[Market Analysis]

The Federal Reserve lowered interest rates by 25 basis points as expected, but there were significant contradictions between its statement, economic forecasts, and Chairman Powell’s remarks, leading to sharp market fluctuations. The US stock market plummeted after the announcement, although it later rebounded, indicating that the market was “not satisfied” with the outcome. The next day, the A-share market opened with more declines than gains, giving a sense of a “shoe dropping,” but subsequently, the three major indices turned positive again, indicating that the A-share market remains strong. The current market has shifted from a broad rise to a localized increase, making it increasingly difficult to achieve passive gains; it is still necessary to select quality targets patiently based on rotation direction!

Observations from Bull and BearFrom the global demand for analog chips, it appears that the market for analog chips has basically bottomed out and is recovering. In the first half of 2025, the largest global analog chip manufacturer, TI, is expected to generate $8.5 billion in revenue, a year-on-year increase of 13.8%, showing a significant improvement compared to the negative growth rates of -12.5% and 10.7% for 2023 and 2024, respectively. The application scenarios for domestic AI chips are continuously expanding, and domestically produced AI chips have a first-mover advantage among leading internet companies. From the perspective of AI technology development, large AI models are the downstream application area with the highest demand for AI computing power, and leading internet companies are investing heavily in this field. Therefore, domestically produced AI chip products recognized by leading internet companies and undergoing large-scale procurement have a first-mover advantage in commercialization.

The three major indices opened lower collectively, with over a thousand stocks in the red at the market open. In terms of sectors, automotive services, home appliance components, and wind power equipment performed strongly, while rare metals, industrial metals, and diversified finance lagged. Chip stocks continued to be strong, with over ten stocks such as Liyang Chip and Huicheng Co., Ltd. rising over 10%. Wantong Development and Rockchip also followed suit, and CCTV reported on the construction achievements of China Unicom’s Sanjiangyuan Green Power Intelligent Computing Center project. Among them, the domestic computing power segment involves multiple brands such as Alibaba’s Pingtouge (Wanka), Muxi Co., Ltd., Birun Technology, Zhonghao Xinying, Suiruan Technology, and Moore Threads, which have signed or are planning to sign contracts.

Robot concept stocks continued to be strong, with Jiesheng Electronics and Jingxing Paper both achieving three consecutive boards. Lihengxing and Kesen Technology also followed suit. Elon Musk announced plans to conduct a technical review of Tesla’s AI5 chip design this Saturday and hold a meeting related to robots next week. The intelligent driving concept fluctuated and rose, with Dezhong Automobile hitting a 30cm limit. Previously, Kebo Da achieved three consecutive boards, and multiple stocks such as China Automotive and Guangyang Co., Ltd. hit their limits. On September 17, 2025, the draft for public consultation on the “Safety Requirements for L2 National Standards for Intelligent Connected Vehicle Combination Driving Assistance Systems” will be officially released, with the policy expected to be fully implemented on January 1, 2027.

Tourism and hotel concept stocks saw unusual rises, with Yunnan Tourism achieving two consecutive boards and Huatian Hotel hitting the limit, while Qujiang Cultural Tourism and Caesar Travel also followed suit, announcing several policy measures to expand service consumption. Additionally, with the “Eleventh” holiday approaching, the tourism market’s heat continues to rise. The wind power sector remains strong, with Dajin Heavy Industry hitting the limit and Tongyu Heavy Industry rising over 10%, while Yunda Co., Ltd. and Haili Wind Power also followed suit. As the wind power industry begins to reverse the internal competition in the second half of 2024, 12 complete machine companies signed a self-discipline agreement in October, and the bidding price for wind turbines is expected to rise starting in the fourth quarter. From January to July this year, the average bidding price for domestic onshore wind power units increased by over 9% compared to the full year of 2024, reaching 1552 yuan/kW.

Market Overview:

Growth Enterprise Market:

[Market Forecast]

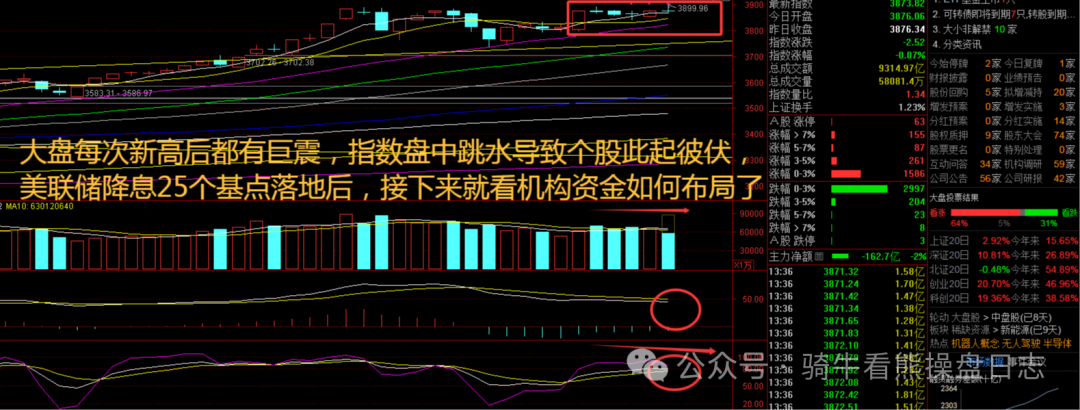

The Shanghai Composite Index reached a new high on Thursday after the overnight Fed rate cut, indicating that the index is bound to break through 3900 points. However, whether it can stand above the significant threshold of 4000 points will depend on the subsequent investment atmosphere.Looking ahead, due to excessively weak employment data, we expect the Fed may cut rates again in October, but after that, rising inflation will make the threshold for rate cuts increasingly high, and the space for monetary easing will also be limited. The current issue with the US economy is not insufficient demand, but rising costs.Next, pay attention to whether the Shanghai Composite Index can stabilize above 3900 points.

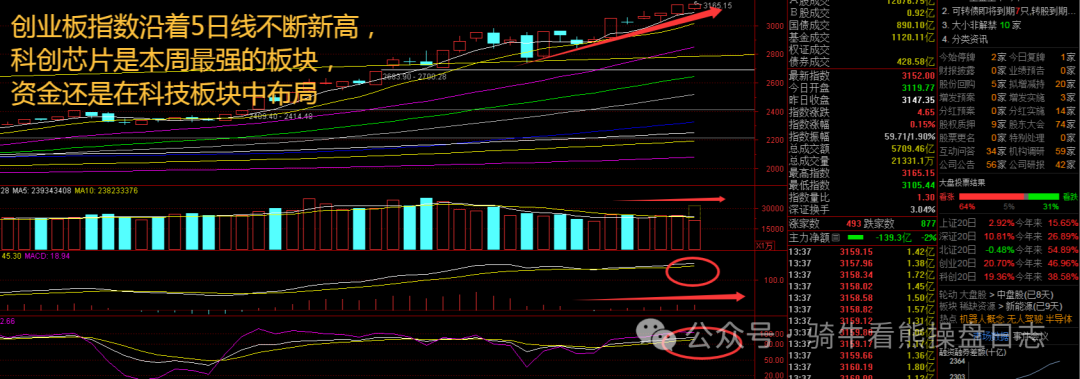

The Growth Enterprise Market Index opened low and rose, continuing to climb above the 5-day line, showing a clear strong upward phase. However, it will be difficult to hold individual stocks for passive gains, and caution is needed for the situation where the index rises while individual stocks fall.The Fed’s September rate cut of 25 basis points met market expectations. The Fed responded well to market concerns but also maintained restraint. The previously anticipated 50 basis point cut did not occur, and there are significant differences among decision-makers regarding the next rate cut. Excessive monetary easing may not only fail to solve employment issues but could also exacerbate inflation, leading the economy into a “stagflation” dilemma.Next, pay attention to whether the Growth Enterprise Market Index can stabilize above 3150 points.

[Gold Mining Plan]

Since September, several fresh data have confirmed foreign capital’s investment enthusiasm for the Chinese market. Data released by global fund flow monitoring agency EPFR shows that actively allocated foreign capital has seen net inflows into the Chinese market for several consecutive weeks. A report from the International Institute of Finance (IIF) indicates that in August, foreign investors invested nearly $45 billion in emerging market stocks and bonds, the highest scale in nearly a year, with the funds flowing into the Chinese market accounting for a major portion. Meanwhile, international investment banks such as Morgan Stanley and UBS have observed that overseas investors’ interest in Chinese assets has reached a recent high. According to international investment banks, factors such as China’s economic recovery, policy support, and continuous innovation and profit improvement of Chinese enterprises have collectively enhanced foreign capital’s willingness to invest.

The automotive services, semiconductor, and IT equipment sectors are the main participants in net capital inflows, while sectors such as feed, film distribution, and diversified finance have seen relatively large net outflows.Observations from Bull and BearAt the “AI Chip Architecture Innovation Forum,” companies in the RISC-V ecosystem such as ESWIN, Andes, and Nuclei showcased their strategic layouts and industrialization progress in the AI computing field. ESWIN proposed a product innovation path centered on “RISC-V + DSC (Domain-Specific Hardware) + AI,” having achieved mass production of 12nm RISC-V SoCs and launched a new generation of solutions aimed at 6nm processes, focusing on video processing, GPU/DSA integration, and multi-form hardware modules (including SBCs, edge computing boxes, and accelerator cards) to demonstrate the significant advantages of RISC-V in high-performance AI acceleration and flexible customization.

The world’s second-largest analog chip manufacturer, ADI, reported a revenue of $6.18 billion for the first three quarters as of the end of July 2025, a year-on-year increase of 13.7%, with growth rates significantly rebounding compared to 2.4% and -23.4% for 2023 and 2024, respectively. Taking the domestic power management and signal analog chip industry as an example, the industry involves 28 listed companies, with a total revenue of 18.28 billion yuan in the first half of 2025, a year-on-year increase of 21.1%, showing a clear acceleration trend compared to the growth rates of 0.9% and 17.4% for 2023 and 2024, respectively. According to the growth reasons disclosed in the semi-annual reports of listed companies, the basic reason is that the industry inventory digestion has basically ended, and downstream demand has begun to recover, with the most significant improvements seen in automotive and industrial demand.

Under the dual impact of declining demand and prices, the proportion of TI’s revenue from the Chinese market has decreased from over 40% to about 20%. However, with the digestion of downstream inventory, analog chips are gradually entering a price increase cycle this year. For example, in June, August, and September, there have been continuous reports of TI chip price increases in the domestic market. In June, it was reported that TI planned to raise prices for about 3,300 models by 5%–35%, while in September, it was reported that it planned to raise prices for about 66,000 models in the domestic market, accounting for about 80% of TI’s available models, with even larger increases of about 10%–25%. It is evident that analog chips are likely entering a dual recovery phase of demand restoration and price rebound.

Domestic AI chips are continuously improving in performance, and the coverage of downstream scenarios is expanding, thereby driving steady revenue growth for related companies. Currently, the global AI wave is accelerating, leading to an exponential increase in demand for computing power. At the same time, domestic large models such as DeepSeek are advancing rapidly. Considering geopolitical factors and the stability of the industrial chain, this will inevitably lead to a sustained increase in domestic computing power demand. As the domestic computing power infrastructure is gradually built and AI chip technology continues to improve, there will be ample space for the localization of computing power. We remain optimistic about investment opportunities related to computing power localization.