Follow us for professional semiconductor news with “zero time difference”!

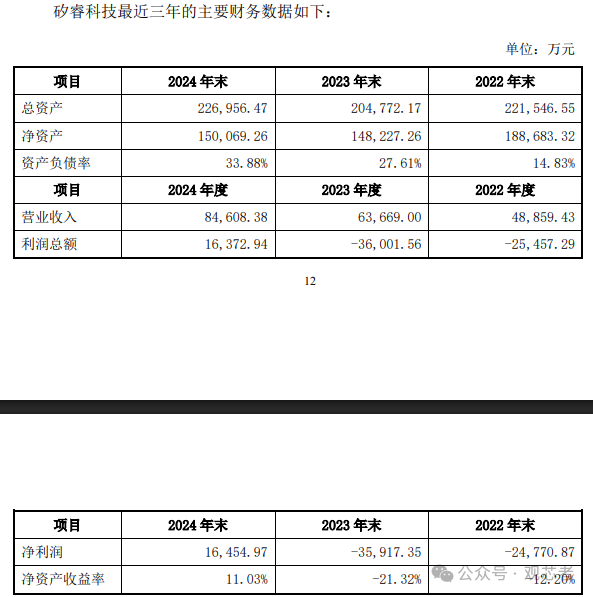

As the “nerve endings” of smart devices perceiving the world, the demand for inertial sensors has surged in recent years across various fields such as consumer electronics, automotive, industrial, and aerospace. Applications like posture sensing in smartphones, motion monitoring in wearable devices, and vehicle positioning in autonomous driving all rely on this core component.The enormous market potential has attracted over 20 domestic companies, including Xindong LianKe, Beimi Sensors, Meixin Semiconductor, and Minxin Co., to flood into the market, creating a vibrant scene of “a hundred flowers blooming”. However, within just a few years, the domestic inertial sensor industry has taken a sharp downturn, experiencing a dramatic polarization akin to “fire and ice”, with an unprecedented restructuring sweeping through the entire industry at a visible speed.Performance Polarization: “Racing” and “Surviving” CoexistThe harsh reality of industry polarization is vividly reflected in corporate performance. The rapid growth of leading company Xindong LianKe starkly contrasts with the “survival crisis” faced by small and medium-sized enterprises.Xindong LianKe’s 2025 semi-annual financial report is impressive: achieving operating revenue of 253 million yuan, a significant year-on-year increase of 84.34%; net profit attributable to shareholders of the listed company reached 154 million yuan, with a staggering year-on-year growth of 173.37%. More crucially, the company’s large annual order of 270 million yuan obtained at the beginning of the year is being delivered steadily as planned, with the order structure primarily focused on high-value-added fields such as industrial and high-end equipment, demonstrating significant risk resistance and sustained strong growth momentum.In contrast, ShenDi Semiconductor, once highly regarded in the MEMS gyroscope field with a valuation of 40 billion yuan and favored by Huawei Hubble, BYD, and Shenzhen Capital Group, is now mired in operational difficulties. As of July 2025, the company has owed employees social security and wages for a year, and the stability of its core team is on the verge of collapse — founder Zou Bo has long left the company. Even with capital intervention pushing for restructuring, the process remains fraught with difficulties due to multiple disputes involving employee debts and supplier arrears, leaving the company’s survival hanging by a thread.Another once-prominent “star enterprise”, Yiboda, is also facing precarious operational conditions. Financial data shows that in 2024, the company achieved revenue of only 1.507 million yuan, while net profit suffered a loss of 18.405 million yuan, with revenue insufficient to cover monthly operating costs; the downturn further intensified in the first half of 2025, with revenue shrinking to 596,100 yuan and net profit loss reaching 5.8306 million yuan. The total assets dropped from 20.6786 million yuan at the end of 2024 to 14.7521 million yuan, and the continuously shrinking assets struggle to support subsequent R&D and production, pushing survival pressure to a critical point.Price Wars “Strangling” Consumer Electronics: Mid- to Low-End Becomes the “Disaster Zone”The predicaments faced by ShenDi Semiconductor and Yiboda are not isolated cases but rather a concentrated outbreak of structural contradictions in the industry. Since 2023, the demand for inertial sensors has reached a “turning point”, with the mid- to low-end market, especially in consumer electronics, becoming the “storm center” of the industry reshuffle.Consumer electronics have long been the “foundation” of MEMS inertial sensor demand — at one point, consumer products accounted for over 85% by quantity. However, as the terminal markets for smartphones and wearable devices entered a phase of “stock competition”, the growth rate of demand has significantly cooled: global smartphone shipments have continued to decline from 2022 to 2024, and shipments of wearable devices are also sluggish, with weak terminal demand directly affecting the upstream sensor sector.Compounding the issue, the previous influx of over 20 domestic companies has led to severe overcapacity in the mid- to low-end inertial sensor market. To compete for limited customer demand, local manufacturers have been forced to engage in a “price war”, resulting in chaotic competition in the mid- to low-end market.Silicon Microelectronics’ operational data exemplifies the impact of the price war in the consumer electronics sector. As one of the earliest companies to enter the MEMS sensor market in China, Silicon Microelectronics holds a 20%-30% share in the consumer accelerometer sensor market, making it a “backbone” of the industry. However, under the pressure of the price war, its MEMS sensor business revenue has declined for two consecutive years: dropping to 286 million yuan in 2023, a year-on-year decrease of 6%; further falling to 250 million yuan in 2024, with the year-on-year decline expanding to 12%.The company explicitly stated in its financial report that “the decline in sensor product revenue is mainly due to the direct impact of falling prices in consumer products” — as the technical threshold for consumer inertial sensors is relatively low, companies can only passively reduce prices to maintain market share, significantly compressing profit margins. Many small and medium-sized enterprises have thus fallen into a vicious cycle of “price reduction to maintain market share — profit decline — insufficient R&D investment — weakened product competitiveness”, facing a dilemma for survival.Minghao Sensor’s fluctuating performance more intuitively reflects the drastic changes in the industry environment. From 2020 to the first half of 2025, it achieved revenues of 85.0351 million yuan, 170 million yuan, 198 million yuan, 253 million yuan, 131 million yuan, and 81.7875 million yuan, respectively; net profits were -50.4085 million yuan, -24.4305 million yuan, 27.8765 million yuan, 21.2621 million yuan, -52.9583 million yuan, and -13.7456 million yuan.On the other hand, Xirui Technology experienced rapid revenue growth from 2022 to 2024, jumping from 489 million yuan to 846 million yuan, but the company reported a net loss of 248 million yuan in 2022; losses further expanded to 359 million yuan in 2023, before successfully turning a profit of 165 million yuan in 2024. It is noteworthy that even with the backing of listed company resources, the survival pressure on small and medium-sized manufacturers has not significantly eased. As a company that has built a complete MEMS chip production system, Jiaxing Najie was acquired by Hanwei Technology in 2024, becoming its controlling subsidiary, gaining capital and resource support. However, from the operational data, the company only achieved operating revenue of 17.9586 million yuan in 2024, with a net profit of 6.0549 million yuan, a relatively small revenue scale, still facing significant competitive pressure in the mid- to low-end market price war, with insufficient growth momentum.High-End Market “High Barriers”: Local Manufacturers Face Greater ChallengesIn contrast to the “chaotic slaughter” in the mid- to low-end market, the high-end inertial sensor market, characterized by high technical barriers, has long been “monopolized” by international giants such as Bosch, ADI, Murata, and TDK — these giants occupy over 80% of the global high-end inertial sensor market share, and local manufacturers seeking breakthroughs must not only cross the technical gap but also face additional pressures from price wars in the automotive industry.In the automotive sector, as autonomous driving technology upgrades to L4 level and above, the requirements for the precision, stability, and reliability of inertial sensors have increased exponentially. For example, L4 autonomous driving requires navigation-grade IMUs (Inertial Measurement Units), with drift rates needing to be controlled within 0.1°/hour, while most domestic manufacturers can currently only produce products with drift rates above 1°/hour, indicating a significant technical gap. Additionally, automotive sensors must pass AEC-Q100 automotive certification, with R&D cycles lasting 3-5 years and substantial upfront investments, posing extremely high barriers for small and medium-sized enterprises.The challenges in the industrial sector are equally daunting. Scenarios such as industrial automation equipment and precision machine tools impose strict requirements on the temperature drift and anti-interference capabilities of inertial sensors. For instance, in industrial environments ranging from -40°C to 125°C, sensor accuracy must remain stable, while local manufacturers’ products still lag behind international giants in performance under extreme conditions. More critically, international giants have established long-term partnerships with industrial equipment manufacturers, making it difficult for local manufacturers to penetrate the supply chain, which requires a lengthy validation period, and it is challenging to shake the existing landscape in the short term.Compounding the situation, since 2024, the automotive industry’s price war has transmitted upstream, with vehicle manufacturers continuously pressing down component procurement costs. Even if local manufacturers break through technical barriers to enter the automotive supply chain, they face the issue of compressed gross margins — a local sensor manufacturer revealed that its automotive-grade MEMS accelerometer products have a gross margin of 25%, only half that of similar products from international giants.Accelerating Restructuring: The Industry Enters a Critical Phase of “Elimination”Currently, the major restructuring of the inertial sensor industry has entered a critical phase of “elimination”: the price war in the mid- to low-end market is rapidly eliminating small and medium-sized enterprises that lack core competitiveness and rely on consumer electronics business; the technical barriers in the high-end market are testing the long-term R&D and breakthrough capabilities of local manufacturers.From an industry trend perspective, in the future, only two types of companies will survive the restructuring: one type is leading companies like Xindong LianKe, which focus on high-end niche markets and possess core technological advantages, building technical barriers through continuous R&D investment to capture high-value orders in industrial, automotive, aerospace, and humanoid robotics sectors; the other type is small and medium-sized enterprises with differentiated competitive capabilities, focusing on specific scenarios (such as medical devices, smart homes, and IoT) and providing customized solutions to avoid the “red sea” of price wars.For the entire industry, this major restructuring is not a “cold winter” but a “necessary path” for industrial upgrading — by eliminating inefficient capacity and promoting resource concentration towards advantageous enterprises, it will accelerate the domestic inertial sensor industry’s transition from “scale expansion” to “quality improvement”, laying the foundation for local manufacturers to break into the high-end market and achieve import substitution. The horn of industry reshuffle has sounded; only by actively seeking change and focusing on innovation can we stand firm in the transformation and promote the high-quality development of the domestic inertial sensor industry.—— END ——

It is noteworthy that even with the backing of listed company resources, the survival pressure on small and medium-sized manufacturers has not significantly eased. As a company that has built a complete MEMS chip production system, Jiaxing Najie was acquired by Hanwei Technology in 2024, becoming its controlling subsidiary, gaining capital and resource support. However, from the operational data, the company only achieved operating revenue of 17.9586 million yuan in 2024, with a net profit of 6.0549 million yuan, a relatively small revenue scale, still facing significant competitive pressure in the mid- to low-end market price war, with insufficient growth momentum.High-End Market “High Barriers”: Local Manufacturers Face Greater ChallengesIn contrast to the “chaotic slaughter” in the mid- to low-end market, the high-end inertial sensor market, characterized by high technical barriers, has long been “monopolized” by international giants such as Bosch, ADI, Murata, and TDK — these giants occupy over 80% of the global high-end inertial sensor market share, and local manufacturers seeking breakthroughs must not only cross the technical gap but also face additional pressures from price wars in the automotive industry.In the automotive sector, as autonomous driving technology upgrades to L4 level and above, the requirements for the precision, stability, and reliability of inertial sensors have increased exponentially. For example, L4 autonomous driving requires navigation-grade IMUs (Inertial Measurement Units), with drift rates needing to be controlled within 0.1°/hour, while most domestic manufacturers can currently only produce products with drift rates above 1°/hour, indicating a significant technical gap. Additionally, automotive sensors must pass AEC-Q100 automotive certification, with R&D cycles lasting 3-5 years and substantial upfront investments, posing extremely high barriers for small and medium-sized enterprises.The challenges in the industrial sector are equally daunting. Scenarios such as industrial automation equipment and precision machine tools impose strict requirements on the temperature drift and anti-interference capabilities of inertial sensors. For instance, in industrial environments ranging from -40°C to 125°C, sensor accuracy must remain stable, while local manufacturers’ products still lag behind international giants in performance under extreme conditions. More critically, international giants have established long-term partnerships with industrial equipment manufacturers, making it difficult for local manufacturers to penetrate the supply chain, which requires a lengthy validation period, and it is challenging to shake the existing landscape in the short term.Compounding the situation, since 2024, the automotive industry’s price war has transmitted upstream, with vehicle manufacturers continuously pressing down component procurement costs. Even if local manufacturers break through technical barriers to enter the automotive supply chain, they face the issue of compressed gross margins — a local sensor manufacturer revealed that its automotive-grade MEMS accelerometer products have a gross margin of 25%, only half that of similar products from international giants.Accelerating Restructuring: The Industry Enters a Critical Phase of “Elimination”Currently, the major restructuring of the inertial sensor industry has entered a critical phase of “elimination”: the price war in the mid- to low-end market is rapidly eliminating small and medium-sized enterprises that lack core competitiveness and rely on consumer electronics business; the technical barriers in the high-end market are testing the long-term R&D and breakthrough capabilities of local manufacturers.From an industry trend perspective, in the future, only two types of companies will survive the restructuring: one type is leading companies like Xindong LianKe, which focus on high-end niche markets and possess core technological advantages, building technical barriers through continuous R&D investment to capture high-value orders in industrial, automotive, aerospace, and humanoid robotics sectors; the other type is small and medium-sized enterprises with differentiated competitive capabilities, focusing on specific scenarios (such as medical devices, smart homes, and IoT) and providing customized solutions to avoid the “red sea” of price wars.For the entire industry, this major restructuring is not a “cold winter” but a “necessary path” for industrial upgrading — by eliminating inefficient capacity and promoting resource concentration towards advantageous enterprises, it will accelerate the domestic inertial sensor industry’s transition from “scale expansion” to “quality improvement”, laying the foundation for local manufacturers to break into the high-end market and achieve import substitution. The horn of industry reshuffle has sounded; only by actively seeking change and focusing on innovation can we stand firm in the transformation and promote the high-quality development of the domestic inertial sensor industry.—— END ——

Recommended Reads:

Revenue Exceeds 1.5 Billion! Huawei and ZTE PCB Suppliers Go Bankrupt

Subsidiary Bankruptcy + Performance Plummeting! Can JinHong Gas’s 61-Year-Old New Leader Save the Day?

65,000 Tons of New Capacity Pressing Down! The Nitrogen Trifluoride Industry Falls into the “More Production, More Decline” Dilemma

Breaking News! The Semiconductor Industry Sees Another “Stampede for Company Seals” Drama

Bankruptcies and Exits Continue! The Third-Generation Semiconductor Industry Winter Has Arrived