Semiconductor measurement equipment is one of the core segments of semiconductor manufacturing equipment, ranking as the fourth largest subfield. It is essential for ensuring chip yield and is a key subdivision in the semiconductor manufacturing equipment sector. Its market size ranks fourth among semiconductor equipment subfields, spanning core processes such as wafer manufacturing and packaging testing, from nano-level defect detection to critical dimension measurement, directly determining chip performance and reliability.The shrinking evolution of each generation of processes imposes exponential growth requirements on the precision, speed, and sensitivity of measurement equipment. This technology-driven upgrade has become the strongest engine driving continuous market growth.

Measurement equipment marketshows steady growth, with Japan and the US remaining mainstream

In 2024, the global semiconductor industry is expected to recover, and the measurement equipment market is also showing a pattern of steady growth. According to various institutions, the global market size is estimated to range from $12.08 billion to $16.88 billion, with QYResearch reporting $12.08 billion. The compound annual growth rate (CAGR) from 2025 to 2031 is expected to reach 4.9%, potentially increasing to $16.83 billion by 2031. The growth is primarily driven by three core directions: the demand for process control due to continuous breakthroughs in advanced logic chip processes, capacity expansion in 3D NAND storage and high-bandwidth memory (HBM) fields, and the increased detection difficulty brought by complex structures such as AI chip heterogeneous integration and stacked packaging.

Especially in the context of explosive growth in the AI industry, the HBM chip market is expected to reach $12 billion by 2025, with a surge in demand for high-precision detection equipment during the packaging phase, further opening up market growth space.

This growth trend strongly echoes the overall recovery of the global semiconductor manufacturing equipment market. In 2024, the global semiconductor manufacturing equipment shipment value is expected to reach $117.1 billion, a year-on-year increase of 10%, with significant growth in both front-end wafer processing equipment and back-end packaging testing equipment, providing a broad application scenario for measurement equipment.

Notably, mainland China has become the largest market for measurement equipment globally, with a compound annual growth rate of 31.74% from 2017 to 2021. The continuous expansion of domestic wafer fabs and the demand for domestic substitution are driving the Chinese market to become the core engine for global measurement equipment growth.

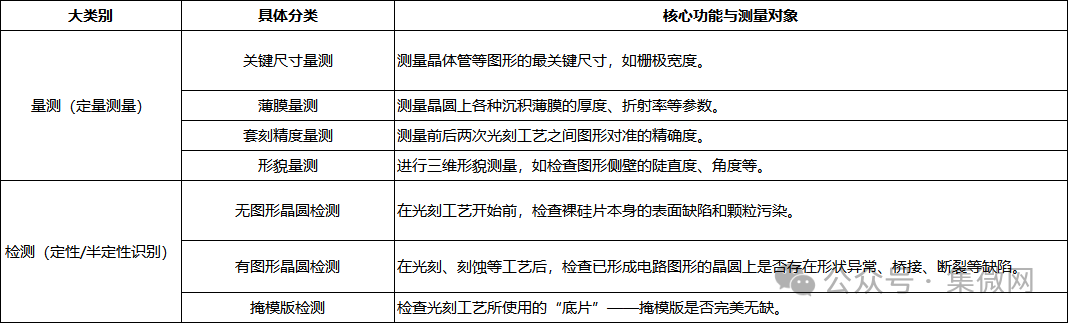

From a market structure perspective, semiconductor testing and measurement equipment show significant differentiation in subfields. According to VSLIResearch statistics, testing equipment accounts for 62.6%, dominating the market, including non-pattern wafer defect detection equipment, patterned wafer defect detection equipment, and mask inspection equipment, which are directly related to defect screening and yield control in the chip manufacturing process; measurement equipment accounts for 33.5%, covering three-dimensional morphology measurement equipment, thin film thickness measurement equipment, and overlay accuracy measurement equipment, focusing on precise control of critical dimensions and process parameters.

In the field of third-generation semiconductors, with the widespread application of materials such as silicon carbide (SiC), non-destructive testing has become a new market demand. The inefficiencies and destructive drawbacks of traditional chemical etching methods are becoming increasingly prominent, driving the upgrade of testing technology towards optical and high-speed methods.

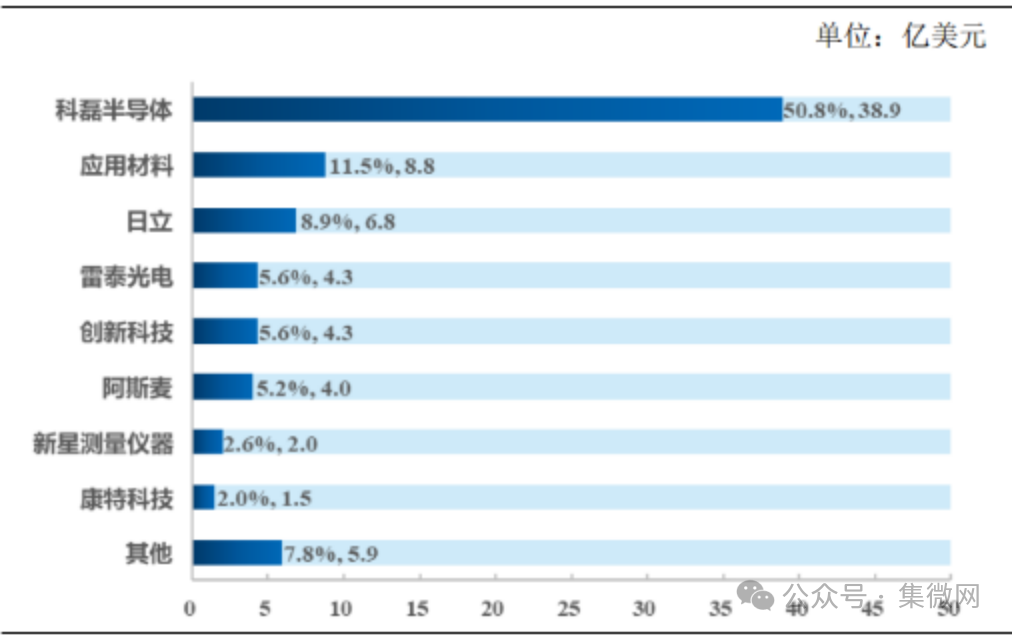

The global market structure exhibits typical oligopolistic characteristics. KLA Corporation in the United States continuously improves its technology and product matrix through ongoing acquisitions, maintaining an absolute dominant position globally, especially in the high-end testing field. Additionally, companies such as Applied Materials in the US, Hitachi High-Technologies in Japan, and Reticle Technologies collectively hold over 90% of the global market share due to decades of technological accumulation, stringent patent barriers, and strong customer loyalty.

Figure: The measurement equipment market is primarily dominated by US and Japanese companies

Source: Zhongke Feice prospectus (2020 data statistics, for market share reference only)

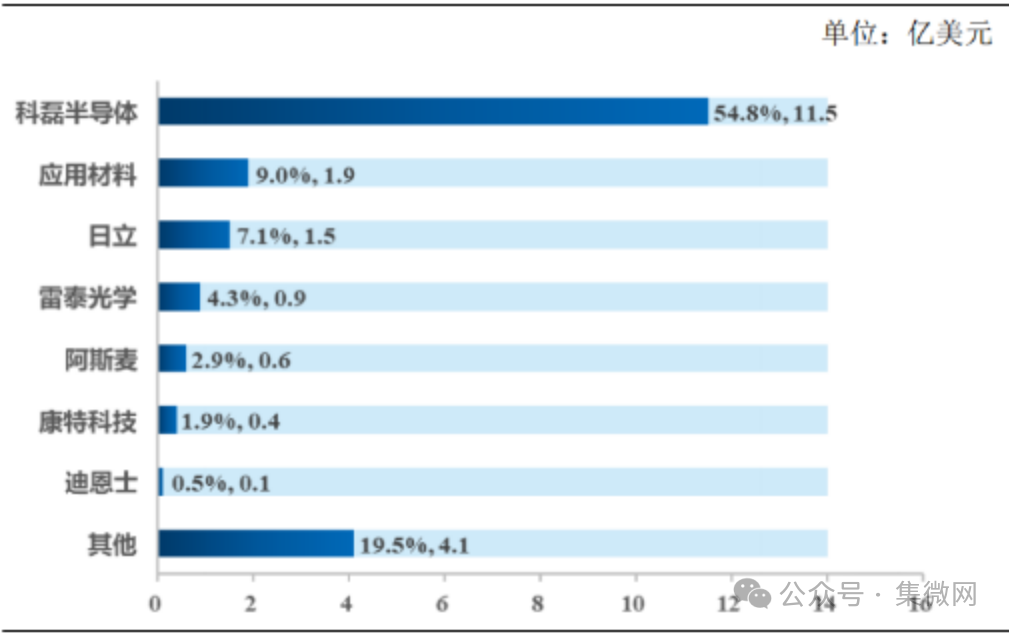

In the domestic market, this monopolistic pattern is even more pronounced, with KLA holding over 50% market share, while domestic manufacturers still face significant gaps in technical performance and brand recognition.

Figure: In the domestic measurement equipment market, KLA holds over 50%

Source: QYResearch, Zhongke Feice prospectus (for market share reference only)

Local manufacturersachieve breakthroughs in subfieldsand form a distinctive competitive landscape

Amid the wave of domestic substitution, domestic semiconductor measurement equipment companies are accelerating their breakthroughs. Although the combined market share of domestic manufacturers is still less than 5%, several outstanding companies have achieved breakthroughs in subfields, forming a distinctive competitive landscape.

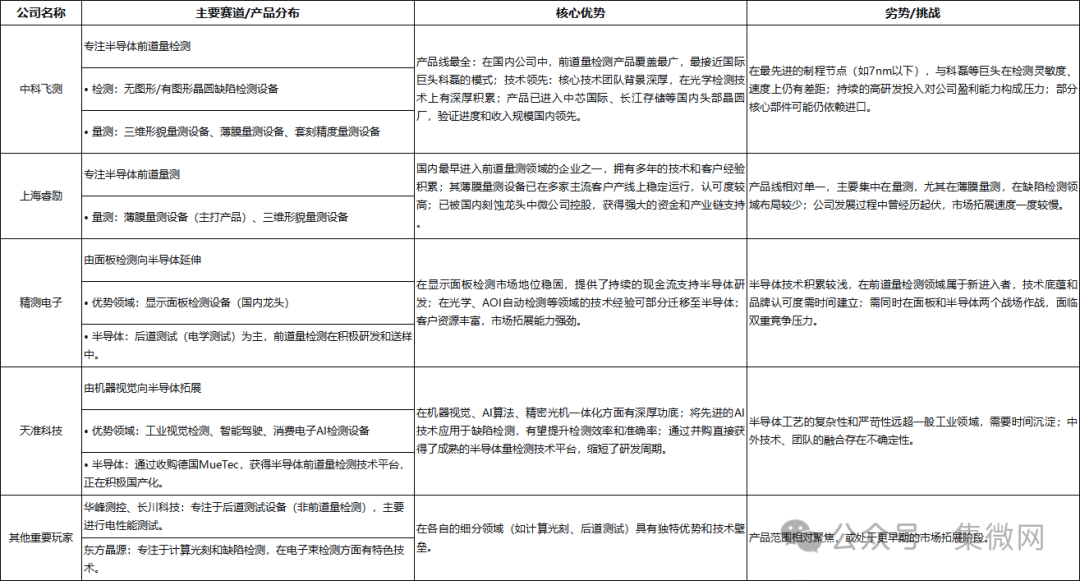

Zhongke Feice, as a leading enterprise in the domestic semiconductor front-end measurement field, has built the most comprehensive product line layout, covering core processes such as wafer defect detection and critical dimension measurement. The company’s core advantage lies in its deep technological accumulation and complete product matrix, with its equipment successfully entering leading domestic wafer fabs and receiving bulk orders, representing the highest level of domestic substitution. However, in the advanced process field, the company’s products still face performance gaps with international giants, and the high investment and long cycle of semiconductor equipment R&D continue to exert pressure on its profitability.

Shanghai Ruile is one of the earliest pioneers focusing on semiconductor front-end measurement in China. Its thin film measurement equipment has been validated in the market for a long time, becoming a flagship product in its subfield. Leveraging years of industry experience and the backing of leading equipment manufacturer Zhongwei, Shanghai Ruile has gained stable financial support and industrial resource synergy, establishing solid customer trust in specific measurement areas. However, limited by a relatively narrow product line, the company has a weak layout in key areas such as defect detection, and its market expansion speed has been somewhat slow in recent times, necessitating technological innovation to broaden its product boundaries.

Jingce Electronics has made a strong entry into the market by leveraging its cross-industry advantages. As an absolute leader in display panel testing equipment, Jingce Electronics possesses substantial financial strength, with its stable panel business providing strong cash flow support for its semiconductor business. Additionally, its technological accumulation in optical detection and automation control enables cross-domain synergy. Currently, the company’s products cover various categories, including film thickness measurement, critical dimension measurement, and electron beam defect detection, with its bright field equipment having completed its first set of deliveries and established partnerships with mainstream domestic wafer fabs. However, as a new entrant in the semiconductor field, its depth of core technology accumulation in front-end measurement and recognition by international brands still need improvement, facing intense competitive pressure from both panel and semiconductor businesses.

Tianzhun Technology’s breakthrough path focuses on technological integration and innovation. Originating from the industrial machine vision field, the company has acquired a high-level technology platform for semiconductor front-end measurement through strategic acquisitions, particularly excelling in combining advanced AI algorithms with machine vision technology to empower the localization and intelligence of its core technology platform. In the trend of AI-driven detection, this technological integration capability has become an important competitive edge. However, the complexity of semiconductor manufacturing processes is extremely high, and the company still needs to deepen its understanding of semiconductor processes quickly while completing cross-border technology integration and team merging to establish a foothold in the demanding semiconductor equipment field.

In addition to these industry stalwarts, a number of emerging companies are breaking the existing pattern through technological innovation. Dalian Chuangrui Spectrum is deeply engaged in the third-generation semiconductor defect detection field, with its SiC-MAPPING532 system being the world’s first third-generation semiconductor defect detection equipment based on transient spectral technology, achieving non-destructive detection of dislocation defects in silicon carbide substrates. It has now entered the systems of leading domestic customers and achieved overseas deliveries, becoming one of the few domestic companies exporting high-end detection equipment. Shenzhen Xinkailai has also made comprehensive layouts, showcasing 16 products, including optical detection equipment, at the Bay Chip Expo, covering all aspects of semiconductor manufacturing front-end. Its subsidiary, Wanlianyan, has launched a 90GHz ultra-high-speed real-time oscilloscope, filling the domestic gap in high-end testing equipment.

In the third-party testing service sector, companies like Shengke Nano have also achieved rapid growth. In the first half of 2025, Shengke Nano achieved operating revenue of 239 million yuan, a year-on-year increase of 29.03%, leading in subfields such as failure analysis and material analysis, with an estimated domestic market share of about 7.44% in 2024, becoming an important beneficiary of the trend towards specialization in the semiconductor industry chain.

Looking ahead, the semiconductor measurement equipment market will continue to grow under the dual drive of technological iteration and domestic substitution. On one hand, process miniaturization, material innovation, and the complexity of packaging processes will drive measurement equipment towards higher precision, faster speeds, and greater intelligence. Technologies such as AI algorithms, non-destructive testing, and multi-dimensional integrated testing will become the core of competition. On the other hand, the expansion demand of domestic wafer fabs and the combined benefits of domestic substitution policies will provide broad market space for local enterprises. Although the monopolistic pattern of international giants is unlikely to change drastically in the short term, with continuous breakthroughs by domestic companies in technology R&D, product iteration, and customer service, the market share of domestic measurement equipment is expected to steadily increase, transitioning from subfield substitution to comprehensive competition, gradually building a self-controllable semiconductor testing equipment industry chain, providing core support for the high-quality development of China’s semiconductor industry.

As industry insiders have said, China is the largest chip testing ground in the world and will undoubtedly become an important pole of global semiconductor technological innovation. The domestic breakthrough path of measurement equipment is a vivid reflection of this process.

Hot Topics:

1.Desperate Measures! Chip Giants Lay Off 35,500 Employees

2.Domestic GPU Leader Successfully Passes IPO3.Chip Equipment Giants Announce Layoffs of Over 1,400!4.Trump Plans to Restrict Exports of US Software Products to China, Confirmed by US Treasury Secretary5.Countdown to Rare Earth Regulation Deadline! Global Automakers’ Inventory Turns Red6.Anshi China Takes a Firm Stand: Has the Right to Refuse External Instructions7.Latest! Anshi Netherlands Refutes: “Not Consistent with Facts”!8.Reversal! Anshi Semiconductor Incident, Netherlands Hopes to Negotiate with China

Follow! Share! Like Together!↓↓↓