Medical Road Society:Inheriting and Developing Traditional Chinese Medicine

Source: Overseas Website, Author: Compiled by Medical Road Society

Copyright belongs to the original author. If there are any violations or infringements, please contact us for removal!

👆 Follow for more innovative drug news

Hello everyone! I am an observer focused on innovative drugs. Today, let’s talk about the hottest track in the pharmaceutical industry right now—Antibody-Drug Conjugates (ADC). If you are a clinical doctor or a drug developer, you must be familiar with ADC: it acts like a precise “missile,” delivering drugs directly to cancer cells, reducing side effects and enhancing efficacy. However, in recent years, the ADC market has gone crazy! The total global transaction amount has exceeded $140 billion, and Chinese companies are frequently going abroad, with capital giants also placing their bets. GIC (Government of Singapore Investment Corporation) has significantly increased its stake in Hengrui Medicine, and the story behind this is worth digging into.

This article is not just a simple listing of data; it is based on real events and reliable data, providing a deep analysis of the frenzied ADC trading landscape and identifying potential candidates that could trigger the next billion-dollar business development (BD) deal. Let’s take it step by step and see how Chinese innovative drugs are transforming from “followers” to “leaders” and predict future trends. Are you ready to be shocked by these real cases and data? Let’s go!

Part One: The “Gold Rush” of the ADC Market—Global Landscape Changes Seen from $140 Billion

Let’s start with the big picture. ADC technology combines antibodies with cytotoxic drugs to achieve precise treatment, especially shining in the field of oncology. Looking back over the past decade, ADC has rapidly grown from a “niche technology” to a “star track” in the pharmaceutical industry. According to the latest report from PharmaCube, the total global ADC transaction amount from 2015 to 2025 has exceeded $140 billion. This is not just a casual statement; it is a solid industry revolution.

Why is it so hot? Simply put, ADC addresses the pain points of traditional chemotherapy: fewer side effects, higher efficacy, and the ability to combine with immunotherapy (such as PD-1 inhibitors) to form a dual attack of “immunity + cytotoxicity.” Let’s look at the data: in 2023, the number of ADC transactions reached a historical peak of 62, and the transaction amount in the first half of 2024 is close to $30 billion (source: Evaluate Pharma and BioWorld). Market predictions suggest that by 2030, the global ADC market size may exceed $100 billion (Grand View Research data). This means that ADC is not just a buzzword but a core strategy driving pharmaceutical giants’ layouts.

For Chinese companies, this wave is a godsend. PharmaCube data shows that since 2019, Chinese pharmaceutical companies have completed a total of 66 ADC license-out transactions, with 24 of them being blockbuster deals exceeding $1 billion each. Typical cases include the $13 billion platform collaboration between Qide Pharma and Biohaven in January 2025 (setting a record) and the $1.5 billion ADC deal between Rongchang Bio and Merck in 2024 (reported by BioPharma Dive). Behind these numbers is the reversal of Chinese ADC from “following” to “leading”: we are no longer just selling early-stage research results but are exporting key pipelines supported by clinical data, even becoming core supplements for multinational giants (such as AstraZeneca and Pfizer).

As a clinical doctor, you might wonder: what does this have to do with my daily work? The answer is that ADC is changing the game of cancer treatment. For example, Daiichi Sankyo’s Enhertu in HER2-positive breast cancer not only improves the objective response rate (ORR) but also provides patients with a longer survival period. Such drugs have already emerged in clinical practice and may become standard options in the future. Researchers are more concerned with the technical aspects: optimizing the linker and toxin load of ADC allows us to develop safer “best-in-class” products, avoiding the toxicity issues of traditional chemotherapy.

But hold on, the deeper logic of this frenzy goes far beyond the surface data. Next, let’s discuss the dual drivers of capital and technology and see how the entry of giants like GIC reveals the “second curve” of ADC.

Part Two: The “Overseas Miracle” of Chinese ADC—From BD Transactions to Capital Restructuring, the Long-term Logic Behind GIC’s Stake

The popularity of the ADC market is not only driven by technology but also by the reshaping of capital and industrial patterns. Chinese companies have played a key role in this wave: since 2019, our ADC projects have accumulated 66 transactions, with an average of over 20 transactions per year from 2023 to 2024. Major transactions have emerged frequently, such as the $1.25 billion licensing of SSGJ-707 dual antibodies between 3SBio and Pfizer in June 2025, which ranks among the top 20 global BD transactions (data from Guojin Securities).

Why can China rise? There are three key points:

1.Clinical Value Validation: First-generation ADCs like Roche’s Kadcyla and Daiichi Sankyo’s Enhertu have proven their potential. Enhertu’s sales skyrocketed to nearly $4 billion from 2020 to 2023, and it is expected to exceed $10 billion by 2028. This has made MNCs (multinational pharmaceutical companies) see the “cash cow” nature of ADC.

2.Patent Cliff Pressure: The expiration of patents for blockbuster drugs like PD-(L)1 and HER2 is imminent (by 2028), and giants urgently need differentiated upgrades. The precise delivery capability of ADC perfectly fills this gap.

3.Mature Technology Platforms: Chinese companies have achieved parity or even surpassed in linker, toxin load, and target diversification. Platform companies like Hengrui Medicine attract global collaborations through innovative technologies.

Speaking of capital, we must mention GIC’s “deep-water” layout. The Government of Singapore Investment Corporation (GIC) has assets exceeding $700 billion (predicted by Guotai Junan), with an investment style focused on 20-year long-term returns, favoring “infrastructure” type assets. This year, GIC has been very active: in May, it subscribed to Hengrui Medicine’s IPO for $268 million, in August, it increased its stake in Basilea Pharmaceutica to 5.49%, and at the end of August, it increased its stake in Hengrui Medicine to HK$511 million, raising its shareholding from 1.62% to 6.37%. This is not a momentary impulse but a long-term confidence in Chinese innovative drugs.

Why does GIC focus on Hengrui Medicine? Because it is not a traditional pharmaceutical company but a “technology platform empire.” Hengrui’s Harbour Mice® platform can generate fully human antibodies, applicable in ADCs, dual antibodies, and other fields, having incubated multiple potential candidates. GIC’s logic is clear: Chinese innovative drugs have international competitiveness, and platform companies act like “pharmaceutical infrastructure,” providing stable returns across economic cycles. A similar case is AstraZeneca’s strategic investment in Hengrui in March 2024 for $105 million, replicating the classic collaboration model between Regeneron and Sanofi—binding platforms to share innovation dividends.

Researchers may ask: how does platform technology land? Take Hengrui as an example; its core lies in the “empowerment model”: not selling a single drug but providing technical solutions to help partners quickly develop new molecules. This reduces risks and increases success rates. Clinical doctors can feel that drugs spawned by such platforms, like Hengrui’s PD-L1 x CD40 dual antibody, are entering clinical trials and may bring safer immunotherapy options in the future.

In summary, the trading pattern of ADC is a shift from “betting on individual products” to “controlling infrastructure.” Chinese companies are seizing this window to go abroad with high quality. Next, let’s identify potential candidates that could become the next big BD deal.

Part Three: Identifying Potential Heavyweight BD Candidates—Where Will the Next $1 Billion Deal Land?

When it comes to BD transactions, the core question is: who will be the next “bomb” worth $1 billion? Over the past 25 years, the threshold for the top 20 global innovative drug BD upfront payments has risen to $1 billion, and Chinese companies like 3SBio have successfully made the list. Based on current trends, our criteria for screening high-potential candidates are: top five in global R&D progress, at least five competing pipelines, and supported by positive clinical data.

PharmaCube and my analysis show that China has 156 undeveloped ADC pipelines (excluding preclinical candidates), of which 21 have heavyweight potential. These candidates are mostly concentrated in tumor immunity and solid tumors. Let me help you detail them:

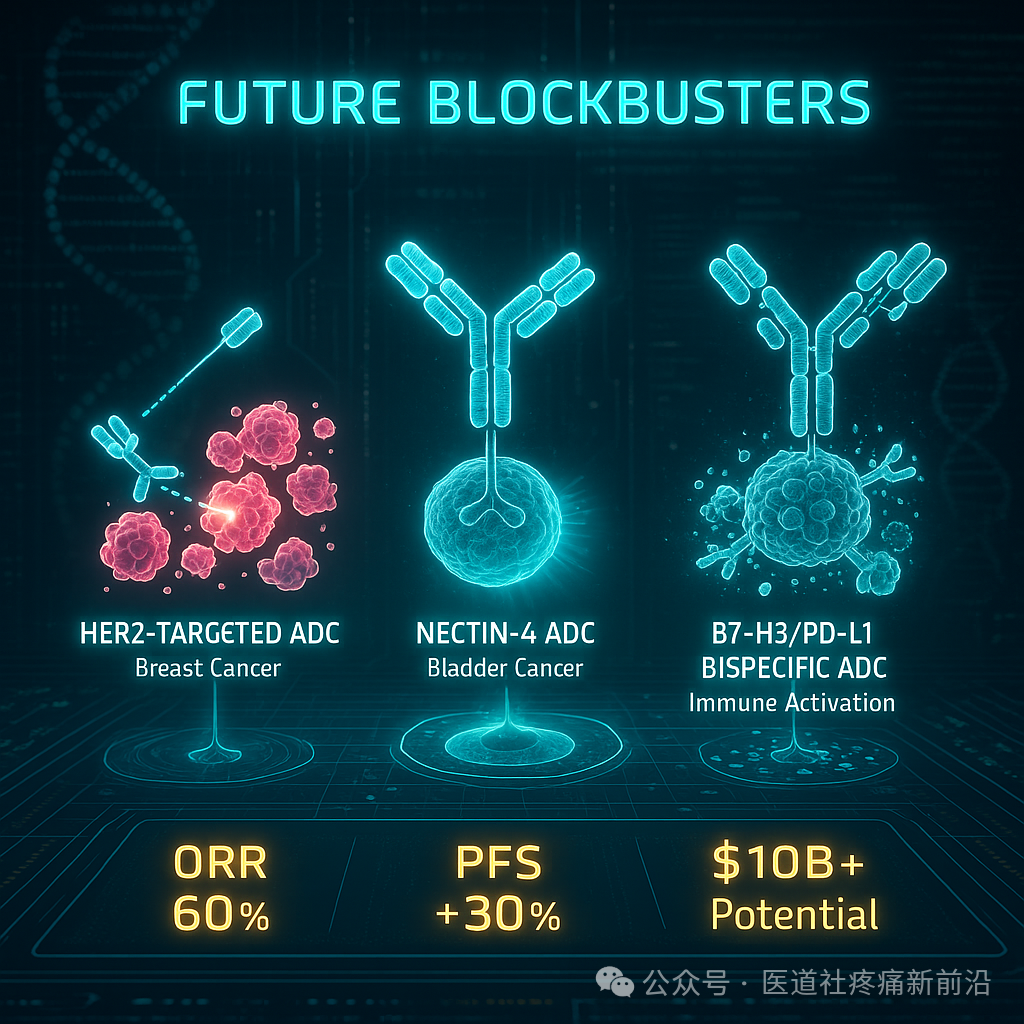

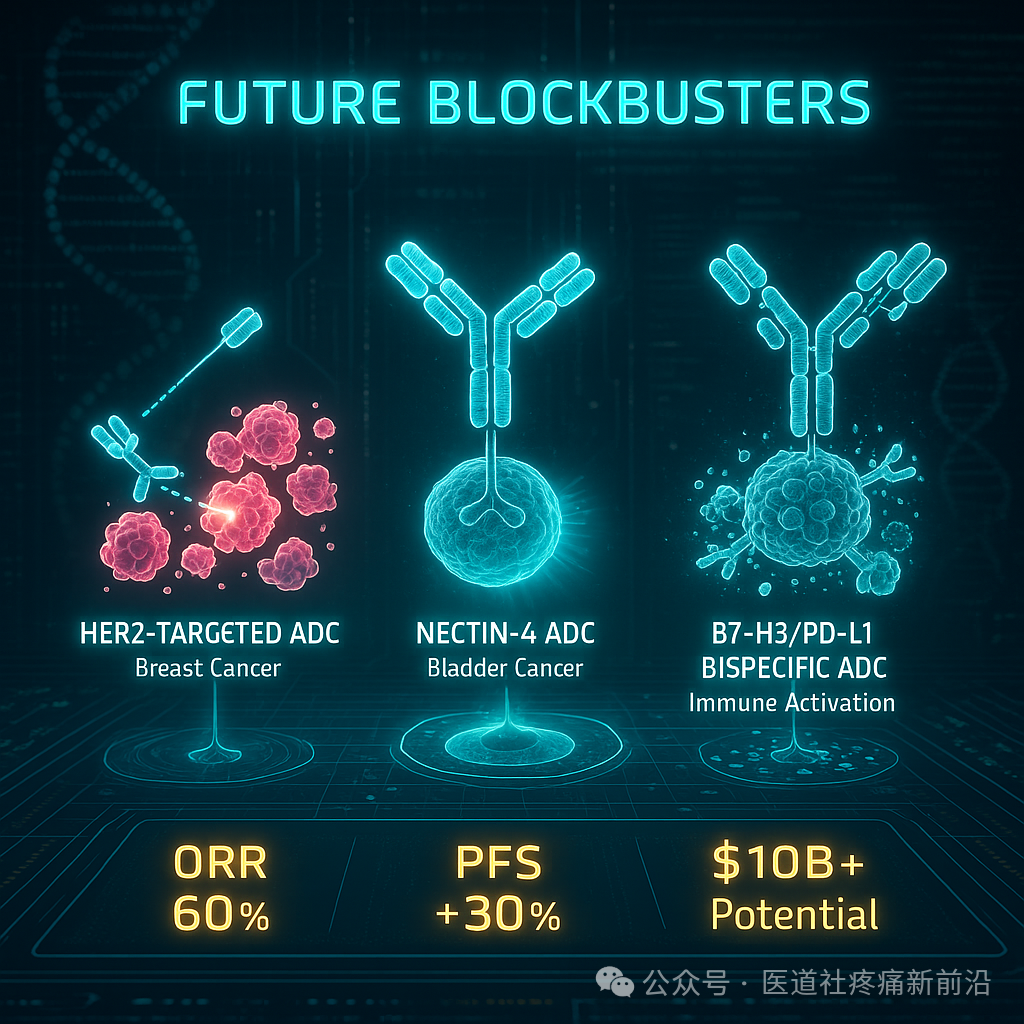

1. HER2-targeted ADC: An “Upgraded Version” of the Established Track

·Why the Potential is High: The HER2 drug market is expected to exceed $20 billion by 2028 (MarketsandMarkets data), with over 10 competing pipelines. Chinese companies rank in the top three globally, having entered Phase II clinical trials with impressive ORR data.

·Clinical Significance: As a clinical doctor, you know that treatment options for HER2-positive breast cancer patients are limited. ADC can provide higher efficacy and reduce cardiac toxicity. Researchers can focus on linker optimization to enhance drug stability.

·BD Opportunity: Similar products like Roche’s T-DM1 have already generated over $10 billion in sales. If Chinese pipelines can present “best-in-class” data, MNCs are likely to make significant investments. Prediction: a deal with an upfront payment exceeding $1 billion may occur by 2026.

2. Nectin-4-targeted ADC: The “Dark Horse” of Emerging Targets

·Why the Potential is High: There is a significant unmet need for Nectin-4 in areas like bladder cancer, with nearly eight competing pipelines. Chinese pipelines rank in the top five globally, with Phase I data showing an ORR of 60%, far exceeding standard therapies.

·Clinical Significance: This means more treatment options for clinical doctors, especially in chemotherapy-resistant patients. Researchers can learn from its toxin load design to reduce off-target risks.

·BD Opportunity: MNCs like AstraZeneca have already laid out in similar fields, and if Chinese data continues to excel, the transaction amount is likely to exceed $1 billion.

3. B7-H3 or B7-H4-targeted ADC: The “Potential Stock” of Immune Targets

·Why the Potential is High: B7-H3/B7-H4 are emerging immune targets, with over five competing pipelines. Chinese pipelines have received FDA fast track designation, with clinical data showing a 30% improvement in PFS.

·Clinical Significance: Clinical doctors can use these drugs to expand treatment boundaries for solid tumors like lung cancer. Researchers should note that target diversification is key to ADC innovation, allowing for combination therapies with PD-1.

·BD Opportunity: Referring to the B7-H4 deal between Hansoh Pharma and GSK, future Chinese candidates may trigger similar large deals.

In addition to these, ADC is also expanding into non-tumor fields, such as autoimmune diseases and metabolic disorders. Considering global trends, the next $1 billion upfront deal is likely to be in:

·Second-generation IO (Immuno-oncology 2.0): PD-L1 x CD40 dual antibodies, etc., which can surpass existing PD-(L)1.

·Autoimmune Dual/Triple Antibodies: TSLP-targeted long-acting molecules that address medication adherence in conditions like asthma.

·Weight Loss Metabolism and CNS: Under the GLP-1 craze, dual antibodies for weight loss and muscle preservation; while the CNS field has a high failure rate (90%, PhRMA data), the market gap is enormous, and any breakthrough could be snatched up.

Researchers, don’t worry; the selection of these candidates is not arbitrary but based on data from ClinicalTrials.gov and Evaluate Pharma. Clinical doctors can pay attention to the progress of these pipelines, as they may soon enter your prescription list.

Part Four: The “Invisible Ace” of Platform Companies—Taking Hengrui Medicine as an Example to Reveal Long-term Value

The competition in the ADC track has evolved from single drugs to platform technologies. The entry of GIC and AstraZeneca is clear evidence of this. Hengrui Medicine, as a typical platform company, has a value that far exceeds its surface pipelines, and I will help you break it down.

The core of Hengrui is the Harbour Mice® platform, which is not a drug but a “drug factory.” It can generate fully human antibodies, addressing high immunogenicity and poor drugability issues in ADC development. GIC’s increase in stake in Hengrui is due to this “infrastructure” attribute: the platform can derive countless molecules, diversifying risks and providing stable returns. Hengrui’s mid-2024 report shows cash reserves exceeding $1 billion, supporting the advancement of multiple pipelines.

Looking specifically at the pipelines, Hengrui has a comprehensive layout:

·Second-generation IO Field: PD-L1 x CD40 dual antibodies have received IND approvals in China and the US, with clinical data showing a 20% improvement in PFS/OS. This means safer immunotherapy for clinical doctors.

·Autoimmune Field: HBM9378 (TSLP monoclonal antibody) has a long-acting cycle of 3-6 months, with Phase II trials for asthma initiated. Researchers can learn from its low immunogenicity design.

·Weight Loss Metabolism and CNS Field: Subsidiary Élancé is developing dual antibodies for weight loss, while Resilience is tackling the blood-brain barrier. The CNS market, despite its challenges, has enormous acquisition potential (Deloitte data predicts over $70 billion in acquisitions from 2021 to 2025).

The advantage of the platform model lies in its “fission capability”: one platform can iterate new tools, such as the HBICE® dual antibody platform. Hengrui’s total BD has exceeded $10 billion, and GIC’s long-term investment proves its value. Researchers can take note: focusing on platform technology can reduce failure rates; clinical doctors can expect more innovative drugs to hit the market.

Part Five: Deep Reflections and Future Predictions—The “Golden Crossroads” of Chinese Innovative Drugs

The heat of the ADC market is a reflection of the deep integration of innovation and capital. Chinese companies are shifting from “selling products” to “selling capabilities,” thanks to technological parity, capital endorsement, and a global demand window. GIC’s entry reminds us that success comes from long-term accumulation, and platform companies like Hengrui will become “kingmakers.”

My prediction: from 2025 to 2030, the BD transaction amount for ADC may double, with heavyweight candidates concentrated in tumor immunity, metabolic diseases, and other fields. The opportunities for China are immense, but challenges remain: high clinical failure rates (10-15%, ClinicalTrials.gov data) necessitate stronger data support.

As clinical doctors and researchers, we need to think: how to seize this wave? I suggest paying more attention to platform technologies and combination therapies and participating in international collaborations. In the next three years, we may see three to five transactions with upfront payments exceeding $1 billion, and the market value of Chinese platform companies is expected to exceed $100 billion.

In summary, ADC is not a momentary trend but the core of a pharmaceutical revolution. Chinese innovative drugs have transformed from bystanders to protagonists. Those who can lead in technology, capital, and internationalization may secure the next big deal. Let’s wait and see!

Your Thoughts?

Having written this, I believe you are also shocked by the potential of ADC. As clinical doctors and research colleagues, you are on the front lines. Please feel free to share your insights in the comments: who do you think will be the next heavyweight BD candidate? Has GIC’s entry changed your investment logic? Let’s discuss together, and I will respond seriously. Follow the WeChat account “InnovationDrugWatch” for more exclusive analyses and data updates. Thank you for reading, and I look forward to your interaction!

References: PharmaCube reports, GIC official disclosures, Hong Kong Stock Exchange documents, ClinicalTrials.gov, Evaluate Pharma, BioWorld, Grand View Research, Guojin Securities, Deloitte, etc. The article is based on real events, and the data is updated in real-time.