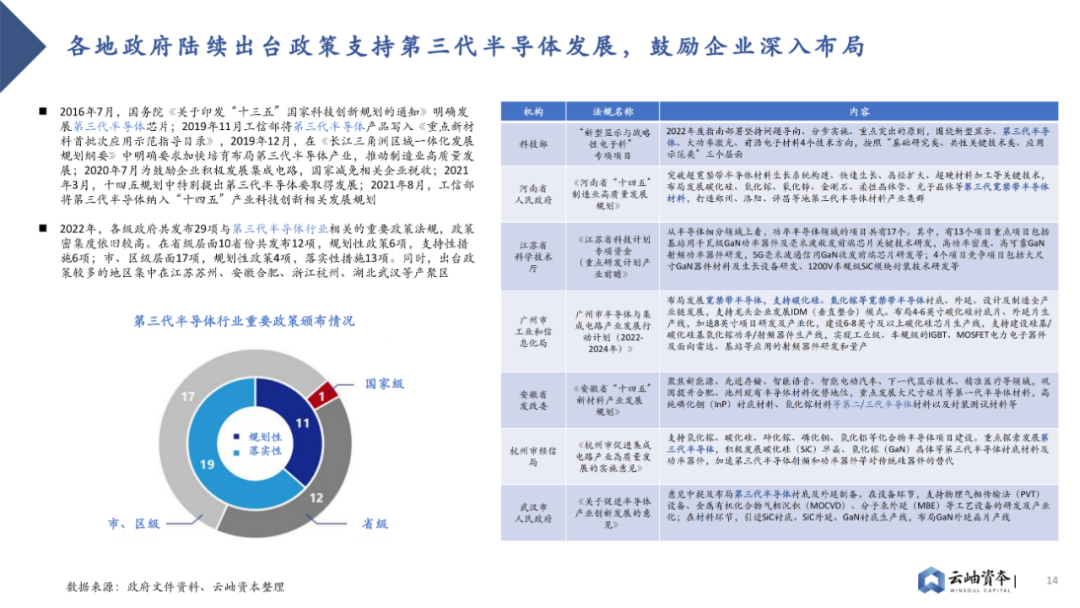

Compared to first and second-generation semiconductor materials, third-generation semiconductor materials have a wider bandgap, higher breakdown electric field, higher thermal conductivity, higher electron saturation velocity, and higher radiation resistance, making them more suitable for the production of high-temperature, high-frequency, radiation-resistant, and high-power devices. Currently, the most mature applications of third-generation semiconductor materials and devices are SiC and GaN semiconductor materials, while research on materials such as zinc oxide, diamond, and aluminum nitride is still in its infancy. The government continues to issue relevant policies to support the development of third-generation semiconductors, In July 2016, the State Council issued the ‘Notice on Printing and Distributing the National Science and Technology Innovation Plan for the 13th Five-Year Plan’, clearly stating the development of third-generation semiconductor chips; in November 2019, the Ministry of Industry and Information Technology included third-generation semiconductor products in the ‘Guidelines for the Demonstration of First Batch Applications of Key New Materials’; in December 2019, the ‘Yangtze River Delta Regional Integration Development Plan Outline’ explicitly requested to accelerate the cultivation and layout of the third-generation semiconductor industry to promote high-quality development of the manufacturing industry; in July 2020, to encourage enterprises to actively develop integrated circuits, the government exempted relevant enterprise taxes; in March 2021, the 14th Five-Year Plan specifically mentioned the development of third-generation semiconductors; in August 2021, the Ministry of Industry and Information Technology included third-generation semiconductors in the relevant development of ’14th Five-Year’ industrial technological innovation.

The government continues to issue relevant policies to support the development of third-generation semiconductors, In July 2016, the State Council issued the ‘Notice on Printing and Distributing the National Science and Technology Innovation Plan for the 13th Five-Year Plan’, clearly stating the development of third-generation semiconductor chips; in November 2019, the Ministry of Industry and Information Technology included third-generation semiconductor products in the ‘Guidelines for the Demonstration of First Batch Applications of Key New Materials’; in December 2019, the ‘Yangtze River Delta Regional Integration Development Plan Outline’ explicitly requested to accelerate the cultivation and layout of the third-generation semiconductor industry to promote high-quality development of the manufacturing industry; in July 2020, to encourage enterprises to actively develop integrated circuits, the government exempted relevant enterprise taxes; in March 2021, the 14th Five-Year Plan specifically mentioned the development of third-generation semiconductors; in August 2021, the Ministry of Industry and Information Technology included third-generation semiconductors in the relevant development of ’14th Five-Year’ industrial technological innovation. Domestic and foreign manufacturers are actively laying out silicon carbide, and the industry chain is becoming increasingly complete. The SiC substrate market is highly concentrated, with Shandong Tianyue holding a 30% market share in the semi-insulating market in 2020. Super Chip Star is one of the few domestic companies mastering both PVT and HTCVD crystal growth technologies. Domestic silicon carbide epitaxy manufacturers represented by Dongguan Tianyu and Hantian Tian have successfully developed 6-inch silicon carbide epitaxial wafers, gradually achieving commercialization. Domestic manufacturers entered the SiC power device field relatively late, and currently have a small market share, but since the industry is in its early stages, the landscape is not yet defined. Changfei Advanced Semiconductor adopts the IDM model, covering the entire industry chain from epitaxy, design, wafer manufacturing to module production. Currently, its SiC MOSFET production capacity and planned capacity are both ranked first in the country, and its products have passed certification from leading automotive manufacturers and Tier 1 customers, making it one of the first domestic companies to supply main inverters for new energy vehicles.

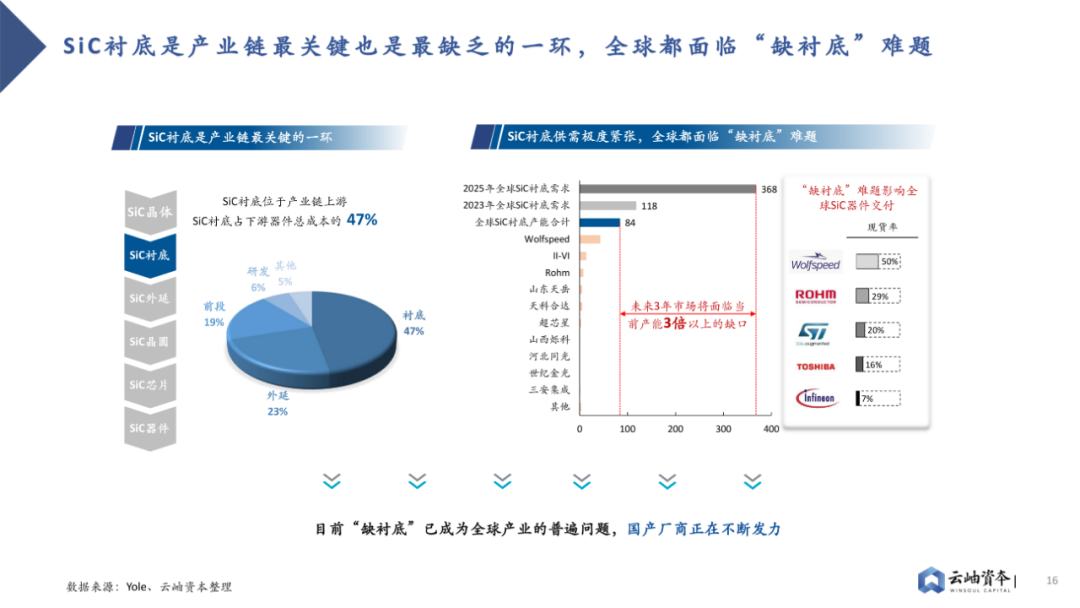

Domestic and foreign manufacturers are actively laying out silicon carbide, and the industry chain is becoming increasingly complete. The SiC substrate market is highly concentrated, with Shandong Tianyue holding a 30% market share in the semi-insulating market in 2020. Super Chip Star is one of the few domestic companies mastering both PVT and HTCVD crystal growth technologies. Domestic silicon carbide epitaxy manufacturers represented by Dongguan Tianyu and Hantian Tian have successfully developed 6-inch silicon carbide epitaxial wafers, gradually achieving commercialization. Domestic manufacturers entered the SiC power device field relatively late, and currently have a small market share, but since the industry is in its early stages, the landscape is not yet defined. Changfei Advanced Semiconductor adopts the IDM model, covering the entire industry chain from epitaxy, design, wafer manufacturing to module production. Currently, its SiC MOSFET production capacity and planned capacity are both ranked first in the country, and its products have passed certification from leading automotive manufacturers and Tier 1 customers, making it one of the first domestic companies to supply main inverters for new energy vehicles. Silicon carbide substrate materials are the most valuable part of the silicon carbide industry chain. The process of making silicon carbide devices can be divided into substrate processing, epitaxial growth, device design, manufacturing, and packaging. There is a significant value inversion phenomenon in the industry chain, where substrate manufacturing has the highest technical barriers and value. In the silicon carbide industry chain, silicon carbide substrates account for about 47% of the cost of silicon carbide devices. In contrast, for silicon-based devices, wafer manufacturing accounts for 50% of the cost, while silicon wafer substrates only account for 7% of the cost.

Silicon carbide substrate materials are the most valuable part of the silicon carbide industry chain. The process of making silicon carbide devices can be divided into substrate processing, epitaxial growth, device design, manufacturing, and packaging. There is a significant value inversion phenomenon in the industry chain, where substrate manufacturing has the highest technical barriers and value. In the silicon carbide industry chain, silicon carbide substrates account for about 47% of the cost of silicon carbide devices. In contrast, for silicon-based devices, wafer manufacturing accounts for 50% of the cost, while silicon wafer substrates only account for 7% of the cost. Thanks to the explosion of the new energy vehicle market, the silicon carbide market will maintain rapid growth from 2022 to 2027; after 2027, overall market growth will maintain an average annual growth rate of 47%, and the proportion of new energy vehicles and photovoltaics in the overall silicon carbide market will remain around 50%.

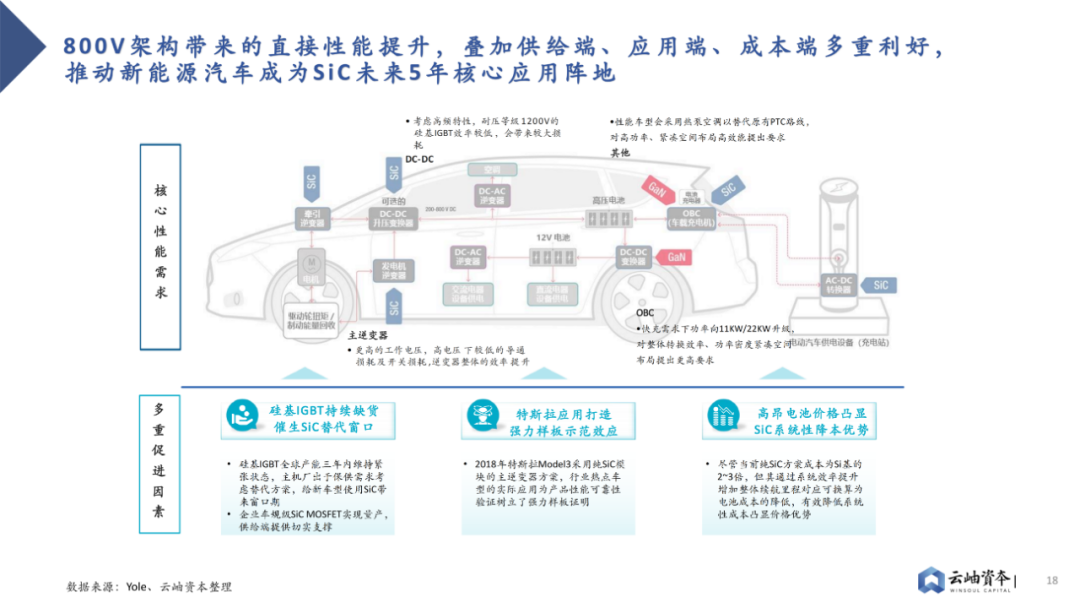

Thanks to the explosion of the new energy vehicle market, the silicon carbide market will maintain rapid growth from 2022 to 2027; after 2027, overall market growth will maintain an average annual growth rate of 47%, and the proportion of new energy vehicles and photovoltaics in the overall silicon carbide market will remain around 50%. From the perspective of penetration rates across different industries, the 800V platform and silicon carbide are driving new energy vehicles to become the largest explosion market in 2023. In segmented applications, the main inverter, as the most core and valuable field, has adopted pure SiC MOSFET replacement solutions, while OBC and DC-DC currently still use SiC SBD as a recent transition.

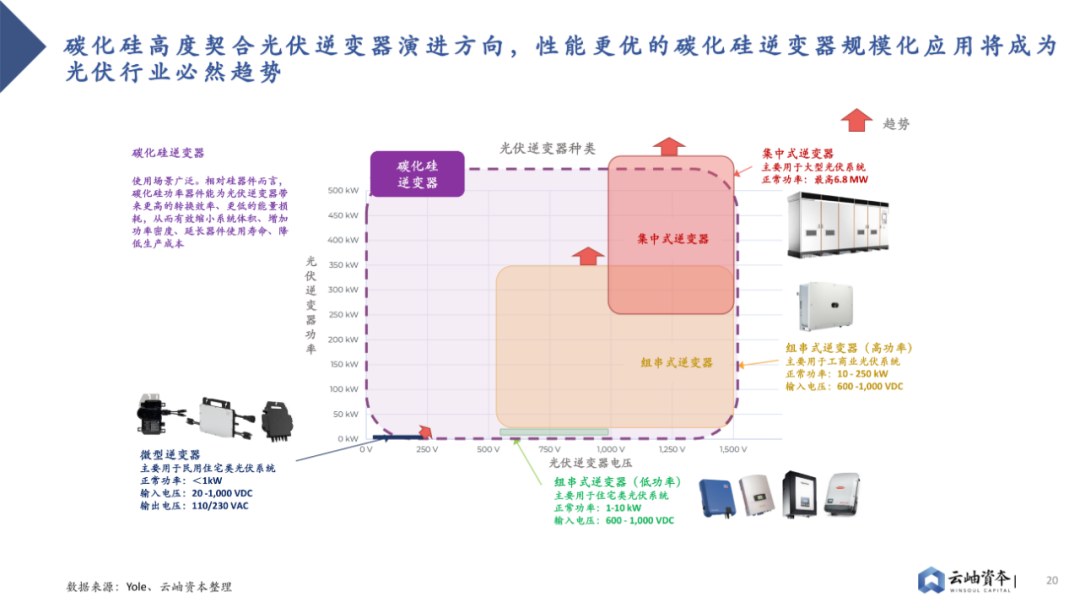

From the perspective of penetration rates across different industries, the 800V platform and silicon carbide are driving new energy vehicles to become the largest explosion market in 2023. In segmented applications, the main inverter, as the most core and valuable field, has adopted pure SiC MOSFET replacement solutions, while OBC and DC-DC currently still use SiC SBD as a recent transition. Compared to silicon devices, silicon carbide power devices can provide photovoltaic inverters with higher conversion efficiency and lower energy loss, effectively reducing system size, increasing power density, extending device lifespan, and lowering production costs. As the size and power density of solar panels gradually increase, traditional silicon-based devices can no longer meet the efficiency and thermal requirements of photovoltaic inverter MPPT (maximum power point tracking) circuits, making the application of silicon carbide power devices with superior performance in all aspects an inevitable trend.

Compared to silicon devices, silicon carbide power devices can provide photovoltaic inverters with higher conversion efficiency and lower energy loss, effectively reducing system size, increasing power density, extending device lifespan, and lowering production costs. As the size and power density of solar panels gradually increase, traditional silicon-based devices can no longer meet the efficiency and thermal requirements of photovoltaic inverter MPPT (maximum power point tracking) circuits, making the application of silicon carbide power devices with superior performance in all aspects an inevitable trend. In photovoltaic power generation applications, although traditional inverters based on silicon devices account for about 10% of system costs, they are one of the main sources of energy loss in the system. Compared to silicon-based IGBTs, SiC MOSFETs have lower conduction losses, lower switching losses, no current tailing phenomenon, and high switching speeds, and can operate in harsh environments such as high temperatures, which helps improve the lifespan of photovoltaic inverters.

In photovoltaic power generation applications, although traditional inverters based on silicon devices account for about 10% of system costs, they are one of the main sources of energy loss in the system. Compared to silicon-based IGBTs, SiC MOSFETs have lower conduction losses, lower switching losses, no current tailing phenomenon, and high switching speeds, and can operate in harsh environments such as high temperatures, which helps improve the lifespan of photovoltaic inverters. As the application fields of gallium nitride continue to expand, the market scale of China’s gallium nitride industry continues to grow. The current application fields are mainly concentrated in consumer electronics, new energy vehicles, photovoltaics and energy storage, data computing centers, etc. The domestic gallium nitride industry is continuing to grow rapidly, with gallium nitride penetration rates expected to reach 40% by 2026.

As the application fields of gallium nitride continue to expand, the market scale of China’s gallium nitride industry continues to grow. The current application fields are mainly concentrated in consumer electronics, new energy vehicles, photovoltaics and energy storage, data computing centers, etc. The domestic gallium nitride industry is continuing to grow rapidly, with gallium nitride penetration rates expected to reach 40% by 2026. Currently, there are many domestic gallium nitride startups, and the industry concentration is relatively dispersed, but companies like Innoscience are clearly advantageous, covering various downstream application scenarios and mastering processes and capacity guarantees independently, and will continue to increase market share in the future.

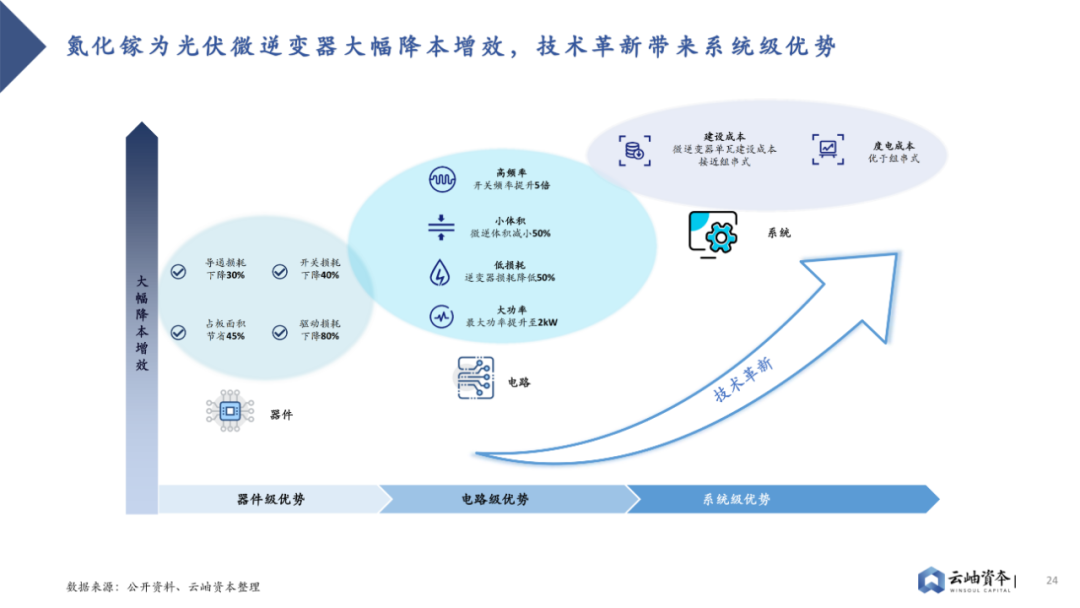

Currently, there are many domestic gallium nitride startups, and the industry concentration is relatively dispersed, but companies like Innoscience are clearly advantageous, covering various downstream application scenarios and mastering processes and capacity guarantees independently, and will continue to increase market share in the future. GaN has solved the bottleneck of silicon-based designs, achieving smaller, lighter, and more cost-effective photovoltaic power generation systems, simplifying installation processes in large-scale deployments and bringing significant cost savings. Through excellent material toughness and reliability, inverters designed based on GaN can reduce overall system maintenance costs, shorten system downtime, while maintaining optimal performance, leading to systemic innovation.

GaN has solved the bottleneck of silicon-based designs, achieving smaller, lighter, and more cost-effective photovoltaic power generation systems, simplifying installation processes in large-scale deployments and bringing significant cost savings. Through excellent material toughness and reliability, inverters designed based on GaN can reduce overall system maintenance costs, shorten system downtime, while maintaining optimal performance, leading to systemic innovation.

Gallium nitride materials have advantages such as high switching frequency, low conduction resistance, and small size, which can achieve higher system efficiency, less power loss, and smaller module size, showing significant advantages over silicon materials in the power device field. Initially, gallium nitride materials were widely used in fast charging for consumer electronics, and are now penetrating into automotive, data center, photovoltaic storage, and other fields, with the market expected to continue stable growth in the future.

Industry Trends and Outlook

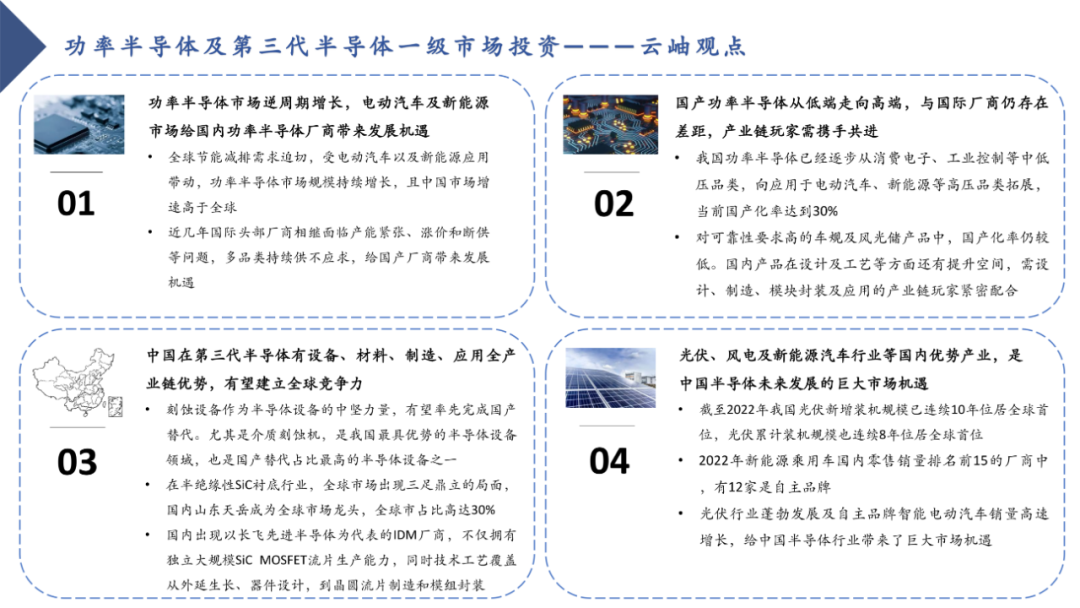

Yunxiu Capital has the following views on the investment in power semiconductors and third-generation semiconductors in 2023: Firstly, the power semiconductor market is growing counter-cyclically, and the electric vehicle and new energy markets are providing development opportunities for domestic power semiconductor manufacturers. Secondly, domestic power semiconductors are moving from low-end to high-end, but there is still a gap compared to international manufacturers, and industry chain players need to work together. Thirdly, China has advantages across the entire industry chain in third-generation semiconductors, including equipment, materials, manufacturing, and applications, and is expected to establish global competitiveness. Finally, industries such as photovoltaics, wind power, and new energy vehicles are huge market opportunities for the future development of China’s semiconductor industry. In recent years, a number of excellent and professional semiconductor teams and startups have emerged in China. With the support of policies and capital, they have quickly gained the strength to compete with foreign manufacturers in certain niche areas within just a few years. In the future, along with China’s development in industries such as photovoltaics and new energy vehicles, supply chain opportunities will continue to drive the rapid growth and technological breakthroughs in the power semiconductor and third-generation semiconductor industries, and the competitive landscape will gradually change. Let us wait and see.

In recent years, a number of excellent and professional semiconductor teams and startups have emerged in China. With the support of policies and capital, they have quickly gained the strength to compete with foreign manufacturers in certain niche areas within just a few years. In the future, along with China’s development in industries such as photovoltaics and new energy vehicles, supply chain opportunities will continue to drive the rapid growth and technological breakthroughs in the power semiconductor and third-generation semiconductor industries, and the competitive landscape will gradually change. Let us wait and see.