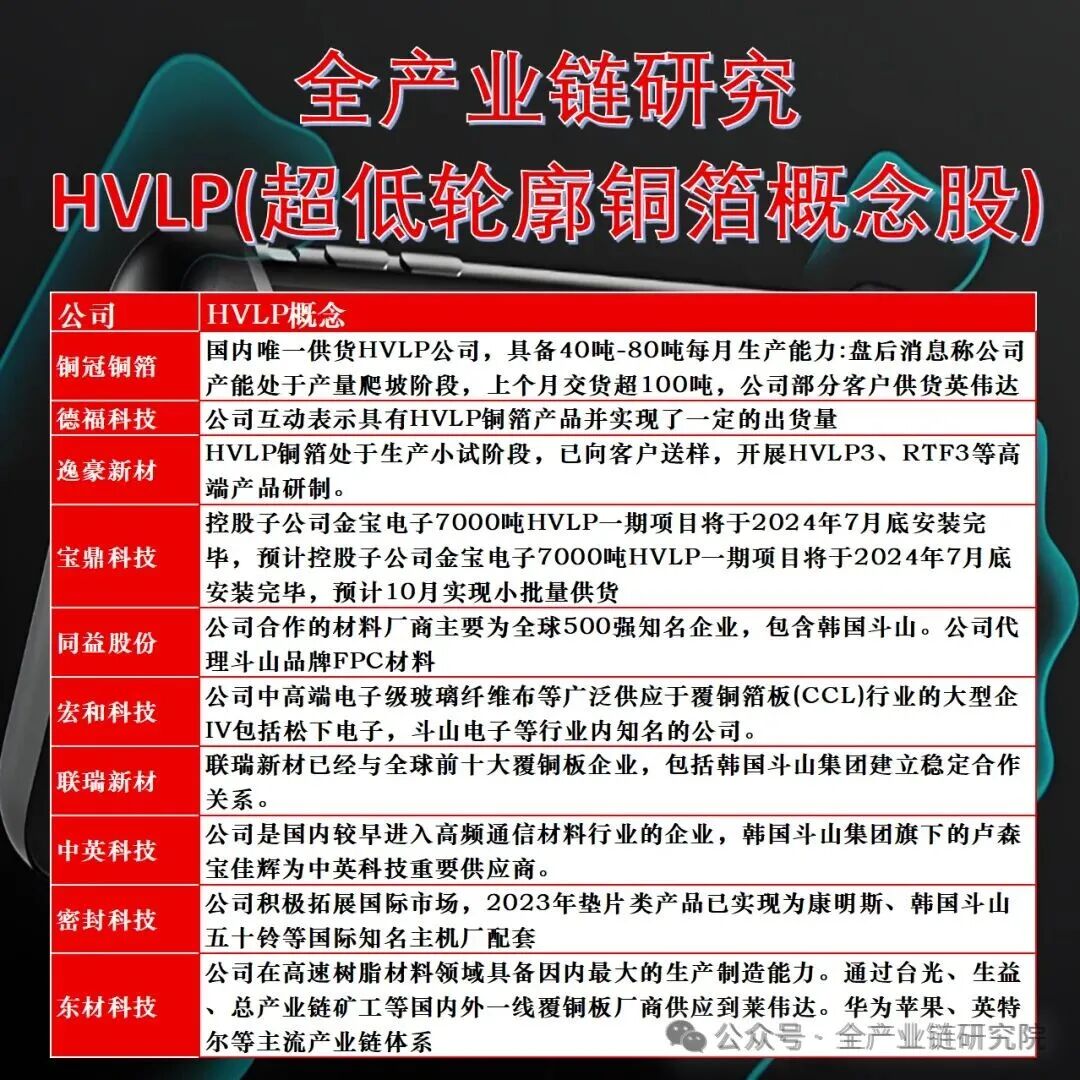

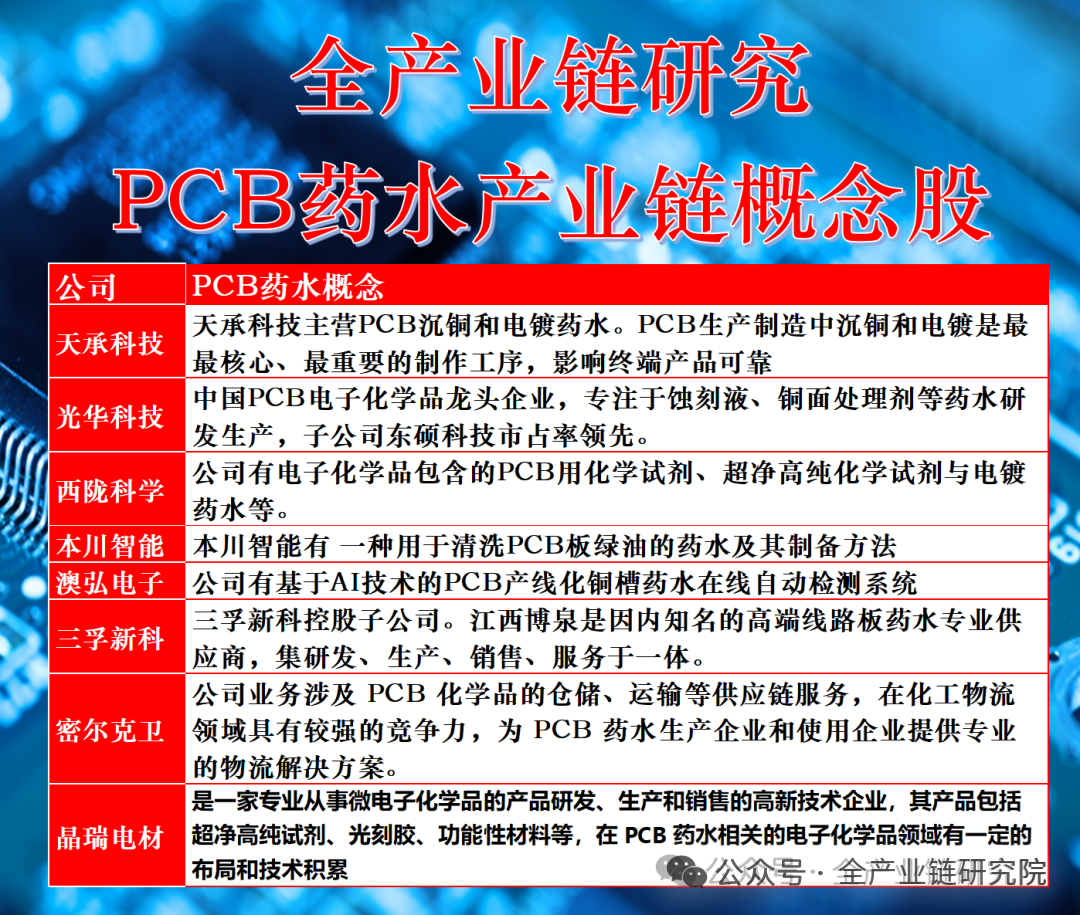

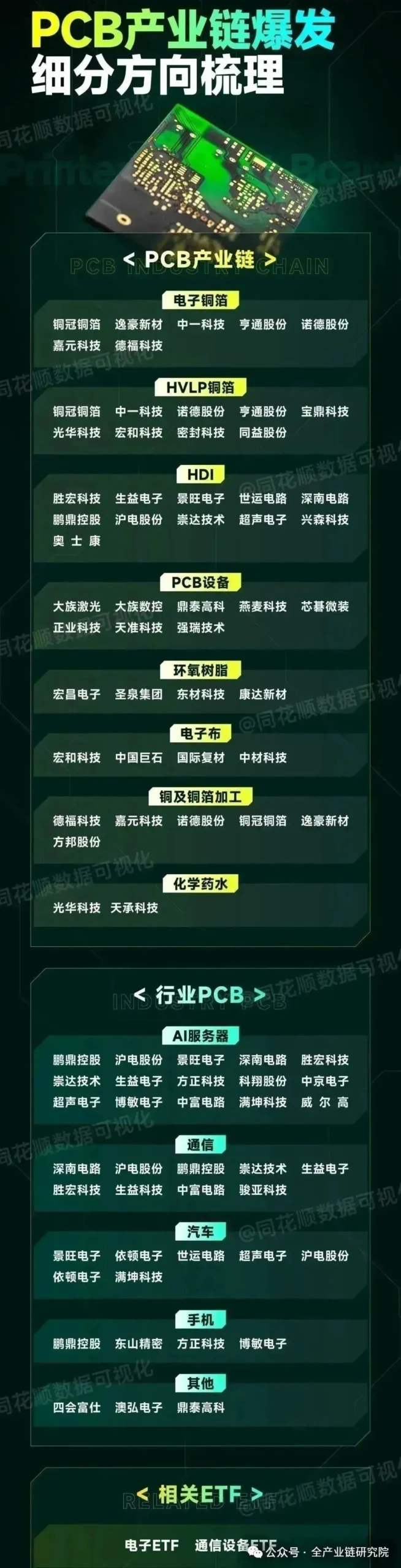

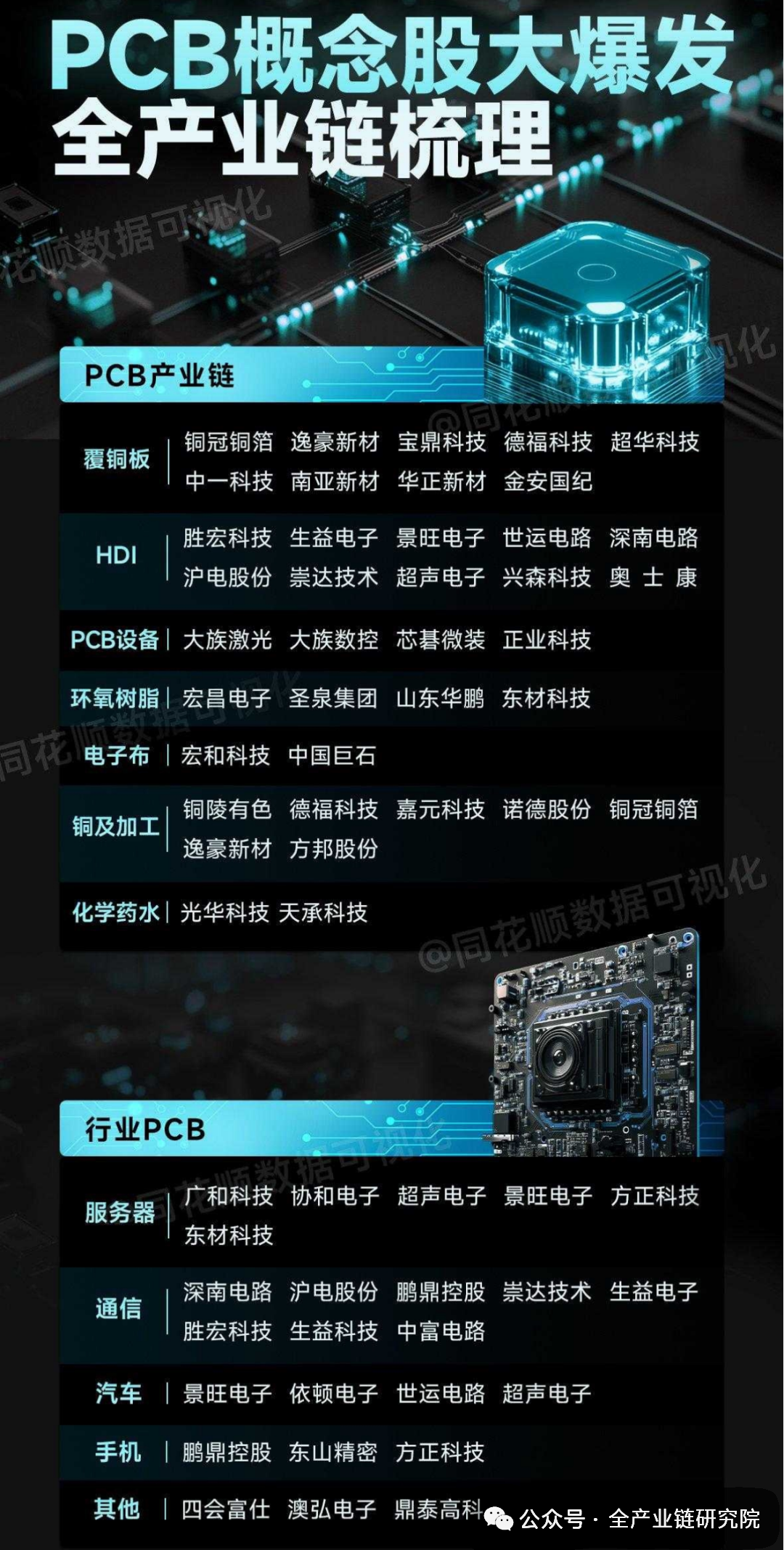

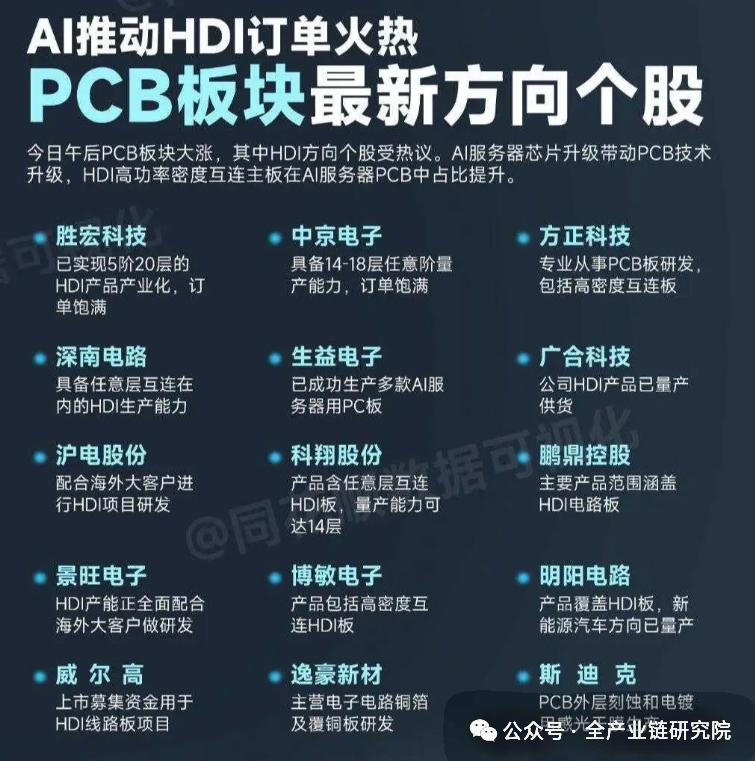

1. Overall Perspective and Core Logic of the PCB Supply ChainThe industry outlook is optimistic with three core reasons: First, the demand for AI computing power is strong and expected to continue, driving the demand for AI PCBs positively; second, the technical specifications and capacity consumption of AI PCBs are significantly higher than traditional PCB products, enhancing product value and positively impacting industry capacity consumption and process patterns; third, the supply landscape for AI PCBs is shifting towards domestic manufacturers. Domestic PCB manufacturers have invested in equipment and talent over the years, seizing the AI opportunity, with companies like Shenghong Technology showcasing China’s PCB manufacturing strength and service efficiency. In the future, domestic manufacturers will continue to leverage their supply chain advantages and engineer dividends, with market and supply shares expected to gradually increase.2. Analysis of the Copper Clad Laminate MarketTechnological Development and Market Scale: Copper clad laminate is a core upstream component and major cost of PCBs, with its technology evolving from standard boards to lead-free halogen-free boards and high-frequency high-speed boards. Traditional copper clad laminates, due to high pollution, are transitioning to lead-free halogen-free boards to meet environmental and performance requirements; with the improvement of chip performance and communication speeds, especially under the high demand for AI computing power, the demand for high-end products like high-frequency high-speed copper clad laminates is increasing, with accelerated penetration and tight processes for high-end high-speed boards. The global copper clad laminate market is expected to reach approximately $13.56 billion in 2024, with an estimated 8% year-on-year increase to $14.66 billion in 2025; driven by demand in AI and 5G equipment, it is projected to reach $20.17 billion by 2029, with a CAGR of 8.3% from 2025 to 2029.Competitive Landscape and Price Dynamics: In 2023, the global rigid copper clad laminate competitive landscape shows that Kingboard holds a 10%-15% market share, leading the top four manufacturers (Kingboard, Shengyi Technology, Taiko Electronics, and Nan Ya Plastics) with a combined market share of 48%. The price of copper clad laminates is positively correlated with copper prices and price increases benefit manufacturers’ profit margins. For instance, in 2021, the average spot price of LME copper rose by 51% compared to 2020, and Kingboard’s gross margin for copper clad laminate business reached 34%, an increase of 7 percentage points year-on-year. The LME copper price is expected to rise steadily in 2025, following an 8% year-on-year increase in the average spot price in 2024, with a further increase of about 4% from January to June 2025. Due to rising raw material prices, Kingboard raised the price of FR4 by 5 yuan per sheet in February and again by 10 yuan per sheet in August. As a leader, its price increase is expected to drive other manufacturers, and with downstream demand declining, price transmission is smoother, leading to a potential recovery in profit margins for related manufacturers.The Trend Towards High-End Products and Domestic Substitution: Currently, copper clad laminates are trending towards high-end products, with the specifications of AI PCBs driving upgrades in core raw materials like copper clad laminates, with demand for materials above 6 layers being strong. As AI chip platforms iterate, high-speed materials are transitioning from M6 to M8, significantly increasing in value, with M8 prices more than doubling compared to M6. Goldman Sachs predicts that the CAGR for the high-end copper clad laminate market will reach 26% from 2024 to 2026, exceeding the overall growth rate. Previously, the high-end copper clad laminate market was dominated by manufacturers from Taiwan and overseas, but in recent years, domestic manufacturers have improved their technology, with mid-to-high-end product performance approaching international levels; companies like Shenghe Technology have become core suppliers for AI PCs. Under these dual factors, domestic high-end copper clad laminates are poised for development opportunities, with high profitability expected to improve the profit levels of domestic manufacturers.3. Analysis of PCB ManufacturingIndustry Growth and Regional Distribution: Benefiting from innovations in AI, automotive electronics, and a recovery in traditional downstream demand, the PCB sector is in an upward cycle. Prismark’s forecast data indicates that the global PCB output value will grow to $73.57 billion in 2024, and is expected to reach $94.66 billion by 2029, with an average annual compound growth rate of 5.2% from 2024 to 2029. In terms of regional distribution, China is the core of global PCB production, with the PCB output value in China expected to account for 56% of the global total in 2024; other Asian countries will account for 29%; Japan will account for 8%.Product Structure and Domestic Market: Based on output value, multilayer boards with 4-6 layers are expected to be the largest PCB type globally in 2025, with a year-on-year increase of 2% to $16.069 billion. Driven by the demand for AI computing power, related PCB product specifications are upgrading, with output values for multilayer boards above 18 layers and HDI expected to grow rapidly, with year-on-year growth rates of 41.7% and 10.4% respectively in 2025. In the domestic market, benefiting from the technological advancements of packaging substrate manufacturers and the demand for domestic substitution, in addition to the rapid growth of output value for high multilayer HDI above 18 layers, the output value of domestic packaging substrates is expected to increase by 7.5% year-on-year to $3.331 billion in 2025.Catalytic Factors and Domestic Advantages: Catalytic factors in PCB manufacturing include: first, AI is driving increased demand for high-end PCB products, with technical specifications improving alongside AI chip platform iterations. Traditional server PCBs mainly consist of 10-20 layer multilayer boards, while AI server PCBs average over 20 layers and show trends towards stacking and increasing layers; the performance, power consumption, and cabinet concentration of AI chips promote the growth of high-end HDI, such as NVIDIA’s Blackview series using 5-layer HDI, and the Ruby series expected to use 6-7 layer HDI in 2026-2027, along with new PCB products like middle-back boards and new technologies like Kewop. Second, the upgrade of PCB specifications and technology increases the consumption of high-end products, coupled with yield limitations, high-end PCB capacity is expected to remain tight until 2026, supporting high-end product prices and maintaining high profitability for AI PCBs; leading manufacturers’ orders overflow, allowing second-tier manufacturers to improve profitability for traditional products. Third, domestic PCB manufacturers have accumulated technology to reach international top levels, possessing capacity positioning advantages, and are expected to increase market share in the AI PCB sector in the future.4. Investment Recommendations and Risk AlertsSpecific Investment Targets: In the context of sustained demand for high-value-added products like AI and PCBs, the performance of related PCB industry companies is expected to develop rapidly. For copper clad laminates, it is recommended to pay attention to Nan Ya New Materials and Shengyi Technology; for PCB manufacturing, focus on Shenghong Technology, Huadian Co., Jingwang Electronics, Shenglan Circuit, Shengyi Electronics, and Xinxing Technology.Main Risk Factors: Currently, the downstream application fields of electronics are showing signs of weak recovery, and if subsequent sales demand recovery slows, it may impact the performance of industry chain companies. The R&D progress of new technologies by domestic manufacturers may not meet expectations, as technological advancement is the source of competitiveness for related industry chain targets; if advanced technology innovation and R&D are hindered, it may be difficult to meet the market’s higher-end demands. Additionally, attention should be paid to the risk of fluctuations in raw material prices, as raw materials are the core cost source for PCB production and manufacturing; if raw material prices fluctuate and companies cannot respond effectively, it may impact profitability.