Recently, Genmab quietly removed another ADC—GEN1160 (targeting CD70) from its clinical list, citing only one reason: “slow enrollment of participants.”

This follows the announcement in September to abandon the PTK7 project GEN1107, marking the second “vessel” lost from the same $1.8 billion acquisition.

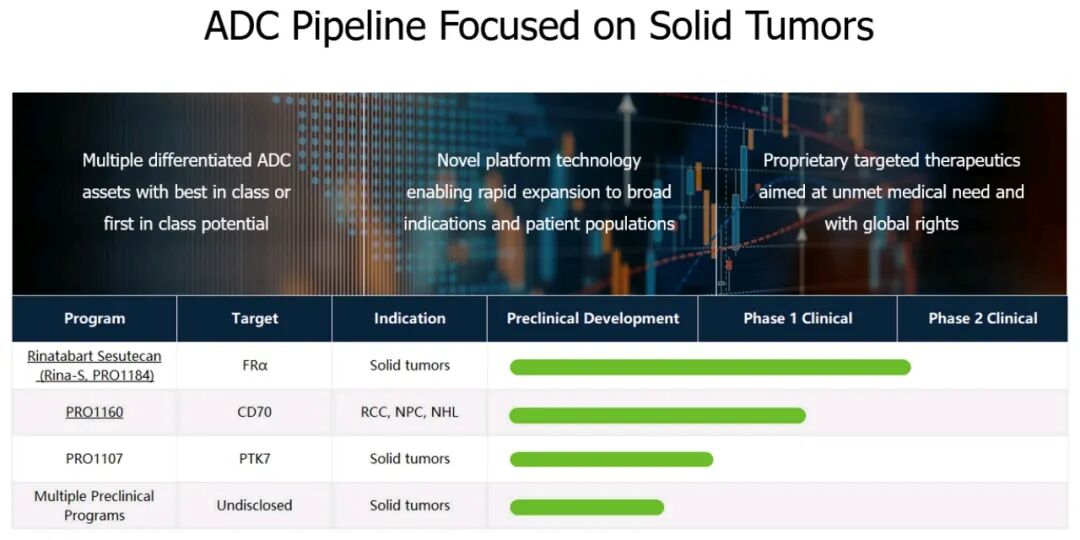

As of now, the three clinical “tickets” sold to Genmab by ProfoundBio have dwindled to just one: Rina-S (FRα-ADC), which is still navigating the waters of Phase III ovarian cancer trials.

From a “trio” to a “unicycle”

In April 2024, Genmab swallowed ProfoundBio, a Seattle-based company with Chinese roots, for $1.8 billion in cash, marking its largest acquisition in 25 years. At that time, the asset package included:

– Rina-S (rinatabart sesutecan, FRα-Topo1 inhibitor ADC) — Phase III, main focus

– GEN1160 (CD70-MMAE ADC) — Phase I/II, targeting renal cell carcinoma, nasopharyngeal carcinoma, NHL

– GEN1107 (PTK7-MMAE ADC) — Phase I/II, targeting multiple solid tumors

Now, less than two years later, in September of this year, GEN1107 was abandoned due to an “insufficient benefit-risk ratio,” and now GEN1160 has been halted due to “slow enrollment,” leaving only Rina-S as the last remaining candidate.

For a nearly $20 billion antibody giant, the only thing that seems to justify the investment is likely the Phase III data for Rina-S and the ADC platform know-how from ProfoundBio.

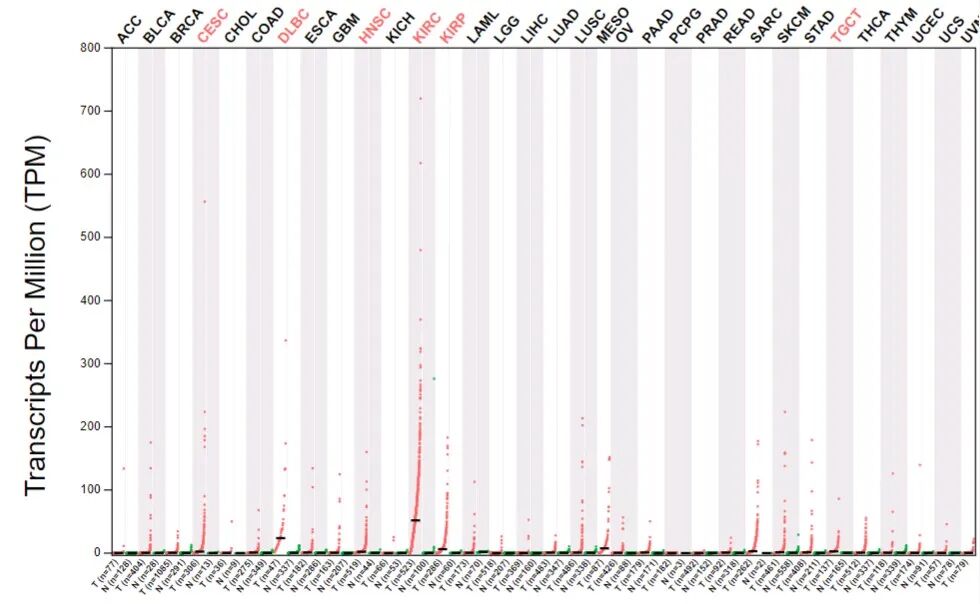

CD70-targeted GEN1160 is not the first to “fall behind”

CD70 is an “old target” in tumor immunology, expressed in renal cancer, nasopharyngeal cancer, and some hematological malignancies, but is almost not expressed in normal tissues, theoretically providing a wide safety window. However, overall, the absolute expression levels of CD70 are relatively low.

The development of ADCs targeting this site has already seen many failures:

In 2014, Seattle Genetics (now Seagen) halted SGN-75 (CD70-MMAF) in Phase II due to high toxicity.

In 2021, Celldex’s CD70-ADC was internally cut due to limited efficacy.

In 2023, AbbVie quietly withdrew its CD70 ADC from the pipeline.

GEN1160 follows the traditional VC-MMAE technology route; although the hydrophilic linker has been optimized, the “target + toxin” combination has failed to escape the gap between safety and efficacy.

A Genmab spokesperson admitted that after 18 months of trial initiation, fewer than 30 cases had been enrolled, stating, “Continuing to burn money is not meaningful.” In the CD70 field, speed is a lifeline; slow enrollment often indicates insufficient voting from doctors and patients regarding “expected benefits.”

Streamlining the pipeline or squeezing valuation?

After cutting two ADCs, Genmab’s public stance has consistently been “strategic focus.” However, the capital market is more concerned with how much premium from the $1.8 billion will be written down in one go. Referring to Incyte’s $240 million write-down in 2023 due to two Phase I failures, it would not be surprising if Genmab reports a $300-400 million write-down in its annual report this year.

The good news is that Rina-S is still running fast. The FRα-ADC field has been validated by ImmunoGen/AbbVie’s Elahere, with global sales expected to exceed $900 million in 2024.

Genmab plans to read out Phase III data in the first half of 2026; if the ORR and PFS outperform Elahere, there is still a chance to leverage peak sales of over $2 billion. In other words, as long as Rina-S succeeds, the $1.8 billion can be recouped; if it fails, this acquisition will completely devolve into “buying a platform and getting a lottery ticket.”

Conclusion: “The Last One Standing”

The tuition Genmab has paid for this acquisition has transformed “diversification” into “concentrated firepower.” If Rina-S succeeds in 2026, all doubts will vanish; if it fails, the $1.8 billion will only leave behind a technology platform and several preclinical molecules. For Chinese biotech companies currently queuing to “sell themselves,” ProfoundBio’s experience serves as a mirror: high-premium acquisitions are not the end, but the beginning of a more brutal elimination race.