【Core Conclusion】Research report predicts that from 2025 to 2027, the company’s net profit attributable to shareholders will be 1.03 to 1.52 billion yuan, and 2.01 billion yuan, as the acceleration of equipment informationization evolves, the downstream market for the company’s products is expected to expand, opening up growth space. A valuation of 45 times for 2026 is given, corresponding to a target price of 40.83 yuan. Initiating coverage with a “Buy” rating.

【Main Logic】Zhimingda is a leading enterprise in the domestic embedded computer industry in key areas, providing customized solutions, products, and services related to embedded computers for key domestic clients based on customer needs. The company is positioned in the midstream, with profit margins expected to recover. The upstream electronic components are mature and supply is stable, while the localization of integrated circuit chips is rapidly increasing; the downstream mainly consists of military research institutes, with a high degree of product customization. Once standardized, products will enter mass production and procurement. As the mechanization, informationization, and intelligence of military equipment continue to improve, the demand for embedded computers will also continue to grow. The company is positioned in the midstream, and profits are expected to recover. As a flexible private enterprise, it is seizing the incremental market. As one of the few qualified high-quality private enterprises, the company has established long-term stable cooperative relationships with clients, possessing certain advantages in flexible production mechanisms, effective incentive measures, and rapid response. The downstream applications are diversifying, and the market space is expanding. The company’s embedded computer products are mainly used in airborne, missile-borne, commercial aerospace, and drone scenarios, with strong demand. The company plans to raise 213 million yuan to seize opportunities in commercial aerospace and unmanned equipment.

Risk Warning: Fluctuations in orders may lead to performance volatility; risks of intensified market competition; risks of digesting new production capacity from fundraising projects and the risk of significant capital investment without profitability in the short term.

1. Company Introduction

1.1 Military Embedded Computer “Little Giant”

Chengdu Zhimingda Electronics Co., Ltd. was established in March 2002, headquartered in Chengdu, Sichuan Province. The company was formerly known as “Chengdu Real-time Digital Equipment Co., Ltd.” and changed its name to “Chengdu Zhimingda Digital Equipment Co., Ltd.” in 2004. In April 2021, the company was listed on the Shanghai Stock Exchange’s Sci-Tech Innovation Board.

The company is a leading enterprise in the domestic embedded computer industry in key areas, mainly serving military clients by providing customized solutions, products, and services related to military embedded computers. Over the past 20 years, the company has continuously focused on the research and manufacturing of military embedded computer module products, dedicated to researching the adaptation of embedded real-time operating systems and driver programs, as well as application program development. Combining the characteristics of users in key national areas, the company adopts a “hardware customization + software customization” approach to meet customer application needs.

The shareholding structure is stable, and long-term incentives motivate core employees to enhance their enthusiasm. Core technical personnel, including Chairman Wang Yong, are the company’s controlling shareholders, with Wang Yong and Zhang Yue holding a combined 30.55% of shares as of the first half of 2025. Core technical personnel Jiang Hu and Long Bo have been with Zhimingda since its founding in 2005, with nearly twenty years of experience. In 2016, the company established a core employee shareholding platform, Chengdu Zhiwei, which holds a total of 4.66% of the company’s shares.

Holding shares in Mingkesiwei, laying out upstream ADC chips. Mingkesiwei, established in 2008, focuses on the design and provision of solutions for core signal chain chips, with main products including high-precision ADC product lines, high-speed ADC product lines, and X-band high-performance silicon-based RF chips. As of the first half of 2021, Mingkesiwei had approximately 40 cooperative clients, mainly military research institutes, and had achieved sales cooperation with 14 clients, with over 10 products entering mass production. In September 2021, the company increased its investment in Mingkesiwei with its own funds, holding 34.99% of its shares. Due to the significant R&D investment required for ADC chip products, there were initial losses, with losses of 50.13 million and 39.17 million yuan in 2023 and 2024, respectively. In July 2023, the company announced the transfer of part of its shares in Mingkesiwei, and it currently holds 18.45% of Mingkesiwei’s shares.

1.2 Demand Recovery, Orders Reach Historical Highs

Deeply engaged in airborne and missile-borne businesses, expanding into commercial aerospace and drones. After years of accumulation, the company has formed a rich product series, widely applied in airborne and missile-borne fields. In 2024 and the first half of 2025, the company achieved operating revenues of 438 million and 295 million yuan, respectively, with year-on-year changes of -33.95% and +84.83%, due to increased customer demand and a significant increase in orders in the first half of 2025, leading to a substantial increase in delivery and revenue; achieving net profits attributable to shareholders of 19 million and 38 million yuan, with year-on-year changes of -79.79% and +2147.93%.

Airborne and missile-borne products are the core sources of revenue, with rapid growth in drone and commercial aerospace revenues. From the revenue composition, in 2024 and the first half of 2025, the airborne business accounted for 63.60% and 67.72%, respectively; the missile-borne business accounted for 10.14% and 3.22%. The company continues to acquire new research projects, laying a solid foundation for the sustainability of future orders.

At the end of 2024 and the beginning of 2025, customer demand surged, with new orders reaching historical highs in the first quarter of 2025. In 2024, due to industry environmental impacts, orders for multiple models were delayed, and new orders fell short of expectations, leading to reduced deliveries. However, at the end of 2024 and the beginning of 2025, with a significant increase in customer demand, as of the end of the first quarter of 2025, the company had an order backlog of 750 million yuan (including verbal orders), a year-on-year increase of 174%, setting a historical record; as of the end of the first half of 2025, the company had an order backlog of 608 million yuan (including verbal orders), a year-on-year increase of 73.71%.

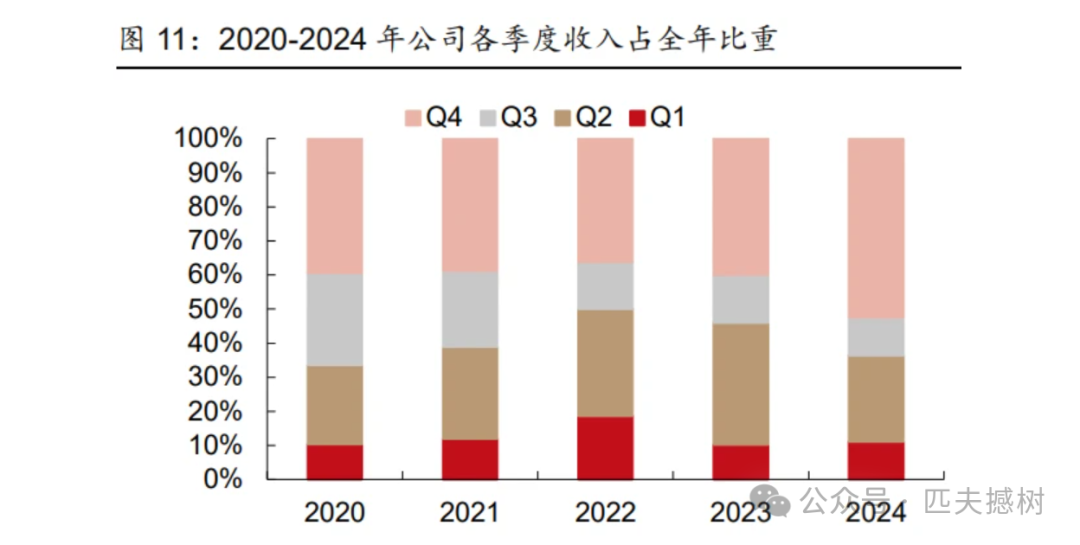

Seasonal fluctuations are significant, with the second and fourth quarters being peak delivery seasons. Due to the concentration of traditional holidays in the first half of the year, as well as factors such as customer annual budget preparation and issuance, supplier responses, delivery, and settlement habits, the sales situation in the second half of the year is generally better than in the first half. Typically, the delivery volume in the second half of the year accounts for about 60% of the annual total, with the fourth quarter accounting for about 40%.

1.3 High Customization, Optimized Supply Chain Management Improves Profitability

Long R&D cycles and small-batch customization. Military products have high requirements for process design, raw material quality, and operational stability. The company’s products also feature long R&D cycles and small-batch customization, with delivered products including hardware and accompanying software, resulting in high gross profit margins. However, there are significant differences between products, and the company’s overall gross profit margin is affected by product structure.

Gross profit margins stabilize, driving internal and external cost reduction and efficiency improvement. Profitability is influenced by sales structure, localization, and product pricing by demand parties. The company’s gross profit margin declined from 2022 to 2023, but began to recover year-on-year from the second quarter of 2024. With the optimization of the company’s supply chain management, strengthening lean manufacturing and digital management levels, the company is expected to further reduce costs and improve efficiency.

Relying on a high-quality R&D team to build core technological advantages and continuously strengthen innovation capabilities. In 2023, 2024, and the first half of 2025, the company’s R&D expense ratios were 18.59%, 22.61%, and 16.35%, respectively. By the end of 2024, technical personnel accounted for 57.08% of the total workforce, with 40 patents and 175 software copyrights. The company has received honors and qualifications such as the national-level specialized and innovative “Little Giant” enterprise, national high-tech enterprise, Sichuan provincial enterprise technology center, Chengdu enterprise technology center, and ranked among the top 100 new economy enterprises in Sichuan Province in 2024. To maintain the continuity of technological innovation, the company will continue to increase R&D and technology investment, strengthen existing core product advantages, and actively develop new core technologies to enhance market competitiveness.

2. Midstream Profit Margins Expected to Recover, Flexible Private Mechanisms Seize Incremental Markets

2.1 Five Major Application Scenarios, Eight Major Functions, One-Stop Solutions

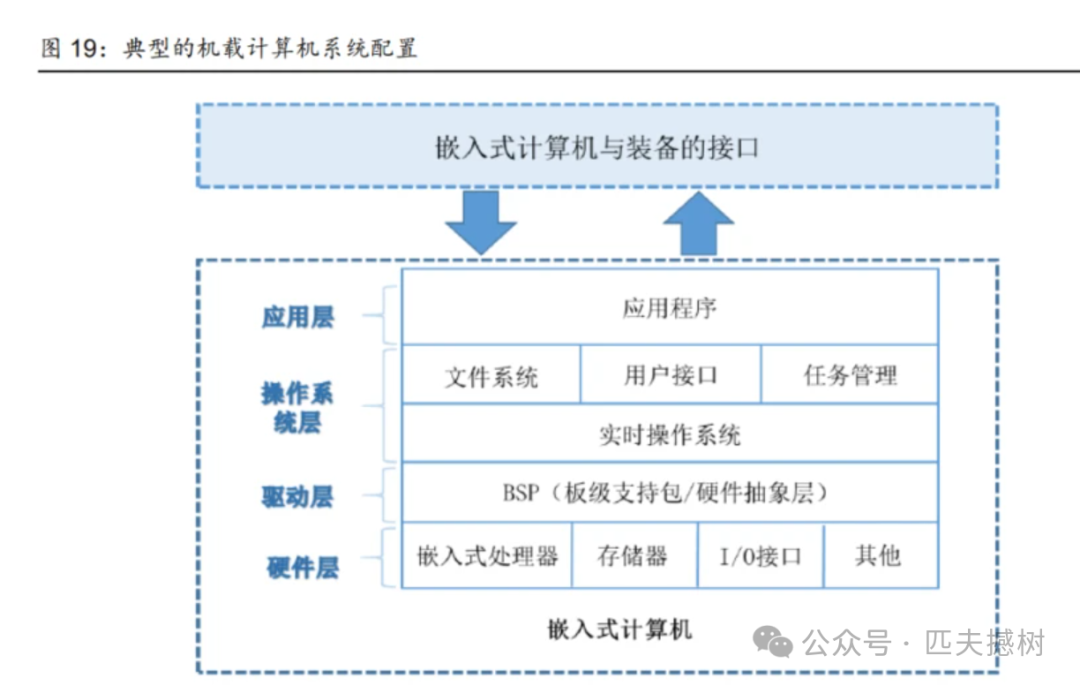

Combining software and hardware, with rich application scenarios. Embedded computer modules mainly consist of embedded software and hardware that supports embedded software, where embedded software includes drivers, application software, and operating systems. The company focuses on the research, production, and service of cutting-edge high-reliability embedded computers, with products widely used in aircraft, missiles, satellites, rockets, unmanned systems, and other high-end equipment, serving key electronic systems such as electronic countermeasures, precision guidance, radar, communication, and flight control, providing one-stop solutions for signal acquisition, image perception and intelligent processing, intelligent computing terminals, bus control, edge storage, and intelligent power supply.

Embedded computers can be divided into four layers: hardware layer, driver layer, operating system layer, and application layer. The hardware layer is the foundation of the entire embedded computer, including embedded processors, memory, I/O interfaces, etc., with the embedded processor being the core part of the hardware layer; the driver layer is the low-level software that interacts directly with the hardware layer, providing hardware drivers or low-level support for the operating system and applications, also known as the Board Support Package (BSP). The operating system layer is responsible for the allocation of all software and hardware resources of the embedded computer, task scheduling, control, and coordination, serving as the software platform for users to run applications. Embedded operating systems differ from common operating systems like Windows, as they must be specifically designed and developed for particular industry applications and specific hardware, characterized by being streamlined, real-time, and reliable; the application layer refers to the software programs that perform specific application functions.

The development of military embedded computers has become an inevitable path and major trend in the defense industry of various countries. The level of informationization of weaponry and equipment is one of the main indicators of battlefield power comparison, and embedded computers, as the intelligent core of weaponry and equipment, hold an irreplaceable position in the intelligence of weaponry and equipment. In 1965, China established a dedicated research institute, the “Chinese Academy of Sciences 156 Project Office,” to support the “Two Bombs, One Satellite” project, which is the predecessor of the Seventh Research Institute of the China Aerospace Science and Technology Corporation, marking the beginning of military embedded computer development. Currently, military embedded computers are experiencing unprecedented rapid development.

2.2 Upstream Cost Reduction, Downstream Demand Prosperity, Midstream Profit Margins Expected to Recover

Compared to weapon system products, the company’s products are typically referred to as modules or components, positioned in the midstream of the industry chain. The company’s products are usually embedded within weapon systems, becoming part of their systems, which may consist of multiple embedded computer modules.

The upstream electronic components are mature and supply is stable, with the localization of integrated circuit chips rapidly increasing. The company’s upstream mainly consists of electronic components, integrated circuits, and other hardware devices, as well as the system software industry. The main raw materials procured include integrated circuits, capacitors, connectors, resistors, structural parts, PCBs, and crystal oscillators. Among these, domestic passive components (capacitors, resistors, etc.) have matured, with stable quality and sufficient supply, and overall prices are on a downward trend. Integrated circuits account for over 50% of the total raw material procurement. In recent years, with the rapid development of domestic integrated circuit technology and changes in international trade conditions, domestic manufacturers have rapidly developed, expanding production capacity significantly, and the localization rate of integrated circuit chips has rapidly increased.

The downstream mainly consists of military research institutes, with a high degree of product customization. Once standardized, products will enter mass production and procurement. The company’s products are mainly supporting products for model weapons, typically positioned in the third and fourth tiers of the weapon production industry chain. The direct downstream customers are state-owned military research and production units, with the end user group being the Chinese military. As the mechanization, informationization, and intelligence of military products continue to improve, the demand for embedded computers will also continue to grow.

2.3 Competitive Landscape: Private Enterprises Break Through Under Qualification Barriers

Embedded computer manufacturers include military research institutes and a few private enterprises. In the past, units engaged in military embedded computer research and production were mainly concentrated in a few state-owned military production enterprises and military research institutes under various military groups. With the gradual opening of key areas by the state, some private companies have gradually been included in the ranks of qualified suppliers for key area products. However, due to the need for relevant qualifications to participate in the defense industry, it is difficult for new entrants to rapidly expand on a large scale, which ensures the core competitiveness of mature enterprises in the industry.

As one of the few qualified high-quality private enterprises, the company has established long-term stable cooperative relationships with clients. Compared to state-owned military enterprises, the company has certain advantages in flexible production mechanisms, effective incentive measures, and rapid response; compared to other private enterprises, it has its own strengths, forming differentiated competition, participating multiple times in the research and production of supporting weapons for national key model projects, and gaining recognition from clients in various fields, achieving a certain level of brand awareness in the industry.

3. Downstream Applications Diversifying, Market Space Expanding

3.1 Airborne: New Aircraft Iteration, Single Aircraft Value Increases

Embedded computers are widely used in aircraft. The airborne computer system refers to the totality of computers and their supporting hardware and software in an aircraft, mostly using embedded computers. Airborne computers include navigation computers, fire control computers, atmospheric data computers, flight control computers, flight management computers, radar data computers, display control computers, communication computers, non-avionics monitoring processors, and general integrated processors. Currently, advanced combat aircraft both domestically and internationally widely use airborne computers, with some aircraft equipped with over a hundred airborne computers, such as the U.S. B-2 bomber, which is equipped with more than 200 airborne computers.

China’s military aircraft still have significant demand for quantity and upgrades. In terms of quantity, according to the “World Air Forces 2025” statistics, as of 2024, the total number of active military aircraft in the U.S. is 13,043, accounting for 25% of the global active military aircraft, ranking first in the world. China’s total number of active military aircraft is 3,309, accounting for 6%, ranking third globally, but still significantly behind the U.S. Among these, China has over 1,583 fighter jets, while the U.S. has 2,679 fighter jets. Currently, China’s military aircraft are in a critical period of upgrading, with most existing old models about to be retired, and new-generation models gradually becoming the main force. In the future, there will also be significant increases and upgrades needed for transport aircraft, bombers, early warning aircraft, and drones.

The increase in informationization will drive the increase in single aircraft value. Since the last century, mainstream air forces around the world have begun to replace some fighter jets with new cockpits and avionics equipment, significantly improving combat capabilities and extending service life through improvements in core computing systems and other aspects. According to the “China Aviation News,” in recent years, the proportion of avionics systems in the factory cost of aircraft has risen sharply, with R&D costs for avionics systems accounting for 30%-40% of the total cost of advanced combat aircraft development, and this trend continues to expand. As high-tech military aircraft achieve various advanced functions, the demand for embedded computers per aircraft will significantly increase compared to traditional aircraft, and the airborne embedded computer market will have substantial market space as military aircraft informationization continues to improve.

3.2 Missile-Borne: Increased Penetration of Precision Guidance, Consumable Attributes Drive Restocking Demand

The demand for missiles is gradually opening up, and total production will further increase. Precision guidance plays an increasingly important role in modern warfare. As China’s defense policy gradually shifts to a proactive defense policy, the requirements for new missile installations and various performance specifications will further increase, and existing missiles will gradually be replaced according to new performance requirements. Missile-borne computers, as the overall control module for guided weapons such as missiles, have a significant impact on the strike effectiveness of guided weapons. For traditional missiles, the missile includes two task processing systems: the navigation computer and the flight control computer. The main task of the navigation computer is to receive and calculate the motion information of the missile body, generate guidance instructions according to the guidance law and predetermined trajectory, and transmit the guidance instructions to the flight control computer. The main task of the flight control computer is to control the missile body to fly along the predetermined trajectory based on the guidance instructions generated by the navigation computer and accurately hit the target.

With the expansion and upgrade of missile quantities, the missile-borne embedded computer market is experiencing year-on-year growth. The guidance system accounts for about 50% of the total cost of missiles, with the proportion of precision-guided munitions exceeding 70%. Embedded computers are the main components of devices such as radio control, automatic radar, and radio fuses. In the future, as low-cost advanced precision-guided main battle equipment enters a period of accelerated release, the missile-borne embedded computer market will enter a phase of rapid growth.

3.3 Satellite-Borne: Satellite Networking Trend, Satellite-Borne Computing Power Multiplies

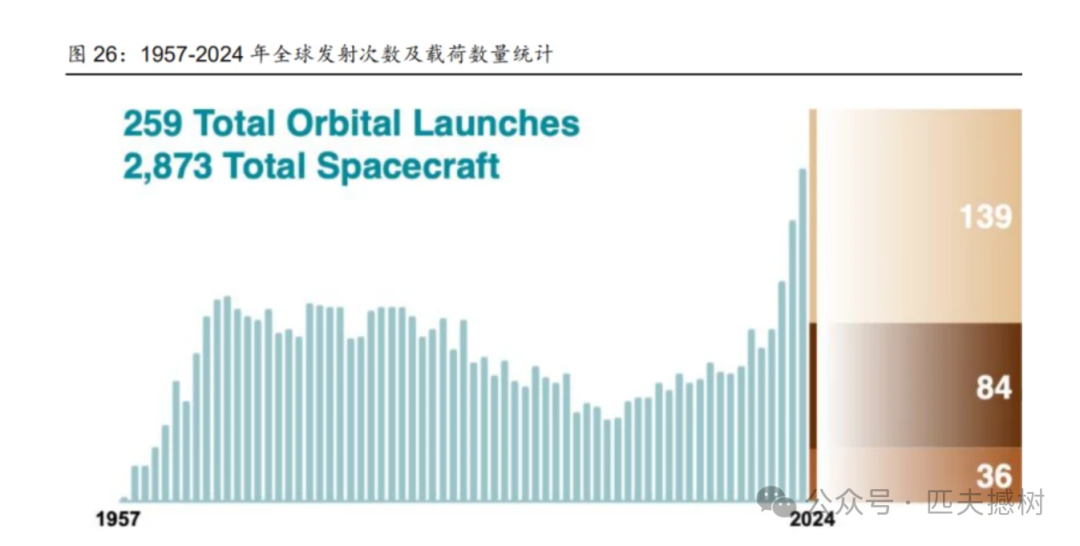

In the past five years, the number of commercial satellites launched into orbit by major countries worldwide has reached new highs every year. According to data from the Satellite Industry Association (SIA), the global deployment volume in 2024 is expected to be 2,781 satellites, a year-on-year increase of 20%, which is seven times that of 1999, with a total of 11,700 active satellites in orbit, a year-on-year increase of 20.73%, which is 4-5 times that of 2019. In 2024, China is expected to launch 201 satellites, with 687 satellites in orbit, ranking second in the world. Additionally, according to astronomer Jonathan McDowell’s analysis, the U.S. SpaceX Starlink program plans to launch a total of 47,000 satellites in two generations of satellite systems, Gen1 and Gen2A, with 7,523 satellites launched by the end of December 2024; China also has three plans for large low-orbit satellite constellations, namely Qianfan (G60), State Grid (GW), and Honghu No. 3, with planned launches exceeding 15,000, 12,000, and 10,000 satellites, respectively.

The 7-year rule forces satellite constellations to seize orbits, and the satellite industry chain is expected to accelerate. To prevent excessive occupation and hoarding of orbital resources, the International Telecommunication Union (ITU) added new rules for satellite constellation operators in 2019, specifying that after submitting satellite network information to the ITU, there is a 7-year validity period for the rules, requiring deployment of 10% of the total number of satellites within 2 years, 50% within 5 years, and 100% by the end of the 7-year period, or the submitted network information will be scaled down accordingly. In the next 3-5 years, global satellite and rocket development and launch, as well as supporting ground equipment development, are expected to see significant growth.

In the total manufacturing cost of satellites, the cost of satellite-borne computers accounts for about 10%. Embedded computers are mainly used in launch vehicles, satellite communication ground stations, and related components needed for low-orbit satellite payloads, such as comprehensive control of launch vehicle engines, satellite communication, sensors, remote control, and telemetry. With years of technical accumulation and a strict quality control system, the company has entered the satellite-borne field, currently providing high-performance computing modules and management control modules mainly for low-orbit satellites.

3.4 Unmanned Equipment Reshaping the Battlefield, Low-Altitude Economy Market Space is Vast

Battlefield demand is driving the development of unmanned equipment, reshaping the battlefield. In the context of the evolving global military landscape, unmanned equipment has become an indispensable strategic force in modern warfare. According to Trend Force’s forecast, the global military drone market size is expected to grow from $16.5 billion in 2022 to $34.3 billion in 2025, with a compound annual growth rate of 27.6%. Unmanned ground vehicles, unmanned underwater vehicles, and surface unmanned boats are also showing rapid growth. Meanwhile, the latest report from the U.S. Congress shows that the U.S. Air Force has 7,494 drones, and when including the Army, Navy, and other military branches, the total number exceeds 11,000; in China, according to the “Chengdu Zhimingda Co., Ltd. 2025 Simplified Program for Issuing Stocks to Specific Objects,” the estimated number of medium and large drones equipped by the Chinese military is about 3,000-3,500. The gap in drone equipment numbers between China and the U.S. is significant, and China is in the process of leapfrogging equipment development during the 14th Five-Year Plan, with rapid increases expected in the procurement scale of drones in key national areas in the coming years.

As an important track for strategic emerging industries, the low-altitude economy is thriving. In terms of civilian applications for drones, China has introduced several strategic plans and policies related to the manufacturing of drones and other aviation equipment in recent years, clearly stating that aircraft manufacturing is a national strategic high-tech industry with significant strategic importance in the national economy and defense capabilities, and providing comprehensive support for the development of the unmanned equipment industry from development strategies, industry legislation, industrial policies, and financial investments.

Embedded computers play a crucial role in the flight control of drones. The realization of functions such as positioning and tracking, real-time monitoring, and information transmission in unmanned systems relies heavily on computer systems for technical support in intelligent recognition, graphical analysis, and data computation.

3.5 Plans to Raise 213 Million Yuan to Seize Opportunities in Commercial Aerospace and Unmanned Equipment

On July 1, 2025, the company announced plans to raise 213 million yuan through a targeted stock issuance to implement the “Research and Industrialization Project for Embedded Computers in Unmanned Equipment and Commercial Aerospace” and to supplement working capital, aiming to invest in equipment to meet the future needs of advanced equipment in key national areas. Once the project is completed and reaches production capacity, it will further enhance the company’s industrialization and mass production capabilities for embedded computers used in key national areas, helping the company quickly seize market share.

In the future, the company will also: ① continue to increase R&D investment, adopting more advanced low-power, high-performance multi-core and multi-processor systems, as well as high-performance data exchange technologies, along with AI intelligent processing and AI signal processing technologies, combined with the company’s years of accumulated high-reliability and high-performance software components, to design higher-performance embedded computer systems while continuously developing new platforms and technologies to optimize product performance; ② leverage the company’s comprehensive capabilities in technology, quality, and service assurance to strengthen customer cooperation, enhance horizontal cooperation among different customers and different subsystem systems for key models, explore customer potential, expand project participation and product variety, and increase the company’s market share.