Core Summary of the 2025 China MCU Industry Chain Map and Investment Layout

This article is based on data from the Semiconductor Industry Research Institute, providing a comprehensive analysis of the 2025 China MCU (Microcontroller Unit, a core component of embedded systems that integrates CPU, memory, and I/O interfaces, applied in automotive electronics, smart home, and other fields) industry landscape from the perspectives of industry chain structure, market scale of each link, key enterprises, and downstream applications.

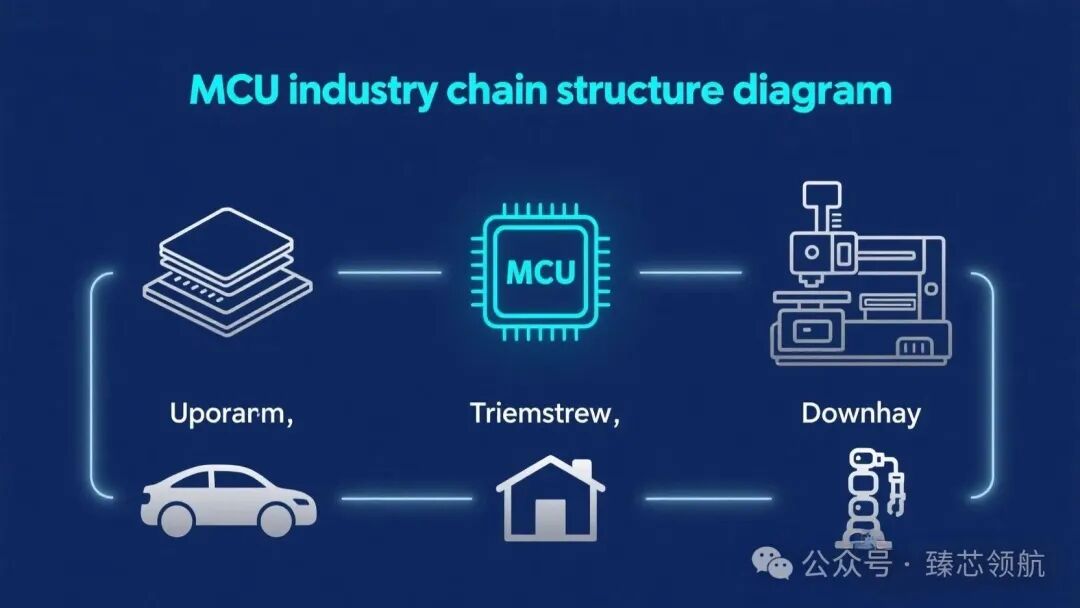

1. MCU Industry Chain Overview

The MCU industry chain is divided into three core segments: upstream, midstream, and downstream, with the specific structure as follows:

Upstream: Mainly includes two categories: materials and equipment. The materials sector covers silicon wafers, photoresists, wet electronic chemicals, packaging materials, photomasks, sputtering targets, etc.; the equipment sector includes photolithography machines, etching machines, thin film deposition equipment, coating and developing equipment, single crystal furnaces, ion implantation equipment, etc.

Midstream: Comprises MCU manufacturers, mainly divided into two types—IDM manufacturers (such as Renesas Electronics, Infineon, NXP, STMicroelectronics, China Resources Microelectronics, Silan Microelectronics, etc.) and Fabless manufacturers (such as Zhongying Electronics, Espressif Technology, Shengxi Microelectronics, GigaDevice, Shanghai Belling, Neusoft Carrier, etc.).

Downstream: The application fields are extensive, covering automotive electronics, consumer electronics, smart home, industrial control, computer networks, and more.

2. Upstream of the Industry Chain: Materials and Equipment—Accelerating Domestic Substitution, Continuous Expansion of Scale

1. Core Materials

(1) Semiconductor Silicon Wafers

Market Size: Predicted to reach 14.6 billion yuan by 2025, with the market size increasing from 7.71 billion yuan in 2019 to 12.33 billion yuan in 2023, an average annual compound growth rate of 12.45%, and approximately 13.1 billion yuan in 2024.

Key Enterprises and Competitive Landscape: Leading domestic companies include Shanghai Silicon Industry, Lianhe Technology, TCL Zhonghuan, Zhongjing Technology, Yangjie Technology, and Yuyuan Silicon. Among them, Shanghai Silicon Industry’s total production capacity of 300mm semiconductor silicon wafers reached 450,000 pieces/month by the end of 2023, expected to increase to 600,000 pieces/month in 2024; Lianhe Technology has a complete layout for 6-12 inch polished wafers and epitaxial wafers; TCL Zhonghuan has already produced and shipped 8-12 inch semiconductor silicon wafers. Currently, domestic manufacturers still have gaps in market share, technology processes, and yield rates compared to international advanced levels, but due to capacity demand gaps and supply security considerations, the industry is in a rapid development phase.

(2) Photoresists

Market Size: Predicted to reach 12.3 billion yuan by 2025, approximately 10.92 billion yuan in 2023, and about 11.44 billion yuan in 2024; the global market has reached a scale of over 10 billion US dollars.

Key Enterprises and Competitive Landscape: Semiconductor photoresist technology is the most advanced, with the market mainly dominated by international giants such as JSR, Tokyo Ohka, Shin-Etsu, DuPont, and Fujifilm. Among domestic companies, Nanda Optoelectronics’ self-developed 193nm ArF photoresist passed customer certification in December 2020 and achieved breakthroughs at the 55nm technology node in May 2021; Beijing Kehua, Jingrui Electronic Materials, Suzhou Ruihong, and Tongcheng New Materials are also continuously laying out in g-line/i-line, KrF, and other photoresist fields. In addition, in the PCB photoresist and panel display photoresist fields, domestic companies occupy a certain market share in subcategories such as wet films, solder mask inks, and color photoresists.

(3) Wet Electronic Chemicals

Industry Trend: The industry’s development is highly dependent on technological breakthroughs and penetration into high-end markets. Companies capable of mass-producing ultra-high purity products and certified by leading wafer manufacturers have greater growth potential, and the domestic substitution process brings structural opportunities to the industry.

Key Enterprises: The top five companies with development potential in 2025 are Jianghua Micro (comprehensive product line, high recognition among semiconductor and display panel customers), Jingrui Electronic Materials (bulk supply of semiconductor-grade products to leading customers), Shanghai Xinyang (deeply engaged in plating solutions for packaging, with smooth progress in wafer manufacturing chemicals), Anji Technology (leading CMP polishing liquid technology, a main force in domestic substitution), and Huate Gas (leading in electronic specialty gases, with a high number of customer certifications). Additionally, companies like Juhua Co., Ltd., DuPont, and Zhongjuxin also have competitive advantages in specific product areas.

2. Semiconductor Equipment

Market Size: Predicted to reach 230 billion yuan by 2025, approximately 219.02 billion yuan in 2023 (accounting for 35% of the global market share), and about 223 billion yuan in 2024.

Key Enterprises and Capacity Layout: Semiconductor equipment has high technical barriers and long R&D cycles, making it a key link in the industry chain. The main enterprises and their predicted capacities for 2025 are as follows:

1. North Huachuang: 500 etching machines/year, 400 thin film equipment/year, covering all process equipment for 28nm and above logic chips and memory chips, with technical directions including 12-inch high-energy ion implanters and ALD atomic layer deposition equipment.

2. Zhongwei Company: 400 etching machines/year, 200 MOCVD machines/year, mass production of etching machines for advanced processes below 5nm, deepening the Mini/Micro LED equipment market.

3. Haiwei Electronics: 50 photolithography machines/year (including SSA800/10), mass production of 28nm DUV photolithography machines, and layout breakthroughs in KrF/A light source technology.

4. TuoJing Technology: 300 thin film equipment/year (mainly PECVD), achieving domestic substitution for 12-inch PECVD equipment, and laying out ALD and SACVD technologies.

5. Xinyuan Micro: 400 coating and developing equipment/year, mass production of front-end I-line/KrF equipment, and an increasing proportion of advanced packaging equipment in the back-end.

3. Midstream of the Industry Chain: MCU Manufacturers—Strong Market Growth, Automotive-grade Becomes Core Track

1. Market Size

Global Market: Driven by demand from automotive and industrial AIoT, the scale reached 30.9 billion US dollars in 2023, approximately 33.8 billion US dollars in 2024, and predicted to increase to 37 billion US dollars in 2025.

China Market: Against the backdrop of domestic substitution and chip shortages, the market size is expected to reach 62.51 billion yuan in 2024 (an increase of 8.64% year-on-year) and 65.64 billion yuan in 2025; the domestic production of mid-to-low-end MCUs has been completed and is continuously penetrating into high-end fields.

2. Core Data of Automotive-grade MCUs

Demand per Vehicle: Traditional fuel vehicles average 70 units, luxury fuel vehicles average 150 units, and smart vehicles average 300 units due to the demand for smart cockpits and autonomous driving (4.3 times that of traditional fuel vehicles).

Market Size: The Chinese automotive MCU market is expected to reach 26.8 billion yuan in 2024 (an increase of 3.47% year-on-year) and predicted to increase to 29.4 billion yuan in 2025; MCUs are core components of automotive electronic control units (ECUs).

3. Core Competitiveness of Enterprises and Distribution of Listed Companies

Top 3 Core Competitiveness Enterprises:

1. GigaDevice: The leading domestic market share in MCUs, with a product line covering general to high-performance products, automotive-grade MCUs certified and entering the supply chain of leading automotive companies, providing integrated solutions with memory chips and MCUs.

2. Espressif Technology: Leading global market share in IoT WiFi/Bluetooth MCUs, with the ESP32 series widely used in smart homes, self-developed RISC-V architecture reducing costs, and a strong ecosystem of open-source development frameworks.

3. Zhongying Electronics: Leading domestic market share in white goods MCUs, core supplier for Midea and Gree, breakthroughs in variable frequency motor control technology, entering the fields of new energy vehicles and robotic joint control.

Distribution of Listed Companies: There are a total of 80 listed companies related to MCUs in China’s A-share market, with 20 in Guangdong Province (the most), followed by 19 in Shanghai and 10 in Beijing; the top three companies by revenue in the first half of 2025 are Midea Group (251.12 billion yuan), Gree Electric (97.32 billion yuan), and Great Wall Motors (92.33 billion yuan).

4. Downstream of the Industry Chain: Application Fields—Automotive Electronics Lead, Smart Home Growth Expected

1. Automotive Electronics

Market Size: Approximately 1.2174 trillion yuan in 2024 (an increase of 10.95% year-on-year), predicted to reach 1.2783 trillion yuan in 2025.

Development Trend: China is the world’s largest producer and consumer of automobiles and new energy vehicles, with demand for automotive electronics continuously increasing alongside the trends of intelligence and electrification, becoming the core driving field for MCUs downstream.

2. Mobile Phones

Market Status: The market is nearing saturation, with demand continuing to weaken. In June 2025, domestic mobile phone shipments reached 22.598 million units (a year-on-year decrease of 9.3%), with cumulative shipments of 141 million units from January to June 2025 (a year-on-year decrease of 3.9%).

3. Smart Home

Market Size: Approximately 876.74 billion yuan in 2024 (penetration rate of 14.5%), predicted to reach 945 billion yuan in 2025.

Development Trend: Breakthroughs in AI and 5G technology are enhancing consumer awareness, with some explosive products releasing demand, becoming a field with significant growth potential for MCUs downstream.

5. Core Conclusions

1. The 2025 China MCU industry chain presents a pattern of “accelerated domestic substitution in the upstream, breakthroughs in automotive-grade in the midstream, and automotive electronics leading downstream,” with the overall market size continuously expanding, driven by automotive intelligence, industrial AIoT, and domestic substitution.

2. The core competitiveness of enterprises focuses on three major directions: ecosystem construction of architectures like RISC-V, breakthroughs in high-reliability certification for automotive-grade, and the collaborative integration capability of “MCU + memory/security/analog chips”; high-end industrial control and automotive electronics are key breakthrough areas for the future.