Introduction to AI Chips

AI Chips: Also known as artificial intelligence chips, AI accelerators, or compute cards, these modules are specifically designed to handle a large number of computational tasks in AI applications.

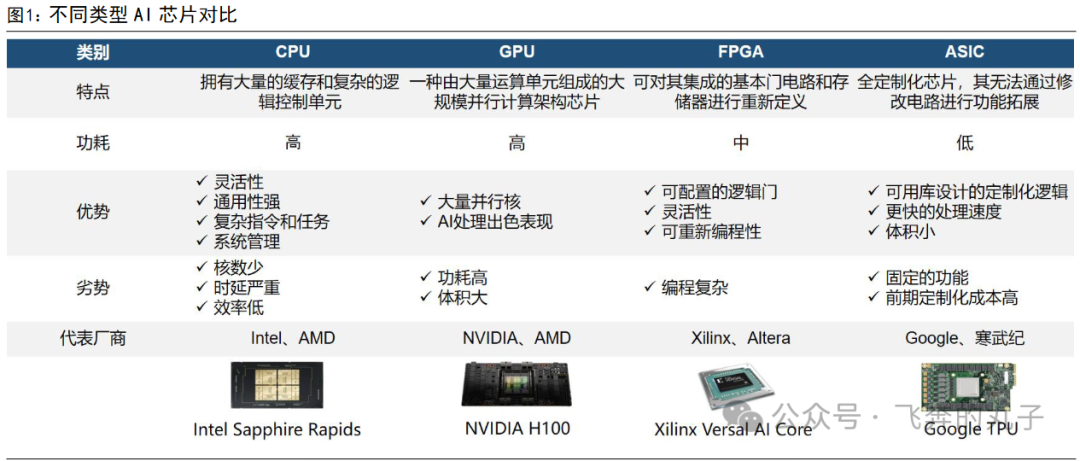

Classification of AI Chips: Based on design requirements, AI chips are mainly divided into Central Processing Units (CPUs), Graphics Processing Units (GPUs), Field-Programmable Gate Arrays (FPGAs), and Application-Specific Integrated Circuits (ASICs). Compared to other AI chips, ASICs are characterized by high performance, small size, and low power consumption.

CPU -> GPU -> ASIC, with ASIC becoming an important branch of AI chips.

1) CPU Stage: At this stage, there were no breakthrough AI algorithms, and the available data was limited, so traditional CPUs could meet the computational requirements;

2) GPU Stage: In 2006, NVIDIA released the CUDA architecture, which first enabled programmability in GPUs, leading to their large-scale application in the AI field;

3) ASIC Stage: In 2016, Google released the TPU chip (ASIC type), which overcame the high cost and power consumption issues of GPUs, leading to the gradual application of ASIC chips in the AI field, making them an important branch of AI chips.

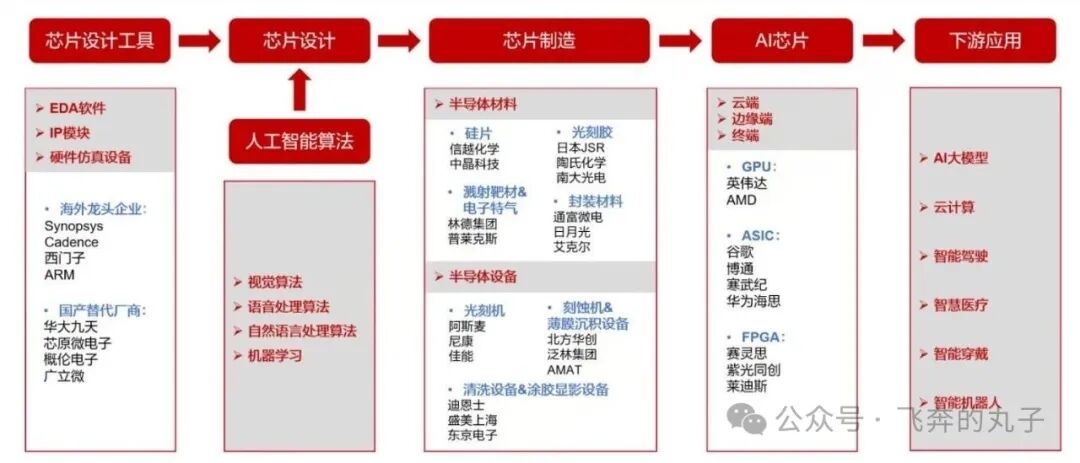

AI Chip Industry Chain

The upstream of the AI chip industry chain mainly includes AI algorithms, design tools, and semiconductor materials and equipment involved in manufacturing, including foundry and packaging/testing processes. AI chips can be widely applied in large models, cloud computing, and various intelligent terminal scenarios.

AI algorithms include visual algorithms, language processing algorithms, natural language processing algorithms, and machine learning.

Chip design tools mainly cover EDA software, IP modules, and hardware simulation devices.

AI chips can be categorized based on application scenarios into cloud, edge, and terminal AI chips. Downstream applications include, but are not limited to, AI large models, cloud computing, intelligent driving, smart healthcare, wearable technology, and intelligent robotics.

Market Size

Market Size

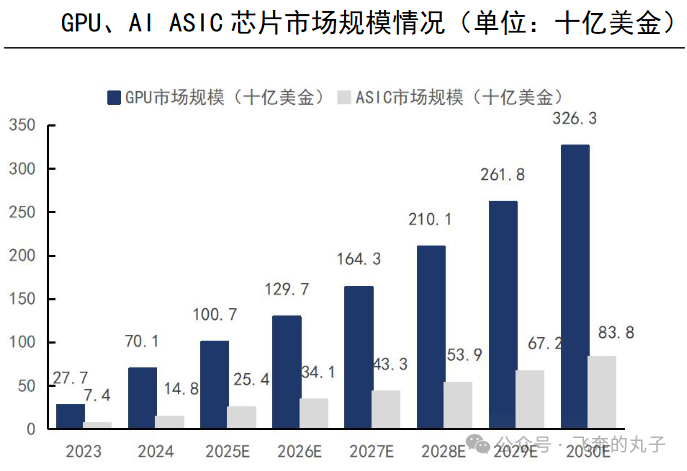

AI ASIC Market Size: Expected to reach $14.8 billion in 2024, with an anticipated growth to $83.8 billion by 2030.

ASIC chips are growing faster than GPUs in the training and dual-use AI chip sectors.

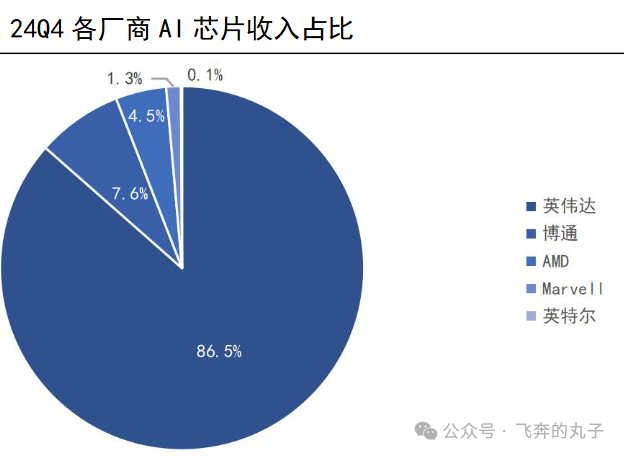

According to IDC data, in Q4 2024, the revenue shares of AI chips from NVIDIA, Broadcom, AMD, Marvell, and Intel are 86.5%, 7.6%, 4.5%, 1.3%, and 0.1%, respectively. Among them, NVIDIA and AMD are GPU compute cards, while Broadcom and Marvell provide custom ASIC chips for Google and Amazon, respectively. Intel develops its own ASIC chips. Summing the market shares of Broadcom, Marvell, and Intel, the AI ASIC chip share in Q4 2024 is 9.0%.

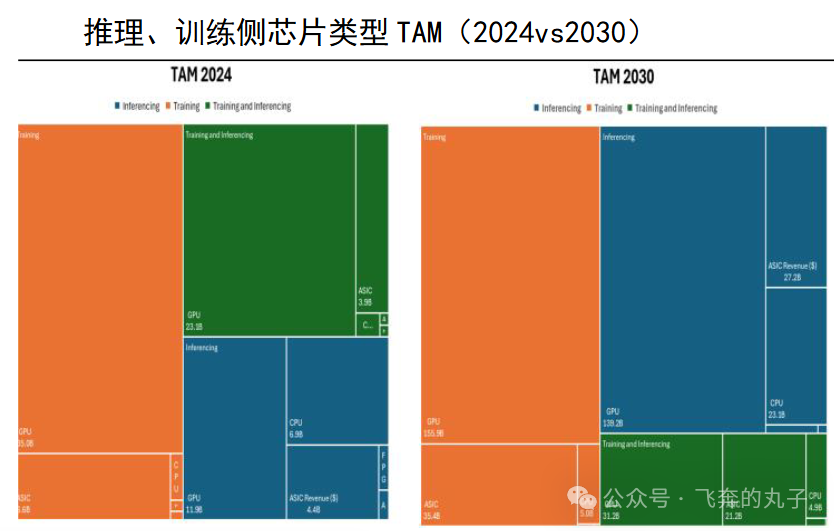

Training AI Chips: In 2024, the Total Addressable Market (TAM) for training AI chips is projected to be $35 billion for GPUs and $6.6 billion for ASICs, expected to rise to $155.9 billion and $35.4 billion by 2030, respectively, corresponding to a CAGR of 28.3% and 32.3% from 2024 to 2030.

Inference AI Chips: In 2024, the TAM for inference AI chips is projected to be $11.9 billion for GPUs and $4.4 billion for ASICs, expected to rise to $139.2 billion and $27.2 billion by 2030, respectively, corresponding to a CAGR of 50.7% and 35.5% from 2024 to 2030.

Dual-use AI Chips for Training & Inference: In 2024, the TAM for dual-use AI chips is projected to be $23.1 billion for GPUs and $3.9 billion for ASICs, expected to rise to $31.2 billion and $21.2 billion by 2030, respectively, corresponding to a CAGR of 5.1% and 32.6% from 2024 to 2030.

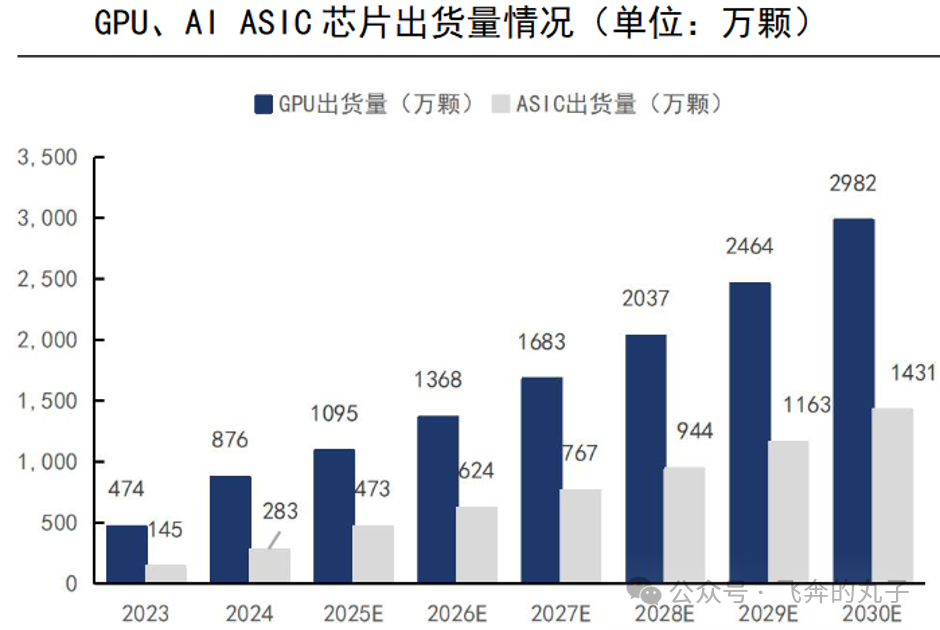

The market size and shipment volume of AI ASIC chips are growing rapidly. According to IDC data, in 2024, the market size for GPUs and AI ASIC chips is projected to be $70.1 billion and $14.8 billion, with shipment volumes of 8.76 million and 2.83 million units, respectively. By 2030, the market size is expected to increase to $326.3 billion and $83.8 billion, with shipment volumes rising to 29.82 million and 14.31 million units, respectively. The CAGR for both market size and shipment volume of AI ASIC chips from 2024 to 2030 is higher than that of GPUs, with a steadily increasing market share.

Domestic Production of AI Chips

Domestic Production of AI Chips

AI chips are divided into three main camps: GPGPU, FPGA, and ASIC, with domestic manufacturers primarily focusing on GPGPU and ASIC.

GPGPU: Highly versatile, used by NVIDIA, AMD, and others, with domestic options including Haiguang Information, Birun Technology, and Moore Threads;

ASIC: Highly customized and specialized, used by major internet companies like Google and Huawei’s Ascend, as well as Cambricon;

FPGA: Semi-customizable, with modifiable functions, high mass production costs, suitable for specific fields, with major manufacturers including Xilinx, Fudan Microelectronics, and Unisoc.

In the past decade, domestic AI chip manufacturers have rapidly emerged, and major internet companies have begun to launch their own AI chips to meet their business needs.

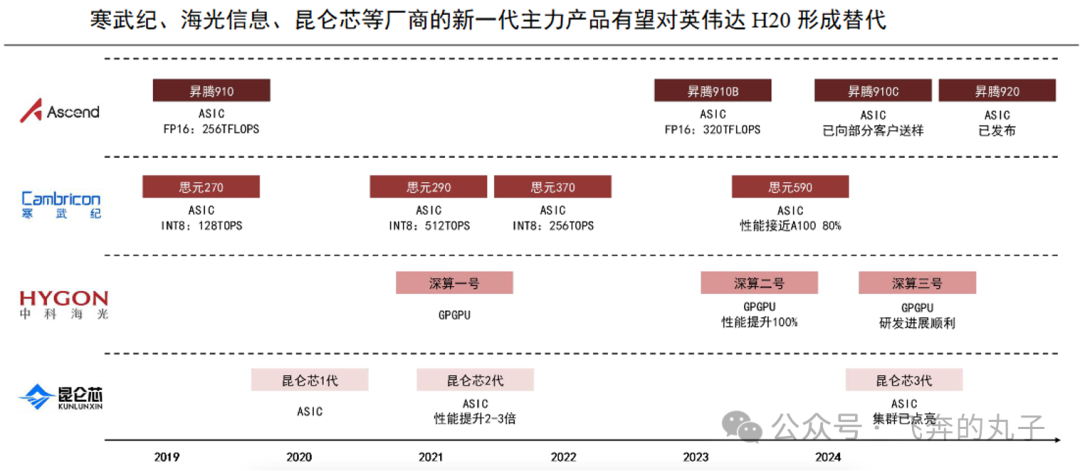

Domestic AI chip manufacturers represented by Huawei Ascend, Haiguang Information, Cambricon, and Kunlun are accelerating their catch-up with NVIDIA. Currently, Huawei’s Ascend 910B is already comparable to the A100, and the new generation 910C is expected to become a strong competitor to the H100.

Cambricon, Haiguang Information, and Kunlun are in the first tier of domestic AI chips, with their new generation flagship products, such as the Siyuan 590 chip, Deep Learning 3, and Kunlun 3, expected to potentially replace NVIDIA’s H20.

Images and References: IDC, Guosen Securities Economic Research Institute, Shanxi Securities Research Institute, and Xinghang Check, etc. This is for sharing purposes only and does not represent my personal stance or constitute investment advice.