From early May to early September 2025, the PCB (Printed Circuit Board) sector in the A-share market experienced a remarkable upward trend. Several companies within the sector reached historical highs in stock prices, becoming a bright spot in this bull market.

The driving force behind this trend is the enormous demand generated by the construction of AI computing power infrastructure, as well as the industry’s upgrade trend towards high-end and refined development. As the “skeleton” of electronic products, the technology content and market demand for PCBs are undergoing profound changes.

01 PCB Concept and Industry Chain Structure

PCB (Printed Circuit Board) is the support and electrical connection provider for electronic components, often referred to as the “mother of electronic products.” The PCB industry’s supply chain is divided into upstream raw material suppliers, midstream manufacturers, and downstream application fields.

The upstream industry consists of raw material suppliers, including copper-clad laminates (copper foil, resin, fiberglass cloth, etc.), prepregs, copper balls, inks, etching solutions, and gold salts. Copper-clad laminates are a crucial raw material for PCB manufacturing, accounting for about 40% of the total material cost.

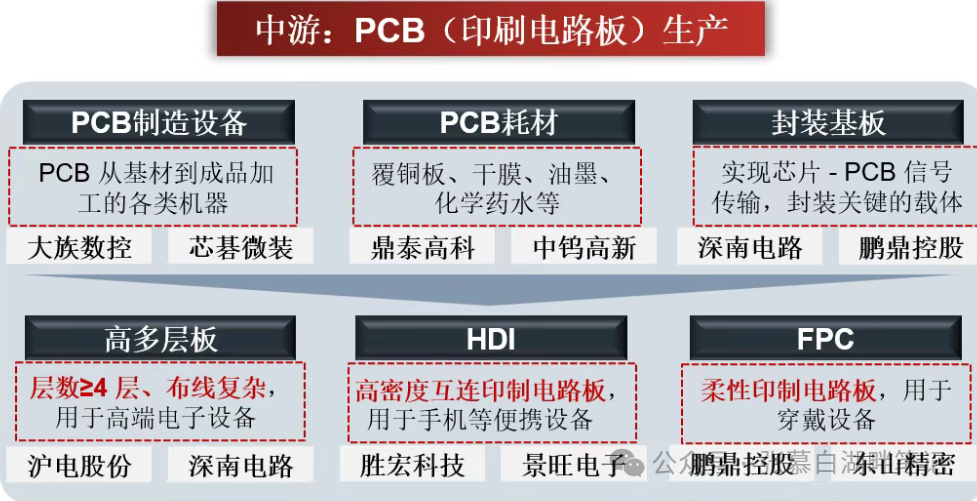

The midstream industry comprises PCB manufacturers, which produce PCBs through processes such as etching, including flexible boards, packaging substrates, high-layer boards, and HDI (High-Density Interconnect) boards.

The downstream application fields are extensive, including communication equipment, computers, consumer electronics, automotive electronics, industrial control, aerospace, and medical devices. The global PCB industry is expected to reach a total output value of $73.565 billion in 2024, a year-on-year increase of 5.8%, and is projected to reach $94.661 billion by 2029.

02 Market Position of Core Enterprises in Upstream and Downstream

Upstream Material Sector

Copper-clad laminates (Shengyi Technology, Jinan Guoji), copper foil (Tongguan Copper Foil), electronic cloth (Honghe Technology), epoxy resin (Hongchang Electronics), etc.;

Shengyi Technology (600183) is the largest copper-clad laminate manufacturer in mainland China, leading in high-frequency and high-speed copper-clad laminate technology, with an annual production capacity of about 100 million square meters, and has been supplying Huawei and ZTE for 5G base stations.

Jinan Guoji (002636) is one of the leading companies in copper-clad laminates, with main products including various general-purpose copper-clad laminates and special requirement products such as halogen-free environmental protection, high flame retardancy, CAF resistance, and high TG series, with an annual output exceeding 40 million sheets.

Midstream Manufacturing Sector

High-end PCB manufacturing (Huidian Co., Shenzhen South Circuit), HDI boards (Shenghong Technology), IC substrates (Xingsen Technology);

Pengding Holdings (002938) is a leading company in the global PCB industry, providing one-stop service capabilities and deeply binding with major clients such as Apple and Microsoft, with a 70% share of the iPhone series mainboards.

Shenghong Technology (300476) has a leading position in the AI computing power PCB field, with its core advantages reflected in ultra-high-end HDI technology, high-layer PCB mass production capabilities, and a full-stack layout for AI servers.

Huidian Co. (002463) is a leading PCB company in the automotive and communication sectors and is the only domestic manufacturer certified by NVIDIA for the GB300.

Shenzhen South Circuit (002916) is one of the leading companies in the domestic PCB industry and a leading enterprise in IC substrates. It ranks eighth among global PCB manufacturers and has three business segments: PCB, packaging substrates, and electronic assembly, with the capability to manufacture rigid-flex boards.

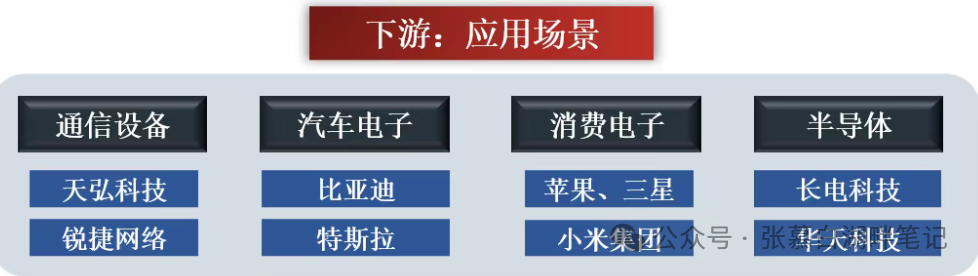

Downstream Application Fields

Communication equipment (Huawei/ZTE), AI servers (NVIDIA/Amazon), new energy vehicles (Tesla/ BYD), etc..

03 Deep Binding with Leading Brand Partnerships

Leading companies in the PCB industry have formed deep supply chain relationships with top global technology companies:

Shenghong Technology has established close cooperation with top global clients such as NVIDIA, Broadcom, AMD, Microsoft, and Tesla. The top five clients contribute over 50% of revenue, and by 2025, the AI business is expected to exceed 60%. The company is a primary supplier for NVIDIA’s H100/B200 GPU substrates, with orders for the GB200 NVLink full interconnect backplane expected to exceed 50% in 2025.

Founder Technology is a long-term stable PCB supplier for Huawei, covering communication equipment and consumer electronics. The company is also one of NVIDIA’s core PCB suppliers in the AI server GPU acceleration card field, with reports suggesting it has entered the supply chain for NVIDIA’s latest GB200 products.

Huidian Co. is the only domestic manufacturer certified by NVIDIA for the GB300, giving it a significant advantage in the AI server PCB field.

Pengding Holdings has deep ties with major clients such as Apple and Microsoft, with a 70% share of the iPhone series mainboards.

Bomin Electronics’ products are applied in communications, medical, automotive, and other fields, achieving breakthroughs in high-end PCB products such as AI servers and automotive electronics.

04 Sector Growth and Speculation Roadmap

Phase Growth Analysis

From June 3 to September 5, the PCB sector experienced a significant phase of growth:

First Phase (Early May to Early July): AI Computing Logic Fermentation

In the early stages of the market, attention focused on the PCB demand upgrade brought by AI servers. Companies like Shenghong Technology and Huidian Co., which directly benefit from the NVIDIA supply chain, were the first to take off. Shenghong Technology’s Q1 performance explosion validated its technological breakthroughs, with net profit increasing by 272%-367%, and a dynamic PE of 25 times indicating elasticity.

It is worth noting that before the overall startup of the PCB sector, the leading stocks were in the raw material branches, particularly electronic cloth and copper foil, with representative stocks including:

Copper Foil:

Tongguan Copper Foil

Defu Technology

Electronic Cloth:

Honghe Technology/Zhongcai Technology

Second Phase (Mid-July to End of August): Diffusion and Supplementary Growth

The trend spread across the entire industry chain, with upstream material manufacturers like Shengyi Technology and Jinan Guoji beginning to perform. Shengyi Technology, as a high-end CCL supplier, has a market share exceeding 30%, with a gross margin of 40% for AI server materials. Meanwhile, companies like Jingwang Electronics (core supplier of BYD’s intelligent cockpit PCBs) in the automotive electronics direction and Pengding Holdings (exclusive supplier of Apple’s AI phone SL boards) in the consumer electronics direction also experienced supplementary growth.

Third Phase (Early September): Divergence and Full Explosion Again

From September 2 to 4, there were three consecutive days of significant adjustments, and on September 5, the PCB sector reached a climax, with stocks like Shenghong Technology, Founder Technology, Tiantong Co., and Guanghua Technology hitting the daily limit, with many stocks in the sector rising over 5%. On that day, over 29 billion in main funds flooded into the electronic sector, with Shenghong Technology hitting a 20CM daily limit, and its stock price reaching a historical high.

05 Market Driving Logic and Future Reasoning

The core logic behind this round of speculation

AI computing demand explosion: The PCB value of AI servers is 3-5 times higher than that of traditional servers. For example, the PCB value of NVIDIA’s GB200 cabinet reaches $171,000/cabinet, second only to the GPU in hardware cost proportion. Shenghong Technology’s technological strength and market share in the AI computing power PCB field are globally leading.

Product structure upgrade and gross margin improvement: High-end products (such as high-end HDI and high-frequency high-speed boards) have gross margins 10-15 percentage points higher than ordinary products. AI servers are driving the high-end iteration of PCBs, creating demand for more advanced manufacturing equipment such as high-precision drilling and laser processing.

Accelerated domestic substitution: High-frequency and high-speed copper-clad laminates are rapidly replacing overseas suppliers like Rogers, with domestic dielectric materials approaching international levels, driving a 20% increase in single-board ASP. Domestic policies are intensifying “new quality productivity,” with the National Development and Reform Commission including FC-BGA substrates and ABF materials in national key projects.

Multiple explosions in downstream demand: Including AI computing infrastructure (major internet companies adjusting capital expenditures for 2025), automotive electronics upgrades (smart driving penetration rate increasing to 45%), and consumer electronics recovery (Apple’s AI phones, Vision Pro, and other edge AI hardware iterations).

Future Speculation Reasoning

Based on this round of PCB trends, future speculation can follow the reasoning framework below:

Leading technological iteration: Focus on companies that can achieve technological breakthroughs first, such as Shenghong Technology’s 8-layer 28-layer HDI technology and Shenzhen South Circuit’s mSAP process. Technological barriers constitute the moat for enterprises and are the core driving force for stock price increases.

Deep customer binding: Suppliers with deep ties to top global technology companies have more certainty, such as Shenghong Technology’s top five clients contributing over 50% of revenue and Pengding Holdings’ 70% share of iPhone series mainboards. Deeply bound supply chain relationships imply sustainability of performance.

Proactive capacity layout: Accelerated capacity layout in Southeast Asia, with Thailand’s PCB industry investment reaching 162 billion baht, and companies like Shenghong Technology and Jiantao Laminates planning to start production in Thailand by 2025, avoiding tariff risks and taking on overseas orders. Global capacity layout has become an important competitive advantage.

Policy support strength: Domestic policies are intensifying “new quality productivity,” with PCB companies purchasing high-end equipment eligible for subsidized loans (interest rates as low as 1.75%). Policy support directions often attract long-term funding favor.

With the continuous growth of demand in AI, automotive electronics, and consumer electronics, along with deepening technological iterations and domestic substitutions, companies with core technologies, deep ties to leading customers, and global layout capabilities will continue to lead industry development.

In the future, investors can pay attention to the progress of companies in emerging fields such as new-generation server platforms, autonomous driving, AR/VR, and breakthroughs in materials and processes, as these may become the ignition points for the next round of market trends.