1. Let’s first discuss the background of the PCB manufacturing industry

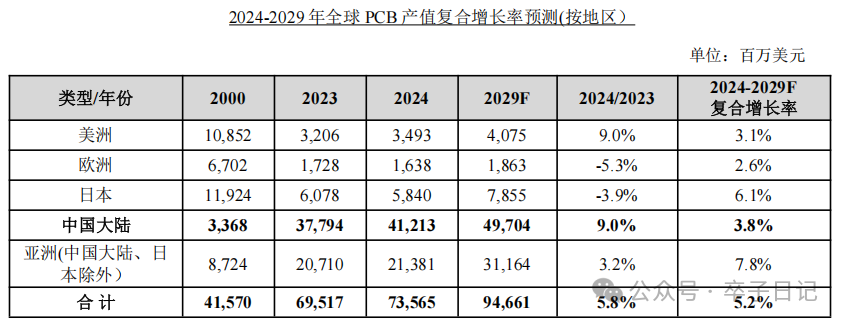

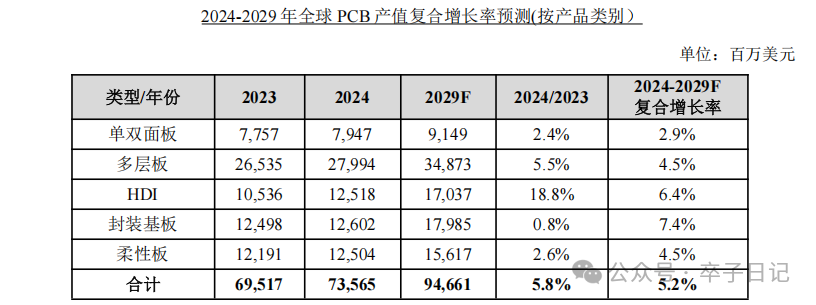

Since 2006, China has surpassed Japan to become the world’s largest PCB producer, with both production volume and value ranking first globally. In the medium to long term, the PCB industry continues to follow development trends of high frequency, high speed, high precision, and high integration. Driven by AI, high-performance computing, and high-speed network communication, the compound annual growth rates for high-layer boards (18 layers and above), HDI boards, and packaging substrates are expected to remain relatively high over the next five years, at 15.7%, 6.4%, and 7.4%, respectively.

2. Comparison of Major Companies in the PCB Industry

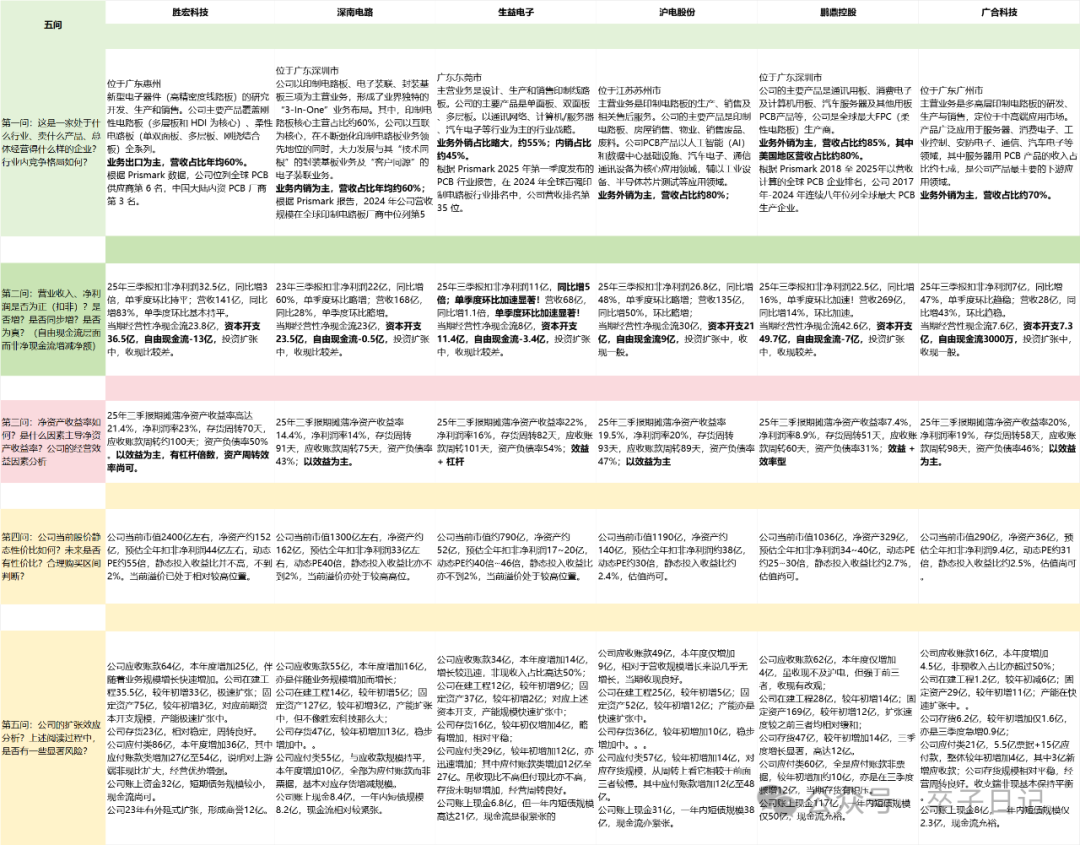

In the industry, there are about fifty to sixty publicly listed companies in the PCB supply chain. Here, we select five leading companies with a market capitalization of over 100 billion and a net profit margin of over 13%, whose main business is PCB production and sales. Additionally, we include a relatively smaller company, Guanghe Technology, which ranks high in profit indicators and asset return ratios, to compare their financial reports. Among them, Shengyi Electronics, as the core subsidiary of Shengyi Technology, focuses on PCB production and manufacturing, and we will refer to Shengyi Electronics instead of Shengyi Technology. Five of the six companies are located in Guangdong!

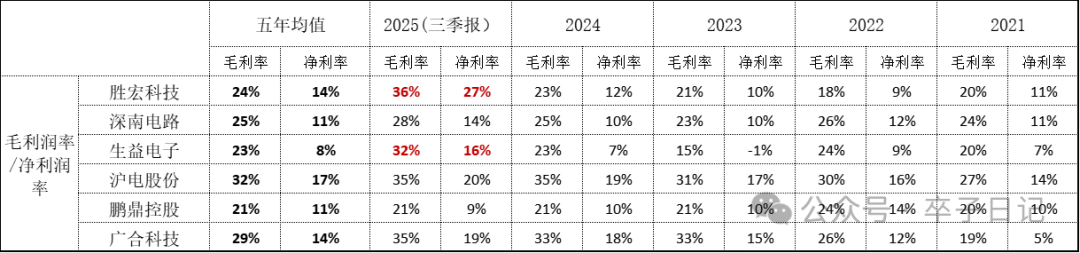

In terms of basic business layout, Shenzhen South Circuit and Huadian Technology have a small proportion of other business income in addition to PCB, while the other four focus solely on PCB production and manufacturing. Furthermore, except for Shenzhen South Circuit, which focuses on the domestic market, the other five primarily export, with Huadian and Pengding having over 80% of their sales coming from exports. Among the five exporters, North America is the main market, confirming North America’s position as a leader in the global AI computing power industry. In terms of operational efficiency, several leading companies in the industry perform well; asset returns are primarily efficiency-based, but there are some differences: Shenzhen South Circuit and Pengding are relatively weaker in both five-year averages and the current quarter of the 25th year; Shenzhen South Circuit has shown some improvement in the 25th year’s performance, while Pengding remains relatively stable and weak, which may be related to its broad business structure. Huadian Technology belongs to the category of stable and excellent performers, with the best five-year average but has recently been slightly surpassed; the two dark horses are Shenghong and Shengyi, both showing a significant increase in current performance indicators, benefiting from capturing new demand opportunities in high-end AI computing overseas over the past year. Under the trend of high-end PCB structure, they will continue to benefit. Guanghe focuses on high-end PCB demand for computing servers, and its performance indicators are also in a relatively favorable position.

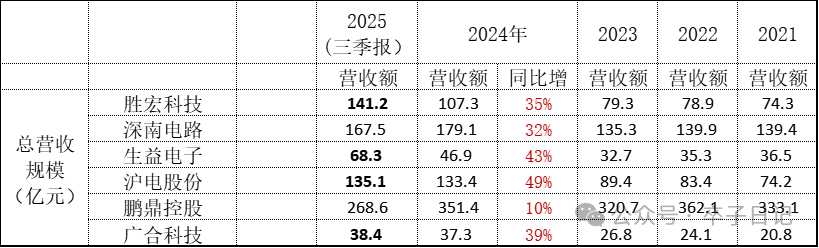

In terms of basic business layout, Shenzhen South Circuit and Huadian Technology have a small proportion of other business income in addition to PCB, while the other four focus solely on PCB production and manufacturing. Furthermore, except for Shenzhen South Circuit, which focuses on the domestic market, the other five primarily export, with Huadian and Pengding having over 80% of their sales coming from exports. Among the five exporters, North America is the main market, confirming North America’s position as a leader in the global AI computing power industry. In terms of operational efficiency, several leading companies in the industry perform well; asset returns are primarily efficiency-based, but there are some differences: Shenzhen South Circuit and Pengding are relatively weaker in both five-year averages and the current quarter of the 25th year; Shenzhen South Circuit has shown some improvement in the 25th year’s performance, while Pengding remains relatively stable and weak, which may be related to its broad business structure. Huadian Technology belongs to the category of stable and excellent performers, with the best five-year average but has recently been slightly surpassed; the two dark horses are Shenghong and Shengyi, both showing a significant increase in current performance indicators, benefiting from capturing new demand opportunities in high-end AI computing overseas over the past year. Under the trend of high-end PCB structure, they will continue to benefit. Guanghe focuses on high-end PCB demand for computing servers, and its performance indicators are also in a relatively favorable position. In terms of revenue scale, the PCB industry is expected to see significant growth starting in 2024. From the emergence of ChatGPT-4 in 2023 to 2024, major AI manufacturers have begun a competition for computing power equipment, directly driving a leap in the PCB industry. This is the industry background, and among these six leaders, Shenghong, Shengyi, Huadian, and Guanghe continue to maintain high growth in the 25th year, having already achieved last year’s total revenue performance by the third quarter of the 25th year.

In terms of revenue scale, the PCB industry is expected to see significant growth starting in 2024. From the emergence of ChatGPT-4 in 2023 to 2024, major AI manufacturers have begun a competition for computing power equipment, directly driving a leap in the PCB industry. This is the industry background, and among these six leaders, Shenghong, Shengyi, Huadian, and Guanghe continue to maintain high growth in the 25th year, having already achieved last year’s total revenue performance by the third quarter of the 25th year. With the continuous expansion of industry demand and structural upgrades, these companies are also on a rapid expansion path. A clear impression is that the current fixed assets and construction in progress of these companies are very large, with assets being quite “heavy”. The three companies with assets that are disproportionately large compared to their total net assets are Shengyi, Shenzhen South Circuit, and Guanghe, especially Shengyi Electronics, whose net assets are almost entirely fixed assets and construction in progress. It can be said that they are to some extent “running with a burden”. In an upward industry cycle, they may gain an advantage, but once the industry growth slows or technology shifts, they may start to struggle. Among them, Huadian and Pengding appear to be relatively “lighter”.

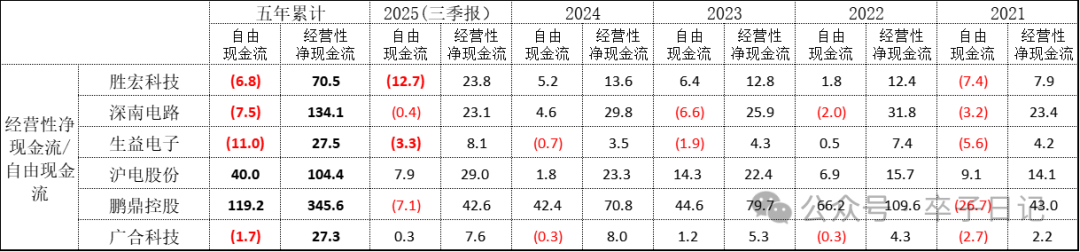

With the continuous expansion of industry demand and structural upgrades, these companies are also on a rapid expansion path. A clear impression is that the current fixed assets and construction in progress of these companies are very large, with assets being quite “heavy”. The three companies with assets that are disproportionately large compared to their total net assets are Shengyi, Shenzhen South Circuit, and Guanghe, especially Shengyi Electronics, whose net assets are almost entirely fixed assets and construction in progress. It can be said that they are to some extent “running with a burden”. In an upward industry cycle, they may gain an advantage, but once the industry growth slows or technology shifts, they may start to struggle. Among them, Huadian and Pengding appear to be relatively “lighter”. In the context of rapid expansion, their cash flow situation does not look as good as their revenue and profits. Over the past five years, four of the six companies have been unable to cover their capital expenditures with accumulated operating cash flow (most of which is applied to fixed asset expansion), while Huadian and Pengding have real surpluses of 4 billion and 11.9 billion, respectively. In the 25th year, compared to their own scale, Shenghong, Pengding, and Shengyi are all making large investments in expansion.

In the context of rapid expansion, their cash flow situation does not look as good as their revenue and profits. Over the past five years, four of the six companies have been unable to cover their capital expenditures with accumulated operating cash flow (most of which is applied to fixed asset expansion), while Huadian and Pengding have real surpluses of 4 billion and 11.9 billion, respectively. In the 25th year, compared to their own scale, Shenghong, Pengding, and Shengyi are all making large investments in expansion. Overall, Shengyi and Shenghong have become dark horses in the past year, accelerating in scale and efficiency, showing a clear upward trend, bringing high expectations, and currently having the highest static valuation premiums in the market; while Pengding, as the largest in scale with a broad business coverage, lacks efficiency to match its size, growing slowly but maintaining its volume, it may be the first PCB company in the industry to transition from a growth model to a mature dividend model; Huadian stands out in terms of efficiency, with a balanced asset structure and relatively good overall strength, and its valuation premium is still acceptable. Guanghe, although a smaller player in scale, focuses on the fastest-growing structural field in the industry, balancing growth and efficiency, and may win more capital favor in the future. Shenzhen South Circuit, primarily focused on the domestic market, may have missed the overseas computing expansion wave and has not performed as prominently in the past year. The high-endization of domestic computing infrastructure may be progressing slowly, but it will eventually catch up.

Overall, Shengyi and Shenghong have become dark horses in the past year, accelerating in scale and efficiency, showing a clear upward trend, bringing high expectations, and currently having the highest static valuation premiums in the market; while Pengding, as the largest in scale with a broad business coverage, lacks efficiency to match its size, growing slowly but maintaining its volume, it may be the first PCB company in the industry to transition from a growth model to a mature dividend model; Huadian stands out in terms of efficiency, with a balanced asset structure and relatively good overall strength, and its valuation premium is still acceptable. Guanghe, although a smaller player in scale, focuses on the fastest-growing structural field in the industry, balancing growth and efficiency, and may win more capital favor in the future. Shenzhen South Circuit, primarily focused on the domestic market, may have missed the overseas computing expansion wave and has not performed as prominently in the past year. The high-endization of domestic computing infrastructure may be progressing slowly, but it will eventually catch up.