From Philips Heritage to Semiconductor Giant: The Transformation Journey of NXP

From Siemens’ Castoff to Europe’s Chip King: Infineon’s Comeback Logic

From Gaming to AI: How NVIDIA Transformed from a Graphics Card Manufacturer to a Computing Powerhouse in 30 Years

Lessons from TI’s Development Path: How Analog Chip Companies Navigate Cycles for Growth

From Motorola to a Smart Future: ON Semiconductor’s Semiconductor Journey

Origins: The Foundations of the Three Giants (Before the 1990s)

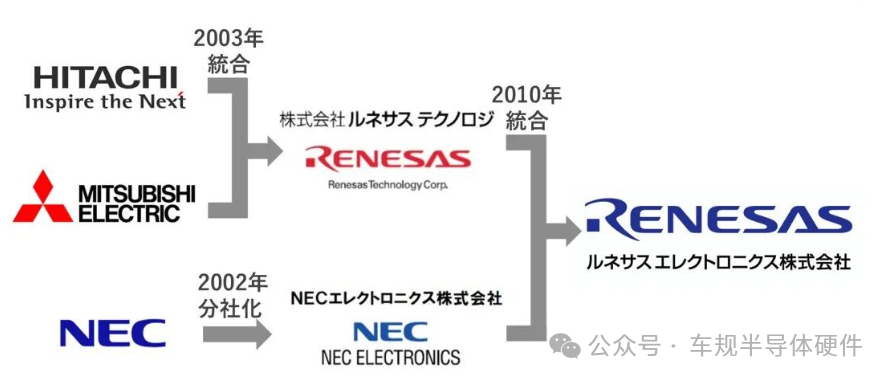

Renesas did not grow organically but was formed through the gradual merger of the semiconductor businesses of Japan’s three major electronics giants—Hitachi, Mitsubishi Electric, and NEC. These three companies have deep accumulations in their respective fields:

-

Hitachi Semiconductor: Strong in MCU, automotive electronics, power semiconductors, and memory (DRAM).

-

Mitsubishi Electric Semiconductor: Specializes in power devices (IGBT, MOSFET), high-reliability MCUs, and RF technology, especially strong in the industrial and automotive markets.

-

NEC Electronics: A global leader in MCUs (especially 16/32-bit products), with outstanding ASIC/SOC design capabilities, widely deployed in consumer electronics, communications, and automotive fields.

Phase One Integration: Hitachi and Mitsubishi Join Forces (2003)

-

Background: In the early 2000s, Hitachi Semiconductor faced fierce competition from Korean and Taiwanese manufacturers, with continuous losses in DRAM and other businesses, necessitating integration to enhance competitiveness.

-

Establishment: On April 1, 2003, the semiconductor businesses of Hitachi and Mitsubishi Electric merged to form Renesas Technology Corporation. It became the world’s third-largest semiconductor company at the time, behind Intel and Samsung Electronics.

-

Equity Structure: Hitachi held 55%, and Mitsubishi Electric held 45%.

-

Objective: To integrate resources and focus on developing MCUs, analog/power devices, and system solutions, aiming to become a leading global semiconductor supplier.

Phase Two Integration: Merging with NEC Electronics, Birth of Renesas Electronics (2010)

-

Background: The global financial crisis (2008-2009) severely impacted the semiconductor industry, prompting Japanese companies to seek further economies of scale.

-

Merger: On April 1, 2010, Renesas Technology (Hitachi + Mitsubishi) officially merged with NEC Electronics Corporation to form Renesas Electronics Corporation.

-

Equity Structure: Hitachi, Mitsubishi Electric, and NEC were the main shareholders, with the introduction of Innovation Network Corporation of Japan (INCJ) (a government-backed industrial fund) for investment.

-

Strategic Significance:

-

Global MCU Dominance: The merger immediately made Renesas the largest microcontroller (MCU) supplier globally, with a significant market share lead.

-

Strengthening Automotive Electronics: Integrated the advantages of the three companies in automotive MCUs, analog chips, and power devices, establishing a leadership position in automotive semiconductors.

-

Expanding Product Line: Covered a complete MCU product matrix from low-end to high-end, along with strong analog, power, and SoC capabilities.

Crises and Restructuring: The Revival Led by INCJ (2012-2016)

-

Severe Challenges:

-

Massive Losses: Due to weak global demand, yen appreciation, low factory utilization, and historical burdens, the company fell into a severe financial crisis (over 100 billion yen loss in 2011-2012).

-

Great East Japan Earthquake (2011): Devastated its main wafer fabs (such as the Naka plant), leading to supply chain disruptions and exposing production concentration risks.

-

INCJ’s Deep Involvement:

-

Closure/Sale of Non-Core Businesses and Plants: Exited unprofitable businesses like TV system chips and mobile basebands; closed or sold redundant wafer fabs (such as Tsuruoka and Kofu plants).

-

Layoffs: Significant global layoffs (about 14,000 people).

-

Production Network Optimization: Implemented a “Fab-lite” strategy, outsourcing some manufacturing to foundries like TSMC while retaining advanced capacity for critical processes (like MCU and power semiconductors) at plants like Naka and Takasaki.

-

Focusing on Core: Fully invested in automotive electronics and industrial/embedded systems, two high-growth, high-profit areas.

-

2012: INCJ led a massive aid package (about 150 billion yen), becoming the controlling shareholder (holding about 70%) and initiating a large-scale restructuring plan.

-

Key Restructuring Measures:

Strategic Transformation: Focusing on Automotive and IoT, Initiating M&A Expansion (2017 to Present)

Under the leadership of CEO Bunsei Kure and his successor Hidetoshi Shibata, Renesas completed its restructuring, significantly improving its financial condition and entering an active expansion phase:

-

Core Strategic Pillars:

-

Automotive Electronics: Providing a full suite of solutions covering body control, powertrains (fuel/electric), chassis safety, cockpit infotainment, and ADAS/autonomous driving, aiming to become the “comprehensive leader in automotive semiconductors.”

-

Industrial/IoT: Offering high-performance, low-power MCUs, MPUs, analog, and connectivity solutions for factory automation, smart homes, infrastructure, and medical devices.

-

General Electronics: Including consumer electronics, communication devices, etc.

-

Key Acquisitions Driving Growth:

-

Acquisition of Intersil (2017, $3.2 billion, equivalent to four times its net profit for the fiscal year ending March 2016, a significant gamble): Significantly enhanced analog and mixed-signal technology capabilities (power management, data converters, interface chips), strengthening automotive and industrial power solutions.

-

Acquisition of IDT (Integrated Device Technology, 2019, $6.7 billion): Gained leading analog mixed-signal product lines (clock generators, data converters, storage interface chips) and wireless connectivity technologies (such as Wi-Fi, Bluetooth, 5G RF components), greatly enhancing its competitiveness in data centers, communication infrastructure, and automotive (sensor interfaces, in-vehicle networks).

-

Acquisition of Dialog Semiconductor (2021, €4.9 billion): Strengthened power management chip (PMIC) technology (especially for mobile devices, IoT, and wearables), gaining Bluetooth Low Energy (BLE), Wi-Fi, and edge computing connectivity and processing technologies, further enriching its IoT product portfolio.

-

Acquisition of GaN device manufacturer Transphorm (2024, ¥2.4 billion): Through this acquisition, Renesas obtained Transphorm’s AFSW wafer fab technology assets located in Aizuwakamatsu, Japan, meaning Renesas will have internal production capabilities for GaN chips, with its gallium nitride products primarily produced at this facility.

-

Internal Integration and Synergy: Deeply integrated the technologies acquired through M&A (especially analog, power management, and connectivity) with its core MCU/MPU platforms to provide “one-stop” system solutions (such as the “successful product portfolio” strategy).

-

Third-Generation Semiconductor Layout: Accelerated development of silicon carbide (SiC) power devices (MOSFETs, diodes) for electric vehicle main drive inverters, charging stations, and industrial power, catching up with competitors like Infineon and STMicroelectronics.

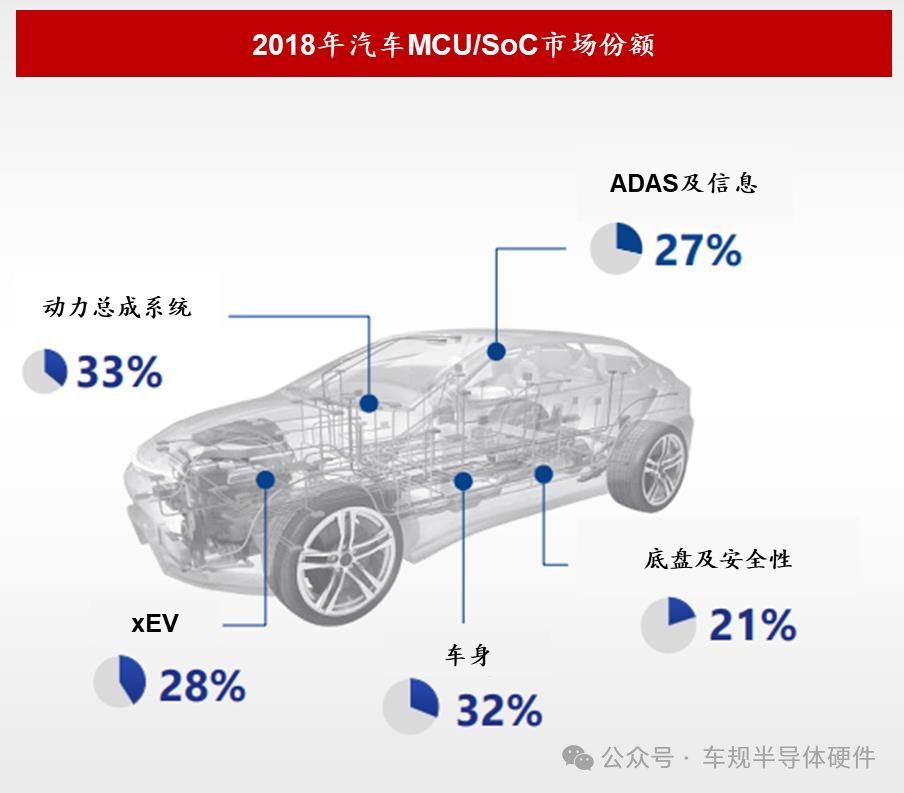

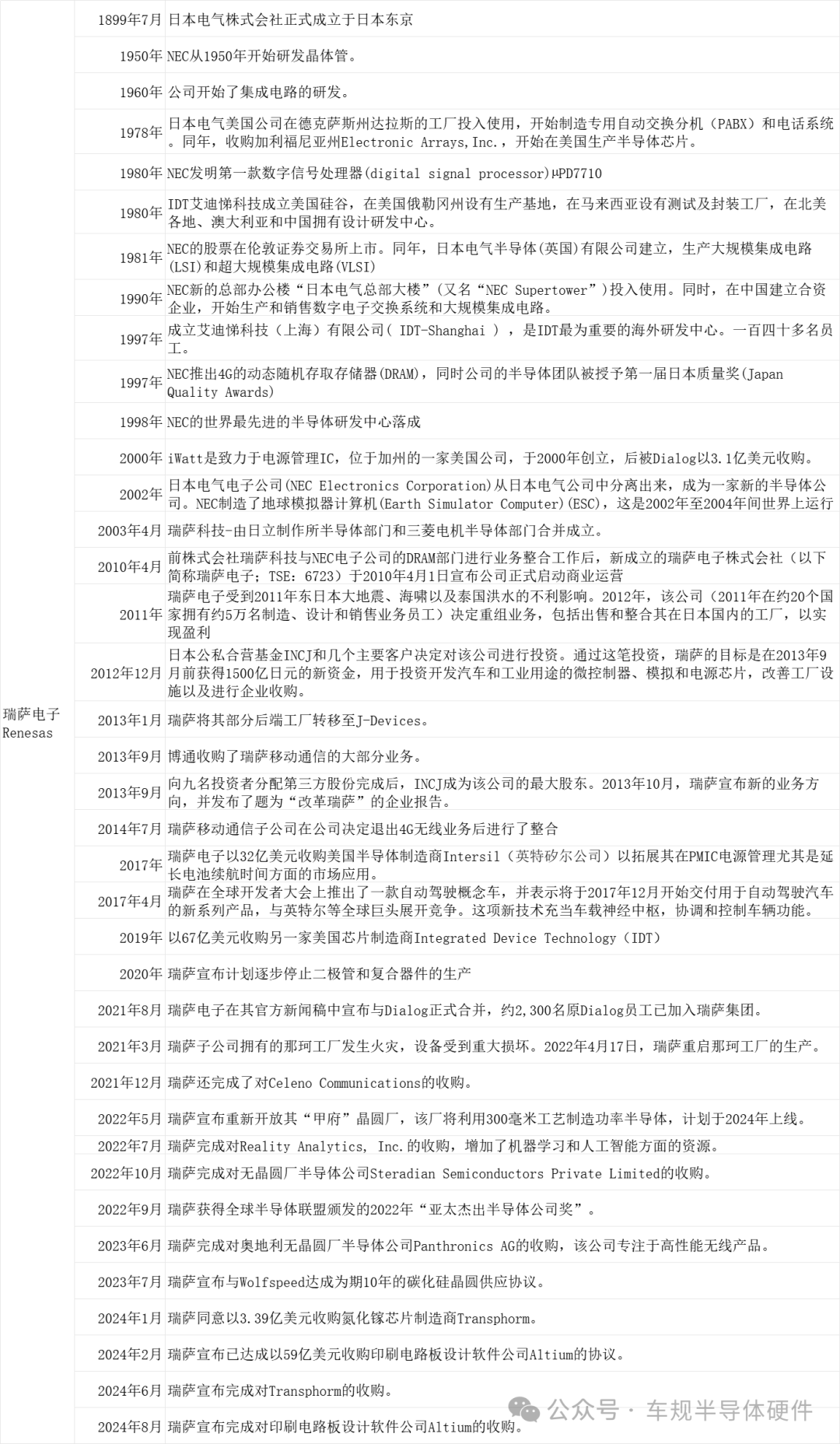

Due to frequent M&A activities, Renesas has spent over a trillion yen in this area in recent years. As of December 2020, the company’s interest-bearing debt reached 717.1 billion yen. Renesas’ main products, microcontrollers and system-on-chip solutions, have achieved leading market shares globally.

In 2019, Renesas held a 31% share of the global microcontroller market, with a 17.2% share in the Chinese market. In 2019, the company had a 6.6% market share in MOSFETs and a 4.8% market share in IGBTs.

In 2018, Renesas’ global market share in automotive microcontrollers/system-on-chip segments

Below is the development history of Renesas Electronics.

Core Advantages and Current Status (2023+)

-

Absolute Leader in Automotive MCUs: Long-term global market share leader (about 30%), with products covering from low-end body control to high-end domain controllers/ADAS processors.

-

Automotive-Grade Analog/Power Experts: Strong capabilities in automotive power management, sensor interfaces, and power semiconductors (IGBT, SiC).

-

Leader in Industrial/Embedded MCUs: RX, RA, RL78 series widely used in factory automation, building control, and medical devices.

-

High-Performance Computing Platforms: R-Car series SoCs are mainstream choices for in-vehicle infotainment (IVI), digital dashboards, and ADAS systems.

-

One-Stop Solution Capability: Through M&A integration, capable of providing complete subsystem solutions of MCU/MPU + Analog/Power + Connectivity + Storage Interfaces, especially favored by automotive and industrial customers.

-

IDM Manufacturing Advantage: Retained internal manufacturing capabilities for critical processes (such as eNVM embedded flash, high-voltage BCD processes), ensuring high reliability and stable supply of automotive-grade products.

- As of 2022, the internal wafer manufacturing of semiconductor devices is managed by Renesas Electronics and its wholly-owned subsidiary Renesas Semiconductor Manufacturing Company, operating five front-end factories in the following regions: Naka, Takasaki, Saijo, Kawajiri, and Palm Bay. The backend facilities directly affiliated with Renesas Electronics and its subsidiaries are located in: Yonezawa, Oita, Nishiki, Beijing, Suzhou, Kuala Lumpur, and Penang.

Summary of Key Points in Renesas’ Development

-

Product of Japanese Giant Integration: Formed through the phased merger of the semiconductor divisions of Hitachi, Mitsubishi Electric, and NEC (Renesas Technology was established in 2003, and merged with NEC Electronics to become Renesas Electronics in 2010).

-

National Capital Redemption: During the 2012 financial crisis, the government-backed INCJ industrial fund took control and led the restructuring, divesting non-core assets and focusing on automotive and industrial sectors.

-

Strategic Transformation: Shifted from a “Japanese IDM giant” to a “system solution provider centered on automotive and IoT.”

-

M&A-Driven Growth: Initiated a “strategic acquisition” model:

-

Intersil (2017) → Strengthened analog/power

-

IDT (2019) → Enhanced analog mixed-signal, connectivity, data interfaces

-

Dialog (2021) → Enhanced power management, wireless connectivity

-

Core Competitiveness: Global automotive MCU leader, building an embedded system ecosystem of MCU + Analog + Power + Connectivity.

-

Future Challenges: Accelerate the development of SiC power devices to meet the explosive demand for smart and electric vehicles; catch up with European and American competitors in AI and high-performance computing; balance IDM model with foundry collaborations.

Long-term goal: Achieve sales exceeding $20 billion by 2030.

Renesas’ journey showcases how the Japanese semiconductor industry has navigated crises through deep integration and national support, and subsequently achieved technological reinforcement and strategic focus through precise acquisitions. Its deep roots in automotive electronics and system-level solution capabilities make it an indispensable core supplier in the wave of automotive intelligence and electrification.

References

1. Chip Company Sharing (Series on Renesas Electronics)

2. Renesas Electronics: From SiC “Amputation” to Strategic Layout of GaN

3. Insights from the Renesas Electronics Fire on Chip Supply and Demand and Inventory

4. Global Top 3, Revenue of $20 Billion, 6x Market Value Growth! What is Renesas Electronics Planning to Achieve These Three Major Goals??