Company Overview and Industry Background

OmniVision Technologies (formerly known as Will Semiconductor, renamed in 2025) is a leadingfabless semiconductor design company in China, with products including image sensors, analog circuits, and display SoCs, widely used in smartphones, security, automotive electronics, action cameras, and panoramic photography. In 2024, its shipments exceeded11 billion units, establishing a significant competitive edge in the global image sensor market. Benefiting from domestic substitution, automotive intelligence, and consumer electronics upgrades, industry demand continues to rise, providing the company with a growth “tailwind.”

Overview of 2024 Annual Performance

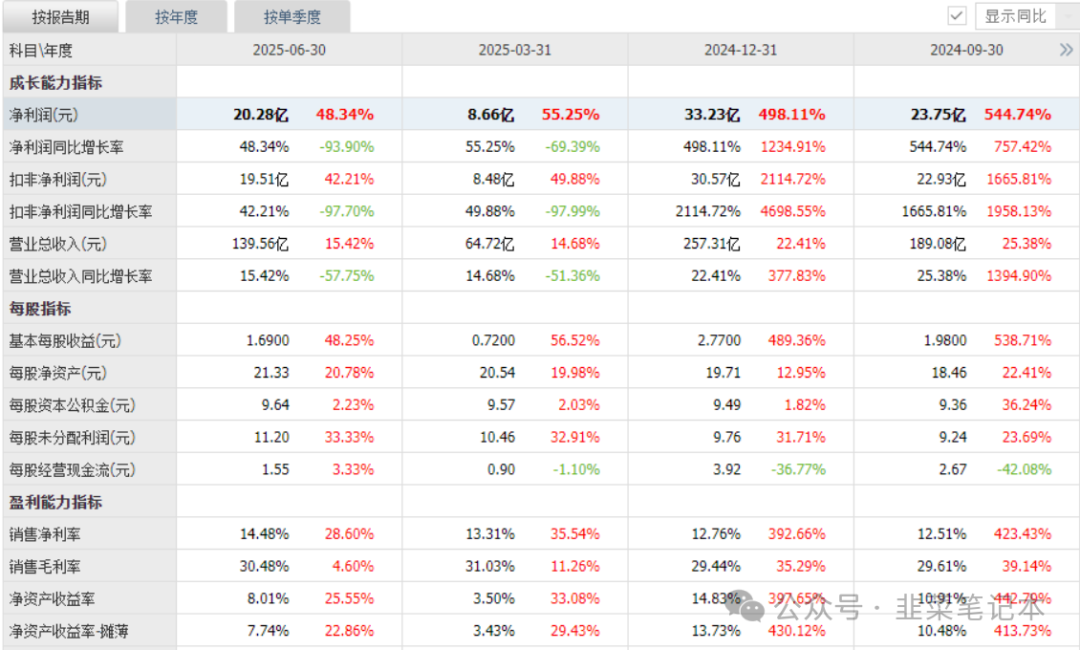

OmniVision achieved revenue of 25.731 billion yuan in 2024 (up 22.41% year-on-year) and a net profit of 3.323 billion yuan (up 498.11%), with a gross margin increase to 28.2%. The core driver was the image sensor business (19.19 billion yuan, accounting for 74.76%), with automotive electronics contributing 31% (up 12 percentage points year-on-year) and smartphones 51%. R&D investment was 3.245 billion yuan (12.61% of revenue), with a total of 4,865 patents, and the market share of automotive-grade CIS reached 32.9% (the highest globally), successfully entering BYD’s “God Eye” 12-camera solution.

Summary of Q1 2025 Performance

In Q1 2025, revenue was 6.472 billion yuan (up 14.68%), net profit was 866 million yuan (up 55.25%), and gross margin was 31.03% (up 2.83 percentage points). Automotive CIS revenue increased by 47% year-on-year (accounting for 34%), with significant contributions from emerging markets such as DJI’s Osmo 360 panoramic camera. Q2 revenue reached 7.4 billion yuan (up 14.77%), setting a historical high, with net profit of 1.11 billion yuan (up 37.21%), and the proportion of automotive electronics revenue increased to 36%, alongside management efficiency improvements driving net profit margin up to 15%.

Highlights: Q2 2025 and First Half Performance

In the first half of 2025, OmniVision’s performance was remarkable, with main revenue reaching 13.956 billion yuan, a year-on-year increase of 15.42%, and Q2 alone achieving 7.484 billion yuan, up 16.07% year-on-year. The net profit attributable to the parent company for the first half was 2.028 billion yuan, up 48.34% year-on-year, with Q2 net profit of 1.162 billion yuan, up 43.58% year-on-year; the non-recurring net profit for the first half was 1.951 billion yuan, up 42.21% year-on-year, with Q2 non-recurring net profit of 1.103 billion yuan, up 36.83% year-on-year.

In the first half, the gross margin was 30.48%, an increase of 4.59% year-on-year, and the net profit margin was 14.48%, a year-on-year growth of 28.63%, indicating a significant improvement in profitability. Total operating expenses were 602 million yuan, with the three expenses accounting for 4.32% of revenue, a year-on-year decrease of 14.57%, demonstrating effective cost control. The company attributes its performance growth to the continued penetration of image sensor products in automotive intelligent driving, panoramic, and action camera application markets, steadily expanding market share. The outstanding performance in revenue and profit in Q2 injects strong momentum for annual performance growth, making future developments worth watching.

This indicates that Q2 is a key node driving the acceleration of annual performance.

Product Advantages and Technical Capabilities

OmniVision’s core advantages are concentrated in the following areas:

Wide Coverage of Image Sensors: Covering applications from smartphones, panoramic photography, action cameras to automotive intelligent driving;Continuous Deep Market Penetration: Accelerated shipments in emerging fields such as automotive, sports, and panoramic photography inject strong growth momentum into performance;Smooth Brand Upgrade Transition: The transition from Will Semiconductor to OmniVision Group helps build a more international and professional image;

Overall, broad technical coverage and clear application paths are fundamental guarantees for its continuous performance improvement.

Industry Competitors and Market Position Comparison

In the CIS (image sensor) field, OmniVision faces major global manufacturers such as Sony and ON Semiconductor, while also competing with domestic rivals like Huawei HiSilicon and Jinghe Integrated:

International Giantshave advantages in technology and production capacity, but their high-end positioning leads to disadvantages in pricing and local supply chain;Domestic Peersare similar in market, but OmniVision has seized opportunities in multiple emerging application fields (such as panoramic and action cameras), with a more forward-looking technology and market layout;

Overall, OmniVision maintains a leading position in several niche markets, and its synergy within the domestic ecosystem adds to its strengths.

Brief Risk Factors Reminder

Despite strong performance, attention should still be paid to the following risks:

Market Demand Fluctuations: If demand in the consumer electronics or automotive sectors slows, it may affect sensor shipments and order rhythms.Rapid Technological Iteration: If competitors achieve breakthroughs in pixel, power consumption, or packaging, it may intensify competitive pressure.High Proportion of Overseas Customers: Exchange rate fluctuations or international trade policies may affect revenue stability.

While these factors exist, they have not significantly impacted the overall performance trend of the company.

Full Summary

Overall:

In 2024, OmniVision’s shipments continue to increase, solidifying its industry position and building momentum for future growth.Q1 2025, revenue reached 6.472 billion yuan and net profit 866 million yuan, both achieving strong growth.First Half of 2025/Q2, revenue reached 13.7–14 billion yuan, net profit 1.9–2 billion yuan, with Q2 making a significant contribution, being the main driver of accelerated growth.Core Advantageslie in the wide application scenarios of image sensors, expansion of emerging markets, and brand upgrades.Industry Positionis among the leading domestic CIS players, with manageable competitive pressure.Risksare mainly concentrated on demand changes and technological substitutions, but the current status is stable.