On September 8, the A-shares experienced overall fluctuations throughout the day, with the three major indices strengthening in the afternoon. The ChiNext index narrowed its decline, while the Shanghai Composite and Shenzhen Component indices surged at one point. By the close, the Shanghai Composite index rose by 0.38%, the Shenzhen Component index increased by 0.61%, and the ChiNext index fell by 0.84%. The total transaction volume in the Shanghai and Shenzhen markets exceeded 2.4 trillion, with over 3800 stocks in the two markets showing gains.

On the market, the sectors of PEEK materials, pork, chemicals, and robotics led the gains, while tourism and hotels, securities, CPO, and retail sectors lagged behind. The satellite internet sector surged in the afternoon, with China Unicom rising sharply by 4.82%, and China Satellite hitting the daily limit.

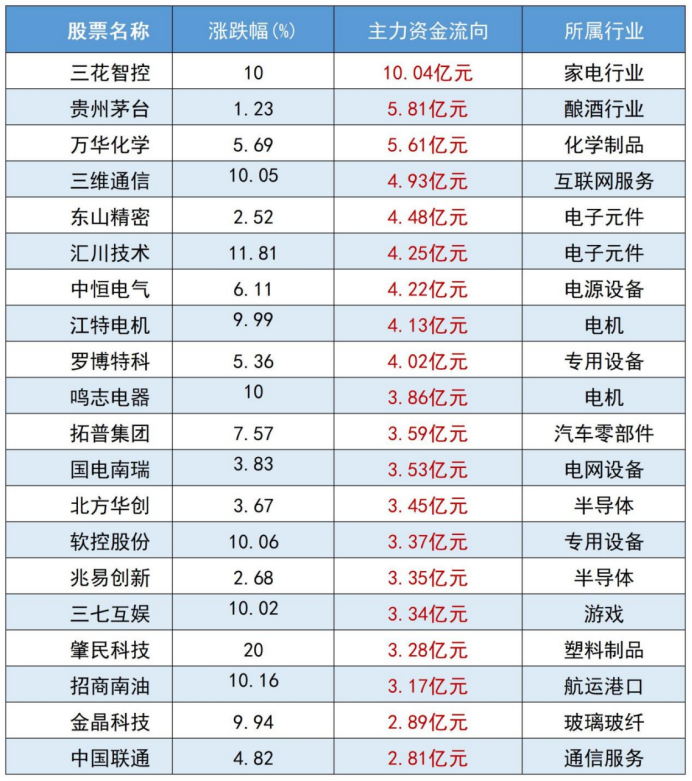

The top 20 stocks with major capital inflows are as follows:

In-depth analysis of the reasons for the rise of PEEK materials and the chemical sector

The recent rise of PEEK materials and the chemical sector is mainly driven by the following factors:

Reasons for the rise of PEEK materials

Explosive demand in high-end applications

As the “crown jewel of high-end engineering plastics“, PEEK materials are experiencing rapid growth in demand in fields such as aerospace, medical devices, and semiconductor equipment. The accelerated advancement of the domestic large aircraft C929 and the speeding up of the localization process of semiconductor equipment have driven the price of PEEK materials to increase by 35% compared to the beginning of the year (data as of 2025-08-11).

Catalysis of the humanoid robot industry

The production target of 1 million units by Tesla in 2026 has driven the demand for lightweight materials, with PEEK being an ideal choice for key components such as joints and structural parts due to its excellent performance (load capacity >400MPa, friction coefficient 0.05-0.1) (data as of 2025-05-18).

Acceleration of domestic substitution

There is a severe global shortage of PEEK production capacity (total capacity of 14,000 tons), while domestic companies such as Yanzhi Co. have achieved breakthroughs in the kiloton level, gradually breaking the monopoly of international giants like Victrex and Evonik (data as of 2025-08-26).

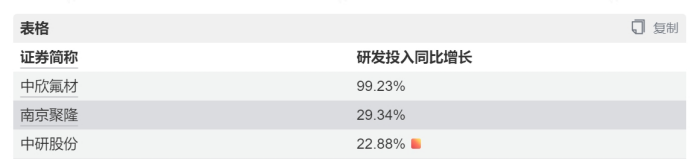

Significant increase in R&D investment

Some PEEK concept stocks have significantly increased their R&D investment in the first half of 2025 compared to the previous year:

Factors contributing to the overall strength of the chemical sector

Effectiveness of anti-involution policies

In the first half of 2025, the gross profit margin of basic chemicals was 16.8% (year-on-year +0.5pct), and the net profit margin was 6.0% (year-on-year +1.6pct), ending a continuous decline for five years. The ratio of construction projects to fixed assets has dropped to 24% (27% in 2015), with a significant contraction on the supply side (data as of 2025-09-04).

Differentiation in sub-sector prosperity

The fertilizer and agricultural chemicals sub-sectors have performed outstandingly in the past month

Continuous capital accumulation

The chemical ETF (159870) saw a net subscription of over 500 million units on September 4, 2025, indicating increased market confidence in the chemical sector (data as of 2025-09-04).

Exit of overseas production capacity

Based on 2022, the production of chemical products in Europe has declined by 15-20%, while China has grown by over 30% during the same period, creating export opportunities due to the restructuring of the global supply chain (data as of 2025-09-04).

Source: Wind

Disclaimer

The above content is for your reference and learning only. All content does not constitute advice for the purchase, sale, or holding of any financial products and should not be used as the basis for any investment decisions. You bear the investment risks and losses. Investment involves risks; please proceed with caution.