On September 8, 2025, the Ministry of Industry and Information Technology issued a satellite mobile communication business operating license to China United Network Communications Group Co., Ltd., allowing it to conduct mobile direct satellite connections, emergency communications, maritime communications, and other services. This is not just the issuance of a license, but a key turning point for China’s satellite communication industry as it transitions from the experimental phase to commercial operation. In just over ten days, policies and the market have achieved efficient linkage—on August 27, the “Guiding Opinions on Optimizing Business Access to Promote the Development of the Satellite Communication Industry” was released, and the first license was quickly granted, marking the official entry of low Earth orbit satellite internet into the era of large-scale application.

Against the backdrop of increasingly fierce competition for global frequency resources, China’s strategic positioning in satellite communications has upgraded from a “supplementary means” to a “core infrastructure.” The Ministry of Industry and Information Technology has clearly stated that by 2030, the number of satellite communication users should exceed ten million, and new business models such as mobile direct satellite connections should achieve large-scale application. Behind this goal is not only the high expectations of national top-level design for aerospace informatization but also a comprehensive test of the industry chain from technological breakthroughs to commercial closure.

▍Policy Breakthrough: From State-led to Private Collaboration ▍

The policy breakthrough has brought fundamental changes to the industry. In the past, satellite communications were primarily led by major state projects, but now private enterprises have been systematically included in the industrial ecosystem for the first time. The “Guiding Opinions” explicitly state that “support for private enterprises to participate in satellite communication business” and differentiate licenses into two categories: A13 (mobile communication) and A23 (fixed communication). Currently, only five companies hold the A13 license: China United Network Communications Group Co., Ltd., China Mobile Communications Group Co., Ltd., China Telecom Group Co., Ltd., China Satellite Communications Group Co., Ltd., and China Communications Construction Company. However, the scope of business varies. China Unicom has been approved to conduct mobile direct satellite connections (classified as A13-1 business), which not only broadens its service boundaries but also brings cooperation opportunities for private enterprises. For example, in terminal chips, ground equipment, and other areas, private enterprises have gradually entered the supply chain system.

▍Accelerating Network Deployment: A Turning Point for Low Cost and High Frequency Launches ▍

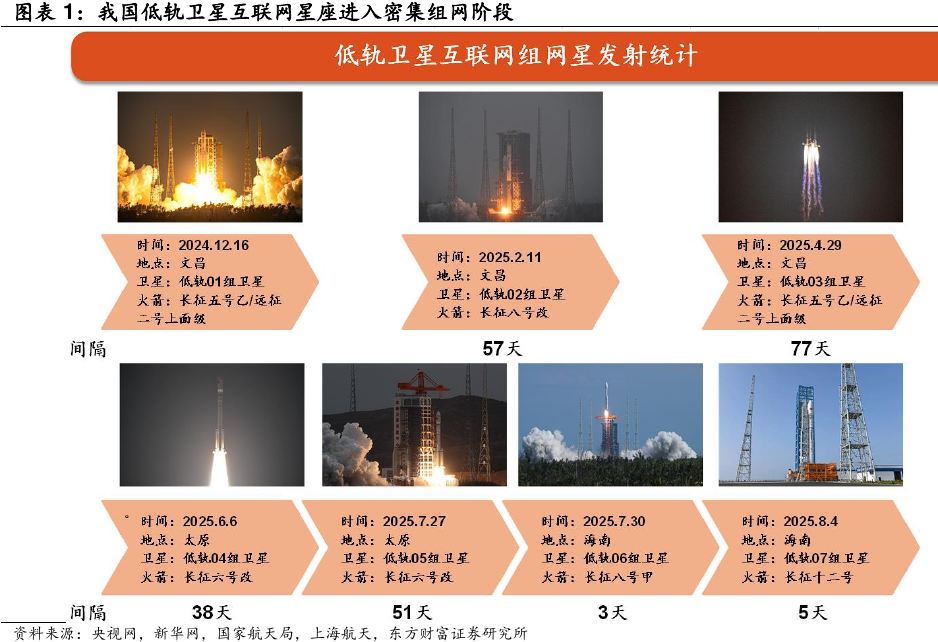

What truly drives the industry towards maturity is the acceleration of network deployment and the continuous reduction of costs. The GW constellation plan coordinated by China Star Network Group aims to launch nearly 13,000 satellites. Since July 2025, the launch frequency has increased from once every 1-2 months to once every 3-5 days, with a total of 72 satellites launched by August. Meanwhile, private aerospace companies have also achieved key breakthroughs in reusable rocket technology. Medium-sized rockets such as Tianbing Technology’s Tianlong-3, Xinghe Power’s Zhishenxing-1, and Blue Arrow Aerospace’s Zhuque-3 plan to achieve their maiden flights within 2025. If the tests are successful, the cost of launching per kilogram is expected to drop from tens of thousands of dollars in traditional models to below $500, which will greatly alleviate the capacity bottleneck in network deployment.

The satellite manufacturing sector is also undergoing a transformation from a “project-based” model to a “production line” model. Companies like Galaxy Space and China Satellite are promoting a 30%-50% reduction in costs for core components such as phased array antennas and baseband chips through standardized designs, with the manufacturing cost per satellite gradually approaching the million yuan level. In the ground terminal sector, manufacturers like Chuangyuan Xinke and Shanghai Hanxun have launched chip products that support 5G NTN (Non-Terrestrial Network), reducing power consumption by 40% while shrinking size, providing the hardware foundation for mobile direct satellite connections.

According to industry chain estimates, the period from 2025 to 2030 will be a critical window for China’s low Earth orbit satellite launches. The two major constellations in China—the GW constellation and the Qianfan constellation—need to complete the launch of over 25,000 satellites, with an average annual deployment of over 3,000 satellites. This scale will drive the development of the entire chain from materials and component manufacturing to rocket launch services.

▍Scenario Reconstruction: From Emergency Communication to Ubiquitous Intelligence ▍

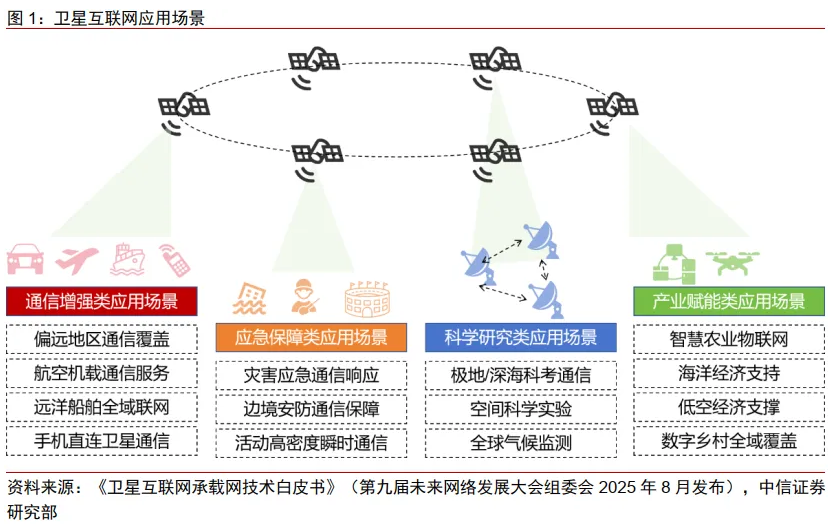

If network deployment is the foundation of satellite internet, then the expansion of application scenarios is the core of commercialization. Currently, three application directions have gradually become clear:

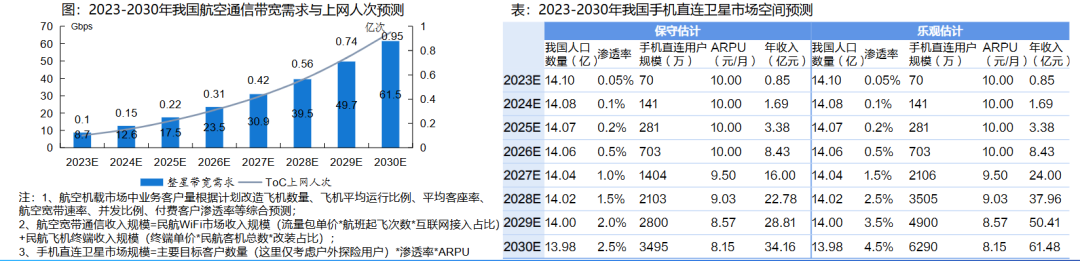

Mobile direct satellite connections are seen as the first market with a user base of ten million. The Ministry of Industry and Information Technology has listed it as a key promotion model, and operators need to collaboratively promote the construction of ground gateway stations, terminal adaptation, and satellite platform scheduling. China Unicom has completed the first round of non-terrestrial network on-orbit tests, achieving a speed of 20 Mbps with a latency of less than 100 milliseconds. Analysts predict that by 2030, the annual revenue scale of mobile direct satellite connections in China is expected to exceed 100 billion yuan, with an ARPU value of 50-100 yuan, reaching 2-3 times that of existing terrestrial communications.

Sources: “White Paper on Innovative Application Scenarios for Satellite Internet Facing Integrated Space and Earth (2024)” (China Mobile), China Telecom official website, United Nations population data, National Bureau of Statistics, Guohai Securities Research Institute

The Internet of Vehicles and low-altitude economy have become important experimental scenarios for space-earth collaboration. In February 2025, China Unicom completed an outdoor test of vehicle-mounted satellite communication based on Geely’s future travel constellation, verifying the full-link capability of “terminal-satellite-platform.” This model can cover existing terrestrial network blind spots in unmanned areas and ocean shipping, solving the problem of 70% of areas not covered by 5G. Governments in Hainan, Chengdu, and other regions have allocated funds to support the construction of satellite super factories and reusable rocket bases.

Satellite IoT is becoming a new solution for wide-area low-frequency connections. For example, in the pastoral areas of Inner Mongolia, satellite IoT can provide real-time feedback on livestock location and temperature data; in the power grid scenario, it can remotely manage substations in remote areas. Compared to traditional IoT, satellite solutions reduce coverage costs by about 60%, making them particularly suitable for applications in sparsely populated areas. China Unicom plans to conduct integrated testing in agriculture and energy sectors based on the Unicom Galaxy 04 satellite to promote the implementation of typical scenarios.

▍Risks and Challenges: Commercialization Must Overcome Three Major Hurdles ▍

Despite the broad prospects, the commercialization of satellite communications still faces multiple challenges.

The pace of license approval affects the depth of participation of private enterprises. Currently, only a few central enterprises hold A13 licenses, and while private enterprises can participate in some segments, there is still no clear timetable for them to enter the market as operators.

Cost control is a prerequisite for large-scale application. Although the costs of rocket launches and satellite manufacturing have been decreasing, they still need to be reduced by more than 50% to support a service system for ten million users. Especially on the terminal side, the RF chips and antenna modules required for mobile direct satellite connections still need to optimize size and power consumption, with a cost threshold of around 100 yuan being the critical point for mass market acceptance.

International competition is also accelerating. SpaceX’s Starlink has covered over 70 countries with more than 3 million users; Amazon’s “Project Kuiper” reached an aviation communication partnership with JetBlue in early September 2025. In contrast, Chinese satellite companies still primarily focus on the domestic market, with room for improvement in global operational capabilities and brand influence.

Sources: “Satellite Industry Status Report” (SIA), “Satellite Communication Technology” (Zhang Hongtai et al.), Guohai Securities Research Institute

From an investment perspective, satellite internet is undergoing a logical transition from “basic investment” to “application explosion.” The period from 2025 to 2027 will be a critical stage for building network capabilities, with rocket launches, satellite manufacturing, and core components benefiting first. However, the commercial realization on the application side will need to wait for the ecosystem to mature, especially after terminal costs decrease and network coverage improves. Investors should focus on companies that truly possess technological breakthrough capabilities, such as hardware manufacturers that can solve antenna miniaturization and low-power chip issues, as well as operators deeply involved in demonstration projects.

This wave of industrial momentum driven by policy, technology, and market not only concerns single-point breakthroughs but also tests ecological collaboration. As the Ministry of Industry and Information Technology stated, the mission of satellite communications is to “support the construction of a strong network nation, a strong aerospace nation, and a digital China.” In the five-year window ahead, the industry chain needs to complete a critical leap from state-led initiatives to civilian popularization, from experimental validation to commercial closure.

Sources: iResearch Consulting, China Business Industry Research Institute, Leqing Think Tank, Chuangyebang, Hualichuangtong Company Announcement, China Satellite Communications Company Official Website, Guohai Securities Research Institute

When the license knocks on the door of commercialization, the true journey of China’s satellite communications has just begun.

-

Summary of Perspectives from Various Institutions

The communication satellite industry exhibits three major characteristics: strong policy drive, rapid technological iteration, and accelerated commercialization. In the short term, focus on the acceleration of satellite network launches (with 2027 as a key node), operational service breakthroughs driven by license issuance, and domestic substitution of core components (such as T/R components and onboard computing modules); in the medium to long term, there is optimism about the application expansion of low Earth orbit satellites in IoT, autonomous driving, and low-altitude economy, as well as global market penetration driven by cost reduction. It is expected that 2025-2026 will usher in an industrial turning point, with companies possessing technological leadership and supply chain integration capabilities benefiting first. The following are the perspectives from various institutions:

AVIC Securities:The satellite communication industry has entered a high-density networking stage, with significant revenue contributions from commercial aerospace; the localization of onboard equipment is accelerating, and demand for military electronics is increasing in military intelligence.

CITIC Securities:The issuance of the satellite mobile communication license to China Unicom by the Ministry of Industry and Information Technology marks a breakthrough in policy access; it is expected that the acceleration of license issuance will lead to a turning point in the industry chain from “manufacturing-launching” to “operation-service,” and it is recommended to focus on satellite manufacturing, launching, and ground equipment segments.

Changjiang Securities:The industry is divided into two phases: the infrastructure investment period (with capital expenditure exploding in 2027) and the application explosion period (with demand for replacement in remote areas); in 2027, the ITU rules will force intensive networking, and reusable rocket technology may reduce costs by 60%-70%. In the medium to long term, pay attention to the potential of low Earth orbit satellites to replace ground base stations.

Guoxin Securities:The “national team + private” hybrid structure (such as the division of labor between Hainan/Shanghai satellite factories) promotes a 35% cost reduction; policy drives the commercialization process, and after the operational license is issued in 2026, a market space for tens of millions of users will open up.

Tianfeng Securities:Demand for onboard active phased array T/R components is significantly increasing, with lightweight and low-cost becoming key technologies; by 2027, the military T/R component market scale may reach 15.8 billion yuan, with cumulative market space in the low Earth orbit satellite field exceeding 100 billion yuan.

Guoxin Securities:Breakthroughs in hollow-core fiber technology have surpassed transmission limits (0.091dB/km), and China Mobile has commercialized cross-border financial links between Shenzhen and Hong Kong, laying the infrastructure foundation for 6G integrated space and earth.

Huaxi Securities:The satellite navigation industry is expected to have a production value of 575.8 billion yuan in 2024 (+7.39%), with rapid penetration of Beidou terminals in transportation and power sectors, driven in the short term by domestic substitution and the integration of “Beidou+” industries.

CITIC Securities:The strategic position of the satellite communication industry is prominent, with clear policy guidance; high-frequency launches are imminent, and the industry turning point is approaching; it is recommended to prioritize attention on the three major operators and leading central and private satellite service providers, as well as investment opportunities in satellite manufacturing, launching, and ground equipment sectors.

Hua Chuang Securities:The military parade highlights the demand for intelligent equipment, and it is recommended to focus on radar, vehicle-mounted communication, and high-precision positioning of Beidou in military scenarios; at the same time, the demand for AI computing power continues to drive the prosperity of underlying technologies such as optical modules.

Guohai Securities:The demand for onboard phased array T/R components in commercial satellites will increase with the construction of low Earth orbit constellations (such as Qianfan and GW constellations), with 2025-2030 being the launch window period, and the cumulative market space expected to exceed 100 billion yuan by 2030.

Xibu Securities:The global satellite networking trend is forcing the industry chain to accelerate, with demand for onboard embedded computing power doubling; the cost share of T/R components and high-performance computing modules in low Earth orbit satellite manufacturing is significant, with clear market increments.

-

Appendix: Related Companies

The content of the above article is referenced from the “Zhizhiu” professional research knowledge base, generated with AI assistance and manually reviewed.