While the entire industry is shouting, “AI PCB is the next golden decade,” we are more concerned about: Is the technical threshold underestimated? Is capacity expansion overheated? Do small and medium-sized manufacturers still have opportunities?

In the past week, the PCB industry chain has entered a “high-energy state”: Shengyi Electronics’ 2.6 billion yuan private placement has been approved, Jiayuan Technology’s copper foil prices have risen again, Shenghong’s first AI-HDI board has rolled off the production line in Vietnam, and Samsung Electro-Mechanics is ramping up its ABF substrate production… Capital and capacity are flooding into the AI high-end track at an unprecedented speed.

However, beneath the fervor, there are undercurrents. In this week’s report, we will help you clarify the data, dissect the logic, and anticipate the risks.

🔍 1. Core Trend of the Week in One Sentence

“Leading companies are accelerating their positioning in AI high-end PCBs, material costs continue to be under pressure, industry concentration is rapidly increasing, and low-end capacity is being cleared out quickly.”

📈 2. Key Data Dashboard (See suggested images at the end)

| Indicator | This Week’s Value | Week-on-Week | Year-on-Year | Trend Interpretation |

|---|---|---|---|---|

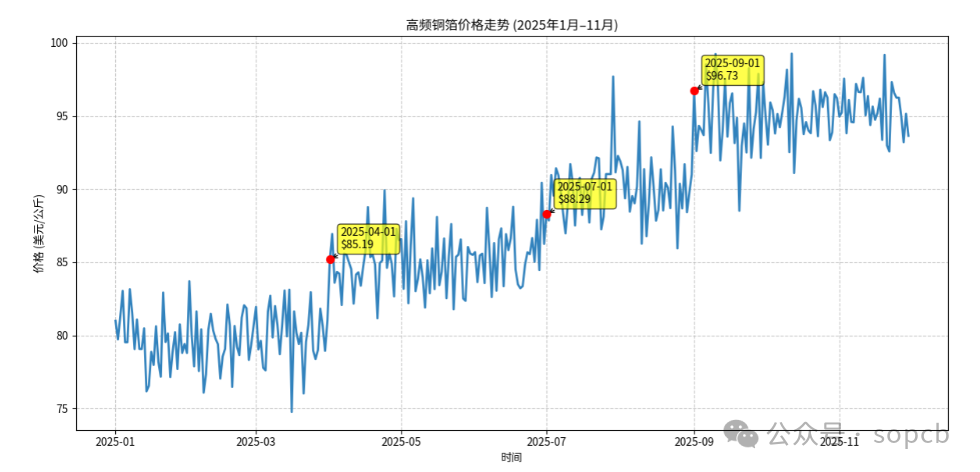

| Average Price of High-Frequency HVLP Copper Foil (4μm) | 280 yuan/㎡ | ↑8% | ↑22% | Jiayuan, Tongguan, and others collectively raised prices due to a shortage of high-purity copper raw materials |

| LME Three-Month Copper Price | 9,820 USD/ton | ↑3.1% | ↑18.5% | Manufacturing recovery + low inventory pushing prices up |

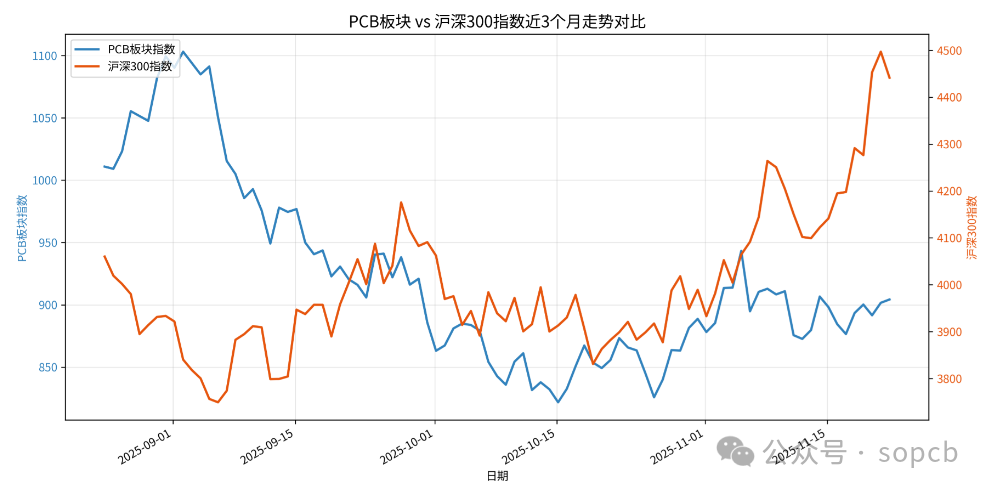

| PCB Sector Index (884132.WI) | 2,156 points | ↑2.8% | ↑35.2% | Driven by AI order expectations, Shenzhen and Huadian lead the rise |

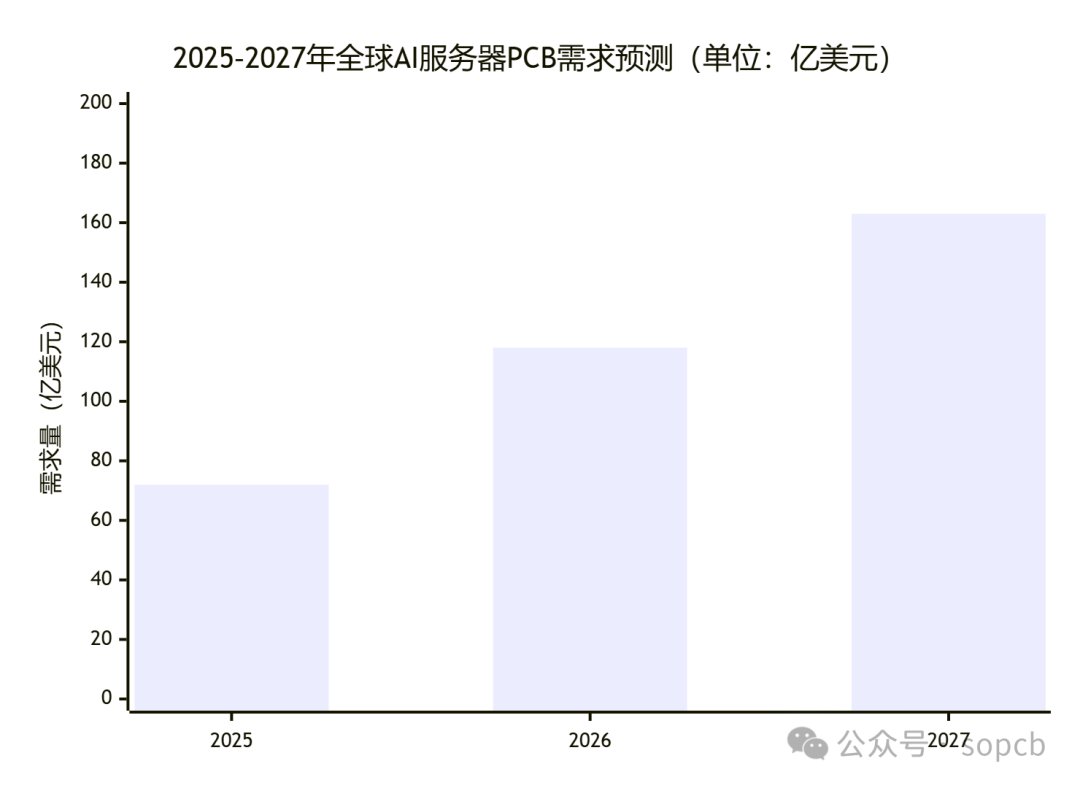

| Value of AI Server Single PCB | ≈2,100 USD | — | ↑40% | High multilayer + HDI + high-frequency materials combined |

💡 SOPCB Reminder: Material costs now account for over 35% of the AI-HDI BOM, companies without vertical integration capabilities will continue to face pressure on gross margins.

Note: The prices shown in this chart are simulated data for demonstration purposes; please refer to authoritative market reports and industry data for actual price trends.

Note: The prices shown in this chart are simulated data for demonstration purposes; please refer to authoritative market reports and industry data for actual conditions.

🏭 3. Top 5 Corporate Dynamics (11.18–11.22)

| Rank | Company | Action | Technical/Business Keywords | Potential Impact |

|---|---|---|---|---|

| 1 | Shengyi Electronics | Approved 2.6 billion yuan private placement | Dongguan AI-HDI (167,000㎡), Ji’an high multilayer (700,000㎡) | Strengthen supply chain position with Nvidia/Huawei |

| 2 | Jiayuan Technology | HVLP copper foil price increased by 8% | 4μm low profile, ultra-high purity copper | Cost pressure on small and medium PCB manufacturers intensifies |

| 3 | Shenghong Technology | First AI-HDI board rolled off the line in Vietnam | Overseas delivery, ODM binding | Avoid geopolitical risks, closer to customers |

| 4 | Samsung Electro-Mechanics | Expanding ABF substrate line in Vietnam | Monthly production of 300,000 pieces, production starts in Q2 2026 | Coordinated layout of packaging substrates and high-end PCBs |

| 5 | Taiko Electronics | Released TUC-9830 material | Df=0.0018@10GHz, Nvidia certified | Domestic substitution faces technical barriers again |

Note: The prices shown in this chart are simulated data for demonstration purposes; please refer to authoritative market reports and industry data for actual trends.

Note: The prices shown in this chart are simulated data for demonstration purposes; please refer to authoritative market reports and industry data for actual conditions.

🧠 4. SOPCB In-Depth Observation: Three Questions on the AI PCB Boom

❓ Question 1: Is the HDI micro-hole yield really just a “paper parameter”?

Many manufacturers claim to be able to produce 50μm micro-holes, but if the actual mass production yield is below 85%, it cannot pass the AI customer audit.

- Real Threshold: Laser drilling consistency + plating hole fullness + AOI detection rate

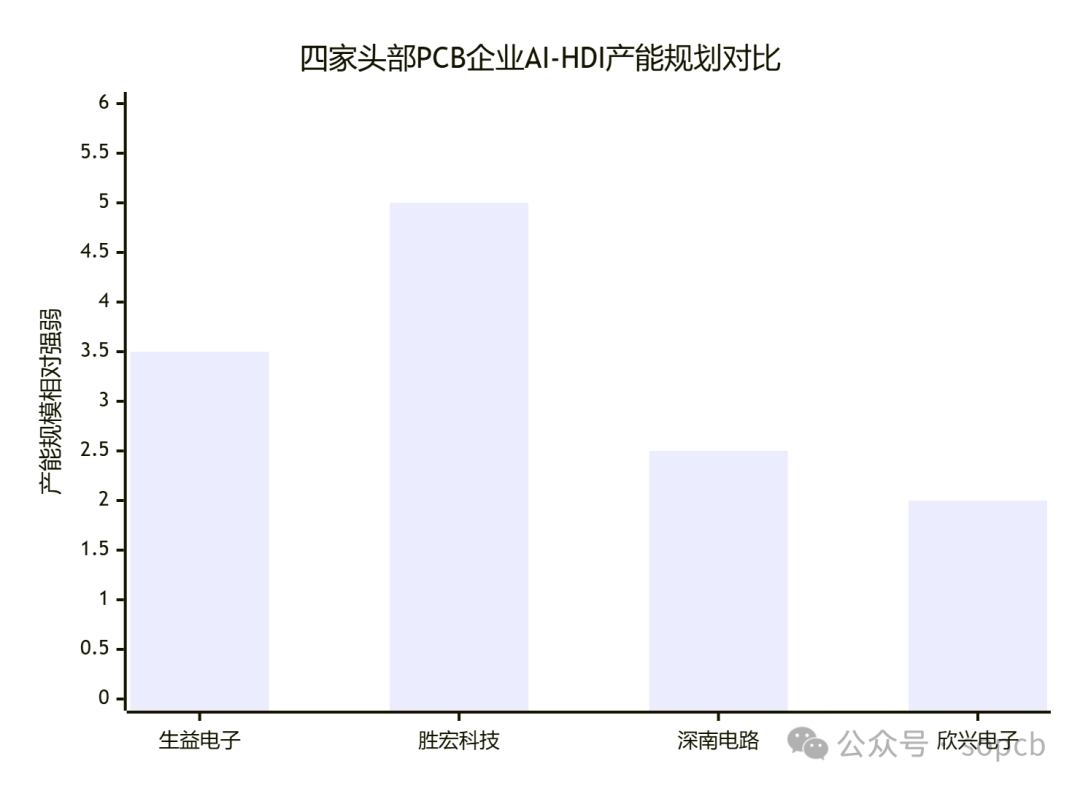

- Current Situation: Only companies like Shenzhen, Shengyi, and Xinxing have stable yield capabilities above 85%

Technology is not about “can it be done,” but “can it be done stably in large quantities.”

❓ Question 2: Binding large customers = easy win? Don’t overlook hidden costs!

A second-tier manufacturer revealed: To secure a North American AI customer, over 20 million yuan was invested in certification costs, with a payment term of 120 days and a gross margin of only 12%.

- Truth: Large customer orders ≠ high profits, certification costs, payment terms, rework rates are often overlooked

- Advice: Prioritize entering the secondary supplier system (such as power modules, switchboards), accumulate experience before tackling mainboards

❓ Question 3: Will there be a “periodic oversupply” of high-end PCBs in 2026?

According to SOPCB estimates:

- By the end of 2025, global AI-HDI effective capacity will be ≈ 1.8 million ㎡/year

- By the end of 2026, it will soar to 3.2 million ㎡/year (+78%)

- However, the demand growth rate during the same period is expected to be **55%** (Prismark)

⚠️ If AI chip shipments do not meet expectations, a price war may occur in Q3 2026.

🔮 5. Next Week’s Preview (11.23–11.29)

- [Exhibition] 2025 China International PCB Exhibition (November 23–25, Shenzhen)→ Focus: Physical display of AI server PCBs, green process solutions

- [Financial Report] Huadian Co., Ltd. will release Q3 performance briefing minutes→ Key: AI order proportion, gross margin changes

- [Policy] The Ministry of Industry and Information Technology may issue the “Advanced Electronic Circuit Industry Support Directory”→ Packaging substrates and high-frequency high-speed materials may be included in the subsidy range

💬 6. Reader Interaction

What do you think will be the biggest variable for AI PCBs in 2026?A. Technological breakthroughs (e.g., optical waveguide PCBs)B. Customer concentration (Nvidia/AMD/Huawei monopoly)C. Geopolitics (Southeast Asia vs. mainland China capacity distribution)D. Material bottlenecks (ABF film, high-frequency resin domestic substitution progress)

👉 Please leave your option letter + your reasoning in the comments!

🔔 Follow SOPCB, we are not just information porters, but trend interpreters

Data sources: Company announcements, Prismark, LME, Wind, CPCA, TTM, SOPCB industry research*Editor: SOPCB Content Center | Original content, reprinting requires authorization and citation of the source

Disclaimer | This article’s information copyright belongs to the original author and does not represent the views of this platform, nor is it a basis for investment and financial decisions, but for sharing purposes. If there are copyright or information errors, please contact us for correction or deletion. Thank you!

SOPCB【搜PCB】| Focus on PCB technology frontiers, market dynamics, and supply chain insights to assist the industry in making precise decisions.

☟☟For more PCB industry news, please followSOPCB WeChat Official Account

Light it up Share it with more people↓

Share it with more people↓