Gene: Goodness • Gratitude • Love • DedicationMission: To help every post-MBA/EMBA growVision: To become the most valuable platform for learning sharing and resource integrationPurpose: Mutual benefit, harmony, and happiness

3604 words | 6 minutes readingSource: Chaos Academy

This report includes six major predictions for 2026, a comprehensive overview of the AI Agent ecosystem (understanding the “rivalry” dynamics), exclusive disclosures on the revenue gradients of leading Agent startups, and the deep integration of AI Agents into enterprise workflows, with industry-specific applications accelerating their implementation.

Some trends and cases mentioned in the article are truly eye-opening, showcasing a future full of infinite possibilities. Various forms of startups are attracting investments with cutting-edge and pioneering approaches. We have extracted the essence of these insights for in-depth interpretation:

10x Acceleration Track is Coming!

Manlio Carrelli, CEO of CB Insights, expressed in the preface:

“AI Agents have transformed from experimental products to corporate priorities in just two years. I have seen a tenfold increase in the mentions of Agents during earnings calls since 2023.This speed is unprecedented!”

“What surprises me the most is that AI Agents are climbing the value chain faster than any technology I have ever seen. Our survey conducted in June 2025 showed that 82% of companies plan to apply AI Agents in customer support within the next 12 months.”

This momentum is accelerating!

Among the 1500+ tech segments tracked by CB Insights, five of the top ten by investment transaction volume in 2025 are directly related to AI Agents; in other words, half of the hottest investment topics stem from the concept of “Agents”.

-

At the unicorn level: One in five newly minted unicorns has made Agent technology its core product.

-

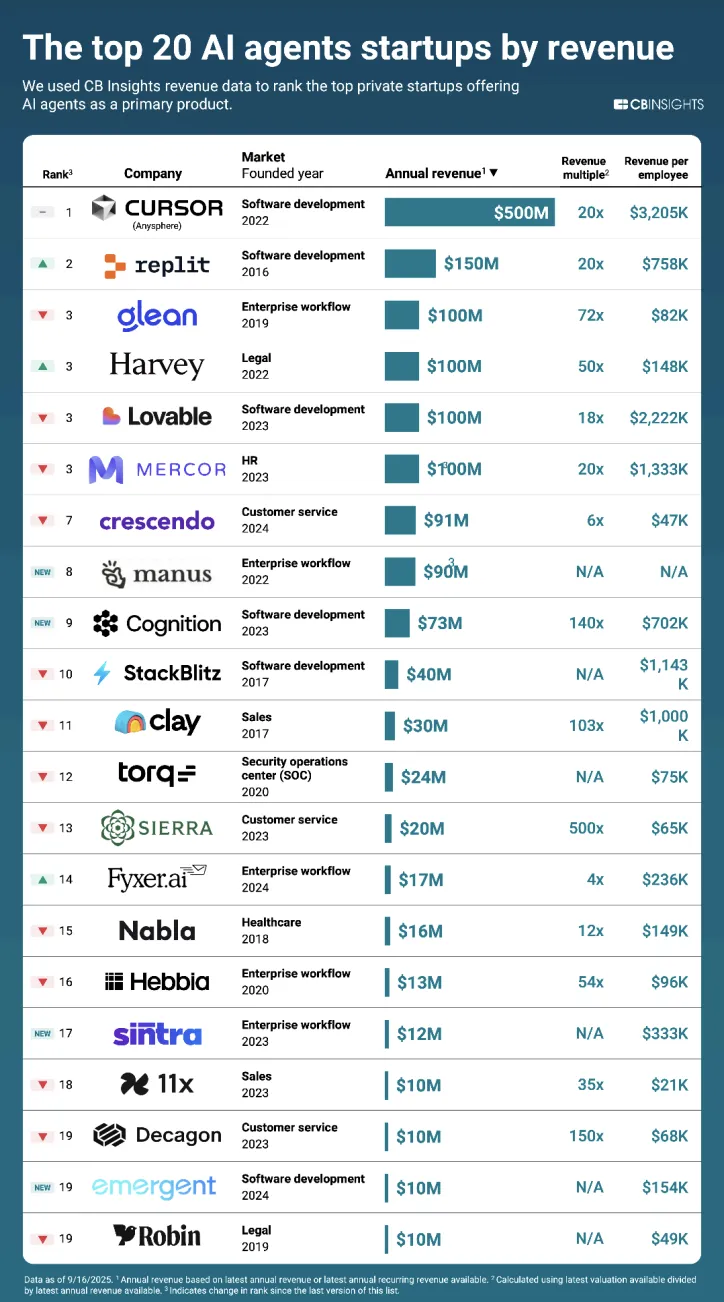

In terms of revenue: Half of the top 20 Agent startups by revenue in 2025 did not exist three years ago, almost “starting from scratch” but quickly breaking into the revenue rankings— including Cursor (revenue of $500 million, founded in 2022), Lovable, and Mercor (both with revenues of $100 million, founded in 2023).

Agents are not only the most lucrative startup track at present but are also simultaneously setting records for the “fastest growth” in both valuation and revenue.

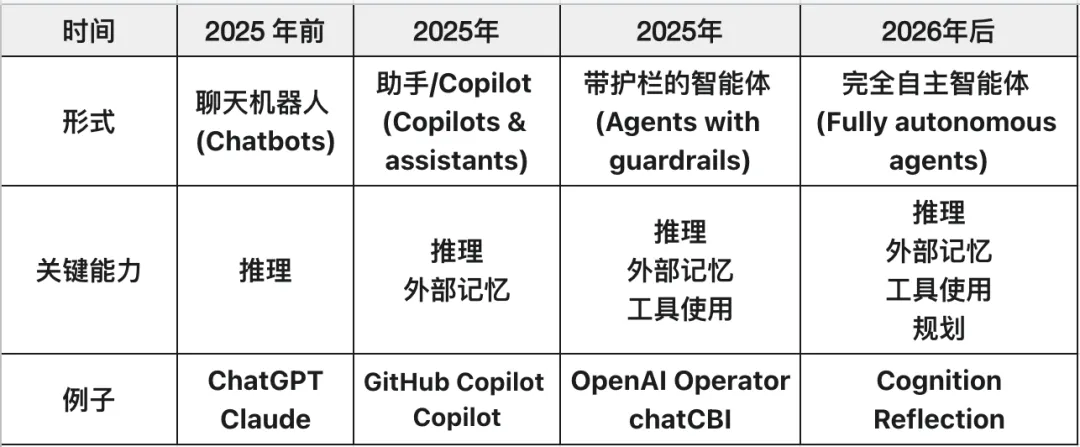

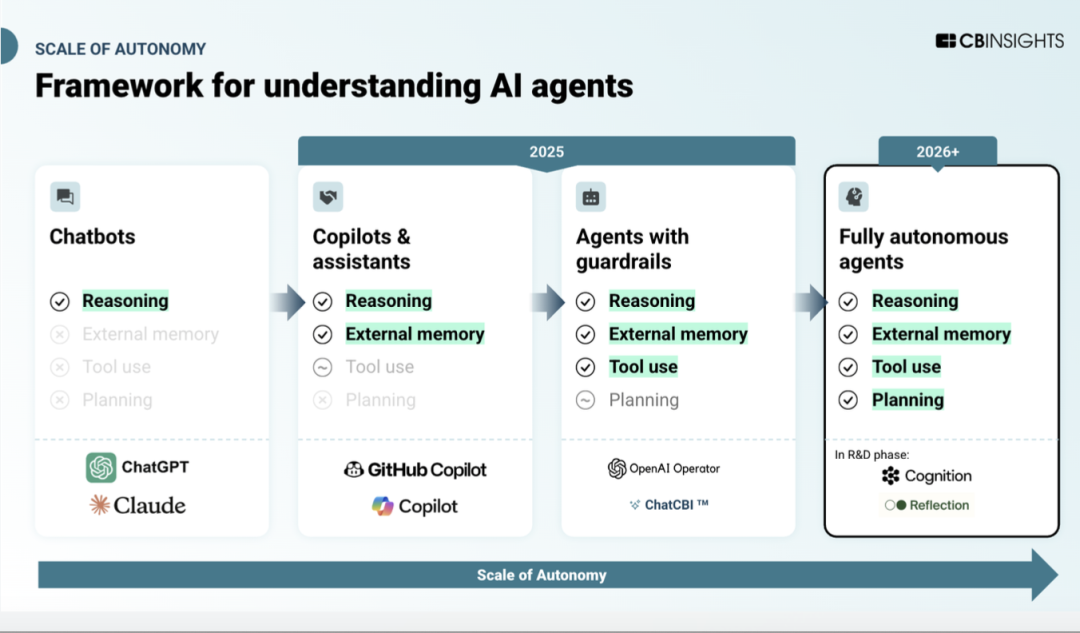

2025: The Inflection Point for AI Agents

2025: Agents with “Guardrails”

AI Agents are systems based on large language models (LLMs) designed to independently represent users in executing tasks through reasoning, planning, utilizing memory, and interacting with external tools and other agents.

Currently, most agents operate in constrained environments, utilizing structured workflows and “guardrails” to achieve specific goals while retaining some decision-making control.

As the capabilities of foundational models improve, agents are expected to become increasingly autonomous.

Post-2025: Fully Autonomous Agents

Agents will operate without human intervention, possessing more complex decision-making, adaptability, and task execution capabilities.

Looking ahead to 2026, pay attention to new forms beyond intelligent co-pilots and chatbot interfaces, which will break the boundaries of “agents”. Early signs in this area include “AI-native” tools—tools and platforms built from the ground up around AI capabilities, rather than adding AI features on top of traditional products.

AI Agents have not yet reached their final form. Today, we are in an “assistant” era, obtaining outputs through AI chat. However, Agents are beginning to transform into something more akin to superpower instruments or tools.

Tools shape the work we do, so an AI super tool will enable our work to go in directions previously thought impossible.

To understand the evolution path of AI Agents, please refer to this autonomy scale diagram.

Six Major Predictions for AI Agents in 2026: Disruption and Reconstruction

CB Insights predicts that by 2026, the following six trends will dominate the development landscape of AI agents:

1. Voice AI Accelerates Rise

The fastest-growing early generative AI companies are concentrated in AI Agent applications, especially in voice AI development. Companies are preparing for a future where humans interact with AI through conversation rather than text interfaces.

For the development of Agentic AI, many companies are preparing for a future where humans interact with AI through dialogue rather than text interfaces. Voice agents will be able to handle complex conversations in areas such as customer service, sales, and IT support, achieving zero human intervention.

Additionally, Meta’s consecutive acquisitions of voice AI startups Play AI and WaveForms AI in 2025 have released strong signals of potential industry consolidation.

2. AI Acquisition Wave Sweeping the Agent Field

AI agent solutions led the top AI exit transactions (Exit refers to a company being acquired or going public) in the first quarter of 2025.

Overall, as of 2025, there have been over 35 acquisitions in the AI agent and Copilot space.

Corporate buyers are increasingly seeking to build comprehensive agent solutions to gain competitive advantages.

3. Profit Pressure Spreads, Non-Programming Fields Also Under Pressure

AI agent startups across various verticals will face the same economic pressures as those in the programming field.

Reasoning models have given rise to the emergence of “Vibe Coding” (granting AI a high-level goal and delegating its multi-step execution process to AI), but this has also increased the number of output tokens by about 20 times, leading to a corresponding rise in computational costs.

In short, the significant increase in computational costs is beginning to erode the profit margins of companies providing AI services.

4. Foundations of Agentic Business Models Solidifying

One of the biggest obstacles to achieving fully autonomous shopping is how to facilitate secure, real-time transactions.

A new wave of startups is directly addressing this challenge by building AI-native payment rails and digital wallets that allow users to authorize and limit AI agents’ spending.

Overall, the AI agent payment infrastructure market is one of the most emerging markets within the entire AI agent technology stack.

For example, payment giant Stripe announced in September 2025 that it would launch an agentic payments API. This $107 billion company collaborated with OpenAI to introduce the Agentic Commerce Protocol.

This protocol aims to provide a standardized communication framework between buyers, AI agents, and businesses, ultimately enabling AI agents to make purchases on behalf of users.

As fintech giants, AI startups, and business platforms focus on the challenge of agentic payments, this early collaboration will shape the future of transactions: secure, autonomous, and occurring within AI interfaces that consumers already trust.

5. “Data Moat Battle” Reshaping Enterprise Software

As the capabilities of AI agents continue to enhance, existing software giants are restricting access to their customer data.

Salesforce’s new rate limits set for the Slack API in 2025, preventing external applications from bulk accessing or long-term storing chat data, is a clear example.

This poses challenges for AI startups (such as knowledge management platforms like Glean) that rely on access to data across multiple systems of record to automate workflows, but it also creates friction for enterprises looking to integrate data into their applications.

This has led to a counter-movement. In September 2025, Snowflake initiated a coalition with over a dozen vendors, including Salesforce, to develop standardized data formats that allow AI to access information across multiple applications.

This tug-of-war will drive enterprises to push for data ownership, increasing market demand for solutions that help them directly own their data infrastructure.

6. Agent Monitoring Tools Become Essential

The reliability of AI agents remains a major challenge in the field. Agents that fail, hallucinate, or behave unpredictably can cause immediate operational issues.

This has driven demand for oversight capabilities aimed at managing agent risks.

Analyzing the seven early transactions (totaling $30.9 million) that have occurred in the AI agent observability, assessment, and governance market so far this year highlights some emerging technological needs:

-

Voice Agent Testing: Cekura ($2.4 million seed round) and Coval ($3.3 million seed round) both focus on voice AI testing and simulation, indicating a need for unique observability approaches for conversational agents.

-

Synthetic User Generation: Several companies (Cekura, Coval, Janus) focus on generating synthetic users for agent testing.

-

AI Productivity Measurement: Larridin secured $17 million in seed funding led by Andreessen Horowitz, demonstrating strong demand from enterprises to quantify the return on investment (ROI) of AI agents, with a focus on measuring the productivity of human-AI collaborative workforces.

Other Exciting Insights

1. AI Agent Revenue Race

Programming AI agents are far ahead in commercialization, with six software development agents entering the top revenue rankings, including market leaders like Cursor (annual recurring revenue of $500 million) and Replit ($150 million). These startups have proven to be the most capital-efficient category, generating an average of $1.4 million in revenue per employee (compared to an average of $594,000 for all top agent categories).

Customer service AI agents have received the highest valuation premiums, with an average revenue multiple of 219 times (compared to an average of 80 times for all top revenue-generating AI agents). This valuation difference reflects investor confidence in the applicability of this field and the expectation that enterprises will quickly replace human support teams with AI agents.

These revenue-leading companies have an average founding age of only 3.8 years. Despite their youth, CB Insights’ business maturity data shows that most are already in the deployment or scaling phase of their products.

Figure: The top 20 Agent startups by revenue in 2025

2. But the Summer of “Vibe Coding” is Over…

The “gold rush” that began in the AI-driven programming field may be evolving into a money-burning bottomless pit, foreshadowing upcoming challenges for other AI agent categories.

Companies like Anysphere (the developer of Cursor) and Lovable, which achieved annual recurring revenue (ARR) exceeding $100 million within months, are now facing the dilemma of LLM reasoning costs increasing by up to 20 times.

This forces them to implement rate limits and price increases, and in some cases, to consider reverse talent acquisition (hiring founders and licensing their technology) as some founders seek exits.

Other AI agent companies (and their supporters) can learn from this.

3. AI Agents Making Progress in Enterprise Workflows

· Software Development Agents Evolving: From Code Assistants to Risk Guardrails

Software development agents are moving beyond programming, incorporating critical “guardrail” functions: startups are transitioning from basic programming assistance to providing testing, quality assurance (QA), code review, and debugging solutions. Over half of the companies are focusing on reducing the risks of “vibe coding” through browser-based testing agents and automated review systems.

· Web Browsing Agents: From General to Specialized

Web browsing agents are moving beyond general scenarios: Y Combinator has incubated over 50% of the existing web browsing agent market, but these startups are differentiating themselves through targeted applications, such as legacy system integration, software testing, and quality assurance. This shift towards specialized browsing agents provides more contextual data access capabilities, improving decision-making and autonomy compared to general alternatives.

· Vertical Agents Targeting Highly Regulated Industries

Highly regulated industries are becoming primary targets for vertical AI agents: in this round of implementation, healthcare and financial services account for 19% of AI agent companies, with 32% of vertical agents actively deploying solutions, and another 45% in emerging/validation stages. Beyond traditional customer service applications, startups are addressing industry-specific workflows such as mortgage processing and medical operations, some of which have begun to handle autonomous research functions that may ultimately replace certain human roles.

↓↓Those who interact will be wiser↓↓

↓↓Click to see will be more blessed↓↓